How to Settle Debt with Portfolio Recovery

Need Help Reviewing Your Account?

Contact UsA letter from Portfolio Recovery Associates rarely feels neutral. It lands at a moment when money already feels tight, decisions feel urgent, and control feels like it is slipping away.

Once that notice arrives, your thinking narrows fast. You want to know whether the claim is real, whether the balance can be reduced, and how much will Portfolio Recovery settle for without creating another problem.

Debt settlement works on structure, not pressure or guesswork. Outcomes depend on verification, timing, affordability, and understanding what makes resolution realistic rather than emotionally rushed.

In this article, we’ll break down how settling with Portfolio Recovery typically works and how to move forward with clarity instead of fear.

Key Takeaways

- Debt buyers like Portfolio Recovery purchase accounts at a discount, which can create opportunities for reduced settlements, but results aren’t guaranteed.

- Verifying the debt, knowing what you can realistically afford, and documenting all communications are key to negotiating safely.

- Settlement amounts vary widely based on factors like account age, payment method, and portfolio priorities, so strategy matters more than guesswork.

- Rejected offers don’t end the process; timing, counteroffers, and your payment capacity can all influence the final outcome.

- Working with a trusted partner like Forest Hill Management can provide structure, clarity, and support, helping you make informed, confident choices without added stress.

Who Is Portfolio Recovery Associates?

Portfolio Recovery Associates (PRA) is a debt buyer. The company purchases charged-off consumer accounts from original creditors after those creditors have written the accounts off as losses. PRA does not issue credit cards or make loans itself.

In most cases, when PRA contacts you, it is not collecting on behalf of the original creditor. Instead, it has purchased the account and now owns the right to collect the debt. Any money they recover goes to them, not to the original lender.

Understanding this business model helps explain why negotiation is sometimes possible. However, the fact that PRA may settle an account does not mean it is required to do so or that every account will qualify for a reduced settlement.

Why Portfolio Recovery May Settle for Less Than You Owe

Because debt buyers purchase accounts at a discount, there is often room for negotiation. Industry reports and regulatory filings indicate that charged-off debts are often acquired at a discount to the original balance, though purchase prices vary widely.

Several factors influence PRA’s willingness to accept less than the full balance:

- Partial recovery can still be profitable: Since PRA’s acquisition cost is lower than the face value of the debt, collecting a portion of the balance may still generate a return.

- Collection efforts have ongoing costs: Phone calls, letters, compliance requirements, legal review, and potential litigation all reduce net recovery, making settlement more attractive in some cases.

- Account age affects collectability: Older debts are generally harder to collect, especially as the statute of limitations approaches or expires, which can reduce leverage and increase settlement likelihood.

- Portfolio-level performance matters: Debt buyers evaluate success across entire portfolios rather than maximizing recovery on every individual account, which can create flexibility in resolving certain debts.

Settlement is common but not guaranteed. Outcomes depend on the specific account, its age, documentation, legal enforceability, and PRA’s internal policies at the time of negotiation.

Also Read: Debt Settlement Explained: How It Works and If It's a Good Option for You

These pressures create opportunity, but settlement amounts depend on factors specific to your account and situation.

How Much Portfolio Recovery Typically Settles For

Public consumer reports and industry observations suggest that some settlements with Portfolio Recovery Associates may fall in the range of roughly 40 to 60 percent of the stated balance, though outcomes vary widely and no settlement amount is guaranteed.

In some cases, particularly with older or weaker accounts, settlements may land lower, while newer or well-documented debts may settle closer to the full amount.

The percentage PRA may accept depends on several factors they evaluate during negotiation:

- Lump sum versus installments: One-time payments often receive deeper discounts because they eliminate future collection costs and provide immediate recovery.

- Account age and history: Newer accounts with recent activity or stronger documentation tend to settle at higher percentages than older debts approaching the statute of limitations.

- Payment capacity signals: If you demonstrate an ability to pay more, PRA may push for higher settlement amounts; communicating limited funds can sometimes support lower offers.

- Balance size: Smaller balances often settle at higher percentages because fixed administrative costs make steep discounts impractical.

- Internal portfolio considerations: Timing, such as quarter-end or year-end reporting periods, may influence settlement flexibility as PRA manages recovery targets across entire portfolios.

Getting favorable terms requires more than understanding typical ranges; it demands strategic execution.

How to Negotiate a Settlement With Portfolio Recovery

Negotiation is about sequencing actions correctly and maintaining documentation at every step. Here's how to guide the process without creating new problems:

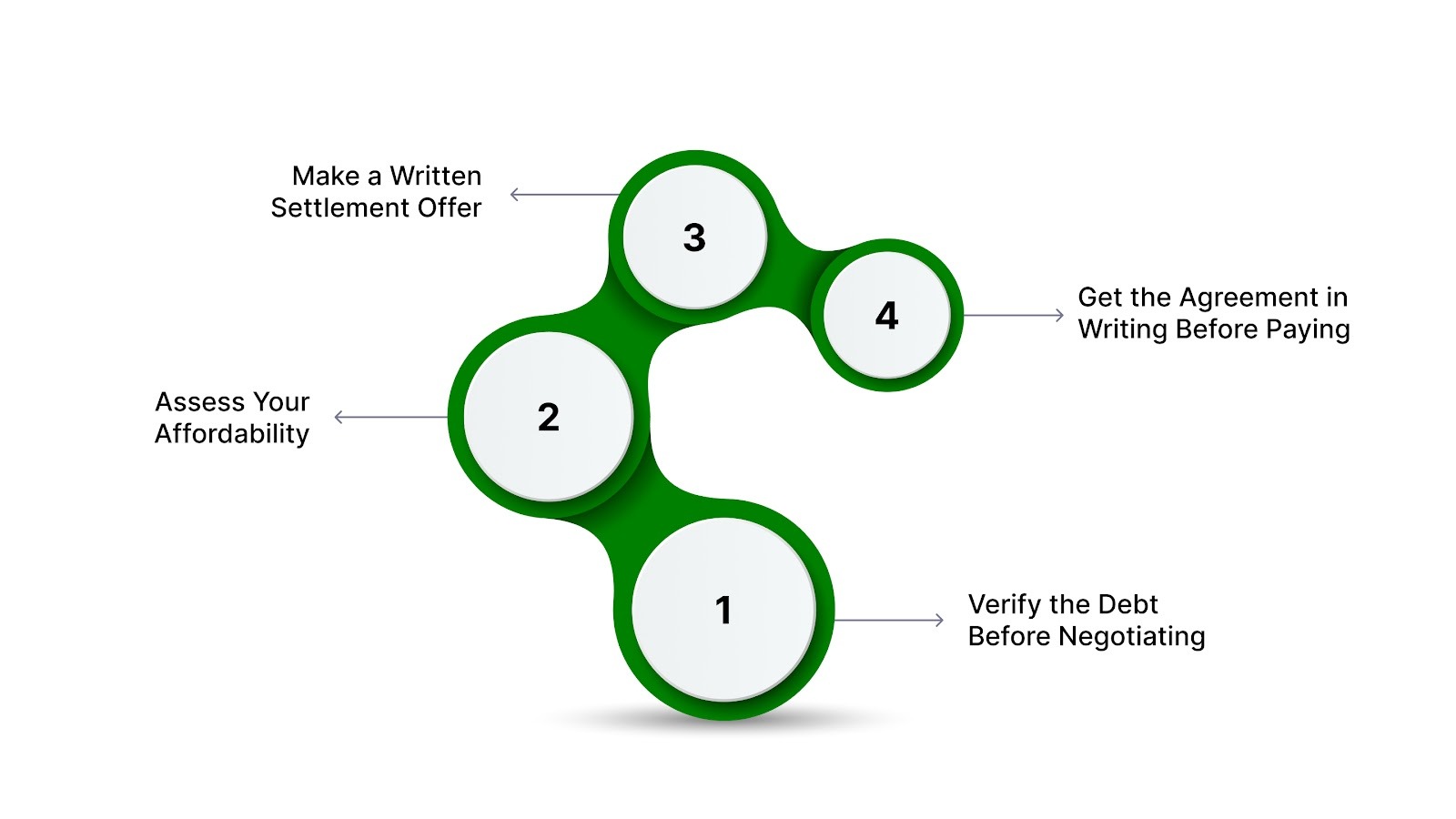

Step 1: Verify the Debt Before Negotiating

After Portfolio Recovery’s first written contact, you have 30 days to request debt validation in writing. If you do so within that window, they must pause collection activity until they provide verification. You can still request verification later, but the same legal protections may not apply.

Debt validation is meant to confirm that Portfolio Recovery owns the account and that the balance they claim matches their records. This helps prevent paying a debt you don’t owe, dealing with the wrong company, or negotiating based on an incorrect amount.

It is generally advisable to confirm the debt information before beginning settlement discussions.

Step 2: Assess What You Can Realistically Afford

Your settlement offer should be based on what you can pay without creating new financial strain, not on what you think the collector expects. Agreeing to terms you can’t meet increases the risk of default and further collection activity.

Collectors often accept lump-sum settlements because they provide immediate payment, though outcomes vary by account. Payment plans are sometimes available but may involve higher total payments over time.

Before making any offer, determine an amount you can realistically pay and allow room for unexpected expenses.

Step 3: Make a Written Settlement Offer

It is common to begin negotiations below your maximum affordable amount to allow room for counteroffers. The exact figures depend on your situation and the account.

Submit your offer in writing, either by mail or another documented method. Include the account number, proposed settlement amount, and whether the offer is a lump sum or payment plan. Keep the communication brief and focused on terms rather than personal financial details unless requested.

Written communication creates a record of the negotiation and reduces reliance on verbal statements that are difficult to verify later.

Step 4: Get the Agreement in Writing Before You Pay

Do not send payment based solely on a verbal agreement. Before paying, obtain written confirmation from Portfolio Recovery stating the settlement amount, payment terms, and that the payment satisfies the debt.

The confirmation should reference your specific account and clearly describe the agreement. While collectors are not required to include detailed credit-reporting language, written settlement terms provide proof if questions arise later.

Only after receiving and reviewing this written agreement should you submit payment, and you should keep copies of all related documents for your records.

Also Read: How to Rebuild Credit After Debt Settlement

Even with careful negotiation, settlement involves trade-offs that extend beyond the immediate transaction.

Risks and Considerations When Settling With Portfolio Recovery

Settling for less than the full balance resolves the immediate collection pressure, but it triggers downstream consequences that affect taxes and credit reporting. These aren't reasons to avoid settlement; they're just realities you should anticipate before finalizing any agreement.

Here's what happens after settlement:

If Portfolio Recovery rejects your initial offer, the negotiation isn't necessarily over.

A declined offer doesn’t necessarily end the conversation. In many cases, it simply determines what happens next in the negotiation.

What Happens If Portfolio Recovery Refuses Your Offer?

Rejection of your first proposal doesn't mean they won't settle; it often means they're testing whether you'll increase your offer or waiting to see if their counteroffer prompts movement. Debt buyers operate with flexibility built into their recovery models.

Here's what typically happens after they decline:

- They counter with a higher percentage: If you offered 30%, they might respond with 50% to gauge your flexibility and move toward the middle ground

- You can decline and wait: Walking away sometimes prompts them to revisit your original offer weeks or months later when their internal priorities shift

- Legal action as a factor: Legal action may become a consideration on some accounts, depending on balance size, documentation, and state law.

Also Read: What Is a Debt Resolution Agreement and How It Works

For some people, this back-and-forth uncertainty is manageable. For others, it highlights why an alternative approach may be worth considering.

How Forest Hill Management Approaches Resolution Differently

Settlement negotiations with debt buyers can work, but they often involve uncertainty: offers, counteroffers, and waiting periods that make it hard to plan with confidence. Forest Hill Management focuses on a more structured approach centered on clarity and consistency.

Rather than navigating uncertain settlement negotiations on your own, you can work with us to understand your account and explore structured repayment options where applicable.

What makes this approach clearer:

- Flexible repayment options: Structured plans based on what you can reasonably afford.

- Clear terms and visibility: You understand your balance, payment schedule, and progress at every step.

- Documented account information: Payment status and account details are available through secure access.

- Secure online payments: Manage payments safely and conveniently, on your schedule.

- Compliant, respectful communication: Interactions are handled in line with federal consumer protection standards, with professionalism and care.

If you want to review your account details or understand available next steps, you can access your information online or speak with a Forest Hill Management advisor.

Conclusion

Facing a debt claim from Portfolio Recovery can feel overwhelming, but understanding how accounts are purchased and what affects settlements gives you perspective and control. Knowledge, patience, and careful decision-making are your best tools for handling these situations thoughtfully.

When making choices about your debt, having support you can trust makes a difference. Forest Hill Management is available as a resource to help you review your account information and understand possible next steps.

Take the first step toward resolving your account with confidence - contact Forest Hill Management today.

FAQs

1. How does the original creditor’s history affect a Portfolio Recovery settlement?

Portfolio Recovery may factor in the creditor’s past reporting, interest patterns, and collection attempts. Accounts from aggressive creditors or frequent charge-offs can affect how flexible they are with settlements.

2. Can disputes with other agencies impact negotiations?

If the same debt is reported or disputed elsewhere, Portfolio Recovery may adjust its offers to avoid conflicting claims. Overlapping disputes can influence timing and counter-offers.

3. How does the timing of portfolio purchases influence settlement?

Debts bought near the fiscal quarter or year-end may prompt quicker settlements to meet internal targets, potentially making lower offers more likely.

4. Do internal metrics vary by account type?

Recovery thresholds differ for credit card, retail, medical, or telecom debts. Settlement flexibility depends on ROI, collection effort, and historical recovery for that account category.

5. Can partial payments affect future settlement opportunities?

Unapproved partial payments may signal willingness to pay but reduce leverage, affecting your ability to negotiate deeper discounts later.