What is Credit Management? A Complete Guide

Transform Your Financial Future

Contact UsEvery missed payment tells a story. For some, it is a customer who promised to pay “next week.” For others, it is a credit card bill pushed aside to cover rent. You are not alone. Recent data shows that more than 14% of U.S. credit card balances are now over 30 days delinquent (Federal Reserve, 2025). Businesses are also feeling the strain, with nearly half of small firms reporting invoices overdue beyond 30 days (QuickBooks, 2025).

These numbers highlight a reality many face every day. Unpaid bills create stress, weaken cash flow, and make it harder to plan for the future. For businesses, late receivables can slow growth and damage customer relationships. Understanding how to manage credit effectively is the first step toward turning this cycle around.

This blog will break down how credit management works, why it matters, and the tools and strategies you can use to stay in control.

Key Takeaways

- Credit management prevents overdue payments through clear policies and monitoring, while collections focus on recovering past-due debts.

- Setting limits, payment terms, and approval processes ensures businesses and individuals reduce bad debt risk while maintaining trust.

- Key metrics track performance. Days Sales Outstanding (DSO), Average Days Delinquent (ADD), Collection Effectiveness Index (CEI), and Bad Debt % provide insight into whether your credit strategy is working.

- Automation, real-time reporting, and advisory services, such as those from The Forest Hill Management, reduce manual work, enhance compliance, and establish a structured path toward financial stability.

What is Credit Management?

Credit management is the process of establishing credit policies, assessing risks, and ensuring that credit is extended responsibly. In business, it’s all about striking a balance between offering credit to customers and protecting the company from non-payment or bad debt. Effective credit management minimizes risk while maximizing revenue by ensuring that payment terms are clear, appropriate, and consistently enforced.

Key Reasons Why Credit Management Matters

Strong credit management affects cash flow, risk, and customer trust all at once. It shapes how quickly you get paid, how much bad debt you carry, and how confidently you can plan for the future.

- Cash Flow Protection: Well-managed credit ensures that a company has consistent cash flow, allowing it to cover operational expenses and invest in growth.

- Minimized Risk: By assessing the creditworthiness of customers, businesses can reduce the risk of bad debts, defaults, and unnecessary losses.

- Building Stronger Relationships: Clear and fair credit policies build trust and cooperation with customers, ensuring that expectations are aligned and reducing disputes.

- Improved Financial Stability: A structured approach to credit management ensures financial discipline, making it easier to forecast cash flow and manage debts.

- Increases Profitability: Efficient collections and fewer overdue accounts mean that businesses can reinvest funds quickly, driving growth and increasing profitability.

Credit management is not about saying “no.” It is about saying “yes” responsibly and protecting both sides of the agreement.

Difference Between Credit Management and Collections

Credit management and collections are closely related, but they serve different roles in the financial process. Understanding the difference helps you see how both work together to protect cash flow and reduce financial stress.

How They Work Together

When credit management is strong, collections are needed less often. But collections still play a role when issues arise. The two functions complement each other:

- Credit policies set clear expectations from day one.

- Monitoring flags risks early so you can act before debts grow.

- Collections provide a structured process when overdue accounts appear.

Credit management prevents problems. Collections solve them. The most resilient approach combines both.

Now that you know why credit management matters, let’s look at how the process works step by step.

Suggested Read: Is Paying Debt Collection Agencies a Bad Idea?

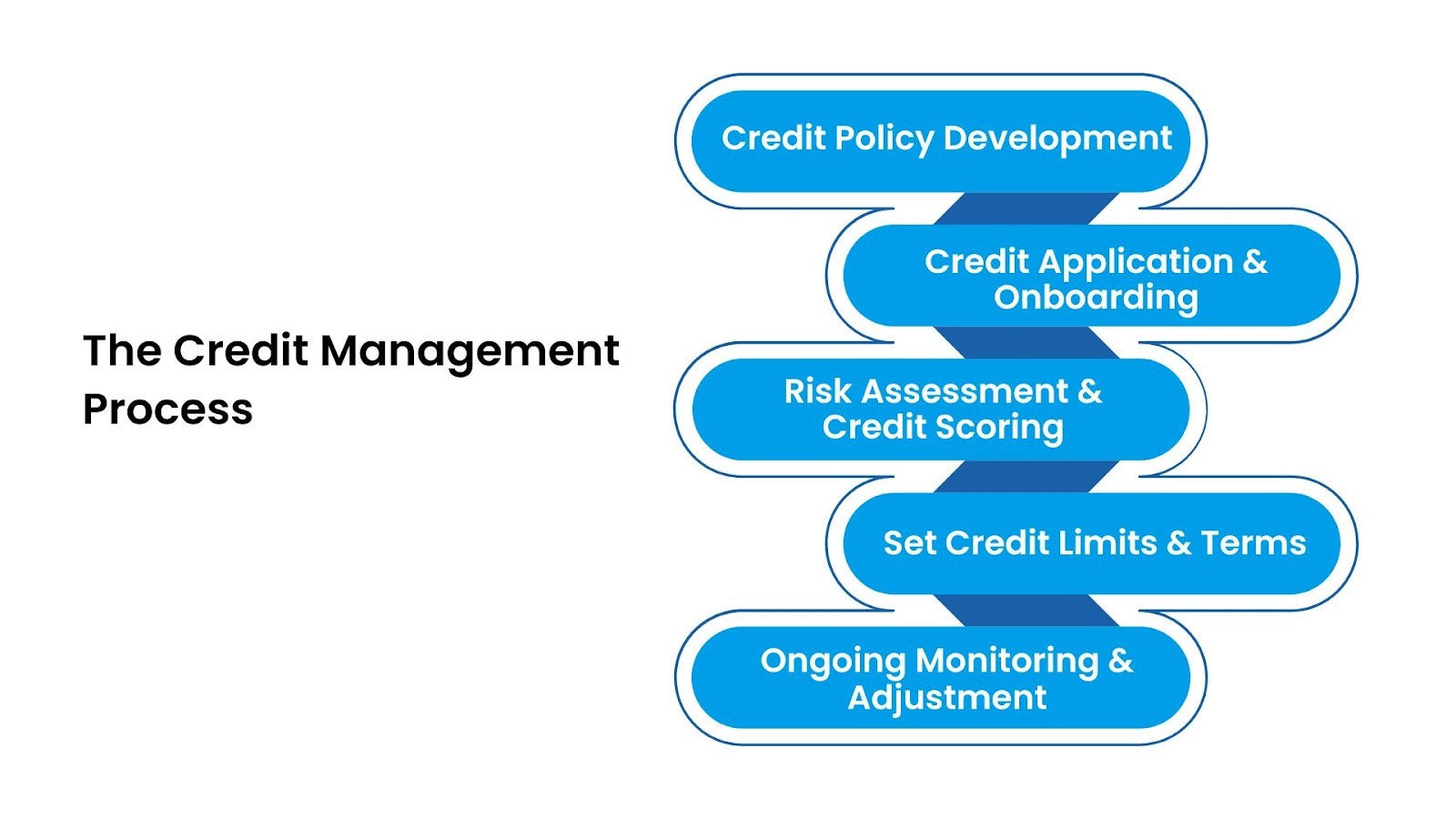

The Credit Management Process

Credit management works best when you follow a structured process. Each step in the process plays a critical role in ensuring that credit is extended responsibly, risk is minimized, and payments are collected on time. Here’s a clear roadmap you can adapt to your situation.

1. Credit Policy Development

The first step in the process is defining your credit policy. This sets the foundation for all your credit decisions and actions.

Key Components of a Credit Policy

- Risk Assessment Framework: Outline the key criteria used to assess the creditworthiness of customers (e.g., credit score, financial health, payment history).

- Establishing Risk Tolerance: Determine how much risk your business is willing to take on. This is often based on the industry, customer history, and the size of the transaction.

- Credit Limit Guidelines: Specify how credit limits are set based on customer risk level and financial capability.

- Payment Terms: Standardize terms such as Net 30, Net 60, or COD based on risk tiers.

- Approval Processes: Define who has the authority to approve credit and set limits. This helps avoid ad hoc decisions that could expose the business to unnecessary risk.

- Review Cycle: Set periodic review dates for credit limits and payment terms to ensure they stay relevant.

2. Credit Application & Onboarding

The credit application process is the gateway to credit management. It’s essential to collect comprehensive information from the customer to make an informed decision about their creditworthiness.

What to Collect in the Credit Application:

- Basic Information: Legal business name, address, phone number, and contact person.

- Trade References: At least 2–3 trade references from current suppliers or business partners.

- Financials: Recent balance sheets, income statements, and cash flow statements (for larger credit lines).

- Credit Bureau Report: Access a credit report from a trusted bureau (e.g., Equifax, Experian) to understand the customer’s credit history.

- Bank References: Contact information for the customer’s bank to assess liquidity and financial stability.

- UCC Search (for secured credit): Conduct a UCC-1 search to determine whether the customer has outstanding secured loans.

- Personal Guarantee (if applicable): For high-risk customers, you may request a personal guarantee from business owners.

Risk Assessment Red Flags:

- A customer’s refusal to provide references or financials could indicate potential risk.

- If the business is unwilling to provide basic company information, it may be an indication that they are trying to avoid scrutiny.

- Be cautious of customers with poor credit history or irregular payment behaviors.

Before approving credit, gather both internal and external data. Combine trade references, credit bureau reports (such as Experian or Equifax), and your own AR history to understand the customer’s financial behavior. Reviewing banking references and financial statements offers context that credit scores alone might miss.

Many businesses apply the 5 Cs of credit: Character, Capacity, Capital, Conditions, and Collateral, to make consistent and fair credit decisions across accounts.

3. Risk Assessment and Credit Scoring

Risk assessment is critical to determine how much credit to extend and under what terms. The assessment should not only rely on credit scores but also consider a customer’s financial stability, payment behavior, and sector risk.

Key Elements of Risk Assessment:

- Financial Ratios:

- Current Ratio: Measures a company's ability to pay short-term obligations with short-term assets.

- Quick Ratio: A more conservative measure of liquidity that excludes inventory from current assets.

- Debt-to-Equity Ratio: Indicates how much debt the business is using to finance its operations compared to its equity.

- Credit History: Review the customer’s credit score and their payment history. Consider the number of recent delinquencies or defaults.

- Industry Risk: Some industries (e.g., high-tech startups, restaurants) may be more volatile than others, affecting their ability to meet credit obligations.

- Geographic Risk: Customers from countries or regions with unstable economies may present a higher risk.

Credit Scoring and Risk Tiers:

- Tier A (Low Risk): Established businesses with strong financials, a high credit score, and a solid payment history. These businesses may receive higher credit limits and more favorable terms (e.g., Net 30).

- Tier B (Moderate Risk): Businesses with some risk factors, such as an average credit score or inconsistent payment history. Credit limits are moderate, and terms are more cautious (e.g., Net 45).

- Tier C (High Risk): New businesses, businesses with poor credit history, or those in high-risk industries. These businesses may require personal guarantees and must be placed on COD or shorter terms.

Go beyond static scores. Use both quantitative ratios (current, quick, debt-to-equity) and qualitative insights such as industry volatility, management stability, and recent payment patterns.

High-performing credit teams often use a credit scorecard that assigns weights to each factor, helping analysts rate risk objectively.

This risk profile becomes the foundation for defining limits and terms. Aligning your risk assessment with industry data and internal trends reduces bias and improves long-term consistency.

4. Set Credit Limits & Terms (and Document Exceptions)

After assessing the customer’s creditworthiness, you need to decide on their credit limit and payment terms.

Credit Limit Determination:

- For Tier A customers, offer generous limits based on their payment behavior and financial stability.

- For Tier B customers, set moderate limits and re-evaluate periodically based on their performance.

- For Tier C customers, limit exposure by offering minimal credit or requiring upfront payment or personal guarantees.

Setting Payment Terms:

- Define payment terms clearly (e.g., Net 30, Net 60) based on the customer’s risk tier and payment history.

- Consider early payment discounts (e.g., 2% off if paid within 10 days) for customers who consistently pay on time.

- Include penalties for overdue accounts, such as late fees or interest charges, to encourage prompt payments.

Documenting Exceptions:

- For customers who are exceptions to the policy (e.g., offering longer terms to a high-risk customer), document the reasoning behind the decision, the approving authority, and the review date for reassessment.

- Keep a record of all exceptions and ensure they are reviewed periodically to ensure that the risk profile has not changed.

Translate the credit review outcome into specific limits and payment conditions. Use results from your scorecard or rating to guide maximum exposure, acceptable payment terms, and any need for collateral or guarantees.

For higher-risk accounts, conditional approvals, such as shorter initial terms or limits that increase with proven payment reliability, can support sales while protecting cash flow.

5. Ongoing Monitoring and Adjustment

Even after extending credit, ongoing monitoring is crucial to ensure that your business is not exposed to unnecessary risk.

- Monitor Payment Behavior: Regularly check customers’ payment histories. Track Days Sales Outstanding (DSO) and Average Days Delinquent (ADD) to stay informed on potential issues before they grow.

- Adjust Credit Limits and Terms: Based on the monitoring of customer behavior, adjust their credit limits and terms as necessary. For example, if a customer’s financial situation worsens, you may reduce their credit limit or adjust payment terms.

Schedule periodic reviews, every 6 to 12 months for low- to medium-risk customers and more often for high-risk ones. Set up trigger-based reassessments when red flags appear, like late payments, order spikes, or negative news.

Use automation tools to pull real-time data from accounting systems and credit bureaus, alerting you to shifts before they impact cash flow. Automation also ensures consistency across teams and minimizes manual review fatigue.

Tips for a High-Performing Credit Manager

Being an effective credit manager involves more than policy-writing and monitoring receivables. The best credit leaders combine strong processes with sharp judgment, clear communication, and strategic thinking. Below are key practices that set top performers apart:

1. Align with sales and finance: A strong credit manager works closely with sales and finance, agreeing on clear credit policies, approval limits, and escalation paths so growth and risk stay in balance.

2. Make decisions driven by data: Use internal data (DSO, aging, dispute rates) together with external signals (credit bureau scores, industry risk) to tier customers, set limits, and adjust terms before problems show up in cash flow.

3. Communicate early and professionally: High performers don’t wait for invoices to go badly overdue; they set expectations upfront, send friendly reminders, and keep conversations firm but respectful to protect both relationships and receivables.

4. Use automation to handle the routine: Automate credit checks, reminders, and risk alerts so your time goes into judgment calls and complex accounts instead of manual data entry and follow-ups.

5. Keep learning and refining policy: Top credit managers review credit policies regularly, stay informed on regulatory changes and market conditions, and update limits, terms, and processes as the portfolio and economy shift.

Having the process in place is one thing, but best practices are what truly make a credit management strategy effective. Let’s explore the key best practices you should follow.

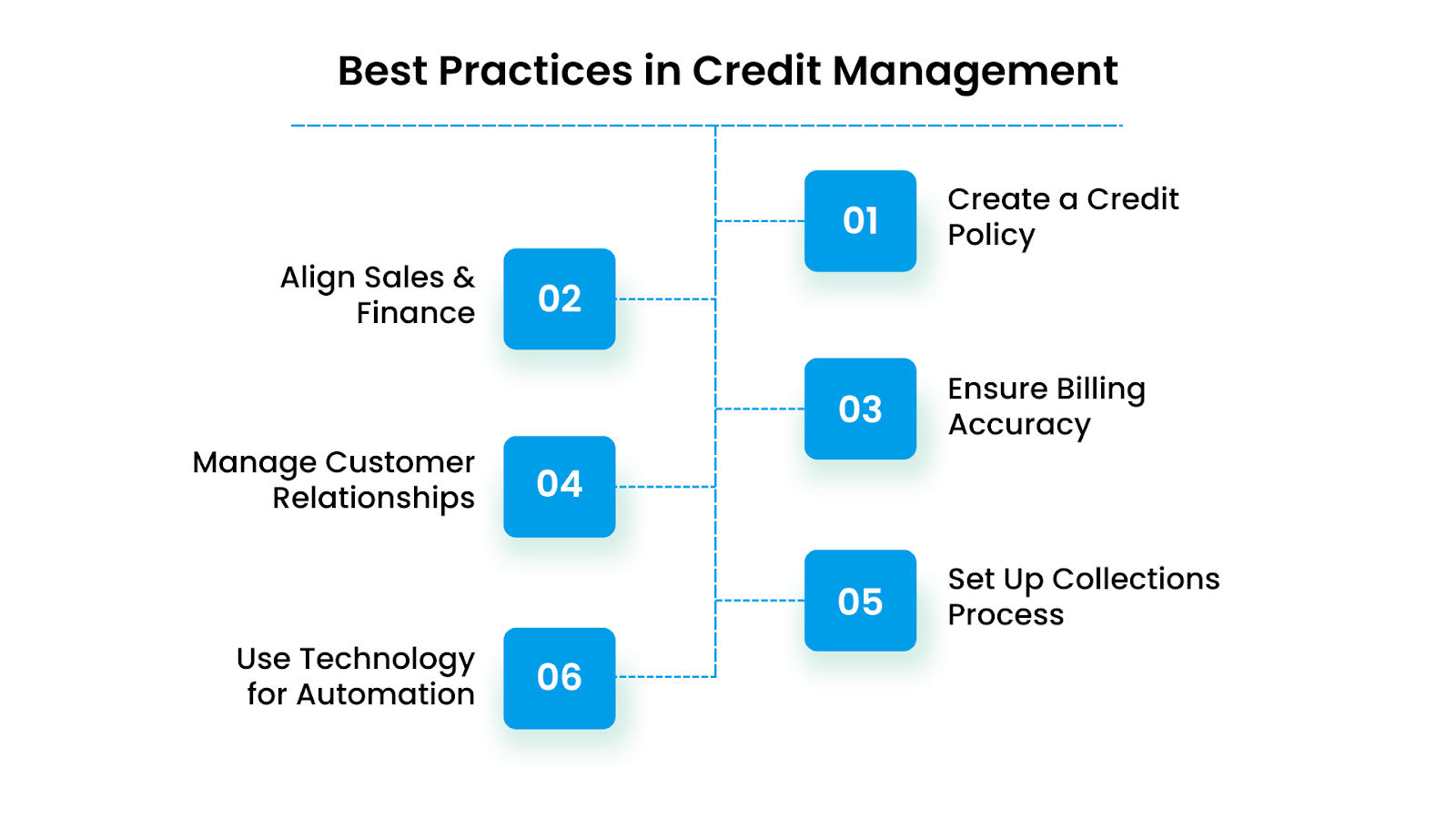

Best Practices in Credit Management

A strong process gives you structure, but best practices are what keep credit management effective over time. Without them, even the best policies can fall apart, leading to delayed payments, rising debt, and damaged trust. By applying proven methods, you reduce risk and build consistency in business credit.

1. Create a Formal Credit Policy

A written policy prevents guesswork. It ensures everyone involved understands the rules and applies them consistently.

- Define payment terms clearly (Net 30, Net 60, or custom terms).

- State who has the authority to approve or decline new credit requests.

- Train your team so that sales, finance, and collections follow the same guidelines.

2. Align Sales and Finance Teams

When sales and finance work in silos, customers may be offered credit that the business cannot afford to risk. Alignment creates balance.

- Use a shared system so sales can check credit limits before closing deals.

- Review customer credit trends together in regular meetings.

- Set clear approval processes to avoid overextending credit.

3. Ensure Billing Accuracy and Timeliness

One of the most common reasons for delayed payments is simple errors. Wrong amounts or late invoices create friction and slow down cash flow.

- Automate invoice generation to reduce mistakes.

- Send invoices immediately after goods or services are delivered.

- Use reminders before, on, and after due dates.

- Track Days Sales Outstanding (DSO) to measure collection performance.

4. Manage Customer Relationships (CRM)

Credit management is not just numbers. It is also about maintaining open, respectful communication. Strong relationships reduce disputes and improve recovery.

- Contact customers before payments are late.

- Keep a record of every discussion in a CRM tool.

- Show flexibility in genuine hardship cases while protecting your policy.

5. Set Up a Collections Process

A clear collection process avoids confusion and ensures you act at the right time. It also keeps the tone professional instead of confrontational.

- Day 1: Send a friendly reminder.

- Day 7: Follow up with a firm but polite message.

- Day 14: Escalate the reminder and apply late fees if stated in policy.

- Day 30+: Consider legal action or outside collection support.

A respectful reminder today prevents conflict tomorrow and often improves payment results.

6. Use Technology for Automation and Monitoring

Utilizing credit management software automates tasks like risk assessment, invoicing, and payment reminders. These tools improve accuracy, save time, and provide real-time visibility into key metrics like DSO and ADD, allowing for faster and more informed decision-making.

With best practices in place, your credit management becomes more predictable and less stressful. Now let’s look at real-world examples to understand how these strategies work in practice.

Need help managing overdue payments or creating a repayment plan?

At The Forest Hill Management, we make credit management simpler with flexible repayment options and clear financial guidance. Contact us today for a free consultation and take the first step toward financial control.

Real-World Examples of Credit Management

Concepts make sense on paper, but they become much clearer when you see them in action. These examples show how credit management decisions play out in everyday scenarios, giving you a better sense of the opportunities and risks involved.

Example 1: Managing a Cash Sale

A business receives payment immediately for goods or services.

- Journal entry: DR Cash 5,000; CR Sales Revenue 5,000

- Impact: Cash flow improves instantly with no collection risk.

- Lesson: Cash sales are the safest, but not always realistic if customers expect credit.

Example 2: Extending Credit to a Customer

A company allows a customer to pay later, creating accounts receivable.

- Journal entry: DR Accounts Receivable 3,000; CR Sales Revenue 3,000

- Impact: Sales increase, but collection risk grows if the customer delays payment.

- Lesson: Extending credit supports growth, but you must set terms and monitor Days Sales Outstanding (DSO) to protect cash flow.

Example 3: Paying for Services (Expense Management)

A business pays for utilities, showing the role of expense tracking in overall credit health.

- Journal entry: DR Utility Expense 600; CR Cash 600

- Impact: Reduces available cash, but ensures operations continue.

- Lesson: Even simple expenses affect liquidity. Tracking them carefully helps avoid overextension when debt obligations are due.

Example 4: Receiving a Loan for Business Expansion

A company borrows money to grow operations, adding both opportunity and obligation.

- Journal entry: DR Cash 10,000; CR Loan Payable 10,000

- Impact: Provides immediate funds for investment, but creates long-term repayment commitments.

- Lesson: Loans can fuel growth, but repayment schedules and interest costs must be managed to prevent future strain.

Every credit transaction has two sides: opportunity and risk. The goal of credit management is not to avoid risk entirely, but to balance it in a way that supports stability and growth.

These scenarios show how credit decisions affect cash flow, risk, and future planning. To know if your approach is working, you need to measure performance with the right metrics.

Also Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

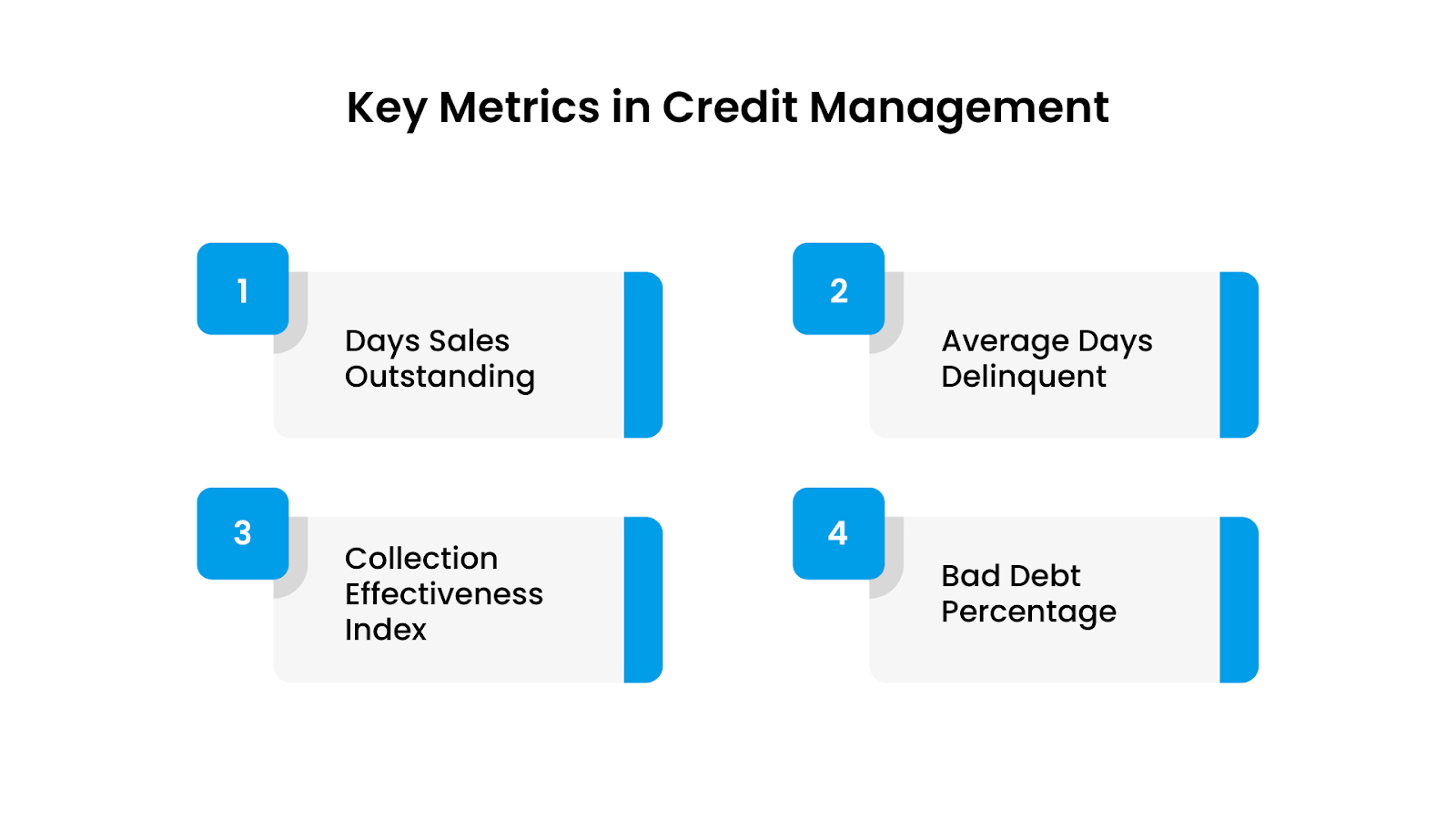

Key Metrics in Credit Management

Measuring progress is just as important as setting up processes. Without the right metrics, you won’t know whether your approach is working or needs adjustment. These are the critical indicators to track.

1. Days Sales Outstanding (DSO)

What it measures: How many days, on average, it takes to collect payment after a credit sale.

Formula (simplified):

DSO = (Accounts Receivable ÷ Net Credit Sales) × Number of Days

Benchmarks (U.S., by industry):

- Retail often sees a DSO of around 30-40 days.

- Manufacturing generally falls around 30-60 days.

- Construction companies often have longer cycles, with 60-90 days being common.

- Some service‐based industries (consulting, architectural & engineering) have DSOs well above 70 days.

Example:

Suppose you run a small manufacturing business. Over 30 days, your Net Credit Sales are $100,000, and your Accounts Receivable is $50,000. Then:

DSO = (50,000 ÷ 100,000) × 30 = 15 days

If your industry benchmark is ~40-60 days, a 15-day DSO is excellent. It means you collect much faster than average, strong cash flow. But if your business model or terms (e.g., your contracts allow Net 60-90) expect slower payments, this might indicate discounting or overly aggressive collection practices.

2. Average Days Delinquent (ADD)

What it measures: How many days past due invoices sit on average.

Relation to DSO:

ADD = DSO − “Best Possible DSO” (i.e., what your DSO would be if all customers paid on schedule)

Benchmarks / Context:

- If your DSO is 45 days but many invoices are due in 30 days, your ADD would be ~15 days; this signals slow late payments.

- In many industries, an ADD above 10-15 days is a warning sign that your collections process needs tightening. (While specific industry numbers are less often published for ADD, trends in DSO and overdue receivables help approximate.)

Example:

Let’s say for a consulting firm, the DSO is 60 days. Their payment terms are “Net 30”. So the Best Possible DSO is 30 days. Thus:

ADD = 60 − 30 = 30 days

That means customers are, on average, 30 days late. That’s high and suggests risk: you might need stricter reminders or penalties.

3. Collection Effectiveness Index (CEI)

What it measures: How efficiently you collect within a period relative to what was collectable.

Formula:

CEI = (Beginning Receivables + Credit Sales − Ending Receivables) ÷ (Beginning Receivables + Credit Sales − Ending Current Receivables) × 100

Benchmarks:

- Across industries, the typical CEI tends to be around 75-90%.

- Companies with strong AR policies and automated collections often push CEI above 90%, especially in consumer goods or retail, where disputes & late payments are lower.

Example:

If at the start of a quarter your receivables were $100,000, you made $200,000 in credit sales during the quarter, and ended with $80,000 in receivables (of which $70,000 are current), then:

CEI = (100,000 + 200,000 − 80,000) ÷ (100,000 + 200,000 − 70,000) × 100

= (220,000) ÷ (230,000) × 100 ≈ 95.7%

That’s strong. It means the collections are very effective compared to what could have been collected.

4. Bad Debt Percentage

What it measures: The portion of sales written off as uncollectible.

Formula:

Bad Debt % = (Bad Debt ÷ Total Sales) × 100

Benchmarks:

- For large, well-managed companies (e.g., Fortune 1000), the Bad Debt to Sales ratio often hovers around 0.1-0.5%.

- Industries with higher risk (e.g., healthcare, consumer credit) see higher percentages, sometimes 2-5% or more. E.g., hospitals often report bad debt of 4-8% of revenues.

Example:

If your business records $1,000,000 in sales in a year and writes off $2,000 as bad debt, then:

Bad Debt % = (2,000 ÷ 1,000,000) × 100 = 0.2%

If your industry average is 0.5%, you are doing well. If you are in healthcare or a high default area, you might expect higher, but you should aim to keep this under 2-3% if possible.

Use benchmarks as guides, not strict rules. Always adjust for your business model, customer base, terms, and industry norms.

With metrics in place, you can measure progress and stay ahead of risks. Next, let’s explore the legal and risk considerations that shape credit management decisions.

Tracking credit metrics can feel stressful, but you don’t have to manage it alone.

Our advisors at The Forest Hill Management work with you to review your situation, set up personalized repayment strategies, and reduce the stress of managing debt on your own. Reach out now for confidential support and take back control of your finances.

Also Read: Consumer Impact Recovery and Debt Collection Guide

How The Forest Hill Management Can Help You Strengthen Credit Management

At The Forest Hill Management, we understand that managing credit effectively can feel overwhelming. That’s why we provide services designed to simplify the process, reduce stress, and help you take control of your financial future.

Here’s how we support you:

1. Portfolio Management

You can easily track overdue accounts and update payment statuses. The Forest Hill Management handles the routine tasks so you can focus on growing your business. With real-time tracking and automated reporting, you'll have more control over your finances.

2. Portfolio Acquisitions

Identify profitable opportunities quickly and get the insights you need to make faster decisions while ensuring due diligence is handled efficiently. We make the process smooth and compliant, so you can grow without the headaches.

3. Compliance & Technology Solutions

You can prioritize your business's security with compliance and technology solutions. Automation ensures that you meet industry regulations while safeguarding your financial data.

4. Personalized Financial Advisory Services

Get personalized financial advisory services to assess your unique needs and design automation strategies that align with your business, improving efficiency and cash flow.

5. Flexible Repayment Options

We set up flexible repayment options for your customers, offering automated payment plans and reminders to ensure timely payments and reduce overdue accounts.

By partnering with The Forest Hill Management, you can move from reactive collections to proactive credit management. We help you automate the routine, stay compliant, and keep cash flow steady.

Take the first step today. Contact our financial advisors for a free, confidential consultation and discover how we can tailor a credit management plan to your needs.

Conclusion

Credit management can feel complex, but the rewards are clear: reduced stress, stronger financial control, and a more secure future. By following a structured process, applying best practices, and using the right tools, you can turn debt from a source of anxiety into an area of confidence.

At The Forest Hill Management, we’re dedicated to helping individuals take that step with clarity and support. Our financial advisors work with you to explore flexible repayment options and provide the guidance you need to create a plan that truly fits your situation.

Contact us today for a free, confidential consultation and begin your journey toward financial stability with a trusted partner by your side.

FAQs

1. What is credit management, and how does it differ from debt collection?

Credit management is the process of assessing creditworthiness, setting terms, monitoring accounts, and preventing late payments. Debt collection (or collections) is what happens when payments become delinquent; it involves reminders, negotiations, and recovery efforts.

2. When do I know that credit control failed and I need help with collections?

If multiple payments slip past due, customer accounts become aged, or your own cash flow is suffering, that signals credit control gaps. At that point, structured collections efforts or outside support can help recover overdue amounts.

3. How does the collections process legally operate in the U.S.?

Collections in the U.S. must follow rules under the Fair Debt Collection Practices Act (FDCPA). Collectors can’t harass, misrepresent, or abuse the person. They must identify themselves and provide certain disclosures.

4. What are the key components of an effective credit management system?

Key components include developing clear credit policies, assessing customer creditworthiness, setting appropriate credit limits and payment terms, continuous monitoring of customer payment behavior, and implementing effective collection strategies for overdue accounts.