Distressed Loan Meaning, Causes, and How You Can Recover

Need Help Reviewing Your Account?

Contact UsA loan can feel manageable at first, then life shifts, and the numbers stop working. A paycheck changes, bills rise, or an unexpected event stretches your budget. Soon, payments feel harder to make on time, and stress grows with every notice or call.

A distressed loan describes that moment when repayment becomes unstable, and the account shows signs of serious strain. The good news is that many distressed loans improve with the right steps and a realistic plan.

This guide explains what a distressed loan means, why it happens, what usually comes next, and how you can move toward recovery with clarity and confidence.

Key Takeaways

- Early action creates options. The sooner you respond, the more paths you have to stabilize payments and reduce pressure.

- A plan beats guesswork. Clear steps and a realistic budget turn uncertainty into steady progress.

- Your rights support peace of mind. Knowing what lawful communication looks like helps you stay calm and in control.

- Support makes progress easier. The Forest Hill Management helps you follow a clear path with secure payments and flexible options.

What is a Distressed Loan?

A distressed loan is a loan that shows serious repayment strain. It usually means payments are late, missed, or at risk, and the current terms no longer fit your financial situation.

In everyday terms, a distressed loan is a loan where making payments as agreed has become difficult or unstable.

Common signs your loan is becoming distressed

You may notice one or more of these signals.

- Payments feel harder to make each month

- Late payments happen more often

- You rely on credit to cover basics

- Minimum payments rise while income stays flat

- You receive more account notices or calls

- You consider skipping one bill to pay another.

These signs help you act early, when solutions feel more flexible.

Also Read: Debt Stacking: How to Prioritize and Pay Off Debt

Why Do Loans Become Distressed?

A loan rarely shifts overnight. Most distressed loans follow a pattern of pressure that builds over time.

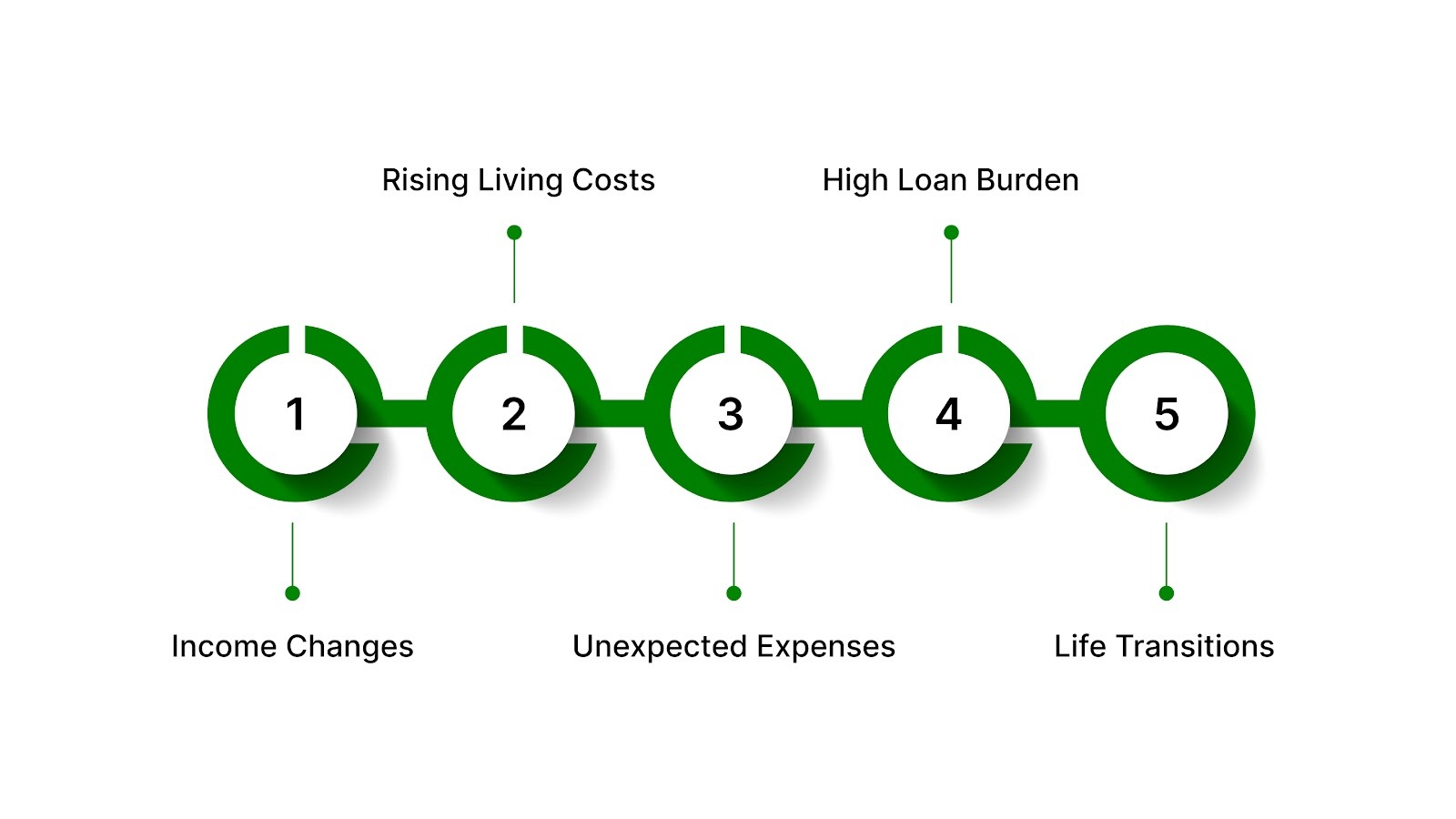

1) Income changes

Job changes, reduced hours, gig work variability, or benefit changes can tighten your monthly margin. When income drops, loan payments feel heavier.

2) Rising living costs

Rent, groceries, utilities, and insurance can rise while your budget stays the same. That squeeze often hits debt payments first.

3) Unexpected expenses

Medical bills, car repairs, family support, or emergency travel can pull money away from your payment plan.

4) High payment structure

Some loans carry terms that strain cash flow, such as high interest, short repayment timelines, or stacked monthly obligations across multiple accounts.

5) Life transitions

Moving, divorce, caregiving, or other major shifts can disrupt routines and budget planning. Even a temporary change can trigger late payments.

When you recognize the cause, you can choose a response that fits your reality, not a one-size path.

Also Read: Why One-Size-Fits-All Debt Solutions Don't Work for Real Relief

What Happens When a Loan Becomes Distressed

When a loan becomes distressed, the situation can feel urgent. You may see more account activity, more communication, and more pressure in your day-to-day life. Knowing what usually happens next helps you stay calm and make better decisions.

1. Account status changes

Most lenders track accounts by how far payments are past due. As time passes, the account may move into a more active management stage.

That can mean clearer reminders, more frequent notices, or new account handling steps.

Common signs include:

- Missed payments that repeat over multiple months

- Partial payments that do not cover the full amount due

- Requests for extensions or schedule changes

- Increasing contact attempts about overdue balances.

2. Credit impact

Late payments can affect your credit report. That impact can feel discouraging, but consistent payments under a realistic plan can help stabilize your credit over time. When you move into consistent payments through a realistic plan, you create a path toward long-term improvement.

A helpful focus point is consistency. One steady plan often supports better outcomes than repeated short-term fixes.

3. More communication

Communication often increases during distress. You may receive letters, emails, or calls asking you to confirm details or discuss next steps.

You can respond with structure by taking a few simple steps.

- Ask for your current balance and payment status in simple terms

- Request written confirmation of any payment plan or agreement

- Save reference numbers, payment receipts, and dates in one folder

- Note the name and role of anyone you speak with.

This habit reduces confusion and keeps you in control.

4. Risk of escalation

If distress continues without a plan, the risk of stronger actions increases over time. Many people reduce that risk by choosing a payment path early and sticking to it. A realistic plan can reduce stress and create a clearer future.

Also Read: Is Debt Settlement a Good Idea for You?

What to Do if Your Loan is Sold or Transferred

When payments fall behind, you may receive notices from a new company. Your loan may be transferred to a new servicer or assigned to a new account manager, without creating a new loan or changing your original obligation. This change can feel confusing, and you can handle it with a few simple checks.

Step 1: Confirm the details before you pay

Use written notices to verify

- The company name

- Your account number

- The payment address or secure payment link

- The customer support contact details.

If anything feels unclear, pause and ask for confirmation. Clarity protects you from sending money to the wrong place.

Step 2: Keep your records organized

A transfer is easier when you track your information in one place. Save

- Notices or emails about the transfer

- Payment confirmations and receipt numbers

- Screenshots of payment instructions

- Dates and notes from calls.

A simple folder on your phone or computer often works well.

Step 3: Expect what usually stays the same

In many cases, the core terms stay consistent. Your balance and payment obligations often remain the same, while the servicing process changes. The biggest shift is usually where you make payments and where you ask questions.

Step 4: Use secure payment options when available

Secure online payments reduce confusion and help you track progress. Clear receipts, confirmation numbers, and payment history visibility support peace of mind during transitions.

Also Read: How to Effectively Manage and Reduce Debt

Options That Can Help You Recover

A distressed loan can feel heavy, and you still have practical options. The right choice depends on your income, the account status, and what you can sustain month to month.

1) Payment plan adjustments

A structured repayment plan can bring stability fast. Adjustments may include

- Smaller payments spread across more time

- A schedule aligned with your pay dates

- A plan that prioritizes consistency over speed.

A plan works best when it fits your real budget, not your best month.

2) Loan modification

Some loans allow term changes that make payments more realistic. This may involve adjusted interest, a longer timeline, or a revised monthly amount.

A modification works best when your income changed long-term, and you need stability, not a temporary pause.

3) Settlement discussions

In some cases, you may resolve the account through an agreed-upon payoff amount, depending on eligibility and confirmation of terms in writing. This option depends on eligibility, timing, and what you can reasonably pay without creating new hardship.

4) Short-term relief steps

If your hardship is temporary, a short-term arrangement may help you regain your footing. A short-term solution can create room to stabilize income and return to steady payments.

How to choose the right option

A simple decision guide helps.

- If your hardship is temporary, short-term relief or a schedule adjustment may fit

- If your income changed long-term, a modification or structured plan may fit better.

- If the balance feels unmanageable, a structured resolution discussion may provide clarity.

Questions that help you choose

- What monthly amount supports essentials and reduces stress?

- What changes if you pay early?

- What happens if you miss one payment?

- How will you receive written confirmation of the agreement?

Also Read: Strategies for Paying Off Personal Loans Faster

A Simple Recovery Plan You Can Start Today

Progress feels easier when you follow clear steps. Use this quick checklist to organize your next move.

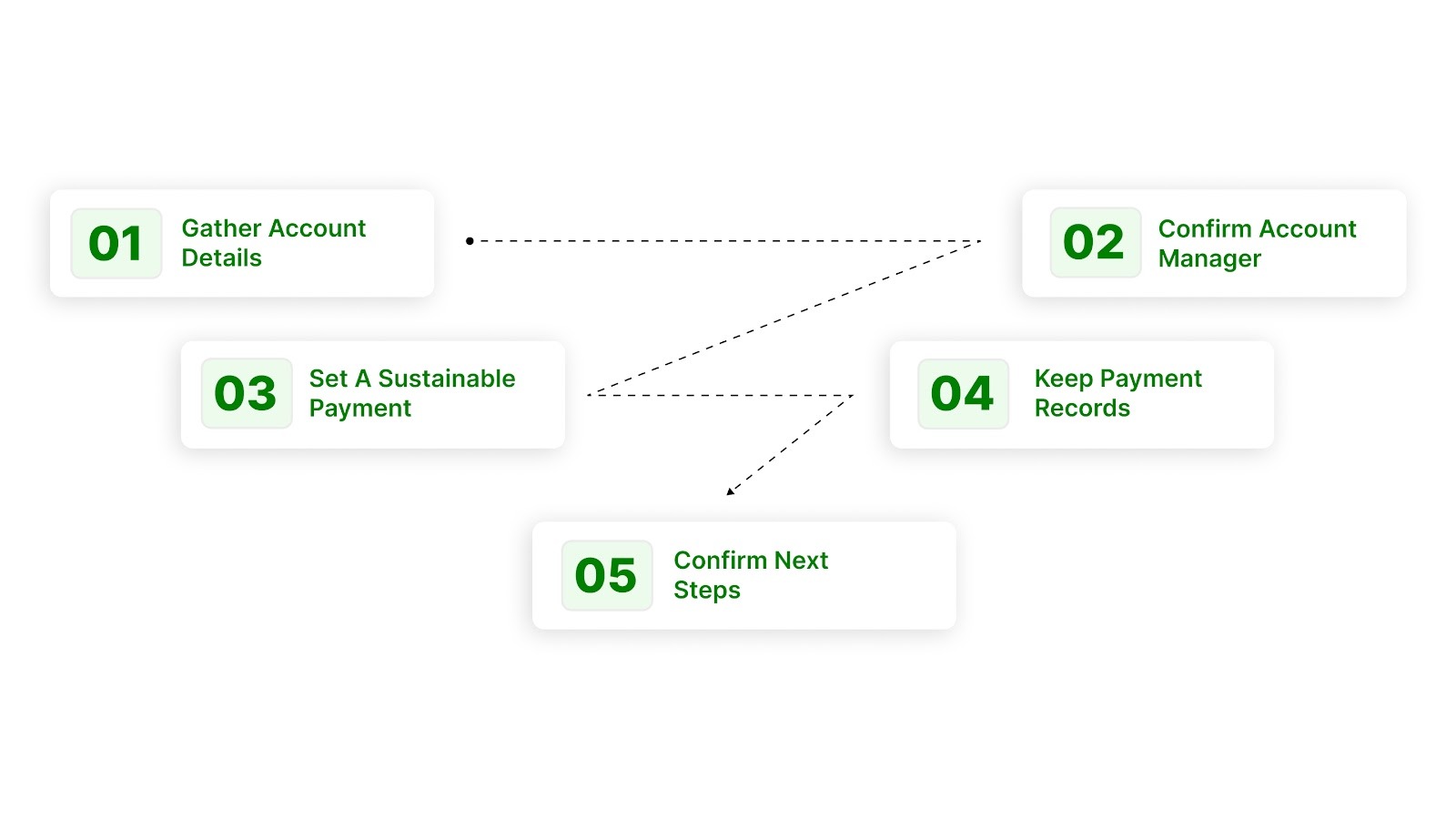

Step 1: Get your facts in one place

Gather the basics:

- Account statements or notices

- Current balance and monthly payment amount

- Due dates and recent payment history

- Any letters or emails about the account.

Step 2: Confirm who manages the account

If you received new notices, confirm the company name, contact details, and payment instructions. Use official channels listed in written communications.

Step 3: Choose a realistic monthly amount

Start with what you can sustain. Consistency supports stability.

A helpful way to test your number:

- List fixed expenses

- List essentials like food and transportation

- Reserve a small buffer for surprises

- Choose a payment amount that fits what remains.

Step 4: Keep a clear record

Save confirmation numbers, receipts, and written communications. Keeping everything in one folder can reduce stress and make tracking progress easier.

Step 5: Ask for clear next steps

When you speak with an account manager, ask for:

- Total balance and payment schedule

- What changes after each payment

- What happens if you pay early

- Written confirmation of any agreement.

Also Read: Impact Of The Debt Relief Plan On Your Financial Future

How to Prepare For a Repayment Conversation

A repayment conversation feels easier when you bring clear numbers and a realistic goal. Preparation helps you stay calm and choose a plan you can follow.

What to gather before you speak with anyone

- Your most recent notice or statement

- Your income amount and pay dates

- A simple list of essential expenses

- Your realistic monthly payment range

- Any payment receipts you already have.

A simple approach that keeps you in control

Start with one goal. You want a plan you can follow consistently.

You can say

- “I want a realistic plan I can follow each month.”

- “Here is the amount I can pay on time based on my budget.”

- “Please confirm the next steps and send details in writing.”

Questions that protect clarity

Ask for

- Your total balance and the next due date?

- How are payments applied and recorded?

- What confirmation will you receive after each payment?

- What happens if you pay early?

Preparation reduces stress and helps you move from uncertainty to a structured path forward.

How Does The Forest Hill Management Help You?

When loan stress builds, clarity and structure help you move forward. The Forest Hill Management supports individuals navigating unpaid accounts and financial pressure through lawful, transparent account management focused on practical resolution.

Here is how The Forest Hill Management supports individuals working through distressed loan situations.

- Secure online payments so you can pay safely, track progress, and reduce confusion

- Flexible repayment options designed to match your situation and support steady improvement

- Personalized guidance that helps you understand where you stand and what comes next

- Compliant, respectful communication that protects your rights and supports peace of mind

You move forward with clear steps, realistic expectations, and support that centers on progress, not pressure.

Conclusion

A distressed loan marks a stressful season, and it also opens a chance to reset your plan. Clear information, steady steps, and realistic repayment options can move you from overwhelm to progress.

If you want support that keeps the process structured, compliant, and easier to manage, reach out to The Forest Hill Management. You will get secure payment options, flexible repayment paths, and guidance that helps you regain financial control.

You can contact The Forest Hill Management to explore clear next steps toward stability and peace of mind.

FAQs

1) What is a distressed loan?

A distressed loan means your loan shows serious repayment strain, such as repeated late payments or missed payments. It signals a need for a clear plan that fits your current budget.

2) Can a distressed loan improve?

Yes. Many distressed loans improve when you act early and follow a structured repayment plan. Consistent payments and clear agreements often support long-term stability.

3) What happens if my account transfers to a new company?

You may see new payment instructions and new contact details. Confirm the new details using official written notices and keep records of your payments and communications.

4) How does a distressed loan affect credit?

Late payments can affect your credit profile. A realistic plan and steady progress often support improvement over time, especially when payments become consistent.

5) When is the right time to seek support?

The best time is when payments start feeling unstable. Early support helps you choose options that reduce pressure and protect your path forward.