Debt Collector Phone Call: When to Answer and What to Ask

Need Help Reviewing Your Account?

Contact UsGetting a call from a debt collector can be stressful. You see an unknown number and immediately wonder, should you answer, ignore it, or let it go to voicemail? Many people feel anxious or unsure about what to do next, and that is completely normal.

Avoiding the call might seem easier in the moment, but it can make things more confusing later. According to a 2025 report from the Consumer Financial Protection Bureau (CFPB), one in four consumers was contacted by a debt collector in 2023. Most debtors are unaware of how to respond or what their rights are.

This guide will help you handle those debt collector phone calls with confidence. You will learn when to answer, what to ask, and how to protect yourself while taking steady steps toward financial control.

Brief breakdown:

- Under the FDCPA and CFPB’s Regulation F, collectors cannot contact you more than seven times within seven days about the same debt. If they do, you may be dealing with harassment or a compliance issue.

- Never send money until you receive a written validation notice that confirms the debt amount, original creditor, and your rights to dispute it. This simple step can protect you from scams and mistaken collections.

- The law prohibits collectors from using threats, harassment, or false statements. You can request that they stop contacting you and report violations to the Consumer Financial Protection Bureau (CFPB) or your state attorney general.

- Be alert for callers demanding instant payment, refusing to share company details, or threatening arrest or lawsuits. Real collectors follow the law, while scammers pressure you to act fast.

- Maintain records of all communications, including dates, names, and payment confirmations. Documentation helps you dispute errors, prove payments, and protect yourself in case of future confusion.

When to Answer a Debt Collector Call?

Getting a call about debt can feel overwhelming. You may not even know who the collector is or whether the debt is legitimate. Still, avoiding every call is not always the best solution.

Ignoring repeated contact can lead to more stress, missed information, or even letters escalating the matter. The key is to know when it makes sense to answer—and when it is smarter to wait.

Here are a few helpful pointers to guide your decision:

- Answer When You Expect Contact: If you have recently received a letter or email about a debt, or if you are aware of an account in collections, answering the call can help clarify details more quickly.

- Let It Go to Voicemail If You Need Time: If you are unsure who is calling or want to gather documents first, it is okay to let it ring. Listen to the voicemail, note the name, company, and callback number, and verify their identity before responding.

- Stay Calm and Take Notes: If you do answer, keep the conversation brief and concise. Write down the collector’s name, agency, date, and any amounts mentioned. You have the right to request all information in writing.

- Remember Your Legal Rights: Under the Fair Debt Collection Practices Act (FDCPA), collectors cannot threaten, use abusive language, or contact you before 8 a.m. or after 9 p.m. They also cannot discuss your debt with anyone else.

- Do Not Share Sensitive Details: Never confirm bank account information, employment details, or make a payment over the phone until the debt is verified in writing.

Sometimes, just knowing your rights can make these calls far less intimidating. It is best to enter a call prepared. The next section covers the things you should ask when a debt collector calls, so you can take control of the conversation from the start.

Suggested Read: How to Effectively Manage and Reduce Debt

Questions That Protect You During a Debt Collector Call

When a debt collector contacts you, your best course of action is to ask clear, direct questions. These help you confirm who you are speaking with, understand what they are claiming you owe, and protect yourself from incorrect or unfair practices.

Under the law, legitimate debt collectors must provide certain information. Asking the following questions puts you in control:

1. “Could You Provide Your Full Name, Company Name, and Contact Information?”

You should ask this first because it verifies the caller’s identity and establishes accountability. According to the Fair Debt Collection Practices Act (FDCPA), debt collectors must clearly identify themselves and state that they are attempting to collect a debt.

2. “Which Debt Are You Contacting Me About, and Who Was the Original Creditor?”

Requesting these details ensures you know exactly which account the collector is referencing—and whether it is legitimate. The collector should provide the amount owed, the name of the original creditor, and relevant dates such as the date of the last payment. This aligns with your right under the FDCPA to receive verification of the debt.

3. “Can You Send Me a Written Validation Notice of the Debt?”

Requesting a validation notice means you are asking for the claim in writing before making any commitments. Under FDCPA § 809 (15 U.S.C. § 1692g), the collector must provide this notice within five days of first contact, outlining how much you owe, who you owe it to, and how to dispute it.

4. “What Are My Repayment, Settlement, or Installment Options?”

Once you establish that the debt is valid and the caller is legitimate, you are entitled to explore your options. Asking this gives you the opportunity to negotiate a manageable plan rather than reacting under pressure or agreeing to terms that do not fit your budget.

5. “How Did You Obtain My Contact Information?”

This question helps you verify that the collector obtained your details through legitimate channels. If the caller hesitates or gives an unclear answer, it could be a red flag. The FDCPA prohibits deceptive practices in collection efforts.

When speaking with a debt collector, asking the right questions can help you protect your rights and avoid unnecessary stress.

Forest Hill Management encourages consumers to request written validation of the debt, understand available repayment options, and confirm the legitimacy of the account before making any commitments. Our team is trained to provide clear, compliant answers that support informed decision-making and long-term financial resolution.

We understand that by asking these questions, you stay informed and protect your financial and personal information. Now that you know what to ask, the next step is how to respond during the call—so you remain calm, informed, and protected.

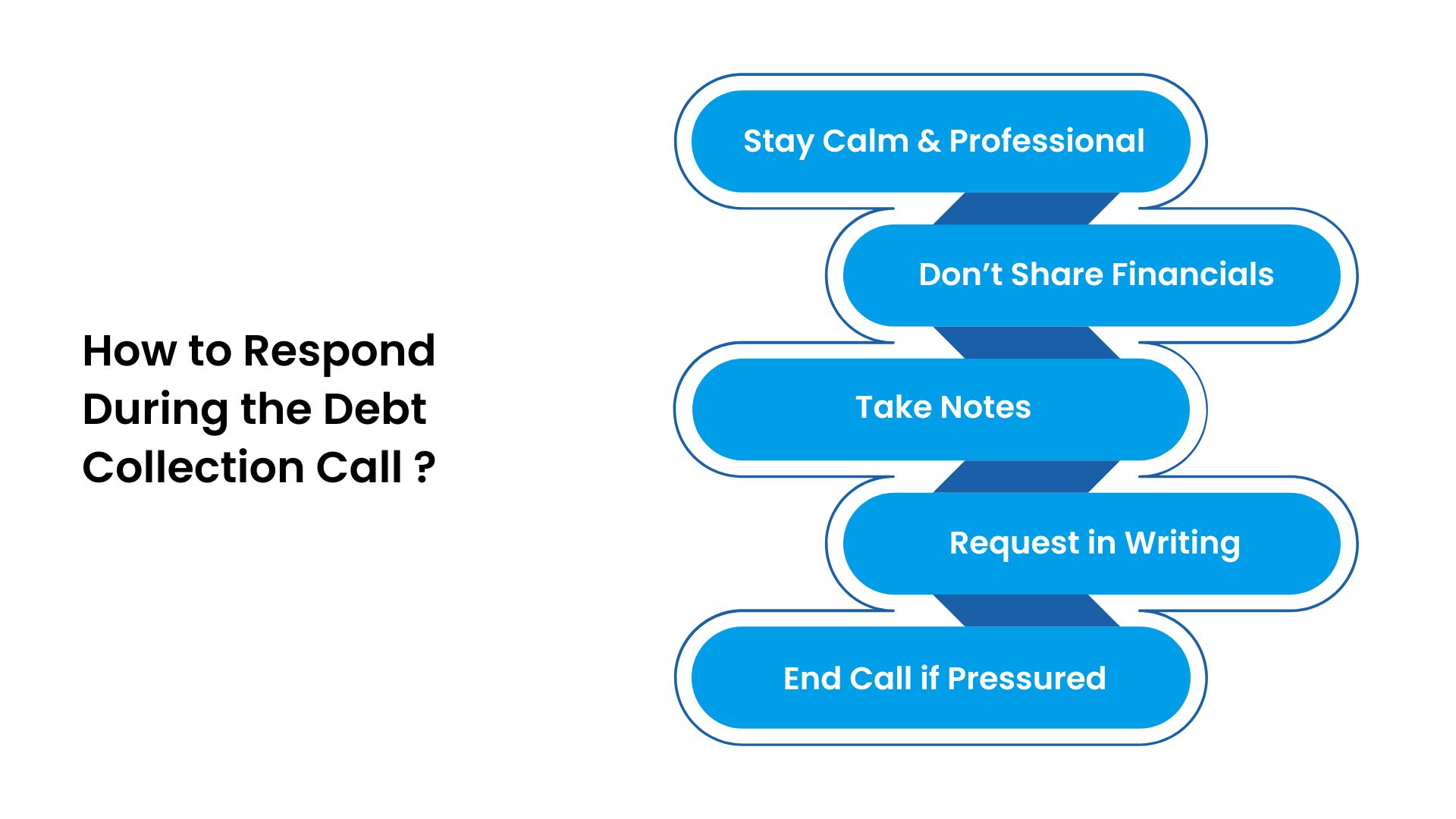

How to Respond During the Debt Collection Call

Even when you know what to ask, the way you respond during a debt collection call can make a significant difference. Remaining calm, focused, and polite allows you to maintain control of the conversation and protect your rights under the FDCPA.

Remember, you do not have to share personal or financial details until the debt has been verified. These are a few other things to remember on the call:

- Stay Calm and Professional: Debt collectors are trained communicators. Responding emotionally can work against you. Keep the conversation factual and short, and avoid arguments or admissions of guilt.

- Do Not Disclose Financial Details: Never share your bank account, credit card number, or other sensitive information until you have received written verification of the debt.

- Take Notes: Record the caller’s name, company, date, time, and any key statements made. This information can be useful if you need to dispute the debt or report misconduct later.

- Ask for Written Communication: You have the right to request that the collector contact you in writing only. This ensures that you have a paper trail and limits unwanted phone calls.

- End the Call If You Feel Pressured: If the caller becomes aggressive or refuses to provide information, politely end the conversation. You can always reconnect once you have received the necessary details.

If the caller is pressuring you to make an immediate payment, share personal details, or refuses to send written proof of the debt, it is probably a scam.

Once the call ends, your next steps matter just as much. Knowing what to do after the conversation can help you verify the debt, protect your credit, and avoid potential scams.

Next Steps After Speaking with a Debt Collector

Debt collection is a regulated process, and your post-call actions can determine whether the resolution is fair, accurate, and sustainable. Even if the conversation felt rushed or unclear, you still have time to take control.

Before you make any payments or commitments, take these steps to protect yourself and move forward with confidence:

1. Request Written Validation

Verifying debt in writing gives you clarity about who is collecting and exactly how much you owe. Under the Fair Debt Collection Practices Act (FDCPA) § 809, you have the right to receive a validation notice within five days of initial contact.

You should:

- Ask the collector to mail or email you the validation notice; do not make payment until you receive it.

- Verify it includes the creditor name, the amount owed, your rights to dispute, and a deadline for response.

- Save the validation notice and reference it in all future communications.

2. Check Your Credit Report

Reviewing your credit report allows you to confirm whether the debt is listed and whether the details match what the collector reports.

According to the Federal Trade Commission (FTC), “Your credit report is an important part of your financial life,” and checking it regularly helps you spot errors or fraud.

Visit AnnualCreditReport.com to get your free report from each bureau. It is the official website authorized by federal law where you can request free credit reports from Equifax, Experian, and TransUnion once every 12 months. It’s operated jointly by the three major credit bureaus and overseen by the Federal Trade Commission (FTC).

You need to:

- Check for account number, balance, and last payment date.

- Compare the debt collector’s details — original creditor, amount, date — with your report.

- If you see an account you do not recognize, suspect fraud, or find mismatches, file a dispute.

3. Compare Records and Document Everything

Aligning what the collector says with your records provides a clear audit trail and helps you identify and correct errors or fraud. Keep detailed documentation of times, names, dates, and notes. This strengthens your position if you need to challenge a collector later.

You should also:

- Maintain a log of the call, including the date, time, agent's name, agency, reference number, and a summary of the discussion.

- Collect supporting documents: past statements, payment history, debt transfers, and emails.

- Store all correspondence in one place (digital or physical) and reference it in future communications.

4. Avoid Immediate Payments Until Verified

Making a payment before verifying the debt may limit your rights and make it harder to dispute incorrect information. Taking time to verify ensures you are paying the correct account under fair terms.

These are a few things to take care of:

- Do not provide your bank account numbers or routing numbers, and refrain from making payments until you confirm the debt.

- Ask for the payment terms in writing (installment plan, settlement offer, required amount).

- Check whether payment will reset the statute of limitations (especially if the debt is older) before you commit.

Even when a debt collector follows the rules, not every call is legitimate, and not every tactic is compliant. As you review what was said or prepare for future conversations, it’s critical to recognize the warning signs that may indicate misrepresentation, harassment, or fraud.

Suggested Read: How Does Debt Consolidation Affect Your Credit Score?

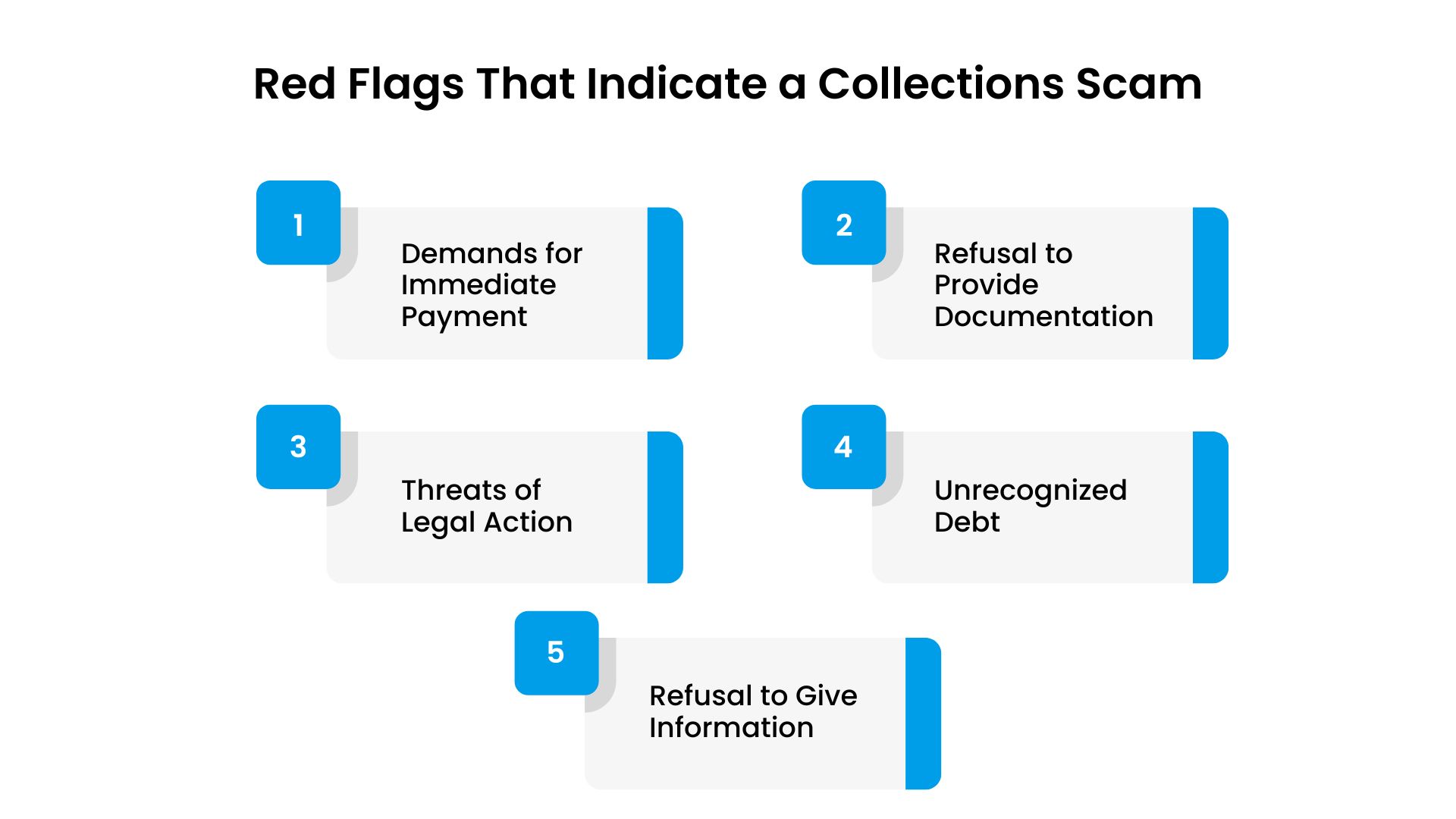

Red Flags That Indicate a Collections Scam

Debt collection scams are rising fast—and so are consumer complaints. According to The Hill, the Federal Trade Commission received over 140,000 complaints about debt collection in Q2 2025, a 220% increase from the same period in 2024. Meanwhile, reported consumer losses to fraud exceeded $12.5 billion in 2024, up 25% year over year.

If a debt-related call feels rushed, vague, or aggressive, those aren’t just uncomfortable moments—they could be signs of a scam. These are specific red flags to watch for, along with guidance on how to respond if something doesn’t feel right.

1. Demands for Immediate Payment

If the caller demands payment right away and insists on methods like gift cards, prepaid cards, wire transfers, or cryptocurrency, that is a major warning sign. Legitimate collectors will provide you with time and written verification before requesting payment.

2. Refusal to Provide Documentation

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to a validation notice that explains the debt’s origin, amount owed, and your rights. If the caller refuses or delays providing such a notice, treat it with caution.

3. Caller Threatens Legal Action

Scammers often use fear tactics like threatening arrest, jail, or immediate legal action — even though most legitimate collectors must first sue you in court and send proper documentation. If they skip that step and go straight to threats, it may be a scam.

4. You Do Not Recognize the Debt

If you have no memory of the debt, it is for an account you closed years ago, or the statute of limitations has passed — these are signs the caller might be pursuing a debt you do not legally owe. Real collectors will provide proof of the debt’s validity, the date of the last payment, and the original creditor.

5. Caller Refuses to Give Information

A legitimate agency should have no trouble giving you its full business name, physical address, and a callback number. If they are evasive or refuse to cooperate, they may be trying to evade detection once you question them.

Steps to Take if the Caller Seems Fake

If the caller resists basic transparency, you have every reason to pause and protect yourself. Here’s what to do if you suspect the call isn’t legitimate.

- Immediately hang up and do not provide any personal or financial information.

- Request all information in writing first. Send a written request for debt validation to the agency supposedly collecting the debt.

- You may consider reporting the incident to the Federal Trade Commission (FTC) or your state attorney general’s office.

Forest Hill Management encourages consumers to remain vigilant for common red flags during debt collection calls, particularly as scam activity continues to increase. Our representatives provide clear, compliant information that will never pressure you into immediate payment decisions. Instead, we focus on transparency, written documentation, and flexible repayment plans that fit your financial situation.

If a caller refuses to provide basic information or pushes you to act fast, it’s worth stepping back and verifying before you proceed.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

Regulations That Protect Debtors from Collection Scams

Federal and state laws clearly outline what debt collectors can and cannot do, ensuring that you are treated fairly throughout the process. Knowing these laws helps you recognize when a collector has crossed the line and gives you the power to act confidently.

You should be aware of the following statutes:

- Fair Debt Collection Practices Act (FDCPA), 15 U.S.C. §§ 1692–1692p

- This is the most important federal law governing debt collection. It prohibits harassment, false statements, and unfair practices. Collectors cannot call before 8 a.m. or after 9 p.m., threaten legal action they cannot take, or contact your employer about your debt without consent.

- Fair Credit Reporting Act (FCRA), 15 U.S.C. § 1681

- This law ensures accuracy and privacy in how your debt is reported to credit bureaus. If a collector reports false or outdated information, you have the right to dispute and request correction within 30 days.

- Telephone Consumer Protection Act (TCPA), 47 U.S.C. § 227

- The TCPA limits automated calls and text messages from collectors. It also allows consumers to revoke consent for robocalls and provides for damages if collectors continue to violate the rule.

- Consumer Financial Protection Bureau (CFPB) Regulation F

- Effective since November 2021, Regulation F expanded the FDCPA by setting clear rules for call frequency, digital communications, and debt validation notices. Collectors cannot call you more than seven times in a seven-day period about the same debt.

- State-Level Debt Collection Laws

- Many states, such as California (Rosenthal Fair Debt Collection Practices Act) and New York (Debt Collection Fair Practices Act), add further protections. This is in the form of stricter licensing and stronger penalties for harassment.

Staying alert and aware of your rights is key to protecting yourself. Yet, even with the best intentions, many consumers make mistakes that slow or derail their progress toward debt resolution. The next section examines the mistakes consumers make during debt collector phone calls.

Suggested Read: Is Paying Debt Collection Agencies a Bad Idea?

Errors That Can Hurt Your Debt Resolution

Some of these errors come from confusion, while others happen because debt collectors and creditors work within complex systems. Understanding these common mistakes and how to correct them can save you money, time, and stress.

Table showing the common mistakes consumers make:

When you understand what to avoid, you protect both your credit and your confidence. Taking small, consistent steps toward accuracy and transparency can make your debt resolution smoother and more sustainable.

Quick Tips to Stay Ahead:

- Keep a Debt Journal: Note every call, payment, and agreement for quick reference.

- Set Up Calendar Alerts: Remind yourself of payment due dates and review periods.

- Educate Yourself: Follow updates from the CFPB to stay informed about your rights.

- Protect Personal Data: Never share Social Security or bank information unless you confirm the collector’s legitimacy.

Reliable, professional guidance can make the debt resolution process less stressful. In the next section, you will learn how Forest Hill Management supports consumers through every step of the process and what you can expect when you engage with their team.

Suggested Read: A Beginner’s Guide to Debt Management Strategies

Resolve Debt Without Added Stress with Us

At Forest Hill Management, we understand that debt can weigh heavily on your mind, especially when you are already doing your best to manage day-to-day expenses. Our goal is to make the debt resolution process transparent, respectful, and stress-free.

We focus on clear communication, secure systems, and personalized support so that you can take control of your finances with confidence. Our services include:

- Personalized Repayment Options

Every individual’s financial situation is different. We help you explore custom payment plans and settlement options that match your ability to pay — without pressure or judgment.

- Helpful and Respectful Communication

From balance verification to written documentation, our team ensures you understand every part of your debt. We provide clear explanations, flexible timelines, and ongoing assistance throughout your repayment plan.

- Secure Online Payment Portal

Our encrypted online payment system allows you to make payments conveniently and securely. This minimizes the risk of fraud and ensures that your personal data remains protected at all times.

- Empathetic Consumer Assistance

Our representatives are trained to engage respectfully, answer your questions clearly, and help you stay informed. You will never face harassment, misleading language, or hidden terms.

- Compliance and Transparency

We strictly follow all federal and state regulations, ensuring that your experience with us is fair, compliant, and easy to understand.

At Forest Hill Management, we believe debt resolution should be a collaborative process, not a confrontation. We work with you, step by step, to bring your account to good standing while supporting your

Conclusion

Falling for a debt collection scam can do more than cost you money. It can also damage your credit, confidence, and peace of mind. Staying informed, verifying every detail, and knowing your rights are your best defenses against potential issues. With the right knowledge and vigilance, you can take control of your financial situation instead of letting fear or confusion guide your decisions.

At Forest Hill Management, we are committed to helping consumers handle their debts responsibly, safely, and respectfully. Our team focuses on transparency, compliance, and compassion, making sure every step you take toward resolution brings you closer to greater financial clarity.

Take charge of your debt today. Contact us to verify your account, explore personalized repayment options, or reach out to our team for assistance.

Frequently Asked Questions

1. How Often Can a Debt Collector Call Me?

Under the CFPB’s Regulation F, a debt collector cannot call you more than seven times within seven consecutive days about the same debt. If they exceed that limit, it may be a violation of the Fair Debt Collection Practices Act (FDCPA).

2. What Should I Say If I Do Not Recognize the Debt?

Stay calm and do not confirm or deny the debt right away. Instead, ask for a written validation notice and review it against your records before taking any action.

3. Can a Collector Leave Voicemails or Text Messages?

Yes, but only under specific conditions. The “limited-content message” rule introduced by the CFPB in Regulation F allows collectors to leave brief, non-threatening messages that do not disclose sensitive information to others.

4. What Does the “11-Word Rule” Mean in Debt Collection?

It refers to a sample phrase often used by consumers to assert their rights: “Please cease and desist all calls and contact immediately.” Once you make this request in writing, collectors must stop most forms of contact under the FDCPA.

This phrase is commonly shared online but is not an official legal term. Consumers can, however, submit written requests limiting communication under the FDCPA.

5. What Should I Do If I Suspect a Scam Call?

Hang up immediately and avoid giving any personal or banking details. Then, verify the debt through written communication or by contacting the original creditor before making payments.