What Is a Debt Resolution Agreement and How It Works

Need Help Reviewing Your Account?

Contact UsManaging debt can feel like a trap, especially when you're overwhelmed by mounting bills, a poor credit score, or the looming fear of wage garnishment. If you're financially stressed, you know how tough it can be to find a way forward.

Shockingly, completion rates for debt settlement programs often hover around 45-50%, meaning many individuals struggle to fully resolve their debts.

But there is hope. A debt resolution agreement could be the solution you're looking for. This blog will explain what a debt resolution agreement is, how it works, and how it can help you regain control over your finances. Let’s get started.

Key Takeaways

- Debt resolution agreements help reduce debt by negotiating settlements with creditors, typically for an amount less than the full amount owed.

- These agreements primarily apply to unsecured debts, such as credit cards, personal loans, and medical bills.

- A successful agreement can ease financial burden by creating manageable repayment plans and preventing legal actions.

- Settling debt through an agreement can impact your credit score, with settled accounts remaining on your report for up to seven years.

- While debt resolution can provide relief, it’s important to understand the risks, including potential tax implications and missed payment consequences.

What is A Debt Settlement Agreement?

A debt settlement agreement is a negotiated deal in which the creditor accepts less than the amount you owe. This is in exchange for a lump-sum or structured repayment. In return, the debt is considered satisfied, and you avoid further collection efforts or legal action.

Debt settlement doesn’t involve new loans or court filings. It’s an informal negotiation that can be highly effective when properly structured.

Debt settlement can be a smart choice if you have unsecured debts like credit cards, personal loans, or medical bills, and can no longer afford the minimum payments. It’s also an option if you have a lump sum of money available or want to avoid bankruptcy.

Now that we’ve covered why these agreements matter, let’s take a look at the key elements that make up a solid debt resolution agreement.

Why Is a Debt Settlement Agreement Important?

A debt settlement agreement can offer significant benefits to both borrowers and lenders when traditional repayment options are not feasible. Here's why it matters:

- Reduces Financial Burden for Borrowers: It allows you to negotiate paying less than the full amount owed, easing your financial strain and helping you get back on track.

- Helps Lenders Recover Some of Their Debt: Instead of pursuing lengthy and costly legal action, lenders can resolve the outstanding debt quickly and efficiently.

- Avoids Long-Term Consequences: For borrowers, this agreement can help prevent further damage to their credit and avoid wage garnishment.

- Creates a Mutually Beneficial Solution: Both parties come to an agreement that allows the borrower to repay a reduced amount and the lender to resolve the debt without unnecessary delays.

A debt settlement agreement offers a viable solution for borrowers, enabling lenders to settle debts and creating a mutually beneficial outcome for both parties.

Also Read: Is Paying Debt Collection Agencies a Bad Idea?

Now that we’ve covered why these agreements matter, let’s take a look at the key elements that make up a solid debt resolution agreement.

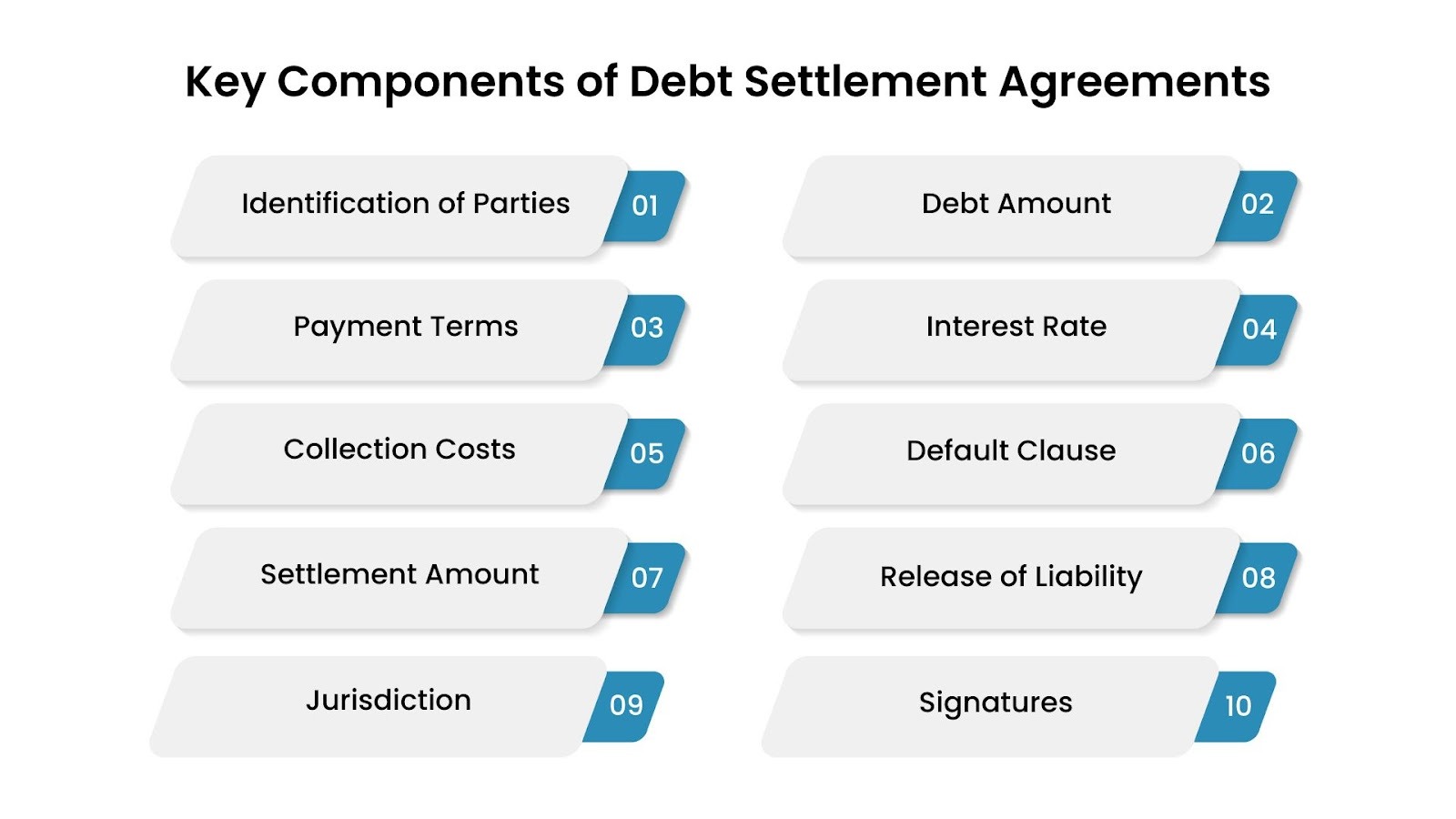

Key Elements of a Debt Settlement Agreement

A debt settlement agreement outlines the terms under which a debt will be resolved. Here are the essential components:

- Identification of Parties: This includes the debtor and creditor, along with their contact details, ensuring both parties are clearly identified.

- Debt Amount: The total debt owed, including the original amount, interest, and additional fees, is specified for transparency.

- Payment Terms: The agreement outlines the payment schedule, specifying the amount due per installment and the due dates.

- Interest Rate: If applicable, the interest rate is defined to clarify the amount that will be paid throughout the settlement period.

- Collection Costs: Any additional costs, such as legal fees, are outlined if the debtor fails to meet the payment terms.

- Default Clause: Specifies the consequences of missed payments, which may include collection proceedings or legal action.

- Settlement Amount: The agreed-upon amount to settle the debt, typically lower than the original, is detailed in the agreement.

- Release of Liability: Upon full settlement of the debt, the debtor is released from all further obligations related to the debt.

- Jurisdiction: Specifies where any disputes arising from the agreement will be resolved, ensuring clarity on legal proceedings.

- Signatures: The agreement is finalized with signatures from both parties, confirming mutual acceptance of the terms.

These key elements ensure both parties are clear about their responsibilities and expectations, ultimately aiming for a fair resolution.

With the key elements in mind, it's essential to consider the potential risks and consequences associated with debt settlement.

Risks and Consequences of Debt Settlement

While debt settlement may offer relief, it's essential to be aware of the potential risks:

- Credit Score Damage: Missed payments and accounts marked as "settled" can remain on your credit report for up to seven years, potentially impacting your credit score.

- No Guarantees: Creditors aren't obligated to accept a settlement offer. They may reject it or escalate to legal action instead.

- High Fees: Debt settlement companies charge fees between 15% and 25% of the enrolled debt, increasing your overall financial burden.

- Stress and Uncertainty: The process can take years, with no guaranteed success. Failed negotiations could worsen your financial situation.

By understanding these potential consequences, you can better assess if debt settlement is the right option for your financial situation.

Also Read: When Does the Collection Process Begin for Overdue Balances

After understanding the risks, let’s review the steps involved in approaching debt settlement to ensure you're prepared for the process.

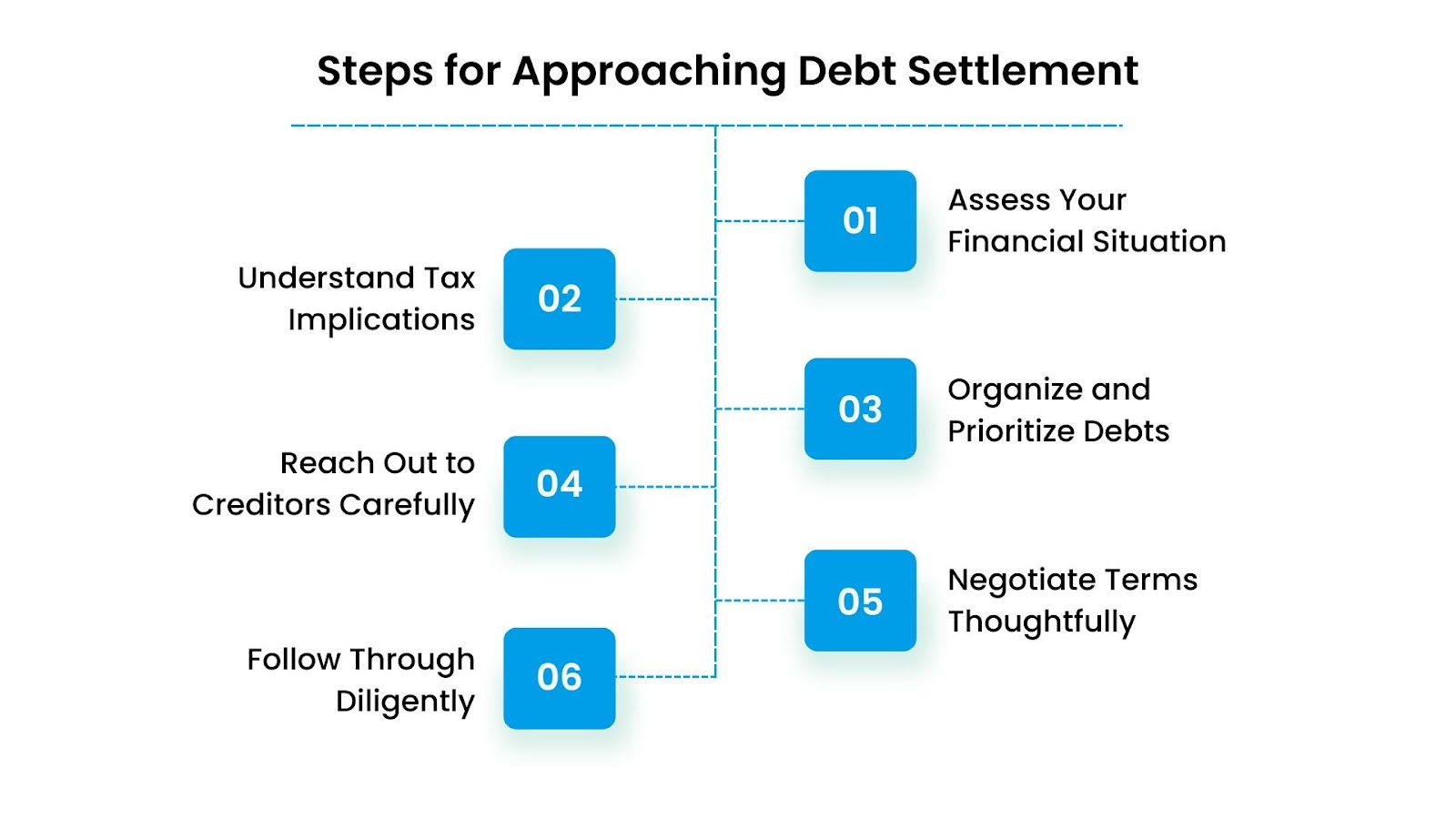

Steps for Approaching Debt Settlement

If you're considering debt settlement, it's crucial to understand the steps involved. Here are key steps to guide you:

1. Assess Your Financial Situation

Start by honestly reviewing your finances. List all your debts, including the balance, interest rate, and collection status. Assess your income and expenses to determine what you can afford for settlement.

2. Understand Tax Implications

Debt forgiveness over $600 is typically considered taxable income. If you settle a debt for less than the amount owed, the forgiven amount may need to be reported on your tax return. However, if your debts exceed your assets (insolvency), you might avoid the tax.

3. Organize and Prioritize Debts

Not all debts are the same. Prioritize those that are in collections, impacting your living situation, or carrying high interest rates. If you can't address them all at once, creating a priority plan will help.

4. Reach Out to Creditors Carefully

Approach creditors in writing, ensuring you have a paper trail. If you’re working with an attorney, they’ll handle this for you. Propose a realistic settlement offer and see how the creditor responds.

5. Negotiate Terms Thoughtfully

When creditors are open to settling, negotiate the terms clearly. Focus on the total settlement amount, payment structure (lump sum or installments), and how the settlement will be reported to credit bureaus. Always get the agreement in writing.

6. Follow Through Diligently

Once an agreement is in place, make sure you meet all payment deadlines. Keep proof of all payments and communications. After settling, confirm the creditor has updated your credit report accordingly.

This structured approach can guide you toward a successful debt settlement process, but it’s essential to stay organized and focused.

The Forest Hill Management can help you tackle these steps with ease. Contact our financial advisors to create a custom plan to guide you through the debt settlement process and ensure you're on the right path to financial freedom.

Now that you know the steps, let's talk about how to choose the right debt settlement company to guide you through the process.

How To Choose The Right Debt Settlement Company

Selecting the right debt settlement company is crucial for achieving financial recovery. Here's how to pick the best one:

- Research the company’s reputation: Look for established companies with a solid reputation and positive reviews and ratings.

- Verify accreditations: Check for certifications from the American Association for Debt Resolution and ensure your counselor is certified by the International Association of Professional Debt Arbitrators.

- Avoid upfront fees: Federal law prohibits charging fees before settling at least one debt. Be cautious if “commissions” come up; it may signal a focus on sales over your best interests.

- Look for experience with your debt type: Ensure the company has experience handling the type of debt you're dealing with, whether it's credit card debt, medical bills, or student loans. Different debts require different approaches.

- Steer clear of unrealistic promises: No company can guarantee results. Be skeptical of companies that offer “too good to be true” promises.

Also Read: Improving Your Company's Financial Health

Choosing wisely means putting your trust in a partner who genuinely has your best interests in mind. It’s time to take that first step toward financial freedom with The Forest Hill Management. Here’s how we can help guide you every step of the way.

Your Path to Debt Resolution Starts Here

If you're looking to resolve your debt and regain financial control, The Forest Hill Management is here to guide you through the process with:

- Debt Resolution Agreements: We help you negotiate agreements with creditors to reduce debt and create manageable payment plans.

- Personalized Financial Support: Our team works closely with you to create a customized strategy for resolving your debt.

- Flexible Repayment Options: Choose from various repayment plans that fit your financial situation, making it easier to stay on track.

- Secure Online Payments: Safely manage your payments through our secure platform, simplifying your debt repayment process.

- Compliant & Transparent Process: We ensure that all debt resolution efforts adhere to industry regulations, providing you with peace of mind.

Take control of your financial future today with The Forest Hill Management. We’re here to support you every step of the way.

Conclusion

A debt resolution agreement can be an effective solution for reducing debt and regaining control over your finances. Negotiating with creditors helps you find manageable payment plans and avoid the stress of overwhelming debt.

Don’t let debt dictate your future; take action now to regain control. Make a payment online today and take the first step toward financial freedom. The Forest Hill Management is here to help you every step of the way.

FAQs

1. Is debt settlement better than bankruptcy?

It depends on your situation. Debt settlement takes longer, doesn’t eliminate all debt, and can still hurt your credit score. Bankruptcy may offer faster relief, but it also damages your credit.

2. Can I negotiate with creditors if my debts aren’t past due?

It’s less common, but possible. Creditors prefer you stick to your payment plan when you’re current. However, if you're facing financial hardship, explaining your situation might help you reach a settlement.

3. Will debt settlement completely erase my debt?

No, debt settlement reduces the amount you owe but doesn’t eliminate all debt. You’ll need to pay the agreed-upon settlement amount. Settled debt stays on your credit report for seven years and may be taxed.

4. How long does debt settlement take?

Debt settlement can take anywhere from a few months to a few years, depending on the amount of debt and the agreements made with creditors. It’s essential to be patient, as the process may take some time.

5. Will debt settlement hurt my credit score?

Yes, debt settlement can negatively affect your credit score. Settling debts may lower your score in the short term, but it can help you get out of debt and rebuild your credit over time.