How to Verify a Debt Collector and Protect Your Rights

Need Help Reviewing Your Account?

Contact UsA call or letter about an unpaid account can leave you feeling uneasy, especially when you are already trying to keep up with bills and daily expenses. In moments like this, knowing how to verify a debt collector can help you slow down and make informed decisions instead of reacting to unexpected pressure.

Many people facing financial stress worry about what a collection notice means for their future. Questions about unpaid accounts, wage garnishment options, or debt repayment plans can quickly add to the anxiety. Learning how to verify a debt collector gives you a practical way to confirm who contacted you and understand your next step with greater confidence.

This guide walks through simple checks that can help you review collection communications carefully, understand your rights, and approach debt resolution with clarity and peace of mind.

Key Takeaways

- Learning how to verify a debt collector helps you avoid fraudulent payment requests, review account details carefully, and make decisions without pressure.

- Legitimate collectors must send written information explaining the creditor, balance breakdown, and dispute timeline so you can confirm the account information.

- Asking for identification, reviewing account documents, researching the agency, and checking your credit report help confirm whether a collection communication is legitimate.

- Warning signs such as urgent payment demands, inconsistent explanations, or unusual contact methods may indicate that the caller is not a legitimate collector.

- Clear account information, secure payment tools, and transparent communication help you understand where you stand and move toward resolving unpaid accounts confidently.

Why It Is Important to Verify a Debt Collector?

When you receive a call or letter about a past-due account, uncertainty can create stress. Verifying the collector helps you pause, review the situation carefully, and protect your finances before taking any action.

Taking a moment to confirm legitimacy gives you control and prevents avoidable financial mistakes during an already difficult situation.

Financial safety often depends on confirming details before responding to collection requests. Key reasons verification protects your financial well-being include:

- Preventing Fraudulent Payment Requests: Scammers sometimes impersonate collection agencies to pressure for quick payments. Verifying the caller protects your money from requests tied to debts that never existed.

- Avoiding Responsibility for Someone Else’s Account: Collection notices occasionally reach the wrong person. Confirming the account details helps prevent paying for a balance that belongs to someone with a similar name.

- Identifying Errors in Account Records: Old accounts may contain outdated balances or added charges. Verification allows you to review the numbers carefully before discussing repayment options.

- Protecting Personal Financial Information: Unverified callers may request details such as bank numbers or Social Security information. Confirming legitimacy first reduces the risk of identity theft or data misuse.

- Maintaining Control Over Financial Decisions: Verifying the collector gives you time to review your options calmly instead of reacting under pressure from unexpected calls or messages.

According to the Consumer Financial Protection Bureau, debt collectors must provide written validation information within five days of their first communication.

Taking a few minutes to confirm who is contacting you helps you move forward with confidence. Careful verification keeps your finances protected while allowing you to address legitimate accounts in a clear and organized way.

Understanding your situation is the first step toward real financial progress. Learn why personalized approaches matter in Why One-Size-Fits-All Debt Solutions Don't Work for Real Relief

What Information a Legitimate Debt Collector Must Provide

When a debt collector contacts you, they must provide specific details that explain the account and who is collecting it. This written information helps you confirm the communication is legitimate and gives you the clarity needed to review the account before discussing payment or next steps.

Important account details that legitimate collectors are required to provide include:

- Clear Identification Statement: The notice must clearly state that the communication comes from a debt collector attempting to collect a debt.

- Consumer and Collector Contact Details: Your name and mailing address, along with the collector’s official company name and mailing address, must be included for transparency.

- Original Creditor Name: The notice must identify the creditor connected to the account so you can recognize where the balance originated.

- Debt Amount Breakdown: The total balance should reflect interest, fees, payments, and credits applied to the account since a specific date.

- Dispute Rights and Timeline: The notice must explain how you can respond if the information appears incorrect and provide a 30-day period to raise a dispute.

Reviewing this information carefully helps you understand where you stand financially and decide how you would like to move forward with resolving the account.

If you are looking for trusted guidance to manage your finances more effectively, explore the top options in Best Finance Advisory Service Providers for Debt Management

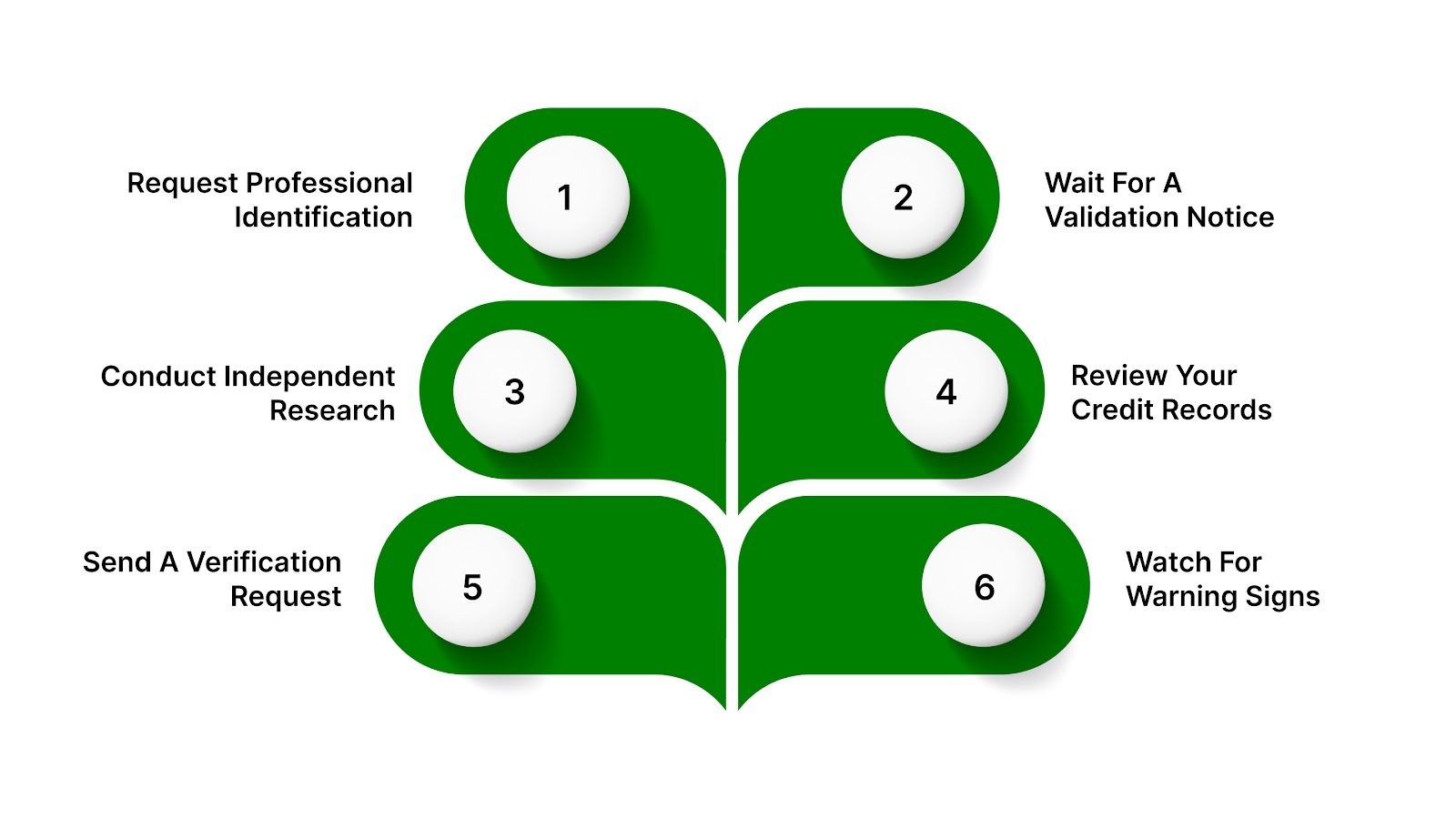

How to Verify a Debt Collector Step by Step?

Receiving a collection call or notice can feel overwhelming, especially if you are unsure why you were contacted. Taking a few careful steps can help you review the situation calmly and understand what the communication means for you.

1. Request Professional Identification

When someone contacts you about a debt, confirming who they are helps you understand whether the communication is legitimate before discussing any financial details.

Simple checks that help confirm the caller’s identity include:

- Ask For Full Contact Details: Request the caller’s name, company name, address, and phone number. For example, a legitimate representative should easily provide their company’s mailing address.

- Request Licensing Information: If your state requires licensing, ask whether the collector has a professional license number. For instance, some collectors will provide this number during the conversation.

- Write Down The Details Shared: Keeping notes during the call helps you verify the information later. For example, recording the company name allows you to search for the organization online.

2. Wait For a Written Validation Notice

After the initial contact, you should receive a written notice explaining the account details. This document allows you to review the information calmly rather than responding immediately.

Information worth reviewing carefully includes:

- Confirm the Account Balance: Review the amount listed in the notice. For example, check whether the balance matches what you remember from an old credit card statement.

- Check the Creditor Name: Look for the creditor connected to the account. For example, the notice may list a bank or credit card company you previously used.

- Review Your Response Options: The notice should explain how to respond if something seems incorrect. For instance, it may explain how to dispute the account within a specific timeframe.

3. Conduct Independent Research

If something still feels unclear, verifying the company independently can help confirm whether the organization contacting you is legitimate.

Independent checks that help provide reassurance include:

- Check With State Regulators: Contact your state attorney general or local regulator to confirm the company can operate as a collection agency in your state.

- Review Consumer Complaint Records: Looking at publicly available feedback can provide context. For example, you may see whether other consumers reported similar experiences.

- Contact The Original Creditor: Reaching out to the company connected to the account may confirm whether your account was transferred to a collection agency.

4. Review Your Credit Records

Looking at your credit history can provide helpful context and show whether the account appears in your financial records.

Helpful review steps include:

- Access Your Credit Report: Review your credit report from the major bureaus to see whether the account appears in your credit history.

- Compare Account Details: Check whether the creditor name and balance match the information shared in the notice you received.

- Look for Unexpected Accounts: Reviewing your report may also reveal accounts you do not recognize, which could signal mistaken identity.

5. Send a Written Verification Request

If questions remain, sending a written request allows you to ask for additional documentation before continuing the conversation.

Actions that support a written verification request include:

- Request Supporting Documents: Ask the collector to provide records showing the agreement connected to the account and documents explaining the balance.

- Ask for Account Ownership Details: Request information explaining how the collection agency obtained the authority to manage the account.

- Send the Request by Certified Mail: Using certified mail helps confirm delivery and provides a record of the communication.

6. Pay Attention to Warning Signs

While reviewing the information, noticing unusual behavior can help you recognize communications that may not follow standard collection practices.

Behaviors that may signal concern include:

- Threats of Arrest or Criminal Consequences: For example, a caller claiming you will be arrested immediately is not following normal collection practices.

- Urgent Pressure For Immediate Payment: Someone insisting you must pay within minutes to avoid legal action may be using pressure tactics.

- Requests For Sensitive Information: A caller asking for bank passwords or full Social Security numbers during verification should raise concern.

Taking time to verify a debt collector helps you understand who contacted you and what the account involves, allowing you to approach the situation with clarity and confidence.

If you are planning for a future home purchase while managing existing balances, it helps to understand how consolidation may influence your options in Does Debt Consolidation Affect Buying a Home?

Warning Signs That a Debt Collector May Be a Scam

Certain communication behaviors can help you recognize when a debt collector may not be legitimate. Warning signs often include unclear explanations, sudden payment pressure, or contact methods that feel unusual.

Identifying these patterns early helps you verify the details before discussing repayment options.

Communication behaviors that may signal a fraudulent collection attempt include:

- Urgent Pressure To Pay Immediately: Scammers often create artificial urgency, insisting that payment must be made right away to avoid consequences or additional problems.

- Unclear or Changing Explanations: When the caller cannot consistently explain the account details or changes their story during the conversation, the information may not be reliable.

- Reluctance to Answer Basic Questions: Someone who becomes defensive or avoids answering reasonable questions about the account may not have legitimate authority.

- Unexpected Contact Methods: Messages sent through unfamiliar channels, such as random text messages or social media, may indicate an attempt to reach you outside normal communication practices.

- Promises That Sound Too Good To Be True: Offers claiming they can completely eliminate a debt or fix the situation instantly should be treated carefully before taking any action.

Taking a moment to notice these patterns allows you to step back and evaluate the situation more clearly before responding to unexpected collection communications.

Secure payment systems can make managing account payments simpler and more transparent. Learn how these platforms operate in Best Debt Payment Gateways and How They Work

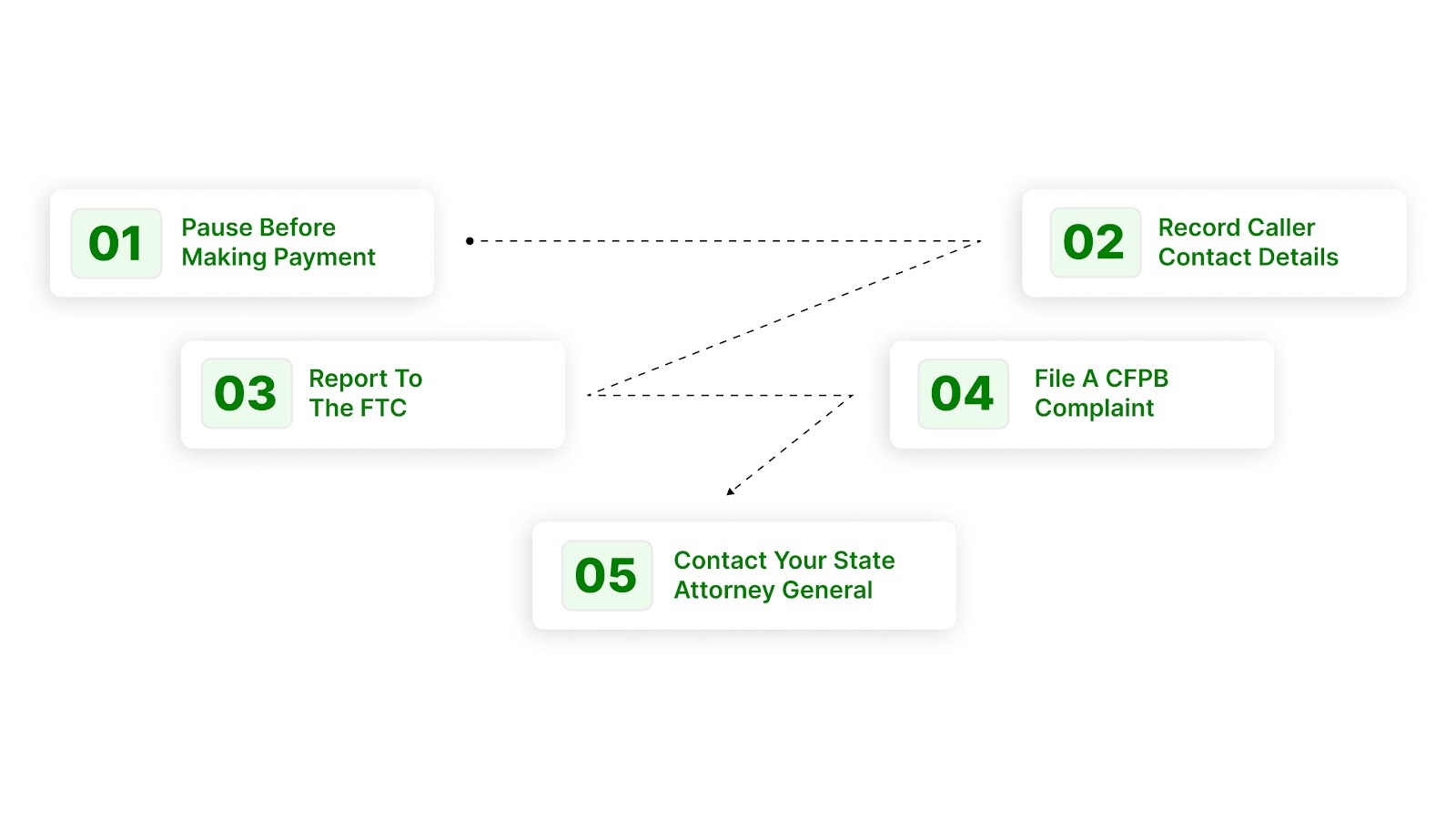

What to Do and Where to Report a Suspected Debt Collection Scam?

Discovering that a debt collection call may not be legitimate can feel unsettling. Taking a few careful steps helps you protect your finances, document the situation, and notify the right organizations that track suspicious activity.

Practical actions that help you respond safely and report suspicious activity include:

- Pause and Avoid Immediate Payment: Take a moment before responding. Scammers often rely on urgency, hoping you will send money before reviewing the situation.

- Gather Contact Details For Documentation: Write down the caller’s name, company name, phone number, and address so you have a clear record of the communication.

- Notify The Federal Trade Commission: You can report suspicious collection activity online at ReportFraud.ftc.gov so federal authorities can investigate patterns of fraud.

- Submit A Complaint To The CFPB: Filing a complaint with the Consumer Financial Protection Bureau helps track harmful practices and supports consumer protection efforts.

- Contact Your State Attorney General: Your state attorney general’s office can review the situation and explain the protections available for consumers in your state.

Taking these steps helps you document the situation and connect with organizations that protect consumers from deceptive practices.

Conclusion

When unexpected collection communication enters your life, clarity can make a meaningful difference. Taking time to understand your situation allows you to approach unpaid accounts thoughtfully instead of reacting to uncertainty or stress.

Financial challenges happen to many people, and addressing them step by step can help restore a sense of control over your finances. With clear information, respectful communication, and safe payment options, resolving an account can become a manageable part of your financial recovery.

If an account is managed through Forest Hill Management, communication and account handling follow documented processes designed to keep information organized and clearly recorded.

Take the first step toward financial freedom by approaching collection communication with careful verification, accurate information, and an informed understanding of your options.

FAQs

1. Can a debt collector contact you before sending written information?

Yes. A debt collector may contact you first by phone, email, or text. Written information explaining the account should follow shortly after the first communication.

2. How can you verify a debt collector if they contact you by text or email?

If a message arrives through text or email, avoid responding immediately. Instead, confirm the company name independently and wait for official written account information before continuing communication.

3. Can caller ID help you verify a debt collector?

Caller ID alone is not reliable for verification because phone numbers can be altered or redirected. Confirming the company name and official contact details provides more reliable verification.

4. How long do you have to verify a debt collector after the first contact?

After receiving written account information, you typically have a limited period to review the details and raise questions if something appears incorrect.

5. What should you do if a verified debt collector contacts you about an account you do not recognize?

If the account does not look familiar, you can request additional information about the creditor and the account history before discussing repayment options.