Debt Mediation and Repayment Strategies: A Clear Guide

Need Help Reviewing Your Account?

Contact UsDebt rarely collapses all at once. It tightens slowly as due dates stack, balances drift upward, and decisions start feeling reactive instead of deliberate. That pressure is no longer personal failure when U.S. household debt sits near $18 trillion, making overload a structural reality, not an exception.

As obligations multiply, the question stops being how hard you try and becomes whether the system you’re using even allows progress. Over 505,000 consumer bankruptcy filings signal what happens when people see no structured middle ground between chaos and collapse.

This is where repayment mediation services enter the picture, not as a rescue fantasy but as a disciplined way to introduce order. The idea is simple: progress improves when negotiation, repayment, and accountability stop competing with each other.

In this article, we’ll explore how debt mediation works alongside repayment strategies and how to move forward without losing control or rushing toward extremes.

Key Takeaways

- Debt mediation provides a neutral space when negotiations break down, but it isn’t guaranteed and can incur fees.

- Repayment strategies balance math and psychology: avalanche minimizes interest, snowball increases motivation, and structured plans reduce stress.

- Mediation works best for disputed or collective debts; structured repayment fits stable incomes and those valuing clarity and compliance.

- Direct plans, like Forest Hill Management, remove intermediaries, offer one point of contact, flexible schedules, and clear tracking.

- Understanding tradeoffs, such as risk vs. certainty, savings vs. simplicity, helps choose a method that prevents burnout and ensures steady progress.

What Debt Mediation Actually Means

Debt mediation puts a neutral third party between you and the companies you owe. Their role is to facilitate conversation when direct negotiation has stalled or when the power imbalance makes independent agreement unlikely.

This differs fundamentally from debt settlement, where a company negotiates lower payoff amounts but doesn't serve as neutral ground. Mediation doesn't create new financial products or absorb your obligations. It creates space for resolution when communication has broken down.

Mediation works best when all parties agree to participate and when there's a genuine willingness to find middle ground. Understanding what mediation is, and isn't, helps you determine whether it fits your situation or whether a different structure makes more sense.

Types of Debts Where Mediation Can Help

Mediation functions best with unsecured obligations, the kind that don't have collateral attached. Credit card balances, medical bills, and personal loans fall into this category because creditors have limited recourse beyond negotiation or legal action.

Once an account lands in collections, mediation can reopen dialogue that might not happen otherwise. This is especially useful if the original creditor sold the debt and the collection agency prefers settlement over prolonged pursuit.

Here's where mediation typically creates the most traction:

- Credit card debt that's gone unpaid long enough for the issuer to consider loss mitigation

- Medical bills disputed for billing errors, insurance miscommunication, or unexpectedly high charges after service

- Personal loans from non-bank lenders where default has triggered aggressive collection but no legal filing yet

- Accounts transferred to third-party collectors who lack complete documentation or face internal pressure to close older files

- Situations where multiple creditors refuse individual negotiation but might engage collectively through a mediator

The method loses effectiveness with secured debt like mortgages or car loans, where the lender's leverage comes from asset repossession rather than negotiation. Student loans also resist mediation because federal servicers operate under strict regulatory frameworks that limit settlement flexibility.

Also Read: Role of Mediation in Resolving Debt Disputes

Once you know what you're working with, the next question is how to actually pay it down.

Common Repayment Strategies That Work

Managing multiple debts effectively means choosing a strategy that fits both your finances and your motivation. Let’s break down the main approaches:

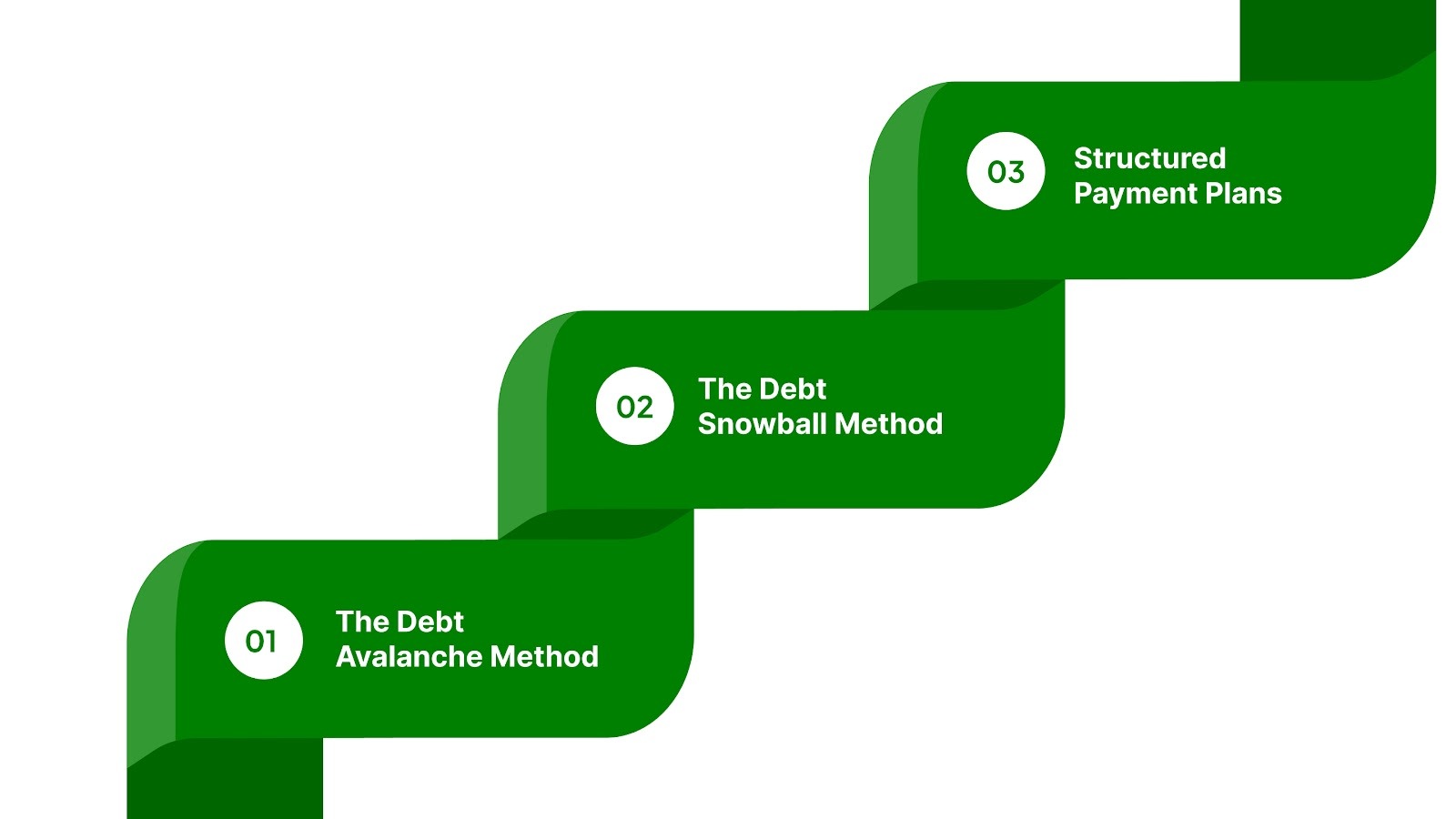

1. The Debt Avalanche Method

One way to tackle multiple debts is by focusing on interest rates first. This approach helps you save the most over time, though it can test your patience. Here’s how it works:

- List debts by APR: Order all your debts from highest to lowest interest rate.

- Make minimum payments on all debts: Keep accounts current while targeting one aggressively.

- Direct extra money to the highest-rate debt: Pay as much as possible on that balance until it’s gone.

- Move to the next highest rate: Repeat the process until all debts are cleared.

- Understand the psychological challenge: High-rate debts with large balances may feel slow to shrink, so patience and long-term focus are key.

2. The Debt Snowball Method

The snowball ignores interest rates and targets the smallest balance first. This approach helps sustain motivation and keeps you engaged with your payoff plan. The process looks like this:

- List debts by balance size: Order all debts from smallest to largest, ignoring interest rates.

- Make minimum payments on all other debts: Keep all accounts current while focusing on one.

- Direct extra money to the smallest debt: Pay it off as quickly as possible.

- Roll payments into the next smallest debt: Once a balance is cleared, apply that same amount to the next smallest account.

- Benefit from psychological momentum: Seeing accounts fully paid off creates visible progress, keeping motivation high.

The tradeoff is real. You'll pay more in total interest if you ignore high-rate debts in favor of small balances. But if the alternative is giving up entirely, the extra cost becomes irrelevant.

3. Structured Payment Plans

Another strategy sets fixed monthly payments to reduce stress and simplify repayment, rather than adjusting each month based on fluctuating minimums. This approach keeps you on track and provides predictability. This method breaks down like this:

- Agree on fixed monthly payments: Set an amount with your creditors that you commit to pay every month.

- Eliminate guesswork: No more recalculating priorities or deciding where extra cash goes each month.

- Freeze interest and penalties: Many plans prevent additional fees and stop further interest from accruing.

- Pause collection actions: Creditors typically halt calls or collection attempts while you follow the plan.

- Gain clarity and reduce stress: Knowing exactly what’s required each month makes repayment manageable and keeps both you and the creditor aligned.

Also Read: The Future of Compliance in Debt Collection: Trends and Innovations

While these strategies put you in control, there are also approaches that involve third parties; each comes with its own advantages and risks.

Advantages and Risks of Debt Mediation

Mediation introduces a neutral negotiator when direct conversation has failed, but it's not a guaranteed path to easier terms. To see how mediation can impact your debt situation, here’s a clear look at its potential advantages and risks:

The method works when both sides want a resolution but can't find it alone. It fails when creditors see more value in pursuing collections through traditional channels or when your financial situation offers nothing they're willing to accept as a settlement.

With these advantages and risks in mind, it’s helpful to consider who might benefit most from mediation versus other repayment strategies.

Who Should Consider Mediation vs. Structured Repayment

Not every debt situation calls for the same response, and knowing which tool fits your reality determines whether you make progress or stall without meaningful progress.

Mediation becomes the right move when:

- Multiple creditors refuse to negotiate individually, but a collective discussion might shift their stance

- Disputed charges or documentation errors block resolution, and you need a neutral party to verify facts

- Direct communication with creditors has turned hostile or legally aggressive to the point where productive conversation is unlikely

- You have leverage to offer (lump sum from savings, proof of hardship, asset liquidation), but need a structured environment to present it credibly

Structured repayment makes more sense when:

- Your income is stable enough to sustain fixed monthly obligations without frequent adjustments

- You want one point of contact managing the entire process rather than coordinating multiple mediators and creditors

- Compliance with federal regulations and transparent tracking matter more to you than negotiating reduced balances

- The cognitive relief of predictable payments outweighs the potential savings from settlement negotiations

- You're willing to commit to a plan that prioritizes completion over flexibility

Neither option is inherently superior. Mediation offers the potential for negotiation at the cost of uncertainty and fees. Structured repayment offers clarity and compliance at the cost of full balance responsibility. Your situation, temperament, and risk tolerance determine which path serves you better.

Also Read: How to Handle Debt Collection Lawsuits Without Panic

For those who prefer clarity, control, and simplicity without extra intermediaries, there’s a more direct way to manage debt.

How Forest Hill Management Provides Structured Repayment Without the Middleman

Some repayment options involve multiple steps or additional parties. Forest Hill Management works directly with you to create a repayment plan that fits your life, keeping things simple and transparent.

Rather than involving a separate mediator, you work directly with us to build a repayment plan that fits your situation.

Here's how that simplifies things:

- One point of contact: No separate mediators, no additional fees, no confusion about who's handling what.

- Plans built around your reality: We assess what you can afford and structure payments accordingly, not the other way around.

- Clear tracking from day one: See your balance, payment history, and progress through a secure online platform.

- Compliance-focused processes: Every step follows federal regulations designed to protect consumers.

- Adjustments when life changes: If your situation shifts, we work with you to modify the plan rather than impose rigid terms.

By working directly with Forest Hill Management, you stay in control every step of the way. You’ll have clarity on what you owe, confidence that your plan follows the rules, and the flexibility to adjust as your life changes.

Conclusion

Mediation and structured repayment serve different purposes. Neither removes your obligations, but both provide clarity and a way to manage them more effectively.

Understanding your options helps you choose the approach that works best for your situation. Some circumstances benefit from negotiation, while others are resolved most efficiently through a direct, structured plan.

Forest Hill Management offers repayment solutions that are straightforward, flexible, and built around your needs.

Explore your repayment options or contact our advisors for personalized support.

FAQs

1. Can debt mediation help with negotiating non-financial terms of debt?

Yes. Mediators can facilitate agreements on billing cycles, reporting timelines, or communication methods, essentially adjusting logistical or procedural aspects without changing the principal owed.

2. How does using a mediator affect the tax implications of forgiven debt?

Mediation itself doesn’t erase debt, but if a creditor later agrees to forgive a portion, that forgiven amount could be considered taxable income. Early consultation with a tax advisor is recommended.

3. Are there industries or debt types where mediation tends to fail despite willingness?

Debts governed by regulatory rigidity, like certain student loans, government-backed loans, or court-ordered fines, often resist mediation because statutory rules limit negotiation flexibility.

4. Can mediation or structured repayment protect you from aggressive debt collectors?

While mediation creates a neutral forum, it can signal good-faith engagement to collectors, potentially reducing harassment. Structured repayment provides documented evidence of compliance, which can prevent unnecessary escalation.

5. How do I know whether mediation or structured repayment is right for me?

The right option depends on your income stability, number of creditors, and whether you prefer negotiation or predictable payments. Speaking with an advisor can help clarify which approach fits your situation.