A Beginner’s Guide to Debt Management Strategies

Transform Your Financial Future

Contact UsFeeling a knot in your stomach every time the phone rings? Do you find yourself avoiding the mail, knowing another bill is waiting inside? If the constant pressure of unpaid bills and looming financial stress feels overwhelming, you are not alone. It’s a reality faced by millions, and it can feel like a maze with no way out.

But what if there was a path? Not just to pay off debt, but to reclaim your peace of mind. Debt management is more than just a financial strategy; it's a step toward a calmer, more secure future, where you regain financial control.

This guide is your first step to understanding what debt management is and how to find a solution that works for you.

Key Takeaways

- Debt management is a proactive strategy to simplify payments, reduce financial stress, and regain control over your money.

- You can start with DIY methods like creating a budget and using the debt snowball or avalanche strategy for smaller debts.

- For overwhelming debt, a Debt Management Plan (DMP) can combine your bills into one affordable payment and lower your interest rates.

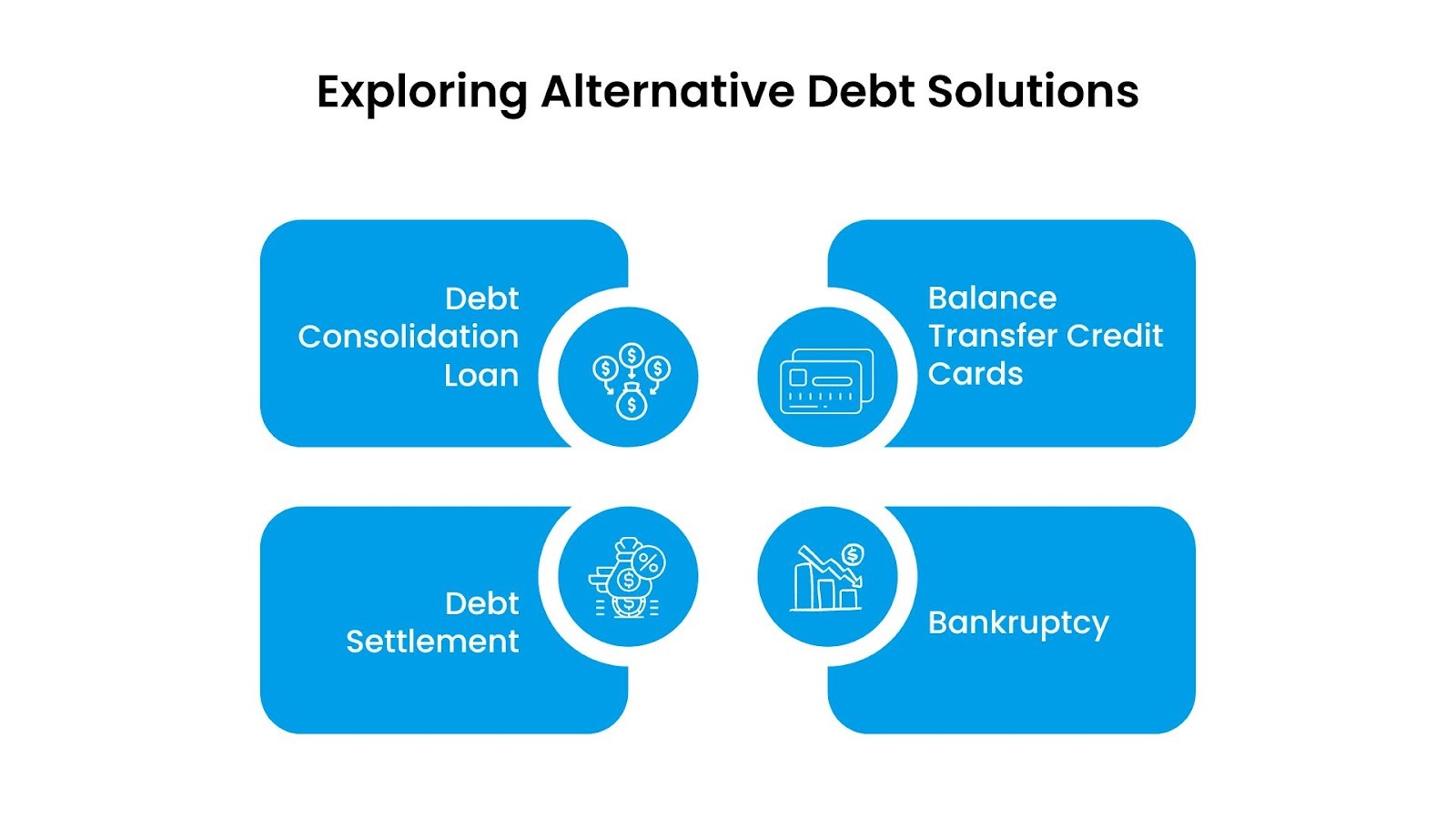

- Alternative options like debt consolidation, debt settlement, and bankruptcy each have different risks and benefits.

- The right strategy is personal; the goal is to choose a path that helps you become debt-free and regain financial control.

What Is Debt Management?

Managing debt means taking a proactive role in your finances to simplify payments and reduce what you owe. It’s a purposeful plan to get out from under the pressure of bills and interest and onto a clear path toward financial freedom.

This isn't an issue that affects just a few people. The burden of debt is a widespread reality for many in the U.S., with total household debt reaching over $18 trillion as of late 2024.

Here’s why a debt management strategy is important:

- Regain control: A plan moves you from feeling helpless to being in charge of your financial situation.

- Reduce stress: It eliminates the chaos of juggling multiple payments and the worry of collection calls.

- Create a clear path forward: It gives you a structured way to become debt-free, often in a predictable timeframe.

- Improve financial health: By focusing on paying down debt, you can improve your credit score and build a more secure future.

This renewed sense of control often begins with a few straightforward, do-it-yourself strategies you can put into practice right away.

Suggested Read: How to Recover from Debt: A Simple Step-by-Step Guide

Your DIY Debt Management Strategies

A do-it-yourself (DIY) approach to debt is a personal plan you create and manage on your own. It requires discipline and effort, but it can be a powerful way to regain financial control. This approach involves a few key actions you can start today.

1. Take Stock of Your Debts

You can’t manage what you don’t know. The first step is to get a complete picture of your financial situation.

- List every debt: Include all credit cards, personal loans, medical bills, and any other outstanding balances.

- Note the details: For each debt, write down the total amount owed, the interest rate, and the minimum monthly payment.

2. Create a Realistic Budget

A budget isn't about telling you what you can't have. It's about giving you control over where your money goes. By creating a spending plan, you can find extra money to put toward debt repayment, even if it's just a small amount.

- List Your Income and Expenses: Start by listing all your sources of income and every single monthly expense, from rent and groceries to subscriptions and dining out.

- Find Room to Reduce: Look for areas where you can trim costs. Even small changes, like cutting an unused subscription, can add up.

- Allocate Money for Debt: Once you know where your money is going, dedicate a specific, consistent amount each month to paying down your debt.

3. Choose a Repayment Strategy

Once you've found money in your budget, the next step is deciding which debt to pay off first. Two of the most common strategies are the debt snowball and debt avalanche methods. Both are effective, but they work on different principles:

- The Debt Snowball Method: Focus on paying off your debts from the smallest balance to the largest. This method provides quick wins and the motivation to keep going.

- The Debt Avalanche Method: Focus on paying off the debt with the highest interest rate first. This approach saves you the most money on interest over time.

4. Negotiate with Creditors

You might be able to improve your terms just by asking. Many creditors are willing to work with you, especially if you've been a long-time customer.

- Be Prepared: Before you call, have your account number and a clear explanation of your situation ready. Stay calm and polite throughout the conversation.

- Know What to Ask for: You can request a lower interest rate, a temporary hardship plan that reduces or pauses your payments, or the waiver of a late fee. Remember, the worst they can say is no.

5. Increase Your Income

Finding a way to bring in more money, even for a short time, can significantly accelerate your debt-free journey.

- Take on a Side Gig: Look for flexible jobs in the gig economy, such as driving for a rideshare service, delivering food, pet sitting, or tutoring online.

- Sell What You Don't Need: Clear out your home and sell unused items on online marketplaces like eBay or Facebook Marketplace. You could also sell unused gift cards for cash.

- Request a Raise: If your workplace has performed well or your responsibilities have increased, gather your accomplishments and make a compelling case for a raise at your current job.

For some, however, the sheer amount of debt makes a DIY approach feel impossible, and that’s when a debt management plan becomes an ideal strategy.

Suggested Read: What Happens if You Miss a Payment on Consumer Easy Credit?

When a Debt Management Plan (DMP) Is the Ideal Strategy

Administered by non-profit credit counseling agencies, a Debt Management Plan is a structured repayment program designed to help you get out of debt. It’s an effective way to simplify your debt and work toward paying it off in a predictable timeframe without the risk of a new loan.

How Does a DMP Work?

A Debt Management Plan consolidates all your payments into one. The process is straightforward, and it's designed to provide you with immediate relief from the burden of juggling multiple bills.

- Consult with an Expert: You have a confidential conversation with a certified credit counselor to review your finances and determine if a DMP is the right fit for you.

- Negotiations on Your Behalf: The agency works with your creditors in an effort to reduce your interest rates and waive late fees.

- One Simple Payment: All your eligible unsecured debts, like credit cards and medical bills, are combined into one single, affordable monthly payment.

- The Agency Handles the Rest: Each month, you will send a single payment to the credit counseling agency, and the agency distributes the correct amounts to each of your creditors.

If a structured plan is what you're looking for, contact the advisors at The Forest Hill Management for personalized support. We have two decades of experience helping individuals with their financial journeys, providing comprehensive, tailored strategies to help you move toward a more secure future.

Pros and Cons of DMPs

It’s important to understand both the benefits and potential downsides of a DMP to decide if it's the right choice for your situation. Here’s a quick look at what you can expect.

Debt Management Plan — Pros & Cons

A quick comparison of the typical advantages and disadvantages of enrolling in a Debt Management Plan (DMP).

| Pros | Cons |

|---|---|

| Simplifies your bills and reduces the stress of juggling multiple due dates. | A DMP requires commitment and takes an average of 3–5 years to complete. |

| The agency's relationships with creditors often lead to significantly reduced interest rates. | You may be required to close your credit card accounts to enroll in the plan. |

| Creditors will stop calling you and direct all communication through the agency. | A DMP does not cover secured debts like mortgages or auto loans. |

| The plan provides a fixed end date, so you always know when your debt will be gone. | The plan only works if you can consistently afford the one monthly payment. |