How to Manage Risks in Portfolio Management

Transform Your Financial Future

Contact UsManaging multiple financial accounts can sometimes feel like balancing several moving pieces at once. A payment schedule shifts, expenses increase unexpectedly, or financial conditions change. When several obligations are involved, even small changes can create uncertainty about how stable your overall financial situation really is.

This is why understanding portfolio risk matters. Research in portfolio theory shows that spreading financial exposure across different assets or accounts can significantly reduce overall risk, because the impact of one underperforming asset is less likely to affect the entire portfolio.

For individuals, this does not require complex financial models. It simply means understanding how risks develop within a group of financial commitments and taking practical steps to monitor and manage them.

In this blog, you will learn what portfolio risk management means, the types of risks that can arise, how those risks are measured, and practical ways to manage them while maintaining control over your financial obligations.

Key Takeaways

- Portfolio risk management involves identifying and managing potential financial, operational, and compliance risks across a group of financial accounts.

- Risks in a financial portfolio can arise from several sources, including missed payments, administrative errors, regulatory requirements, data handling issues, and unclear communication.

- Monitoring account activity and using risk measurements such as volatility, correlation, and Value at Risk helps create a clearer understanding of how stable a portfolio may be.

- Practical strategies such as diversification, balanced financial planning, regular monitoring, and consistent payments can help reduce uncertainty and maintain financial stability.

- Structured account oversight, clear communication, and secure payment options from organizations like Forest Hill Management can help individuals better understand and manage their financial obligations.

What Is Portfolio Risk Management?

Portfolio risk management refers to the structured process of identifying, evaluating, and addressing potential risks that could affect a group of financial accounts managed together. In simple terms, it involves recognizing possible problems early and putting systems in place to reduce their impact before they escalate.

When multiple accounts are handled as part of a portfolio, different types of risks can arise at the same time. Some accounts may fall behind on payments, records may become inconsistent, or communication may not follow the correct regulatory standards.

Risk management helps ensure that these situations are identified quickly and handled through clear, responsible processes.

Core Components of Portfolio Risk Management

Portfolio risk management works best when it follows a clear framework that guides how accounts are monitored, documented, and serviced. These core components help maintain stability across large portfolios while supporting fair and transparent communication with individuals.

- Risk Identification and Assessment: The first step involves identifying potential risks within the portfolio. This may include accounts that are becoming delinquent, inconsistencies in documentation, or patterns that suggest repayment challenges. Early identification addresses issues before they grow into larger financial or operational problems.

- Account Monitoring and Performance Tracking: Ongoing monitoring helps understand how accounts are performing over time. Reviewing payment trends, delinquency stages, and consumer engagement patterns allows servicing teams to identify when additional support or communication may be needed.

- Compliance and Consumer Protection Oversight: Risk management also requires strict adherence to regulatory standards governing debt collection and consumer communication. Systems and procedures are designed to ensure that interactions remain respectful, documented, and aligned with legal requirements.

- Secure Data and Information Management: Accurate records and secure data handling are essential for reducing operational risks. Maintaining reliable documentation helps prevent errors in balances or payment histories while protecting sensitive personal and financial information.

- Structured Communication and Resolution Processes: Clear communication plays an important role in managing portfolio risk. When individuals receive accurate information about their accounts and repayment options, they are better able to respond and work toward a resolution in an organized way.

Together, these components create a structured environment where accounts are handled responsibly, risks are addressed early, and consumers receive clear guidance about their financial obligations and available options.

Also read: What Investment Portfolio Management Means for Managing Debt Over Time

With these foundational elements in place, it becomes easier to understand the different types of risks that can arise within a financial portfolio.

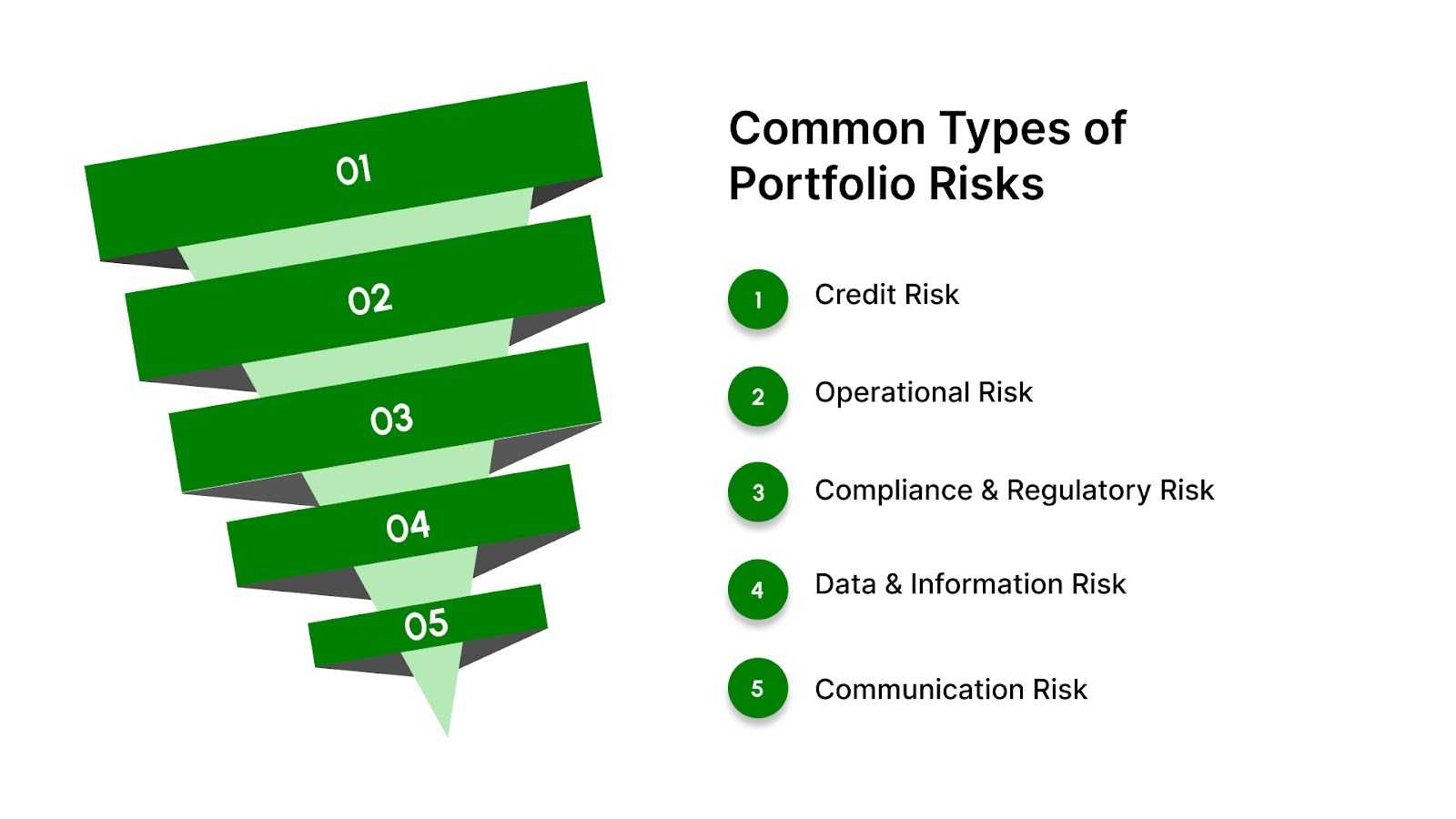

5 Common Types of Portfolio Risks

When multiple financial accounts are managed together, different types of risks can influence how those accounts perform and how they are serviced.

Understanding the different types of portfolio risks helps explain why structured account oversight is important. When risks are identified early, individuals can respond with clearer communication, better documentation, and responsible repayment discussions that support resolution.

Below are some of the most common risks that can arise when managing financial account portfolios.

1. Credit Risk

Credit risk refers to the possibility that a borrower may be unable to meet repayment obligations according to the original agreement. Changes in financial circumstances can affect an individual’s ability to make payments consistently, which can influence how accounts perform within a portfolio.

Common factors that contribute to credit risk include:

- Income disruptions: Job loss, reduced working hours, or unexpected financial obligations can affect a person’s ability to maintain regular payments.

- Rising financial obligations: When multiple debts accumulate at the same time, managing monthly payments can become increasingly difficult.

- Economic conditions: Broader economic changes, such as inflation or industry downturns, can affect many borrowers at once and increase delinquency levels across a portfolio.

2. Operational Risk

Operational risk arises from issues within the systems or processes used to manage financial accounts. These risks often relate to administrative errors, inconsistent recordkeeping, or communication breakdowns.

Operational risks may appear in several ways:

- Inaccurate account documentation: If balances, payment histories, or account details are not recorded consistently, it can lead to confusion or disputes.

- Delayed or inconsistent communication: When information is not delivered clearly or on time, consumers may struggle to understand their account status.

- Process inefficiencies: Poorly organized servicing systems can slow down account updates and create unnecessary complications.

3. Compliance and Regulatory Risk

Individuals responsible for managing financial accounts must follow strict consumer protection laws governing communication and account servicing. Compliance risk occurs when these regulations are not followed properly.

Important compliance considerations include:

- Adherence to consumer protection laws: Regulations such as the Fair Debt Collection Practices Act set rules on how communication with consumers must occur.

- Accurate account verification procedures: Individuals have the right to request validation and confirmation of account details.

- Fair and transparent communication standards: Organizations must avoid misleading statements, harassment, or excessive contact.

4. Data and Information Risk

Portfolio management relies heavily on accurate and secure data. If information about accounts is incomplete or improperly handled, it can create significant operational challenges.

Key data-related risks include:

- Incomplete or outdated records: Missing payment details or incorrect balances can affect both decision-making and consumer trust.

- Data security concerns: Sensitive personal and financial information must be protected against unauthorized access.

- Information handling errors: Improper documentation or data transfers may result in incorrect account reporting.

5. Communication Risk

Clear communication plays a critical role in helping individuals understand their financial obligations and available options. When communication becomes unclear or inconsistent, misunderstandings can occur.

Communication risks may include:

- Unclear account explanations: Consumers may struggle to understand balances, creditor information, or repayment expectations.

- Inconsistent messaging: Different messages from multiple sources can create confusion about the account status.

- Limited access to support: Without reliable support channels, individuals may find it difficult to ask questions or clarify concerns.

Recognizing the different forms of portfolio risk is only the first step. It is equally important to understand how these risks are measured and monitored over time.

How to Measure the Risk of a Portfolio?

Measuring portfolio risk helps you understand how stable or uncertain a group of financial accounts may be over time. From a consumer standpoint, this means reviewing patterns such as payment consistency, balance changes, and overall account activity to see whether financial obligations are becoming easier or harder to manage.

Common ways portfolio risk is measured include:

- Standard Deviation (Volatility Measurement): Standard deviation measures how much returns or performance values move above or below their average. If the variation is large, the portfolio is considered more volatile and therefore riskier because outcomes can change significantly over time.

- Beta (Market Sensitivity): Beta evaluates how sensitive a portfolio is to overall market changes. A higher beta means the portfolio tends to react more strongly to market movements, while a lower beta suggests more stability compared with the broader market.

- Sharpe Ratio (Risk-Adjusted Performance): The Sharpe ratio compares the return of a portfolio with the level of risk taken to achieve that return. A higher ratio indicates that returns are being generated efficiently relative to the amount of risk involved.

- Value at Risk (VaR): Value at Risk estimates the potential loss a portfolio could experience over a specific time period under normal conditions. It helps quantify the maximum expected loss within a certain confidence level.

- Correlation Analysis: Correlation analysis examines how different assets within a portfolio move in relation to each other. If assets move in different directions, overall risk may be reduced because losses in one area can be balanced by stability in another.

Understanding these measurements helps create clearer expectations around financial obligations. When risk is monitored regularly, it becomes easier to identify challenges early, maintain accurate records, and create repayment discussions that are realistic and manageable.

After understanding how portfolio risks are evaluated, the next step is to explore the practical strategies used to manage and reduce those risks.

How to Manage Risks in Portfolio Management?

Managing risks within a financial portfolio involves taking practical steps that help keep accounts organized, obligations manageable, and financial decisions well-informed.

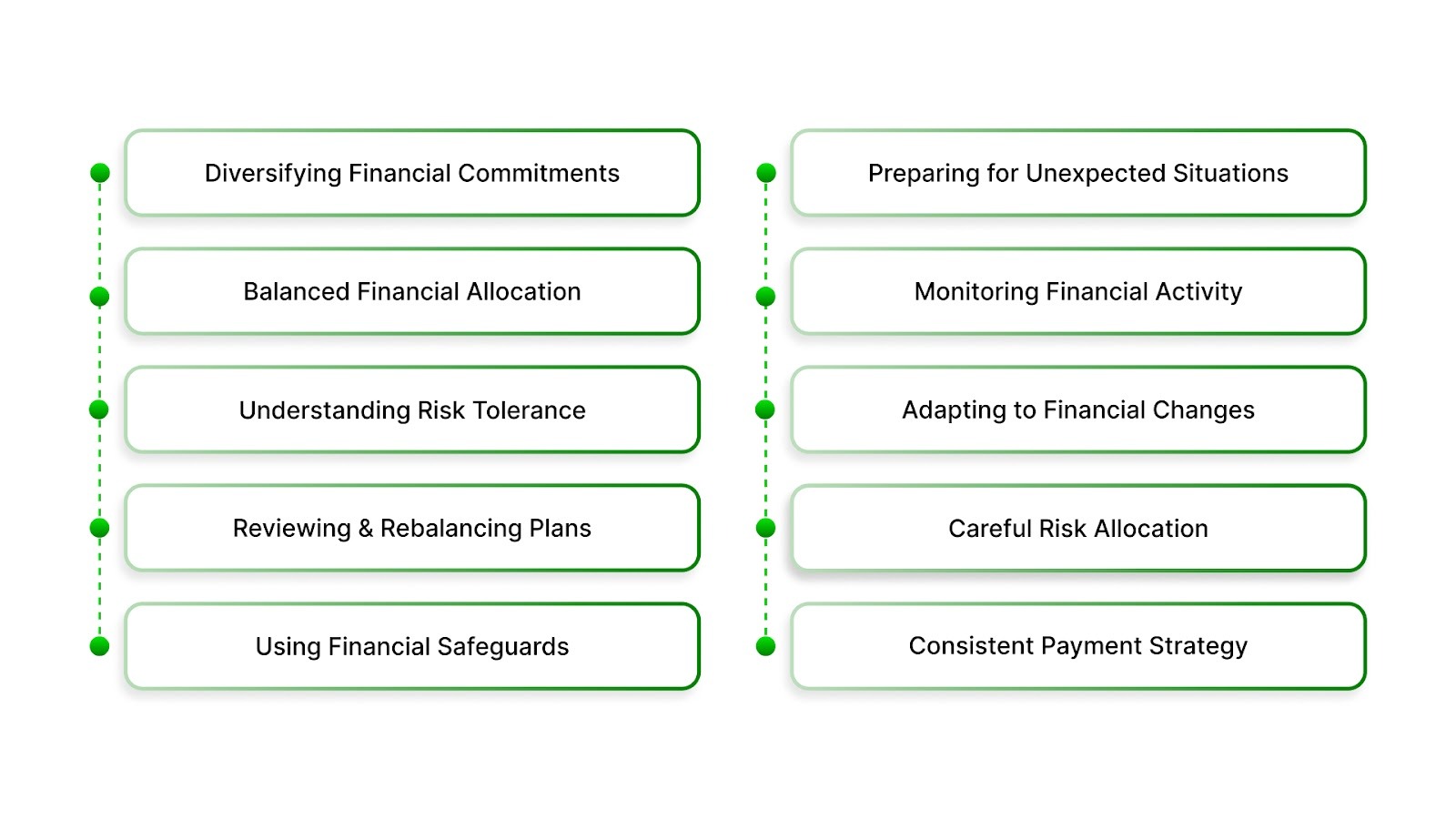

For individuals, this means maintaining visibility over balances, understanding repayment commitments, and ensuring financial decisions remain aligned with personal capacity and long-term stability. The following approaches are commonly used to reduce risk and maintain better control over financial portfolios:

- Diversifying Financial Commitments: Diversification means avoiding reliance on a single financial obligation or income source. When financial responsibilities or assets are spread across different areas, the impact of one issue becomes easier to manage. This approach helps reduce the pressure that may arise if one account becomes difficult to maintain.

- Maintaining Balanced Financial Allocation: A balanced mix of financial responsibilities and resources can help you manage risk more effectively. Reviewing how income, savings, and financial commitments are distributed allows you to ensure that obligations remain manageable over time.

- Understanding Your Risk Tolerance: Risk tolerance refers to how much financial uncertainty you can realistically manage without causing stress or instability. Taking time to evaluate your financial capacity helps ensure that repayment plans or financial commitments align with your current situation.

- Reviewing and Rebalancing Financial Plans: Financial situations can change over time, which is why it is important to review your financial arrangements periodically. Adjusting payment schedules, budgeting strategies, or financial priorities can help keep your overall obligations balanced.

- Using Financial Safeguards: Some financial tools or safeguards can help limit potential financial pressure. These may include structured repayment plans, clear documentation of financial commitments, and verified payment channels that keep records organized.

- Preparing for Unexpected Situations: Stress testing your financial situation means thinking ahead about how you would respond if unexpected events occur, such as reduced income or increased expenses. Planning ahead allows you to adjust strategies before challenges escalate.

- Monitoring Financial Activity Regularly: Keeping track of account balances, payment confirmations, and financial records helps you stay aware of how your obligations are evolving. Regular monitoring reduces the risk of overlooked payments or unexpected account changes.

- Adapting to Changing Financial Conditions: Financial environments can shift due to economic conditions, employment changes, or personal circumstances. Being flexible and adjusting financial plans accordingly helps maintain stability during periods of uncertainty.

- Allocating Risk Carefully: Risk budgeting involves deciding how much financial responsibility you can comfortably manage across different obligations. By distributing commitments realistically, you reduce the likelihood that one issue will affect your entire financial situation.

- Making Consistent Payments Over Time: Consistent payments, even if they are smaller amounts, can help maintain progress while reducing the pressure of large one-time payments. This steady approach can help smooth financial fluctuations and keep obligations manageable.

Managing portfolio risks ultimately comes down to staying informed, organized, and proactive.

Also read: Benefits and Process of Portfolio Management Services

While these strategies provide a general framework for managing financial risk, structured account oversight and clear communication can make the process much easier to navigate.

Conclusion

Financial portfolios are rarely static. Balances change, circumstances evolve, and unexpected events can affect how accounts perform over time. Understanding how risk works within a portfolio helps transform what might feel like uncertainty into something more manageable.

When risks are monitored carefully and financial information remains clear, it becomes easier to stay organized and make informed decisions.

This is where having the right support can make a meaningful difference. The Forest Hill Management focuses on bringing clarity and structure to the account management process, helping individuals understand their balances, track payment activity, and explore repayment options that align with their situation.

If you have questions about an account or want to review your available options, reach out to The Forest Hill Management today.

FAQs

1. Can portfolio risk change even if my financial situation stays the same?

Yes. Portfolio risk can change due to external factors such as economic conditions, interest rate changes, or market fluctuations, even if your personal financial situation remains stable.

2. Does managing portfolio risk mean eliminating risk completely?

No. Risk cannot be eliminated entirely in financial portfolios. The goal is to identify and manage risk effectively so that potential challenges are reduced and financial decisions remain manageable.

3. How often should a financial portfolio be reviewed for risk?

Many financial experts recommend reviewing portfolios periodically, such as quarterly or annually, or whenever there are major financial changes like new obligations, income changes, or economic shifts.

4. Why is accurate financial documentation important for managing risk?

Accurate records help ensure balances, payment histories, and account details are correct. This reduces misunderstandings, prevents administrative errors, and helps individuals make better financial decisions.

5. Can clear communication reduce financial risk?

Yes. When account information, balances, and repayment options are explained clearly, individuals can respond more confidently and avoid misunderstandings that might otherwise create additional financial complications.