How to Handle Debt Collection Lawsuits Without Panic

Need Help Reviewing Your Account?

Contact UsFew things feel as stressful as being sued over unpaid debt, and it is happening more often than you might think. According to research, debt collection lawsuits are surging across the United States to pre-pandemic levels. States like Connecticut saw filings rise by nearly 24% in early 2025 as compared to 2024.

Debt lawsuits can be intimidating, but they are also a process; one that can be managed with calm, informed action. Understanding how to respond, your rights, and the next steps to take can make all the difference.

In this guide, we break down exactly how to handle a debt collection lawsuit without panic, from the initial notice to the final resolution.

After reading this guide, you will know:

- A debt lawsuit is manageable with the right response. Receiving a summons does not mean you have already lost; it simply starts a process you can navigate calmly and confidently.

- Responding on time protects your rights. Filing an answer prevents a default judgment and keeps the court from deciding the case without your input.

- Verification and documentation matter. Always confirm that the debt is valid, accurate, and within the statute of limitations before taking any action.

- Legal defenses can make a difference. Mistaken identity, expired time limits, or missing documentation can all affect the outcome of a case.

- Communication and negotiation reduce stress. Speaking directly with the agency and exploring settlement options can help you resolve the situation faster and with less uncertainty.

Who Are You Dealing With in a Debt Lawsuit

Debt lawsuits can be intimidating, but they often follow a predictable timeline. Typically, an account becomes seriously past due after 90 to 180 days of missed payments. Importantly, that does not mean you are out of options.

Every state has what’s called a statute of limitations, usually between three and six years, which limits how long a creditor or collector can take legal action. Once that time passes, the debt may still exist, but they can no longer sue to collect it. Knowing this gives you perspective and power, not panic.

When a lawsuit happens, it helps to understand who is involved and what their role is. This is the who’s who in a debt collection case:

- Creditor: This is the original company or lender you borrowed from, like a credit card provider or bank. In the lawsuit, they are the Plaintiff, the one bringing the case. If they win, they become the Judgment Creditor, meaning the court has confirmed the debt.

- Debt Collector: A debt collector or collection attorney works to recover debts on behalf of others. Sometimes, creditors sell old debts to these collectors. Once purchased, the collector becomes the new creditor, legally allowed to pursue repayment.

- Debtor: If you owe the money, you are the Defendant in the case. If a judgment is entered, you become the Judgment Debtor, meaning you are legally responsible for the specified amount.

- Judgment: This is the court’s official decision about the case. A money judgment simply states that one person or company owes another a specific dollar amount.

When the original creditor sues, they usually have complete records. But when a third-party debt buyer files, they may not. This lack of proof can work in your favor. Either way, knowing the players replaces fear with clarity.

Now that you understand who’s involved, let us explore what happens when you are sued for debt and how to approach each step calmly and confidently.

Suggested Read: A Beginner’s Guide to Debt Management Strategies

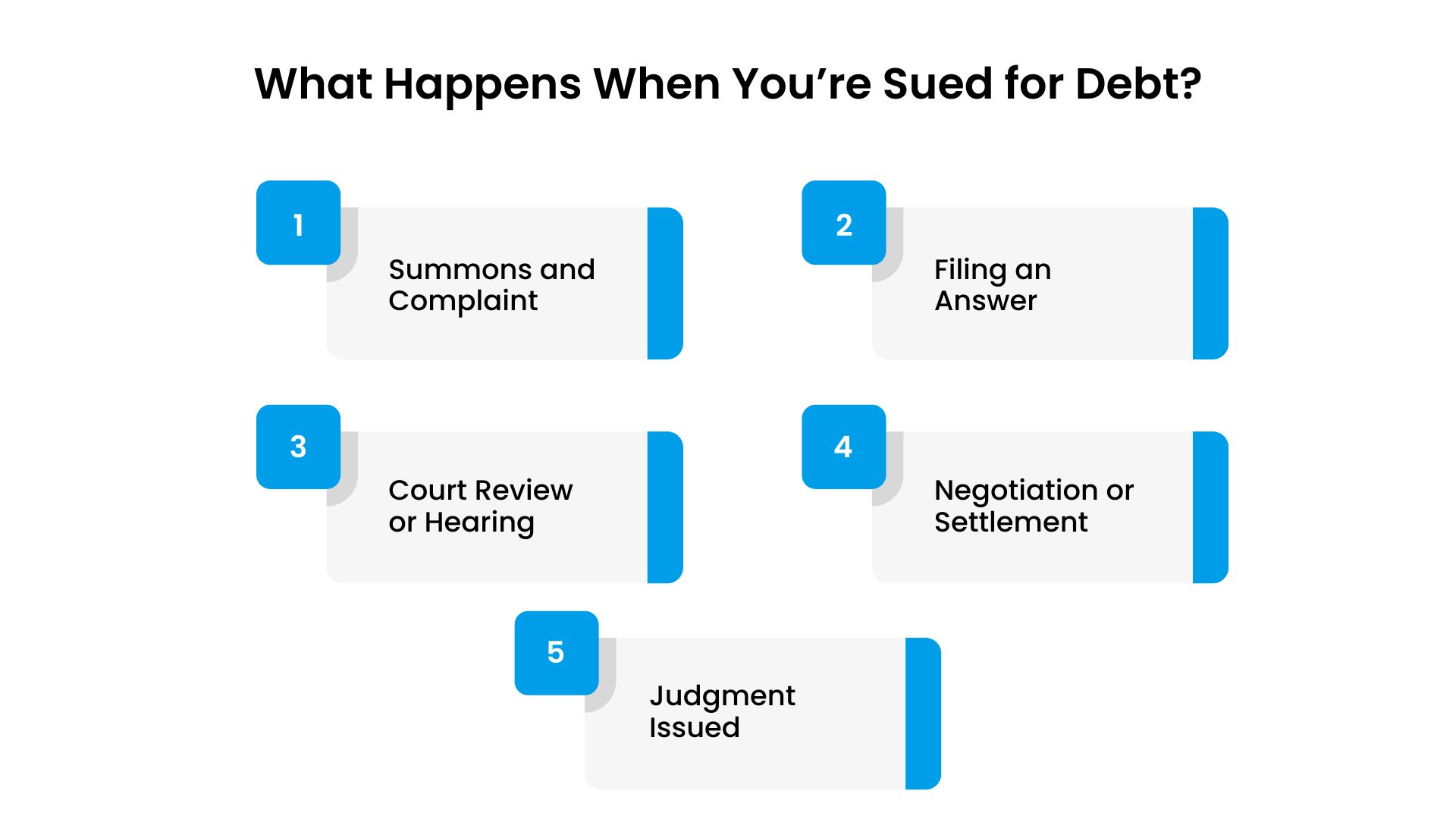

What Happens When You Receive a Debt-Collection Lawsuit??

When a summons or complaint arrives, it means a creditor or collector has taken the first legal step to recover a debt. If you do not respond in a timely manner (usually within 20–30 days), the court may issue a default judgment. This means the case is decided without your input.

Responding ensures your voice is heard and keeps all options available to you. Here’s what usually happens in a debt collection case:

- Summons and Complaint: These documents tell you who is suing you, how much is claimed, and what you need to do next. Review them carefully and note the response deadline.

- Filing an Answer: You submit a written response to the court, confirming or disputing the debt. This is your chance to present facts, not emotions, and to request documentation.

- Court Review or Hearing: Once you respond, the court may schedule a hearing or encourage mediation. Both sides can share information or discuss settlement options.

- Negotiation or Settlement: Many cases end before trial. You can agree to a payment plan, a lump-sum settlement, or a reduced balance through direct communication.

- Judgment Issued: If the court rules in favor of the creditor, a judgment confirms the amount owed. It can appear on your credit report and may later result in wage or account actions, but these steps involve notice and a period of time.

A judgment does not mean the end of your financial stability. It simply marks a point where repayment becomes formalized. You can still take proactive steps to manage the outcome, rebuild your credit, and regain control.

Now that you understand how the process unfolds, the next section will walk you through what to do first and how to respond effectively.

Suggested Read: Understanding Medical Bills and Collections: Know Your Rights

Response Plan After Receiving a Lawsuit Notice

As the Ohio State Bar Association notes, “You are only responsible for your debt, and no one else’s.”

That reminder is key. It means that every debt lawsuit deserves careful attention, not fear. The goal is not to panic or rush, but to approach each step with understanding and confidence.

Step 1: Stay Calm and Read Everything

Your first response sets the tone for the entire case. Opening and reading every document helps you understand what is being claimed and by whom; nothing more, nothing less.

Here’s what to look for in your paperwork:

- The summons and complaint (who is suing you and for how much).

- The deadline to respond (usually 20–30 days from the date served).

- Any case number or court details for filing your reply.

Remaining calm keeps you focused. Most deadlines are firm but manageable, and understanding them early helps you stay ahead.

Step 2: Verify the Debt

Not every lawsuit is valid, and not every debt is accurate. Before responding, make sure the amount, creditor name, and account details are correct.

Here’s what to review before taking action:

- Compare the claim to your credit reports and old statements.

- Check if the debt is past the statute of limitations in your state.

- Watch for duplicate or previously settled accounts.

Verification ensures you only respond to legitimate claims and protects you from paying a debt that is not yours.

Step 3: Know Your Rights

You have the right to ask for proof, to dispute inaccuracies, and to be treated fairly throughout the process. The Fair Debt Collection Practices Act (FDCPA) protects you from harassment or misleading practices.

Here’s what your rights include:

- Requesting debt validation in writing.

- Being free from threats, intimidation, or repeated calls.

- Receiving accurate information about your debt and your options.

Knowing your rights gives you confidence to engage from a position of clarity, not fear.

Step 4: Respond to the Lawsuit

Filing an Answer is the most critical step. It prevents a default judgment and ensures the court hears your side of the story.

Here’s what to include in your response:

- State whether you admit, deny, or lack knowledge about each claim.

- Assert valid defenses, such as expired statute of limitations or identity errors.

- File your response before the deadline and keep copies for your records.

Your response does not have to be perfect. It just needs to be timely and truthful.

Step 5: Consider Legal Help

Even if the debt is small, professional advice can make a big difference. Many legal aid organizations or consumer law attorneys offer affordable or free consultations.

Here’s where to find help:

- Legal aid offices or nonprofit law clinics in your area.

- State bar associations with referral programs.

- Consumer protection attorneys experienced in debt defense.

Having guidance can help you avoid errors, identify defenses, and negotiate from a stronger position.

Step 6: Explore Settlement or Repayment Options

Not all debt lawsuits end in court judgments. Many are resolved through communication and cooperation. Reaching an agreement can help you close the matter faster and with less stress.

Here’s what to explore before trial:

- Negotiate a lump-sum settlement or structured payment plan.

- Request written confirmation of any agreement before paying.

- Work with trusted organizations that offer flexible, transparent repayment options designed to help you regain control.

Settlements turn confrontation into resolution and give you a clean starting point for rebuilding your finances.

Step 7: Show Up in Court If Required

If a court appearance is scheduled, attending shows responsibility and respect for the process. It also gives you the chance to share your side directly with the judge.

Here’s how to prepare for your appearance:

- Bring all documents, receipts, and correspondence related to the debt.

- Dress neatly and arrive early to check in.

- Speak clearly and respectfully when addressed by the court.

Showing up matters. It keeps the process fair and often leads to more understanding outcomes.

Working with The Forest Hill Management can make managing your receivables and collection obligations far less stressful. Our tailored repayment plans, transparent communication, and flexible scheduling support you while you navigate your debt and account-management path.

With our guidance, you can move from reacting to your debt to confidently managing it. Contact us today.

Suggested Read: How Does Debt Consolidation Affect Your Credit Score?

What Happens If You Ignore a Debt Collection Lawsuit?

A recent report from the National Center for State Courts suggests that the rise in debt collection lawsuits may, in part, stem from automated filing systems that use artificial intelligence to process claims in bulk.

This means some lawsuits could contain errors in the form of wrong amounts, outdated debts, or even mistaken identities. Ignoring the summons gives those mistakes power.

By staying silent, you lose the opportunity to correct false claims and protect your rights. If you ignore a debt collection lawsuit, here’s what typically happens:

- Default Judgment Issued: The court automatically rules in favor of the creditor because you did not respond, even if the claim has errors.

- Wage Garnishment: Once a judgment is in place, the creditor can ask the court to withhold part of your paycheck until the debt is paid.

- Bank Account Levy: Creditors may seek permission to withdraw funds directly from your bank account to satisfy the judgment.

- Property Liens: In some cases, a lien can be placed on property you own, affecting future sales or refinancing.

- Credit Score Impact: A judgment appears on your credit report and can remain for up to seven years, reducing access to new credit or loans.

While these outcomes sound serious, they are not inevitable. Responding with a simple denial or request for proof can pause the process and give you time to review, negotiate, or dispute the claim.

Understanding what happens if you do nothing highlights the importance of taking action. Next, we will look at ways to identify and assert your rights when a lawsuit may not be as clear-cut as it seems.

Suggested Read: Top 12 Proven Steps to Becoming Financially Stable

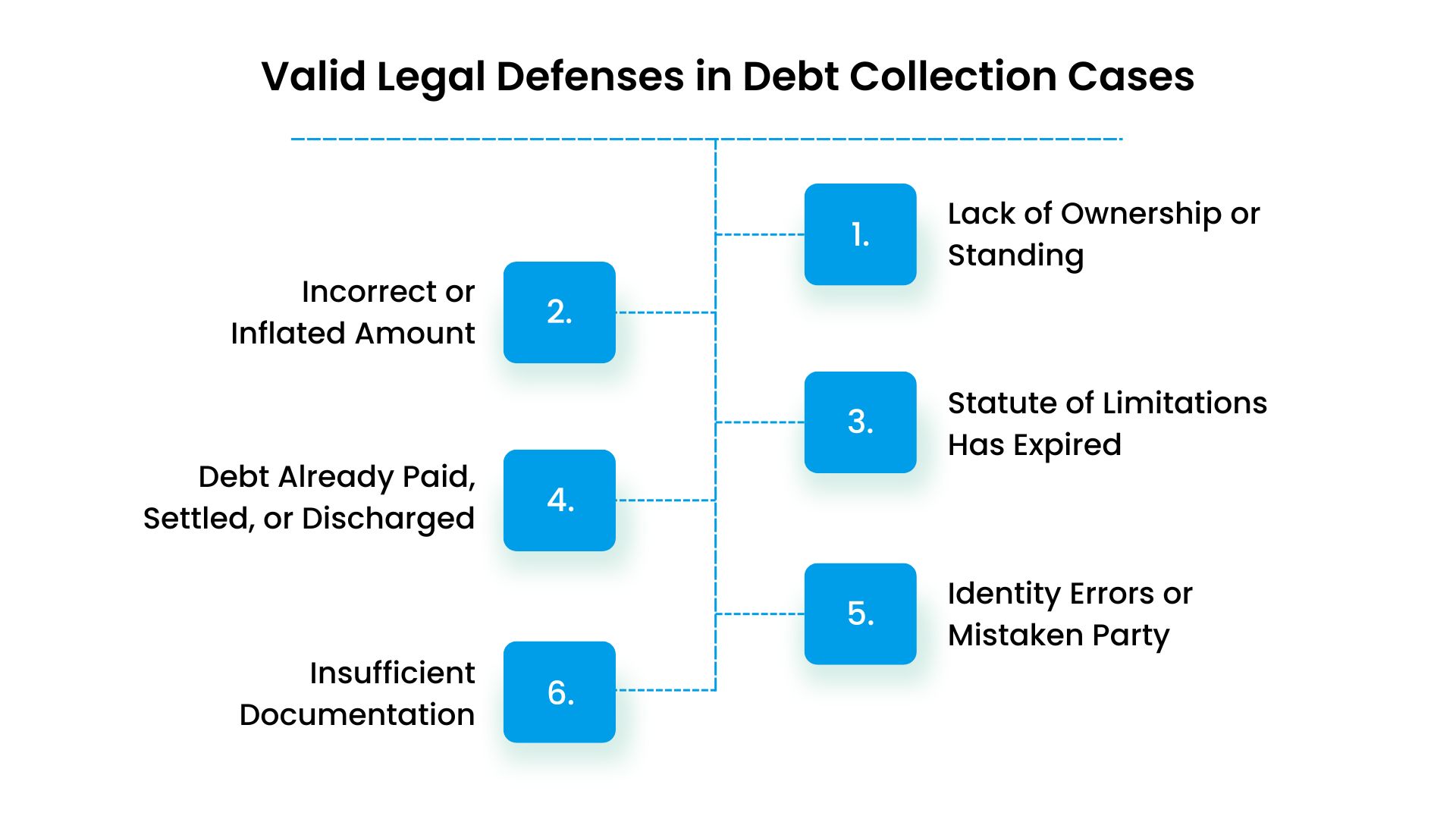

Valid Legal Defenses in Debt Collection Cases

Not every debt collection lawsuit is accurate or legally enforceable. Creditors and debt buyers must prove that the debt is legitimate, that they have the right to collect it, and that they have followed all applicable laws. Understanding common legal defenses helps you respond effectively — and ensures that you only pay what you truly owe.

Here are some valid defenses that may apply in debt collection cases:

- Lack of Ownership or Standing: The company suing you must prove it owns the debt. If the debt was sold multiple times, they must show a complete paper trail from the original creditor to them.

- Incorrect or Inflated Amount: Errors in calculations, unauthorized fees, or double-counted interest can make the claimed amount inaccurate.

- Statute of Limitations Has Expired: Each state limits how long a creditor can sue after a missed payment. This is typically three to six years. Once expired, the debt may still exist but cannot be collected through the courts.

- Debt Already Paid, Settled, or Discharged: If you have already paid or settled the debt, or if it was discharged in bankruptcy, the lawsuit is invalid.

- Identity Errors or Mistaken Party: Sometimes lawsuits are filed against the wrong person due to similar names, shared addresses, or outdated records.

- Insufficient Documentation: The creditor must provide original contracts, account statements, and assignment records, since without these, they cannot prove the claim.

If any of these situations apply, you can raise them in your response or discuss them with an attorney before the court date.

Presenting a valid defense does not erase the debt instantly, but it can prevent an unfair judgment and give you time to negotiate or verify the facts. The next section lists other ways you can protect yourself during this process.

How to Protect Yourself During the Process

Small, proactive measures can make a major difference in how the case unfolds. Beyond simply “showing up,” there are strategic ways to safeguard yourself from unnecessary stress, errors, and escalation.

Here are five ways to protect yourself during a debt collection case that most people overlook:

1. Keep a Communication Log

Document every phone call, email, and letter with the creditor or collector, including dates, times, and names. A detailed log can become valuable evidence if there are inconsistencies or violations of the Fair Debt Collection Practices Act (FDCPA).

2. Request All Communication in Writing

Politely ask that the collector communicate in writing only. This prevents misunderstandings, gives you a paper trail, and helps you avoid emotional pressure from phone conversations.

3. Review Court Filings for Accuracy

Errors occur more frequently than people realize, with amounts, dates, or even names being incorrect. Check all filings closely and compare them to your own records. Request corrections through the court if needed.

4. Freeze Unnecessary Credit Activity

Pause new applications for loans or credit cards until the case is resolved. New credit inquiries or accounts can complicate settlement discussions or appear as instability during negotiations.

5. Check for Improper Service or Filing Errors

Courts require that you be properly “served” with notice of a lawsuit. If you never received proper service or the plaintiff filed in the wrong venue, that can be a valid procedural defense.

Protecting yourself is about staying one step ahead: organized, informed, and intentional. When you know what to document and when to act, you shift from defense to control.

In the next section, we examine how taking action before a lawsuit escalates can simplify repayment and mitigate the long-term financial impact.

Explore Repayment Options Early with The Forest Hill Management

At Forest Hill Management, we believe that financial challenges should be resolved through understanding, not pressure. Our goal is to help individuals take control of their obligations before they ever become overwhelming.

By offering flexible repayment plans, clear communication, and a human approach to account management, we help you handle collection-related debt proactively, though you may still need legal advice for court representation.

Here is how Forest Hill Management supports you every step of the way:

- Personalized Repayment Solutions: Every financial situation is unique. We create repayment plans tailored to your budget and timeline, helping you stay consistent while maintaining balance in your everyday life.

- Flexible Payment Options: Whether online, by phone, or through scheduled arrangements, we provide multiple ways to make payments that fit your routine.

- Transparent Communication: We believe clarity builds trust. Our team explains every step, ensuring you understand your account, payments, and options with no surprises, ever.

- Compliance and Data Security: All processes follow strict legal and privacy standards, keeping your financial information safe and handled with care.

- Supportive Account Assistance: Our representatives listen before they act. We focus on helping you regain stability with respect, professionalism, and compassion.

Addressing debt early opens the door to peace of mind and long-term financial control. With Forest Hill Management by your side, you can take proactive steps now. Reach out today to explore how a personalized repayment plan can help you regain clarity and move confidently toward financial freedom.

Conclusion: Turning a Lawsuit Into a Fresh Start

Receiving a summons can feel intimidating, but it is not the end of the world. It is simply a call to action. It is an opportunity to understand the claim, gather information, and speak directly with the agency before anything escalates.

In many cases, honest communication and negotiation lead to repayment or resettlement options that are fair, manageable, and far less stressful than going through the courts. Taking initiative early shows responsibility and puts you back in control of your financial journey.

At Forest Hill Management, we are here to make that process smoother. Our flexible repayment plans, transparent communication, and supportive approach are designed to help you close this chapter with confidence and clarity. We focus on simplifying repayment, so you can move forward, debt-free and worry-free.

Take control of your next step. Contact us to discuss personalized repayment options.

Frequently Asked Questions

1. If I don’t win in court, can the creditor take all my money?

No, creditors cannot take all your money. Even after a judgment, certain income sources, like Social Security, disability benefits, and a portion of your wages, are protected by law. Most states limit how much can be garnished, ensuring you still have enough for basic living expenses.

2. How much time do I have to respond to the lawsuit?

You generally have 20 to 30 days from the date you receive the summons to file your response, depending on your state’s rules. The exact deadline is listed on your court papers, so review them carefully. Filing your response on time is critical to prevent a default judgment.

3. What happens if I pay the debt after being sued?

If you pay or settle the debt after a lawsuit has been filed, the creditor must notify the court, and the case can be dismissed or marked as resolved. Always get a written confirmation of payment or settlement before sending any money.

4. Can I negotiate with the creditor after being sued?

Yes, you can still negotiate even after receiving a lawsuit notice. Many creditors are open to discussing lump-sum settlements or structured repayment plans to avoid court proceedings, especially if you communicate early and in writing.

5. Will a debt collection lawsuit affect my credit score?

Yes, a judgment or unpaid collection account can appear on your credit report and may lower your score temporarily. However, once the debt is paid or settled, your report will reflect the updated status, and your credit can begin to recover over time.