Cost of Debt Formula: Calculate What You Really Pay

Need Help Reviewing Your Account?

Contact UsYou look at your balances, your interest rates, and your monthly payments, and it still feels unclear. How much is your debt actually costing you? Not just the payment due, but the real price of carrying those balances month after month. When money already feels tight, uncertainty like this adds another layer of stress.

That's where understanding the cost of debt formula helps. It turns scattered numbers into one clear percentage, so you can see the full picture instead of guessing. Once you know that number, decisions about payments, priorities, and next steps start to feel more manageable and less overwhelming.

Although the cost of debt formula comes from corporate finance theory, this guide focuses on how it applies to people managing real balances such as credit cards, personal loans, and account obligations.

Key Takeaways

- The cost of debt formula shows the effective percentage your borrowing carries, giving one clear number behind multiple balances.

- A basic cost of debt calculation uses interest actually paid, not just advertised rates, to reflect the real cost of carrying debt.

- The before-tax cost of debt formula shows what borrowing costs right now, while the after-tax cost of debt formula appears more often in financial modeling contexts.

- Looking at all debts together helps when determining the cost of debt across credit cards, loans, and other balances.

- Understanding the cost of debt equation turns scattered figures into a clearer picture of how interest is affecting your overall financial situation.

The Cost of Debt Formula

When balances stretch across different accounts, it's easy to lose track of what borrowing is really costing you. The cost of debt formula pulls everything into one clear percentage, so you can see the true rate behind the numbers on your statements.

Basic Cost of Debt Formula (Before Tax)

This is the most direct way to calculate the pretax cost of debt and understand your current borrowing cost.

Formula: Pre-Tax Cost of Debt = Annual Interest Expense ÷ Total Debt

Because balances change over time, this calculation is best viewed as an estimate rather than a precision metric.

What does this mean in plain terms?

You add up the interest you actually paid over a year and divide it by everything you owe. The result is the blended rate your debt is costing you right now.

Key points

- Uses interest actually charged, not just advertised APRs

- Works across loans, credit cards, and other borrowing

- Gives a real-world snapshot of your current cost of debt calculation

- Helpful when determining the cost of debt across multiple accounts

After-Tax Cost of Debt Formula (Academic Context)

You may encounter a second version of the cost of debt formula in finance literature:

After-Tax Cost of Debt = Pre-Tax Cost × (1 − Tax Rate)

Why is this formula mentioned?

This version exists mainly in academic and corporate finance contexts, where borrowing costs are adjusted for tax treatment. For most personal debt situations, it serves as background theory rather than a practical calculation.

Important context for you:

- Seen primarily in business finance and textbooks

- Used in company-level financial analysis

- Personal interest deductions are limited or situation-specific

- Not a direct measure of what your debt costs today

Which Version Matters for People Managing Debt?

Seeing two versions of the cost of debt equation can feel confusing. In personal debt situations, the difference is simpler than it sounds.

One formula shows your true borrowing rate right now. The other adjusts the number for how interest is sometimes treated in financial models.

Use the Pre-Tax Formula When You Want Clarity on Your Current Cost

This version reflects the interest you’re actually paying relative to what you owe.

- Best for understanding what your debt costs you today

- Useful when reviewing personal loans, credit cards, or mixed balances

- Shows the real pressure your balances are creating, without adjustments

- Helps you decide which debts feel heavier relative to their size

Use the After-Tax Formula in Financial Modeling Contexts

This version adjusts the number because interest can reduce taxable income in certain business situations.

- Seen mostly in business finance and textbooks

- Used in academic and company-level finance analysis

- Not how most personal borrowing costs are calculated

- Helpful to understand the theory, but not a decision tool for most individuals

Use a Weighted Approach When You Have Multiple Debts

If your balances carry different rates, a blended calculation gives a more complete view.

- Combines interest from all accounts into one effective rate

- Prevents one high-rate account from being overlooked

- Helps when determining the cost of debt across several balances

- Useful for prioritizing where changes may matter most

For most people managing real balances, the pre-tax formula is the one that reflects what debt costs today.

The pre-tax formula focuses on your present cost. The after-tax version appears in structured financial analysis. A weighted calculation helps when your debt is spread across more than one account.

Step-by-Step: How Do You Calculate the Cost of Debt With Multiple Loans?

When your debt is spread across different accounts, it can feel hard to see the overall borrowing view. This method brings everything together into a single blended rate, so you can understand your overall borrowing cost instead of looking at each balance in isolation.

Step 1: List Each Debt

Start by writing down every account where you're paying interest.

For each one, note:

- Current balance

- Interest rate

- Interest paid over the last year (or your best estimate)

The interest paid matters more than the advertised rate because it shows what the debt actually costs you during that period.

Step 2: Add Total Interest Paid

Now add up all the interest amounts from each account.

This gives you the total cost of borrowing across all debts for the year.

Step 3: Add Total Debt

Next, add together the balances of all those accounts.

This number represents the total amount you owe.

Step 4: Apply the Formula

Now use the core cost of debt equation:

Cost of Debt = Total Interest ÷ Total Debt

The result is a percentage. That percentage shows how much your overall debt is costing you relative to what you owe, a blended view that helps you understand the real weight of your balances.

Example of Cost of Debt Calculation

It’s easier to understand this formula when you see it with numbers that look like real-life accounts, not bond math. Here’s how a blended cost of debt calculation might look across common types of borrowing.

Example scenario

- Credit card balance: $6,000

Interest paid this year: $1,200 - Personal loan balance: $12,000

Interest paid this year: $900

Step 1: Add total debt

$6,000 + $12,000 = $18,000 total debt

Step 2: Add total interest paid

$1,200 + $900 = $2,100 total interest

Step 3: Apply the cost of debt formula

Cost of Debt = Total Interest ÷ Total Debt

$2,100 ÷ $18,000 = 0.1167

Final percentage: 11.67%

That 11.67% is the blended rate showing how much your debt costs you over the year relative to what you owed. It doesn’t replace the individual rates on each account, but it gives you a single blended rate to understand the overall weight of your borrowing.

4 Common Mistakes When Calculating Cost of Debt

Even a simple formula can give the wrong picture if the inputs aren’t consistent. Here are the mistakes that most often distort a cost of debt calculation, and how to correct them.

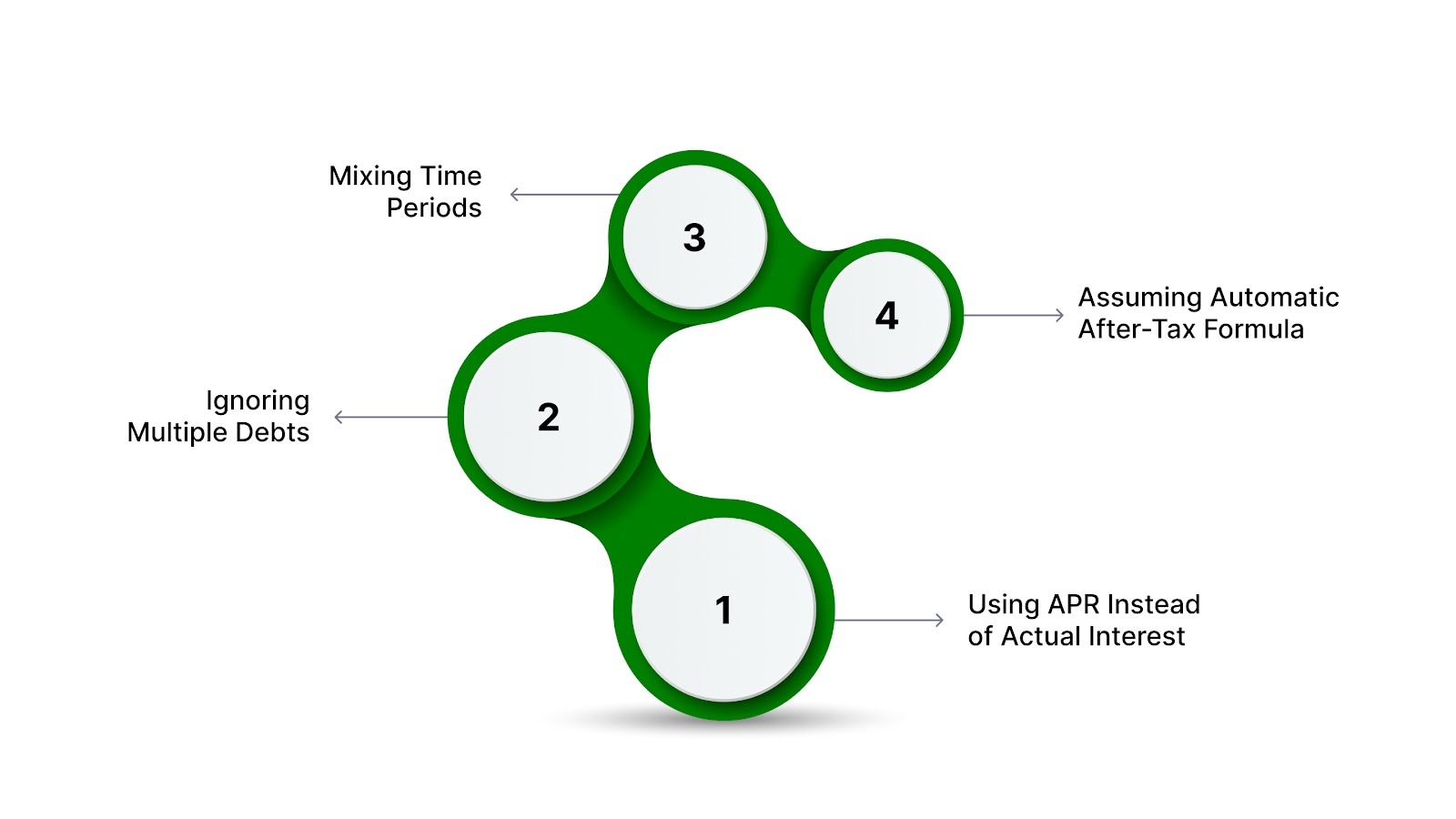

1. Using APR Instead of the Interest Actually Paid

Solution: APR shows the annualized rate, but the cost of debt calculation often works better with the interest actually charged during the period, since balances and usage change over time.

2. Ignoring Multiple Debts

Solution: Include all balances that carry interest so your total cost of debt reflects your full borrowing picture, not just one account.

3. Mixing Time Periods

Solution: Keep everything in the same timeframe, such as yearly interest with yearly balances, to avoid skewing the percentage.

4. Assuming the After-Tax Formula Applies Automatically

Solution: Treat the after-tax cost of debt formula as a financial concept. Tax treatment depends on the type of debt and individual circumstances.

Why Your Cost of Debt Changes Over Time?

If your cost of debt looks different from one year to the next, it doesn't always mean you did something wrong. Borrowing costs can shift for several reasons, some of which are outside your control.

- Market interest rates: When overall interest rates rise or fall, lenders adjust rates, especially on new or variable-rate borrowing.

- Credit profile changes: Changes in payment history, balances, or credit usage can affect how lenders view risk, which can influence rates.

- Missed payments: Late or missed payments can lead to penalty rates or higher ongoing interest costs on some accounts.

- Variable-rate adjustments: Some loans and credit products have rates that reset based on market benchmarks, which can increase costs over time.

- Account status changes: When an account moves into a different status (such as late or transferred), the structure of the balance or added charges may affect how the debt grows.

What to Do If Your Cost of Debt Feels Too High

Seeing your cost of debt as one percentage can feel discouraging, but that number is meant to bring clarity. If sorting this alone feels overwhelming, structured account support can help bring clarity.

It highlights where borrowing is weighing on you most, so your next steps can be more informed and less reactive.

If You're Still Current

When your accounts are up to date, you have more flexibility to adjust before stress builds.

- Prioritize higher-interest balances first: Even small extra payments can reduce how quickly interest grows over time.

- Ask about hardship or temporary relief options early: Reaching out sooner can keep situations simpler and more manageable.

- Be cautious about adding new high-interest debt: New balances can raise your overall cost of debt faster than expected.

If You’re Behind or Getting Notices

This stage often brings the most anxiety, but understanding the situation usually reduces uncertainty.

- Don’t ignore communication: Most notices are about account status and next steps, not immediate action.

- Confirm balances and account details: Knowing exactly what is owed helps you make practical decisions.

- Ask about structured repayment options: Many accounts can be addressed through plans designed around what you can realistically manage.

If You Need a Clear Path Forward

When things feel unclear, structure can make the situation feel more manageable. That’s where organizations like Forest Hill Management provide support focused on clarity, compliance, and steady progress.

- Secure online payment options help you track progress with transparency

- Flexible repayment plans can break large balances into manageable steps

- Structured, compliant account support is designed to protect your privacy and rights throughout the process

If you’re ready to move forward with clearer information and a more structured approach, having the right support can make the path feel more manageable.

Suggested Read: How to Settle Debt with Portfolio Recovery

Bring Clarity to Your Next Steps

Understanding the cost of debt formula brings clarity to something that often feels uncertain. When you can see the percentage your borrowing carries, it becomes easier to make calm, informed decisions instead of reacting to stress or guesswork.

If your numbers feel heavier than expected, that doesn't mean you've failed; it simply shows where attention and structure can make the biggest difference.

Taking one steady step, even a small one, can help you move from uncertainty toward progress. If you need guidance that's clear and structured, you can also reach out for support.

If you prefer a structured way to move forward, you can make a payment online or speak with an advisor for guidance.

FAQs

Q1. What is the cost of debt formula in simple terms?

A1. The cost of debt formula shows the percentage of your borrowing costs over a year. You calculate it by dividing the interest you paid by your total debt, which gives you a clearer picture of the real weight of your balances.

Q2. Is the cost of debt the same as my interest rate?

A2. Not exactly. Your interest rate applies to each account, but the cost of debt can combine multiple debts into one blended percentage, helping you understand your overall borrowing cost.

Q3. How do you calculate the cost of debt if you have more than one loan?

A3. Add up the interest paid on all accounts, then add up all balances. Divide total interest by total debt to find one overall percentage that reflects your full borrowing picture.

Q4. Why does my cost of debt increase even if I haven't taken new loans?

A4. Changes in interest rates, missed payments, or variable-rate adjustments can raise how quickly interest grows. Even without new borrowing, existing balances can become more expensive over time.

Q5. What should I do if the cost of debt feels too high?

A5. Start by reviewing which balances carry higher interest and look for structured repayment options that fit your situation. Clear information and steady steps can make the situation feel more manageable.