How to Manage Multiple Loan Repayments Effectively

Transform Your Financial Future

Contact UsManaging multiple loans does not usually feel overwhelming in the beginning. One credit card, one personal loan, maybe a car payment. But over time, those separate commitments start to overlap. Different due dates, different amounts, different logins. And suddenly, it feels like you are constantly trying to keep up.

The numbers reflect how common this has become. In 2025, more than 26.4 million Americans held a personal loan, and overall consumer debt continued to rise steadily across credit cards, auto loans, and other borrowing.

This means millions of people are not just managing one obligation, but several at the same time.

In this blog, you will learn how to manage multiple loans in a way that feels structured and realistic, how to organize your repayments, avoid common mistakes, and take steady steps toward regaining control.

Key Takeaways

- Managing multiple loans becomes easier when you bring all your accounts into one place and clearly understand your balances and due dates.

- The biggest challenge is not the number of loans, but the lack of structure in tracking and managing them.

- Covering minimum payments and focusing on one loan at a time helps create a steady and manageable repayment process.

- Simple systems like reminders, tracking, and record-keeping can significantly reduce missed payments and confusion.

- Consistency and clarity matter more than speed when working toward resolving multiple loan obligations.

Challenges of Managing Multiple Loan Repayments

Managing more than one loan at the same time can feel manageable at first, but it often becomes complicated as details start to overlap. Most challenges come from too many moving parts at once, which can create confusion and increase the risk of small mistakes over time.

Here are some of the most common challenges people face when managing multiple loan repayments:

- Keeping track of multiple due dates: Each loan may have a different billing cycle, which means you are managing several payment deadlines throughout the month. Without a clear system, it becomes easy to miss a date or lose track of what is due next.

- Not having a clear view of total obligations: When loans are spread across different accounts or platforms, it can be difficult to understand how much you owe in total. This lack of visibility can make planning and decision-making more stressful.

- Uncertainty about what to prioritize: When funds are limited, deciding which loan to focus on can feel unclear. Without a structured approach, you may end up spreading payments too thin or overlooking an account that needs attention.

- Higher risk of missed or delayed payments: Managing several accounts increases the chances of missing a payment, even unintentionally. Missed payments can lead to additional charges and further complicate the situation.

- Difficulty staying consistent over time: Even with a plan, maintaining consistency across multiple accounts can be challenging, especially if your financial situation changes or unexpected expenses arise.

- Emotional stress and mental fatigue: Constantly thinking about multiple payments, deadlines, and balances can feel overwhelming. This mental load can make it harder to stay organized and take clear next steps.

These challenges are common and do not mean you are doing something wrong. They simply highlight the need for a more structured way to manage your accounts.

Once you understand where the complexity comes from, it becomes easier to bring clarity and control back into the process.

How to Manage Multiple Loan Repayments Effectively

Managing multiple loans becomes easier when you approach it step by step, rather than trying to handle everything at once. The goal is not to clear all balances immediately, but to create a clear, consistent system that helps you stay organized and make steady progress over time.

Here is a structured approach you can follow to manage multiple loan repayments more effectively:

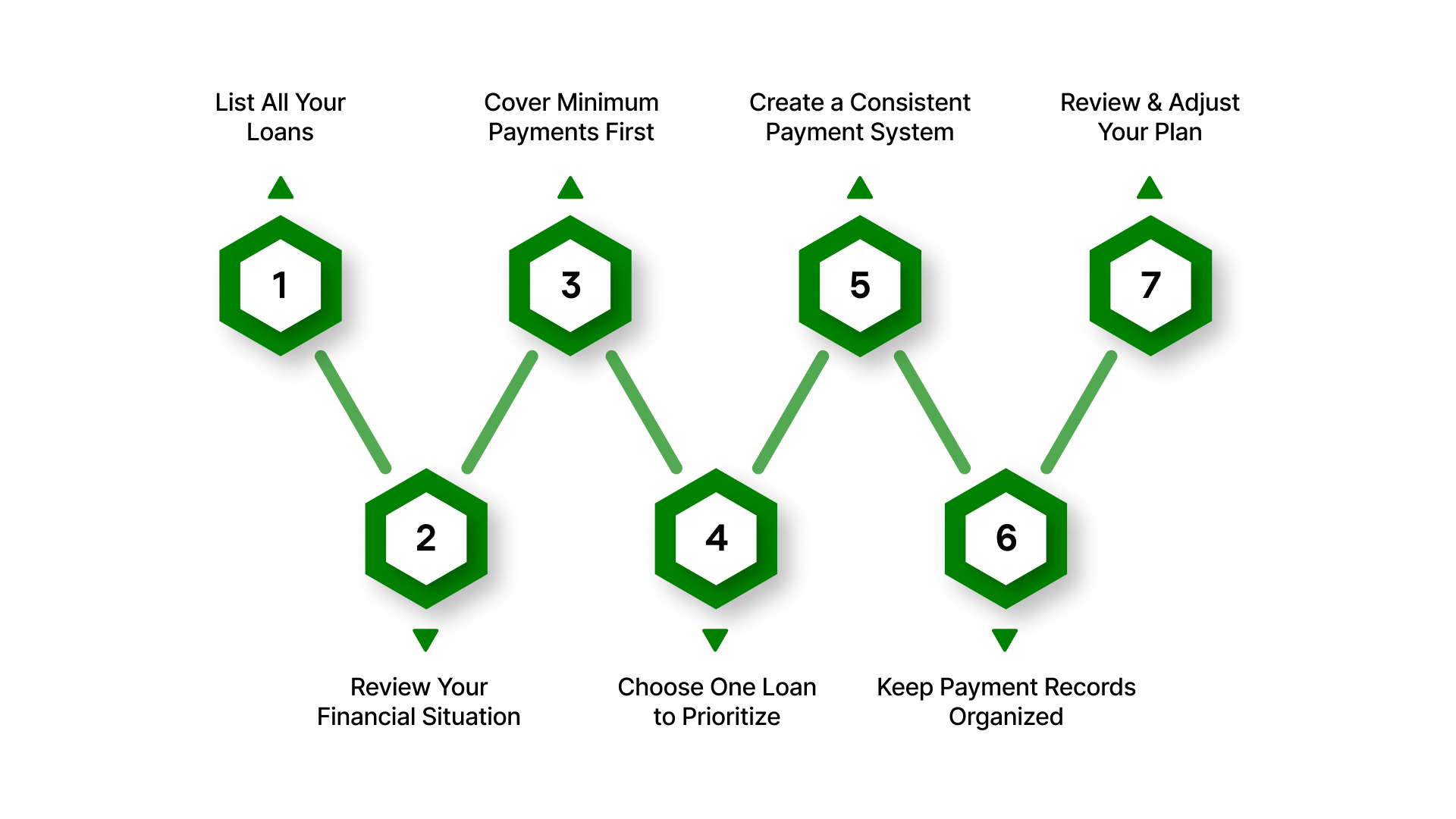

- Step 1: List all your loans in one place

Start by writing down every active loan you have, including balances, due dates, and minimum payment amounts. Having everything in one place gives you a clear picture of your total obligations and removes guesswork.

- Step 2: Review your current financial situation

Take a close look at your monthly income and essential expenses. This helps you understand how much you can realistically allocate toward loan repayments without creating additional financial strain.

- Step 3: Ensure minimum payments are covered

Make it a priority to meet the minimum payment requirement for each loan. This helps you avoid late fees, additional charges, and further complications across multiple accounts.

- Step 4: Decide which loan to focus on first

After covering minimum payments, choose one loan to prioritize. This could be based on urgency, balance size, or your current financial comfort. Focusing on one loan at a time makes the process more manageable.

- Step 5: Create a simple and consistent payment system

Organize your payment schedule by tracking due dates, setting reminders, or using scheduled payments where possible. A consistent system reduces the risk of missing payments and helps you stay in control.

- Step 6: Keep records of all payments and communication

Maintain a record of payment confirmations, account updates, and any communication related to your loans. This helps you track progress and ensures you have clarity if questions arise later.

- Step 7: Review and adjust your plan regularly

Your financial situation may change over time. Revisit your repayment plan periodically to make sure it still works for you, and adjust it if needed to stay consistent and realistic.

Managing multiple loans is not about doing everything perfectly. It is about creating a system that works for you and sticking to it.

Also read: 11 Best Tips to Pay Off Debt Fast

Once you have a clear understanding of your loans and the challenges involved, the next step is choosing a repayment approach that helps you stay consistent and in control.

Best 5 Strategies for Managing Multiple Loans

In many cases, a simple and steady plan is more effective than trying to manage everything at once without a clear system. The most effective strategy is one that fits your financial situation and feels manageable over time.

Below are some of the most commonly used strategies to help manage multiple loans more effectively.

Debt Avalanche Method (Focus on High-Interest Loans First)

This approach prioritizes paying off the loan with the highest interest rate while continuing minimum payments on the others.

Over time, this helps reduce the total amount of interest you pay and can make repayment more efficient financially. It is a structured method that works well if your goal is to minimize long-term costs.

Debt Snowball Method (Start with the Smallest Balance)

With this method, you focus on paying off the smallest loan first while maintaining minimum payments on all others.

Once one loan is cleared, you move to the next. This approach can create a sense of progress and motivation, which can be helpful if you are feeling overwhelmed by multiple balances.

Debt Consolidation (Combining Multiple Loans into One)

Consolidation involves combining several loans into a single payment, often with a different interest rate or repayment term.

This can simplify your repayment process by reducing the number of payments you need to track. However, it is important to fully understand the terms before choosing this option.

Balance Transfer Options (For Credit Card Debt)

In some cases, high-interest credit card balances can be transferred to a new card with a lower or temporary 0% interest rate.

This can provide short-term relief by allowing you to focus on reducing the principal amount. It is important to be aware of time limits and any associated conditions.

Automating Payments to Stay Consistent

Setting up automatic payments or reminders can help ensure that you do not miss due dates. This reduces the risk of late fees and helps maintain consistency across multiple accounts, especially when managing several payment schedules at once.

Also read: Debt Verification With The Forest Hill Management: What to Expect

Each of these strategies offers a different way to bring structure to multiple loan repayments.

Conclusion

Managing multiple loans can feel like you are constantly trying to stay one step ahead. What changes that is not a perfect strategy. It is clarity and consistency.

When you know exactly what you owe, when it is due, and what you can realistically manage each month, the situation becomes easier to handle. You stop reacting and start making decisions with more confidence.

If your account is being managed by The Forest Hill Management, you are not expected to figure this out on your own. The focus is on helping you understand your account clearly, keep your payments organized, and explore repayment options that actually fit your situation.

You do not need to fix everything at once. Start by understanding where you stand.

FAQs

1. Can I manage multiple loans without combining them into one?

Yes, you can manage multiple loans individually by organizing your payments, tracking due dates, and following a structured repayment plan that fits your financial situation.

2. What should I do if I lose track of one of my loans?

If you are unsure about an account, review your credit report or past statements to identify it, and then verify the details with the organization managing the account before making any payments.

3. Is it better to focus on one loan or pay all of them equally?

In most cases, it is helpful to maintain minimum payments on all loans while focusing extra effort on one, as this creates a clearer and more manageable repayment path.

4. How can I stay consistent if my income changes month to month?

If your income is not fixed, it helps to review your finances regularly and adjust your repayment plan so that it remains realistic and sustainable.

5. Should I speak to someone before deciding on a repayment approach?

Yes, if you feel unsure, speaking with the organization managing your account can help you understand your options and make more informed decisions.