Is 698 a Good Credit Score?

Transform Your Financial Future

Contact UsA 698 credit score can leave you wondering whether you're on track or falling short. With credit card utilization rising to 35.5% in 2025, many individuals are using credit to manage day-to-day expenses, which can negatively affect their scores.

For those of you already feeling the strain, whether you’re managing credit card debt or applying for a loan, this can feel like a roadblock. This blog will break down what a 698 credit score really means, how it impacts your loan options, and what you can do to improve it.

We’ve got you covered, whether you're striving to boost your score for better interest rates or simply want a clearer understanding of your financial health. Let’s understand how this score stacks up and the steps you can take next.

Key Takeaways

- What a 698 Credit Score Means: Falls in the "Good" range, providing access to loans and credit cards but with higher interest rates compared to excellent scores.

- Improving Loan Opportunities: A 698 score qualifies you for credit, but improving your score can help secure better terms and lower interest rates.

- Factors Impacting Your Credit Score: Payment history, credit utilization, credit history length, and credit mix all contribute to your score.

- Steps to Improve Your Credit Score: Reduce credit utilization, make on-time payments, and explore options such as credit builder loans and being an authorized user to boost your score.

- Disputing Errors and Paying Off Collections: Disputing inaccuracies on your report and paying off collections accounts can quickly improve your credit health.

What Is A Credit Score?

A credit score is a three-digit number that reflects your ability to manage credit responsibly. Creditors use this score to assess the level of risk you pose when borrowing money. The higher your score, the more likely creditors are to trust you with credit.

Credit scores are generated using information from your credit report. Different scoring models weigh various factors differently, resulting in slight variations in your score depending on the model used. These factors include your payment history, credit utilization, and length of credit history.

Now that you know what a credit score is, let’s look at the different ranges and how your score compares, and whether a 698 credit score is good.

What Are Credit Score Ranges?

Credit scores can vary based on the scoring model used. Here’s a breakdown of typical credit score ranges:

- 800 to 850: Excellent

Individuals in this range are considered low-risk borrowers and may have an easier time securing loans and credit on favorable terms. - 740 to 799: Very Good

Those in this range are well-regarded by lenders and are likely to be approved for new credit with competitive rates. - 670 to 739: Good

Borrowers in this range are considered acceptable, though not as low-risk as those with higher scores. Approval for loans and credit is likely but not guaranteed. - 580 to 669: Fair

Individuals in this range may be considered higher-risk borrowers, making it more challenging for them to qualify for new credit. - 300 to 579: Poor

A score in this range makes it difficult to secure new credit. Improvement is necessary to access better loan terms or qualify for credit.

It’s essential to note that each lender may have distinct criteria for evaluating your credit. Scoring models can vary among providers, including FICO and the three major credit bureaus: Equifax, Experian, and TransUnion.

Is a 698 Credit Score Good?

A credit score of 698 falls within the "Good" range (670-739). While not exceptional, it's still a solid score. You’re considered a lower-risk borrower, and you can expect to qualify for most loans and credit cards.

However, you might not receive the most favorable interest rates or terms. With a bit of effort, you could boost your score into the very good or excellent range, potentially obtaining better opportunities in the future.

Also Read: Calculating Financial Freedom Number using Passive Income Formula

A 698 credit score is solid, but what does it actually get you? Let’s explore the financial opportunities available with this score.

What Does a 698 Credit Score Get You?

A 698 credit score places you in the "Good" range, which opens doors to a variety of credit options, but not always the best terms. Here’s a breakdown of what you can expect:

With a credit score in this range, this is what you qualify for:

1. Credit Cards

- Store Credit Cards: You may qualify for store cards, which offer rewards or discounts for purchases made at specific retailers.

- Unsecured Credit Cards: A 698 score puts you in line for unsecured credit cards, often without annual fees. You may also gain access to rewards cards, although interest rates may be higher than those offered to individuals with higher credit scores.

- 0% Intro APR Cards: Unfortunately, your score may limit access to the best 0% APR credit cards, which are usually reserved for those with excellent credit.

2. Auto Loans

You should be able to qualify for an auto loan, but expect higher interest rates than those with a higher score. Your 698 score will qualify you, but it's also important to shop around for the best deal.

3. Home Loans

A 698 score helps you qualify for most mortgages, but it’s unlikely you'll get the most competitive rates. However, you should still be able to find reasonable rates and secure financing for your home purchase.

4. Personal Loans

Qualifying for a personal loan with a 698 score is possible, but not guaranteed. Some lenders may require a higher score, while others may offer competitive terms.

5. Student Loans

If you're applying for federal student loans, your credit score won’t be a major factor. However, for private loans, a 698 credit score typically qualifies you for standard terms.

While a 698 credit score gives you access to credit, it often comes with higher interest rates and less favorable terms. Don’t settle for that. Contact our financial advisors to create a custom plan and work toward better rates, giving you more control over your financial future.

Now that you know what you can access with a 698 credit score, let's break down the key factors that influence your score.

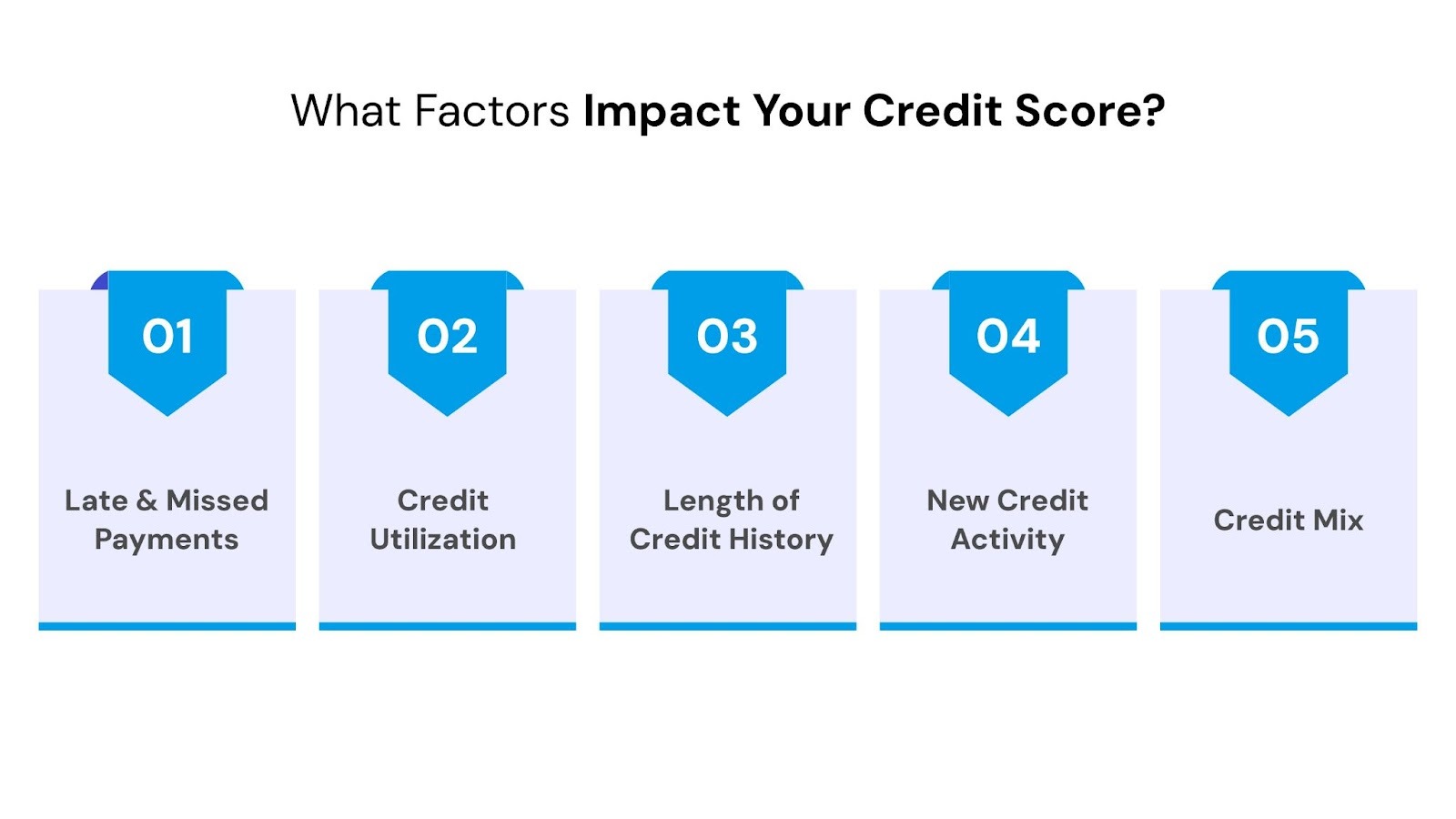

What Factors Impact Your Credit Score?

Your credit score is impacted by several key factors that reflect your financial habits and credit management. Here’s a breakdown of the most important ones:

- Late and Missed Payments: Late or missed payments, which account for 35% of your score, show lenders that you may be at risk of defaulting on debt.

- Credit Utilization: This measures how much of your available credit you’re using. When your credit utilization rate exceeds 30%, your score tends to drop.

- Length of Credit History: The longer your credit history, the more positively it impacts your score. This factor makes up 15% of your score.

- New Credit Activity: Opening new credit accounts can temporarily lower your score, as it suggests an increased risk to lenders. This factor makes up 10% of your score.

- Credit Mix: A variety of credit accounts, such as credit cards and installment loans, can improve your score. Having a balanced mix of revolving and installment credit contributes 10% to your score.

Understanding these factors helps you take steps to improve your credit score and achieve better financial opportunities.

Also Read: What Happens If You Miss a Payment on Consumer Easy Credit?

Improving your score takes effort, but it’s achievable. Let’s talk about how you can take control of your credit score.

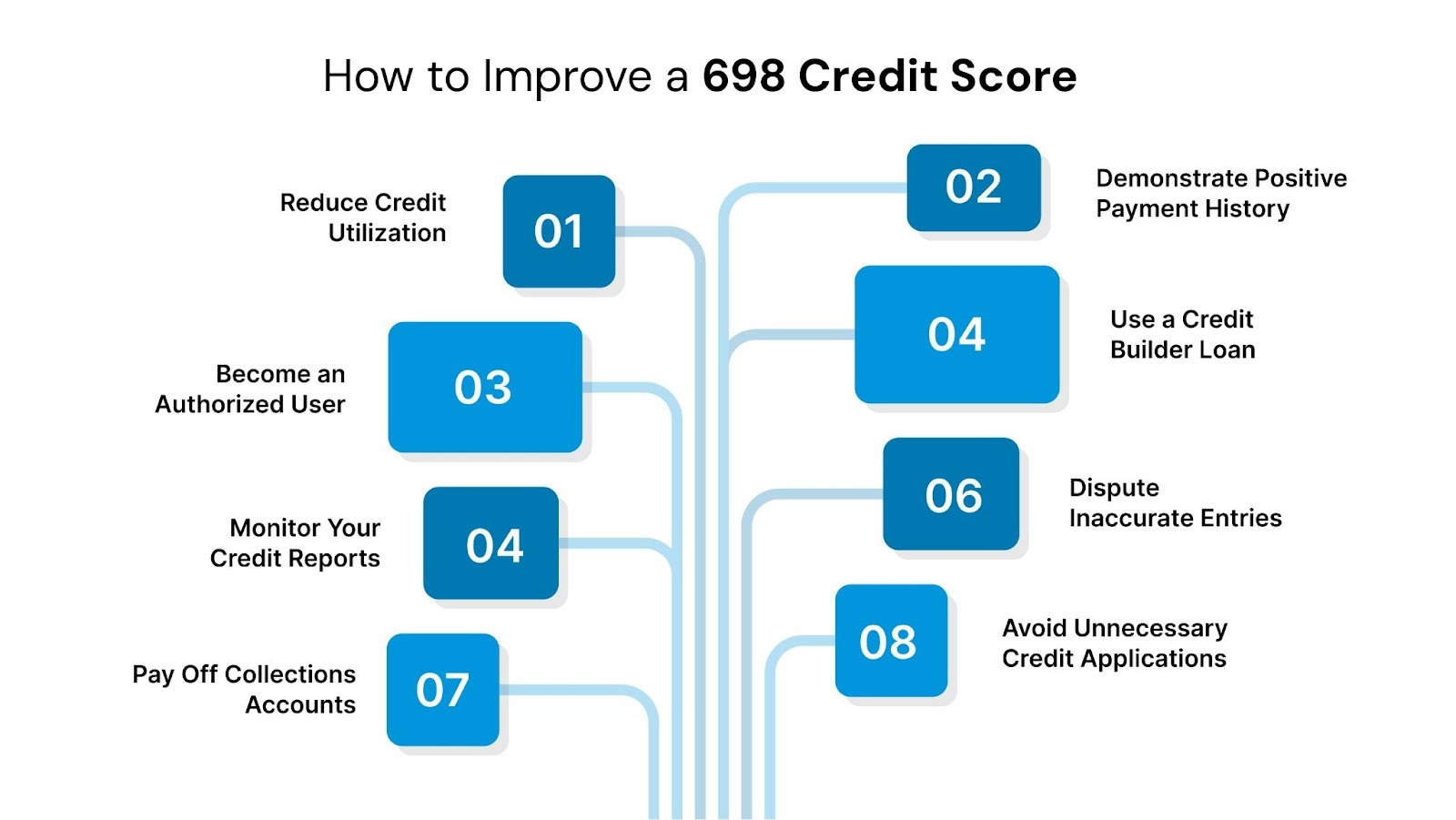

How to Improve a 698 Credit Score

Improving your 698 credit score is possible with consistent effort and smart financial habits. Here’s how you can boost your score:

- Reduce Your Credit Utilization: Keep your credit utilization below 30%, and strive for even lower levels. Pay down credit card balances and avoid maxing out your cards to boost your score.

- Demonstrate a Positive Payment History: Ensure timely payment of all bills. Automating payments can help you stay consistent and avoid missed payments, both of which are key to improving your credit score.

- Become an Authorized User: If you're new to credit, being added as an authorized user on a trusted account can help you build a credit history. If the primary user manages the account well, it can boost your credit score.

- Use a Credit Builder Loan: If your credit history is limited, a credit builder loan can help. These loans are designed to help you build credit by reporting your payments to credit bureaus.

- Monitor Your Credit Reports: Regularly check your credit reports to spot any issues or potential fraud early. This can help you stay on top of any changes that could impact your score.

- Dispute Inaccurate Entries: If there are inaccuracies on your credit report, dispute them. Removing incorrect entries can improve your credit score.

- Pay Off Collections Accounts: Once a collection account is paid off, it will no longer affect your VantageScore 3.0. Bringing the balance to zero is a big step toward improving your score.

- Avoid Applying for Unnecessary Credit: Applying for new credit can result in hard inquiries, which can negatively impact your credit score. Only apply for credit when it's necessary.

Pro Tip: If you pay off a credit card balance, consider keeping the account open. This can help increase the length of your credit history. However, if the card has a high annual fee or tempts you to overspend, it might be better to close it.

Following these strategies can gradually improve your credit score, setting you up for better financial opportunities in the future.

Take control of your financial health today. Contact our financial advisors to create a personalized plan, explore flexible repayment options, and start your journey toward better credit.

Now that you know the steps, it’s time to take action. Let The Forest Hill Management guide you through improving your credit and financial health.

Take Control Of Your Credit Score Today

A 698 credit score places you in a solid position, but there's always room for improvement. With consistent effort, you can boost your score and open doors to better loan rates and financial stability.

If you're looking to improve your credit score and regain control of your financial health, The Forest Hill Management is here to help. Our services are designed to support you every step of the way:

- Personalized Financial Advisory: Work with our experienced advisors who tailor solutions to your unique financial situation, helping you build a stronger credit score.

- Secure Online Payment Platform: Easily manage your payments through our secure platform, streamlining the process of staying on top of your finances.

- Flexible Repayment Options: We offer a range of repayment plans tailored to your budget, making it easier to reduce debt and improve your credit score over time.

- Credit Score Guidance: Get expert advice on how to improve your credit score, manage debt, and make informed decisions that benefit your financial future.

Don’t wait to make progress; take charge of your credit health now. Contact our financial advisors to create a personalized plan to start improving your credit with The Forest Hill Management’s support.

FAQs

1. What’s the ideal credit score for getting better loan rates?

A good credit score is typically 740 or higher. The higher your score, the better your chances of securing lower interest rates and better loan terms.

2. Can I improve my credit score quickly?

While improving your credit score takes time, making small changes, such as paying off high-interest debt and reducing credit card balances, can lead to noticeable improvements over a few months.

3. Does checking my credit score hurt it?

No, checking your own credit score is considered a soft inquiry and won’t impact your score. It’s a good idea to monitor it regularly for any changes.

4. How long does it take to see improvements in my credit score?

It depends on your specific situation, but with consistent effort, you might start seeing improvements within a few months. The key is to stay on top of your payments and manage credit responsibly.

5. Should I close old credit accounts to improve my score?

Not necessarily. Closing old accounts can lower your credit limit and hurt your credit utilization ratio. If you don’t need the card, it’s better to leave it open with no balance.