Effective Portfolio Management Best Practices Guide

Transform Your Financial Future

Contact UsManaging your finances can often feel reactive, balancing high-interest debt, protecting your credit score, and trying to make progress without a clear plan. But long-term financial stability isn’t built through isolated decisions; it comes from structure and strategy.

By applying portfolio management best practices to your personal finances, you can organize your debts, income, and expenses into a clear, manageable system.

This approach helps you prioritize what matters, reduce risk, and allocate resources intelligently, turning scattered financial obligations into a clear, goal-driven roadmap for financial recovery and long-term stability.

Key Takeaways

- Every major financial decision should align with a specific long-term life goal to remain purposeful and sustainable.

- Use your credit score and interest rate data to drive every decision, rather than relying on emotional impulses.

- Clear personal financial rules or a structured budget remove stress from daily money decisions.

- Your limited resources (time and money) should be allocated to the debts or financial obligations that provide the greatest relief or cost reduction over time.

- Working with knowledgeable, compliant support services can help you understand options and manage debt more confidently.

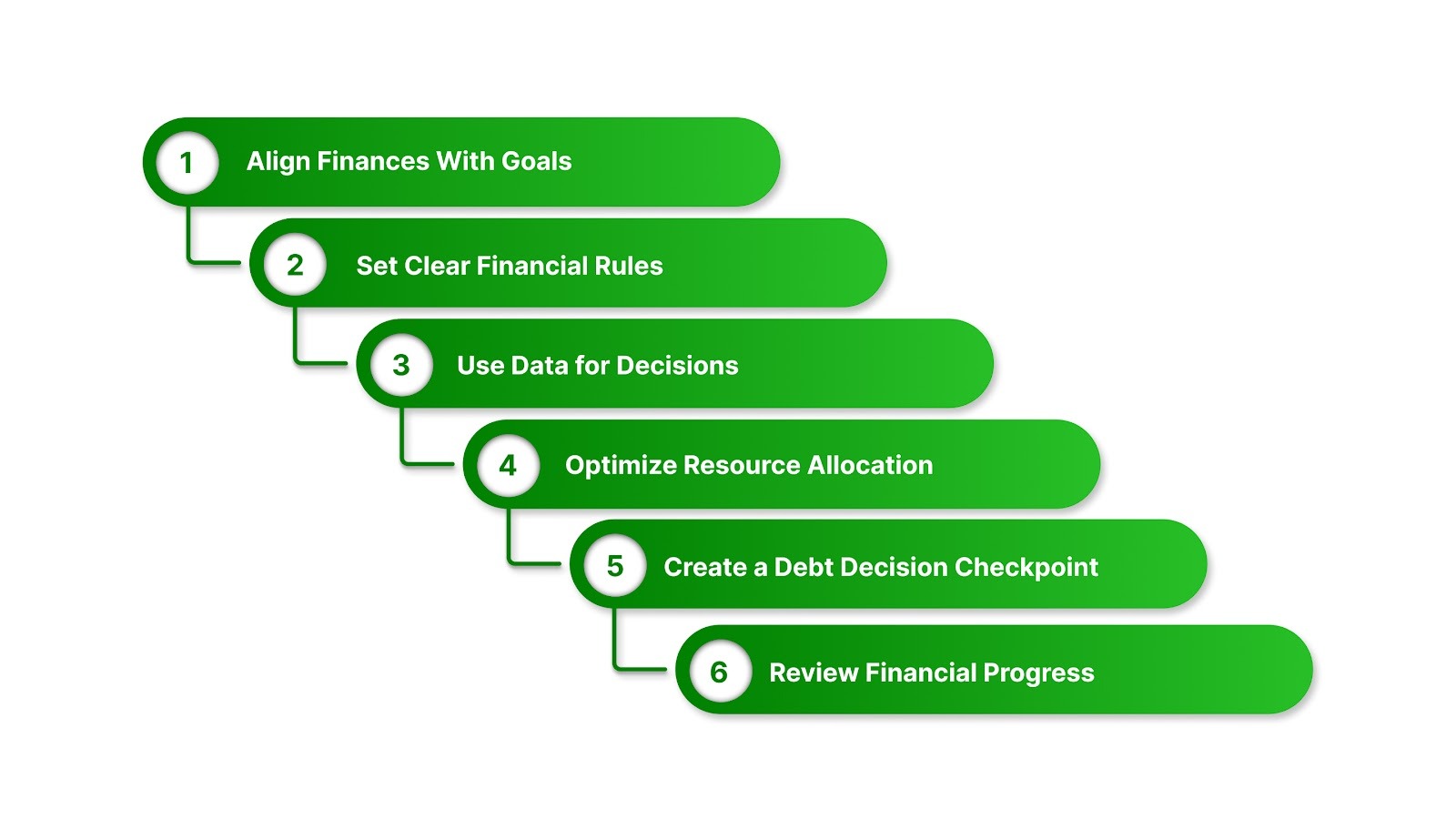

6 Portfolio Management Best Practices

Transforming your financial life requires moving away from reactive habits and adopting a structured, repeatable approach. By treating your debts, bills, and financial obligations as part of one connected financial picture, you can make decisions that prioritize long-term stability over short-term stress.

These portfolio management best practices provide the essential blueprints you need to navigate the complexities of modern personal finance with confidence and clarity.

1. Align Your Financial Decisions With Personal Goals

In personal finance, financial stability comes from making sure each major decision supports your long-term goals. In your personal life, your long-term goals guide financial decisions, whether that means buying a home, retiring early, or living free from collection calls.

Defining The Practice

Aligning your finances means reviewing every dollar you spend or borrow against your long-term goals. If a purchase doesn't bring you closer to financial independence or provide a necessary utility, it doesn't fit your strategy.

Implementation Tips

- Write Your Mission Statement: Define what financial success looks like for you in three sentences.

- Calculate the Cost Impact: Before paying off a debt, ask: ‘Will paying this down save me more in interest or fees than alternative uses of this money?'

- Audit Your Subscriptions: These recurring expenses quietly affect your overall financial picture.

Common Challenges

The biggest hurdle is "emotional spending." When we are stressed about debt, we often spend money to find temporary relief. By aligning with a strategy, you create a logical barrier against these impulses.

2. Set Clear Personal Financial Rules

Having clear financial rules may sound rigid, but it reduces stress and confusion over time. It is the set of rules, roles, and processes you use to manage your money.

Defining The Practice

Clear personal financial rules mean setting non-negotiable guidelines for how money enters and leaves your budget. It involves deciding who makes decisions (you or a partner) and what criteria must be met before taking on new debt.

Benefits of Clear Financial Rules

- Reduced Decision Fatigue: You don't have to wonder if you can afford a meal out; the rules are already decided for you.

- Consistency: Clear rules ensure debt payments continue even during busy or stressful periods.

- Accountability: It gives you a clear way to measure progress and identify areas that need adjustment.

Also Read: How to Effectively Manage and Reduce Debt

3. Implement Data-Driven Decision Making

In 2026, guessing about your finances is no longer necessary. With newer credit-reporting tools that integrate cash-flow and banking data, consumers now have access to more actionable financial information than ever before.

Defining The Practice

Data-driven decision-making means looking at the hard numbers, your debt-to-income ratio, your weighted average interest rate, and your credit utilization, before making a move.

How To Use Data

- Track Your Interest Cost: How much money is lost to interest each month?

- Monitor Your Utilization: Keeping your credit card balances below 30% of their limits is a widely recognized data-driven method that may help improve credit profiles over time.

- Analyze Trends: Are your expenses increasing or decreasing? Use an app to visualize your spending over the last six months.

Impact On Personal Financial Management

By using data, you move from reacting emotionally to making informed, practical financial decisions. You can see exactly how a $100 extra payment on a high-interest card will affect your overall financial progress over the next year.

4. Optimize Resource Allocation

Your resources are limited: you only have a certain amount of income and a certain number of hours in a day. Good financial planning means directing limited money toward the debts that cause the most harm.

The Debt Snowball vs. The Debt Avalanche

Two of the most popular resource allocation strategies are:

- The Debt Snowball: Allocating extra resources to your smallest balance first. This creates psychological "quick wins" that keep you motivated.

- The Debt Avalanche: Allocating extra resources to the debt with the highest interest rate. This approach is often considered more cost-efficient over time due to reduced interest accumulation.

Balancing The Budget

Optimizing resources also means knowing when not to pay down debt. If you don't have an emergency fund, your "resource allocation" should prioritize saving $1,000 to $2,000 before aggressively attacking your credit cards. This prevents a single car repair from sending you back into a debt spiral.

Suggested Read: Is Paying Debt Collection Agencies a Bad Idea?

5. Create a Spending and Debt Decision Checkpoint

Every new loan, credit card, or recurring expense adds another financial obligation to your budget. Healthy personal finances benefit from a simple decision checkpoint before taking on new obligations.

Defining The Practice

A spending checkpoint is a 24-hour to 7-day waiting period before any significant financial commitment. It involves asking:

- Does this decision support my overall financial goals?

- Do I have the "resource capacity" (money) to handle the monthly cost?

- What is the "exit strategy" (payoff plan) for this debt?

Benefits

By vetting your intake, you avoid "bad debt", the kind of high-interest consumer debt that depreciates and clogs up your overall financial picture. This keeps your financial life lean and focused on stability and progress.

6. Review Your Financial Progress Regularly

Personal finances are not ‘set it and forget it’; they require regular attention to stay aligned as economic conditions change.

Defining The Practice

Set aside time each month to review your financial progress.

- Did my net worth increase?

- Did my total debt decrease?

- Did my credit score improve?

Adjusting When Circumstances Change

If your performance review shows that you are falling behind, you must be willing to "pivot." This might mean cutting more expenses, finding a side hustle, reaching out for professional debt-related support, or account management assistance. Resilience in the face of a bad month is what separates those who get out of debt from those who stay in it.

Conclusion

Taking a structured, organized approach to your personal finances can significantly reduce stress and uncertainty.

By aligning your spending with your life goals, establishing clear financial rules, and making decisions based on hard data, you are setting yourself up for a financial comeback that lasts.

Your Roadmap To Success:

- Define your "Why": Align your payments with your future.

- Build your Rules: Establish a budget and stick to it.

- Analyze the Data: Know your interest rates and credit score.

- Allocate Resources: Prioritize the debts that hurt the most.

- Manage the Risk: Get professional help when the storm gets too heavy.

The Forest Hill Management is available as a supportive resource in this financial management journey. Whether you need to make a secure payment online or need clear, compliant account support to navigate your debt, Forest Hill Management is here to help.

Frequently Asked Questions About Portfolio Management

1. How is "Portfolio Management" different from just budgeting?

Budgeting is about tracking money in and out. Portfolio management is a broader personal finance approach that looks at how your debts, income, and goals interact to improve financial stability and reduce risk.

2. Can I use these best practices if I have a low credit score?

Absolutely. In fact, these practices are more important for those with low scores. Data-driven decision-making and clear financial rules are some of the fastest ways to rebuild your credit profile.

3. What is the "ROI" of paying off debt?

Think of it this way: if you have a credit card with a 24% interest rate, paying it off avoids ongoing interest costs that can significantly slow financial recovery. Very few investments can match that.

4. How do I manage the risk of wage garnishment?

The best way is through proactive communication. If you cannot pay, don't hide. Use services like The Forest Hill Management to negotiate flexible repayment options before the situation escalates to a legal level.

5. Why is "Project Intake" important for my finances?

Most people fall into debt through a "thousand small cuts", small subscriptions and minor loans that add up. An intake process stops the "leakage" before it starts.

6. Is the Debt Snowball or Debt Avalanche better?

Mathematically, the Avalanche is better because it saves you the most in interest. However, if you have struggled to stay motivated in the past, the Snowball's quick wins might be the better structured choice for you.