How America Collects Debt: Your Rights & Options Explained

Need Help Reviewing Your Account?

Contact UsThe first collection notice often feels confusing. One message, one balance, and suddenly you’re dealing with an unfamiliar financial system that already has momentum.

What most people don’t realize is that this system was designed to be structured, supervised, and rule-bound from the start. Debt collection in the U.S. operates at a national scale under federal oversight, primarily enforced by the Consumer Financial Protection Bureau, with agencies tracking complaints and setting standards for how consumers must be treated.

That changes the frame. You aren’t stepping into chaos. You’re entering a process built around documentation, communication limits, and defined consumer protections.

In this article, we’ll explain how debt collection works in the U.S. and how understanding the system can help you respond with confidence.

Key Takeaways

- Debt collection in the U.S. is structured and federally regulated, so understanding the system lets you act strategically instead of reacting emotionally.

- Your engagement influences outcomes: timely communication and documentation can prevent escalation, reduce fees, and protect credit.

- Legal protections hold collectors accountable, giving you leverage if errors or abusive tactics occur.

- Knowing your options: dispute, verify, negotiate, lets you control financial decisions instead of feeling trapped.

- Being organized and informed makes debt resolution manageable rather than overwhelming.

How Debt Collection Works in the United States

Missing a payment does not immediately send an account to collections. At first, the account becomes delinquent, and the original creditor usually contacts you with reminders by mail, email, or phone. This commonly happens within the first 30-60 days past due, though timelines vary by creditor.

If the account remains unpaid, many creditors may choose—often between 90 and 180 days past due, to either:

- Assign the debt to a third-party collection agency while retaining ownership, or

- Sell the debt, transferring ownership to a debt buyer.

These timeframes are common but not required by federal law and can differ based on the creditor, debt type, and state law. Your legal rights exist throughout the process, but Fair Debt Collection Practices Act (FDCPA) protections apply most clearly once a third-party collector is involved.

Federal Laws That Govern Debt Collection in America

The Fair Debt Collection Practices Act, passed in 1977, created the legal boundaries for how third-party collectors can interact with consumers. The Consumer Financial Protection Bureau (CFPB) enforces these rules by supervising collectors, issuing regulations, tracking complaints, and taking legal action against violators, alongside state regulators and attorneys general.

States may add stronger protections on top of federal law. For example, California restricts certain contact practices, and New York requires debt collectors to be licensed. These laws do not replace the FDCPA; they supplement it.

Also Read: How to Keep Your Debt Resolutions in 2026

Within this legal framework, the FDCPA sets explicit limits on collector behavior.

What Debt Collectors Cannot Do Under Federal Law

Federal law prohibits debt collectors from using abusive, deceptive, or unfair tactics when attempting to collect a debt. These rules are designed to prevent harassment, protect consumers from false claims, and limit improper collection practices.

Here’s what debt collectors are not allowed to do:

- Harass or abuse you: including repeated calls meant to annoy, obscene or profane language, threats of violence, or publicly listing you as a non-payer.

- Misrepresent themselves or their authority: such as posing as an attorney, government official, or credit bureau, falsely accusing you of a crime, or threatening arrest or legal action they cannot legally take.

- Use unfair collection practices: including charging unauthorized fees or interest, mishandling postdated checks, or contacting you at work when they know or should know your employer prohibits personal calls.

Next, let’s take a closer look at the specific actions debt collectors are required to take to stay compliant.

What Debt Collectors Must Do to Stay Compliant

Under FDCPA §809(a), a collector must send a written notice within 5 days of the first communication if the initial contact was oral. This notice includes the creditor's name, the amount owed, and a clear statement of your right to dispute the debt within 30 days.

If you dispute in writing within that window, collection activity must pause until the agency provides verification. They need to show documentation proving the debt is yours, and the amount is accurate. Collectors must generally stop contacting you if you send a written cease communication request, except to notify you of specific actions such as filing a lawsuit.

The exception: they can notify you if they're taking specific action, like filing a lawsuit.

Also Read: Best Finance Advisory Service Providers for Debt Management

Knowing the rules only helps if you understand how they apply when an agency actually reaches out.

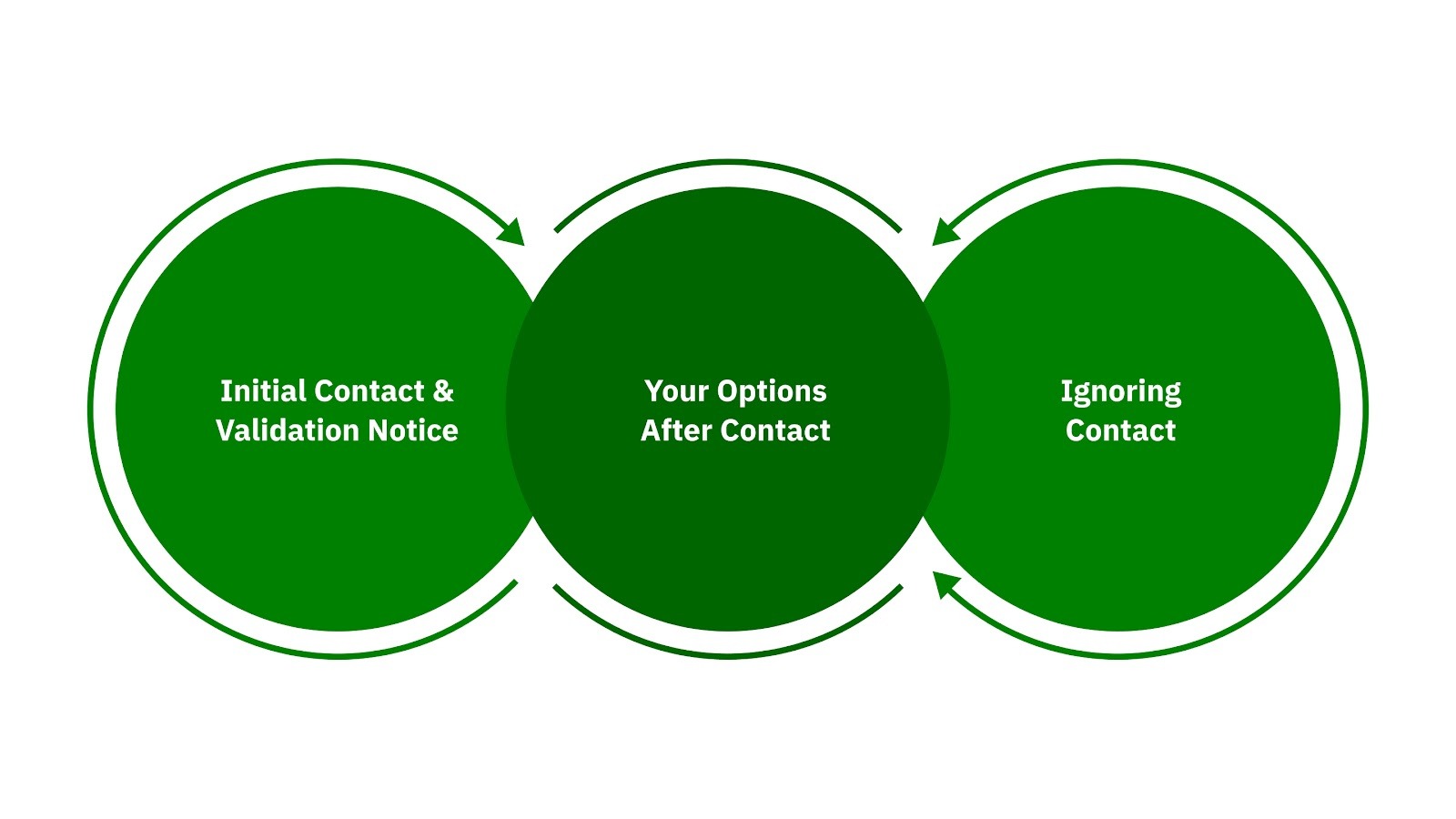

The Debt Collection Process from Initial Contact to Resolution

Debt collection generally follows a standard process, though details may vary by agency. Federal law sets clear rules about how collectors must communicate and what rights you have.

1. Initial Contact and Validation Notice

When a collector first contacts you, whether by phone, mail, email, or text, the written validation notice they send must include:

- The amount of the debt

- The name of the creditor

- A statement of your right to dispute the debt within 30 days

If you do not dispute the debt within 30 days, the collector may assume it is valid.

2. Your Options After Contact

Once you receive the notice, you have three main options:

- Dispute the debt: If you believe the debt is inaccurate, not yours, or the amount is wrong, send a written dispute within 30 days. The collector must pause collection activities until they provide verification showing the debt is valid and the amount is correct.

- Request more information: Even if you don’t dispute the debt, you can ask for documentation such as statements or payment history. Collectors are required to provide this if requested.

- Negotiate payment: If the debt is accurate, you can discuss payment plans or settlements. Always get any agreement in writing, including the amount, payment schedule, and confirmation that the debt will be considered satisfied once you pay.

3. Ignoring Contact

Ignoring collection attempts does not erase the debt. Possible consequences include continued reporting to credit bureaus, potential lawsuits, and wage garnishment if a court judgment is obtained.

Settlement and Payment Plans

- Settlements: You may negotiate to pay less than the full balance in exchange for closing the account. Amounts accepted vary by agency and account history.

- Payment Plans: Collectors may allow you to spread payments over time. Terms vary, and some agencies may charge interest or fees. Written documentation of any plan is essential to protect your rights.

Also Read: Why One-Size-Fits-All Debt Solutions Don't Work for Real Relief

These options only work if you know your legal standing at the start of the process.

Your Rights as a Consumer in Debt Collection

Debt collection operates within a structured system, and as a consumer, you’re not powerless; you have ways to influence how the process unfolds. Understanding your position helps you respond strategically and avoid unnecessary stress.

- You can participate, not just react: Collectors expect a response, but how and when you engage is your choice. Being proactive can prevent escalation, reduce fees, and limit negative credit reporting.

- You have leverage through documentation: Requests, disputes, and written communication create a paper trail that protects you if disagreements arise.

- The system assumes fair play: Agencies are legally bound to follow rules, and regulators monitor compliance. Knowing this gives you confidence to push back against errors or abusive tactics.

- Legal oversight exists: Complaints and enforcement by the CFPB, state agencies, or courts provide avenues for resolution if a collector steps out of line.

- Financial decisions are yours to control: Even if a debt is valid, you choose whether to settle, negotiate a plan, or contest errors. Your rights give structure to those decisions.

Knowing what's legally required is different from knowing what happens when you work with an agency that treats compliance as more than a checkbox.

How Forest Hill Management Approaches Debt Resolution

When Forest Hill Management contacts you about a past-due account, we operate within a framework designed to help you resolve your debt while respecting your rights and financial reality.

Here’s what our approach looks like in practice:

- Full FDCPA compliance in every interaction, from initial contact to final resolution

- Clear validation notices explaining the debt, original creditor, and your right to dispute within 30 days

- Flexible repayment options, including plans customized to your budget, settlement opportunities, or extended schedules

- Respectful communication through your preferred channel: online portal, phone, or written correspondence

- Transparent account management, allowing you to track balances, payment history, and progress anytime online

We understand that dealing with debt can feel overwhelming. Our goal isn’t to add stress; it’s to work with you toward a resolution that protects your rights and fits your circumstances.

Conclusion

Debt collection in the U.S. follows clear rules designed to protect your rights while providing a path to resolution. Knowing what to expect, from validation notices to your repayment options, gives you control and confidence.

If you have an account with Forest Hill Management, we’re here to help you take the next step without added stress. You can make a payment online today, explore flexible repayment options, or speak with our advisors at (888) 471-0109 for personalized guidance tailored to your situation.

If your account is managed by The Forest Hill Management, support and clear next steps are available to help you move forward with confidence.

FAQs

1. How does debt affect my ability to rent or lease a home?

Landlords often check credit reports before approving a rental. Outstanding debts may lower your credit score and influence rental decisions, though it doesn’t automatically prevent you from securing housing.

2. Are there protections for debt owed by a deceased family member?

Generally, debts do not automatically transfer to relatives unless they co-signed. Estate assets may be used to settle outstanding obligations, but surviving family members usually aren’t personally liable for the debt.

3. How long do debts stay on my credit report?

Most debts remain on your credit report for up to seven years from the date of the first delinquency. This includes accounts sent to collections, which can affect credit history and future lending decisions.

4. Can a debt collector contact me outside of normal business hours?

Debt collectors are generally restricted to reasonable hours, usually between 8 a.m. and 9 p.m., local time. Contact outside these hours is considered harassment under U.S. regulations.