11 Best Tips to Pay Off Debt Fast

Need Help Reviewing Your Account?

Contact UsDebt can build gradually, often through everyday expenses, unexpected emergencies, or periods of financial pressure. What begins as manageable borrowing can quickly feel overwhelming when interest charges, multiple bills, and rising living costs start competing for the same income.

Financial priorities across the country reflect this reality. Nearly 97% Americans say they have at least one financial priority for 2025, and the most common goal is reducing debt, cited by 42% of respondents. This shows how many households are actively looking for ways to regain control of their finances and reduce the pressure of outstanding balances.

The challenge is that paying off debt quickly rarely happens by accident. It usually requires a clear plan, consistent payments, and practical strategies that help you reduce balances without creating new financial strain.

In this blog, we’ll explore practical debt resolution strategies that can help you move forward faster.

Key Takeaways

- Paying off debt faster starts with clarity. Listing all your debts, interest rates, and payment deadlines helps you prioritize payments more effectively.

- Interest rates and minimum payments often slow progress. Targeting high-interest balances or smaller debts strategically can accelerate repayment.

- Choosing the right payoff method matters. The debt avalanche minimizes total interest costs, while the snowball method builds motivation through quick wins.

- Protecting essential expenses is critical. A debt plan should never jeopardize housing, utilities, or other necessary living costs.

- Consistent habits create long-term progress. Organized payments, smart spending adjustments, and tracking milestones can steadily reduce financial pressure over time.

Factors That Are Slowing Your Debt Payoff Down

Many people begin their repayment journey with the goal of eliminating debt as quickly as possible. However, progress can feel slow even when you are making regular payments. In many cases, the issue is not a lack of effort but certain financial factors that quietly extend repayment timelines.

Understanding what might be slowing down your progress can help you make more informed decisions and adjust your repayment strategy more effectively.

- High Interest Rates Continue Increasing the Balance: Many types of consumer debt, particularly credit cards and certain personal loans, carry relatively high interest rates. When interest accumulates each month, a significant portion of your payment may go toward interest rather than reducing the principal balance. This means the overall debt decreases more slowly than expected.

- Relying Only on Minimum Payments: Minimum payments are designed to keep accounts current, but they rarely reduce balances quickly. In many cases, the minimum amount covers mostly interest charges with only a small portion applied to the original balance. As a result, debt can remain active for years even when payments are made consistently.

- Managing Multiple Debts at the Same Time: When you have several debts with different balances, interest rates, and due dates, it can be difficult to decide which one to prioritize. Without a structured repayment strategy, payments may become scattered across accounts, slowing overall progress.

- Irregular or Unexpected Expenses: Financial surprises such as medical bills, car repairs, or sudden changes in income can interrupt repayment plans. When these unexpected costs arise, money that might have gone toward debt payments often has to be redirected to immediate needs.

- Lack of a Clear Repayment Strategy: Many people simply make payments as they can without a defined strategy. Without prioritizing certain balances or following a structured plan, repayment may become inconsistent, making it harder to reduce total debt efficiently.

Recognizing these factors is an important first step toward paying off debt faster. Once you understand what may be slowing your progress, it becomes easier to adopt more effective strategies that move you closer to financial stability.

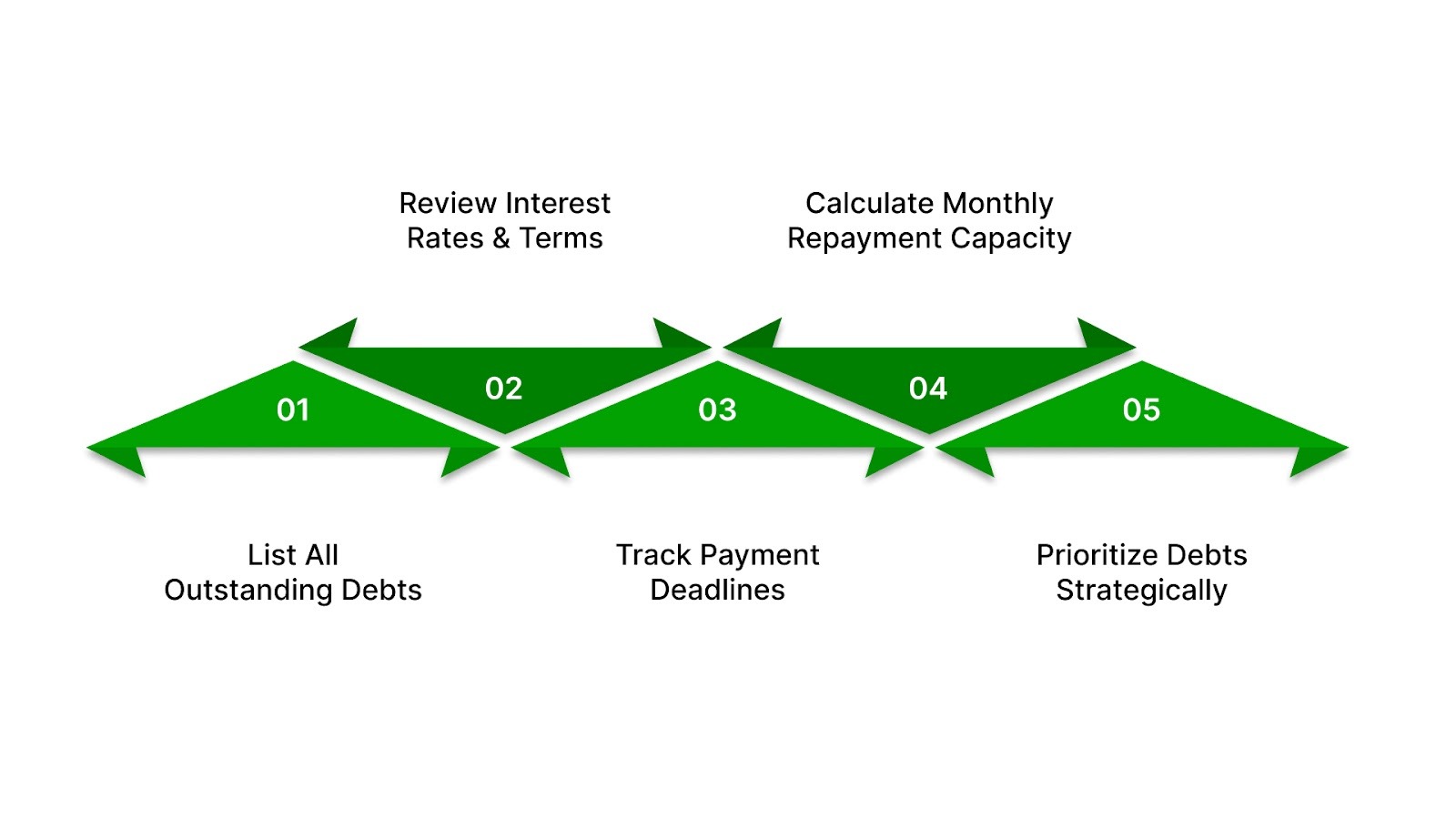

5 Clear Requirements To Pay Off Debt Fast

When people search for how to pay off debt fast, the first instinct is often to make extra payments immediately.

Taking a few structured steps to organize your finances can help you prioritize payments and reduce your total debt more efficiently.

1. List Every Debt You Currently Owe

Before creating any repayment strategy, start by identifying all outstanding balances. Many people underestimate their total debt simply because the accounts are spread across different lenders or payment platforms.

- Write down every account and balance: Include credit cards, personal loans, medical bills, student loans, or any other outstanding obligations. Seeing the full list in one place helps eliminate uncertainty about what you owe.

- Include the creditor name and account details: This helps you stay organized and prevents confusion when multiple payments are due each month.

- Note the current balance for each account: Having accurate numbers allows you to calculate your total debt and decide where to focus your efforts first.

Creating a full list gives you a clear starting point for building a repayment plan.

2. Identify Interest Rates and Payment Terms

Interest rates have a major influence on how quickly debt grows and how long repayment will take. Understanding these details helps you determine which accounts may be costing you the most over time.

- Record the interest rate for each account: Higher interest debts typically accumulate costs faster, making them more expensive if they remain unpaid for long periods.

- Review the minimum payment requirement: This helps you understand how much you must pay each month to keep the account current.

- Check how interest is applied: Some debts compound daily or monthly, which can increase the total balance if payments are delayed.

Knowing these details allows you to make smarter decisions about where extra payments will have the greatest impact.

3. Track Payment Deadlines and Monthly Obligations

Managing multiple debts becomes easier when you clearly understand when each payment is due and how much is required.

- Create a simple payment calendar: Listing all due dates in one place helps prevent missed payments and late fees.

- Track the minimum payment for each account: This ensures you keep every account current while still allocating extra money toward priority debts.

- Set reminders for upcoming payments: Automatic reminders or scheduled payments can help maintain consistency.

Staying organized with deadlines helps protect your credit history and prevents additional financial penalties.

4. Determine How Much You Can Apply Toward Debt Each Month

Before making additional payments, it is important to understand how much money you can realistically dedicate to debt repayment.

- Review your monthly income: Include all reliable income sources such as salary, freelance work, or other earnings.

- Subtract essential living expenses: Housing, food, utilities, transportation, and healthcare should always be covered first.

- Calculate the amount available for debt payments: The remaining amount represents the money you can safely apply toward reducing balances.

This step ensures that your repayment plan remains sustainable rather than creating additional financial strain.

5. Prioritize Your Debts Strategically

Once you understand your balances, interest rates, and monthly budget, you can begin organizing your debts into a clear repayment strategy.

- Identify which debts should receive extra payments: Many people prioritize high-interest balances to reduce overall costs.

- Decide how extra payments will be distributed: Concentrating additional payments on one debt at a time often creates faster progress.

- Track your repayment progress over time: Monitoring balances each month helps you stay motivated and adjust your strategy if necessary.

When your debts are clearly organized and prioritized, every extra payment you make becomes more effective in helping you move toward financial stability.

If reviewing balances, payment terms, and account details feels overwhelming, structured guidance can help bring clarity. The Forest Hill Management works with individuals to review account information, organize repayment options, and provide a clearer path toward resolving outstanding balances.

With a clear understanding of your balances, interest rates, and payment obligations, you can begin deciding how to prioritize repayment.

Choosing the Right Debt Payoff Method for Your Situation

Once you understand your full debt picture, the next step is choosing a repayment strategy. Many people searching for how to pay off debt fast assume the solution is simply making larger payments. In reality, the way you prioritize those payments can significantly affect how quickly your balances decrease.

Two of the most widely recommended strategies are the debt avalanche and debt snowball methods. Financial counseling organizations such as the Consumer Financial Protection Bureau (CFPB) and the National Foundation for Credit Counseling (NFCC) recognize both approaches as effective ways to organize debt repayment.

The key difference lies in how you decide which balance receives extra payments first.

Debt Avalanche Method

The debt avalanche method focuses on reducing the most expensive debt first. This approach prioritizes interest rates, which means you direct extra payments toward the account that costs the most to carry each month.

- How the avalanche method works:

- Continue making minimum payments on every debt to keep accounts current.

- Direct any additional payment toward the balance with the highest interest rate.

- Once that debt is paid off, move the extra payment to the next highest interest rate balance.

- Why do some people prefer this strategy:

- It reduces the total interest paid over time.

- High-interest debt stops growing as quickly once targeted.

- It can lower the total cost of repayment when balances carry different interest rates.

Because high-interest debts accumulate charges faster, paying them down first can significantly reduce the total amount of interest paid over time.

This method tends to work well for individuals who are focused on the mathematics of debt repayment and long-term savings, since it minimizes interest costs while steadily reducing balances.

Debt Snowball Method

The debt snowball method takes a different approach by prioritizing smaller balances first to create visible progress early in the repayment process.

How the snowball method works:

- Pay the minimum amount on every account.

- Put extra money toward the smallest balance first, regardless of interest rate.

- After the smallest debt is paid off, redirect that payment to the next smallest balance.

Why this method works for many people:

- Small debts can be eliminated quickly.

- Each completed payoff creates momentum and motivation.

- Seeing progress can help people stay committed to their repayment plan.

The CFPB also highlights the snowball strategy as a commonly used debt reduction approach. According to the National Foundation for Credit Counseling, the snowball method can be especially effective for individuals who stay motivated by seeing quick progress.

Both strategies can help you reduce debt effectively, but they define “fast” in slightly different ways.

When the avalanche method may work better:

- You want to reduce the total interest cost of your debt.

- Your debts have very different interest rates.

- You are comfortable focusing on long-term financial efficiency.

When the snowball method may work better:

- You want quick wins to stay motivated.

- Your debts include several small balances that can be eliminated quickly.

- Visible progress helps you stay disciplined.

Also read: Debt Mediation and Repayment Strategies: A Clear Guide

In practice, the most effective strategy for how to pay off debt fast is the one you can follow consistently every month. A clear structure, steady payments, and gradual balance reductions often lead to meaningful progress over time.

While repayment strategies focus on reducing balances efficiently, it is equally important to understand the protections available to you during the process.

Know Your Rights During Debt Resolution

When you are working to repay or resolve debt, it is important to understand that you also have legal protections. U.S. consumer protection laws are designed to ensure that debt collection and account management practices remain fair, transparent, and respectful.

Knowing these rights can help you communicate with confidence, verify account details properly, and avoid unnecessary pressure while you focus on resolving outstanding balances.

Request Written Verification of the Debt

Before making payments toward a debt, you have the right to confirm that the balance and account details are accurate.

- Ask for written validation of the debt: Under the Fair Debt Collection Practices Act (FDCPA), collectors must provide written information about the debt, including the amount owed and the name of the current creditor.

- Review the documentation carefully: Confirm that the balance, account history, and creditor information match your records before agreeing to repayment.

- Submit a written dispute if something appears incorrect: If you believe the debt is inaccurate, you can dispute it and request further verification.

Verifying the debt helps ensure you are addressing the correct account and prevents mistakes from affecting your repayment process.

Expect Respectful and Lawful Communication

Debt collectors must follow strict rules about how they communicate with consumers.

- Know the permitted contact hours: In most cases, collectors cannot contact you before 8 a.m. or after 9 p.m. unless you agree otherwise.

- Understand that harassment and threats are prohibited: The FDCPA forbids abusive language, repeated calls intended to intimidate, or misleading statements about the debt.

- Request written communication if needed: If phone calls feel overwhelming, you can ask that future communication be conducted in writing.

These protections exist to ensure that the debt resolution process remains respectful and fair.

Protect Your Personal and Financial Information

Your personal data must be handled responsibly during debt resolution.

- Limit who can receive information about your debt: Collectors generally cannot discuss your debt with friends, neighbors, or coworkers except in limited situations for locating contact information.

- Confirm secure payment methods before sending money: Always use trusted payment platforms or official payment portals to protect your financial information.

- Keep records of all payments and communication: Maintaining documentation ensures transparency and protects you if questions arise later.

Protecting your personal information is an important part of managing debt responsibly.

Understand Your Right to Dispute or Negotiate

Debt resolution often involves communication and negotiation, and consumers have the right to explore reasonable repayment options.

- Ask about repayment arrangements if full payment is difficult: Structured payment plans may allow balances to be resolved gradually.

- Request written confirmation of any agreements: Documenting payment terms helps avoid misunderstandings and ensures both sides understand the arrangement.

- Take time to review any proposed settlement terms: Never feel pressured to accept repayment terms without fully understanding them.

Clear communication and documented agreements can make the debt resolution process smoother and more manageable.

Also read: Ethical Debt Collection Practices and Strategies

When you know what protections exist and how the process should work, it becomes easier to focus on the practical steps needed to move toward financial stability.

With both a repayment strategy and an understanding of your rights in place, the next step is applying practical habits that support consistent progress.

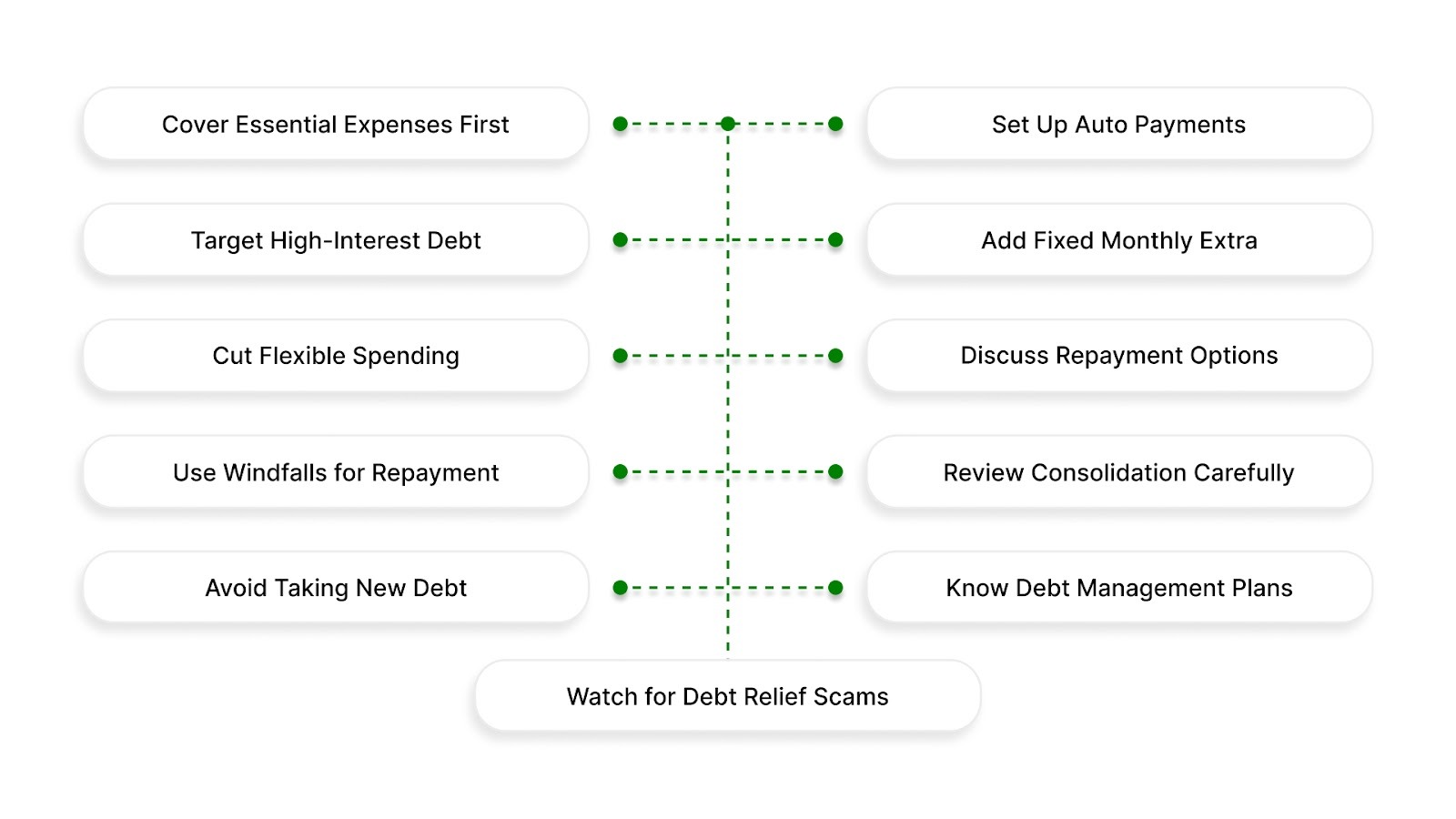

11 Practical Tips to Pay Off Debt Faster and More Safely

Paying off debt faster usually requires a combination of smart prioritization, spending adjustments, and consistent repayment habits. The following tips focus on practical actions that can help you reduce balances while maintaining financial stability.

- Keep Essential Living Expenses Stable First: Before accelerating debt payments, make sure your core bills, such as housing, utilities, food, transportation, and insurance, remain covered. A repayment plan that causes you to miss essential bills can create new financial problems and undermine your progress.

- Prioritize High-Interest Debt Aggressively: Credit cards and other revolving balances often carry the highest interest rates, which means interest compounds quickly. Directing extra payments toward these accounts first can reduce interest costs and help balances decrease more efficiently.

- Reduce Flexible Monthly Spending Categories: Certain expenses reset every month and can be adjusted temporarily to free up additional funds. Areas such as takeout, subscriptions, impulse purchases, and entertainment spending often provide opportunities to redirect money toward repayment.

- Use Temporary Financial Gains to Reduce Debt: Occasional cash inflows such as tax refunds, bonuses, side income, or money from selling unused items can significantly accelerate repayment when applied directly to outstanding balances.

- Avoid Replacing One Debt With Another: Borrowing new money to manage existing balances can sometimes create a larger problem. High-cost credit products, short-term loans, or advance-fee loan offers may increase financial pressure instead of solving it.

- Set Up Automatic Payments for Minimum Balances: Automatic payments help ensure that all accounts remain current and prevent missed due dates. Keeping accounts in good standing protects your repayment plan from avoidable setbacks.

- Add a Fixed Extra Payment Every Month: Consistency often produces better results than occasional large payments. Even a modest fixed extra amount applied each month can steadily reduce balances and shorten repayment timelines.

- Ask About Realistic Repayment Options: If paying the full balance immediately is difficult, discuss alternatives such as a one-time settlement or a structured repayment plan that aligns with your income schedule.

- Evaluate Consolidation or Debt Relief Carefully: Debt consolidation may help only if it lowers interest rates, reduces overall costs, or simplifies payments without hidden fees. Carefully compare options before committing to a new loan or repayment program.

- Understand the Difference Between Consolidation and Debt Management Plans: Debt management plans arranged through nonprofit credit counseling organizations combine payments into a structured repayment program. Unlike consolidation loans, they do not create new debt.

- Watch for Warning Signs of Debt Relief Scams: Be cautious of companies promising guaranteed results, requesting large upfront fees, or pressuring you to stop paying creditors without a documented plan. Regulatory agencies such as the FTC warn consumers about deceptive debt relief practices.

When repayment is guided by clear priorities and sustainable habits, financial stability becomes far more achievable.

Final Thoughts

Paying off debt quickly is rarely about one dramatic financial move. More often, it comes from understanding your full financial picture, choosing a repayment strategy that fits your situation, and applying consistent effort month after month.

Just as importantly, debt resolution should be realistic. If you’re managing past-due balances or accounts that feel difficult to resolve on your own, structured support can help simplify the process. The Forest Hill Management works with individuals to bring clarity to outstanding accounts, provide secure payment options, and explore repayment arrangements that align with real financial circumstances.

Contact The Forest Hill Management today to review your account options and take the next step toward resolving your balances with confidence.

FAQs

1. How long does it usually take to pay off debt?

The timeline varies based on the total balance, interest rates, and how much you can pay each month. With a structured repayment plan and consistent extra payments, many people can significantly shorten their payoff timeline compared to making only minimum payments.

2. Should I close credit cards after paying them off?

Closing accounts immediately may affect your credit utilization ratio and credit history. In many cases, keeping older accounts open with a zero balance can help maintain a stronger credit profile.

3. What should I do if my income changes while paying off debt?

If your income decreases or increases, review your repayment plan and adjust it accordingly. A flexible strategy that adapts to income changes is often more sustainable than rigid payment targets.

4. Is it better to pay off debt or save money at the same time?

Many financial advisors recommend maintaining a small emergency fund while paying down debt. Having some savings can prevent new borrowing if unexpected expenses arise.

5. When should someone consider professional help for debt resolution?

If balances feel difficult to organize, payments are becoming overwhelming, or accounts have moved into collections, structured support from experienced account management professionals may help clarify options and establish manageable repayment arrangements.