Calculate the Impact of Your Credit Score on Loan Offers

Transform Your Financial Future

Contact UsYour credit score can significantly impact the loan offers you receive. According to Experian, the average FICO® Score in the United States reached 715, influencing everything from interest rates to loan approvals. This level determines everything from your loan approval odds to the interest rate you will pay.

Even a slight difference in your score, say 20 points, can change how much you pay over time. Understanding this impact can help you make smarter financial decisions before you borrow.

In this guide, you will learn how your credit score shapes loan offers, what lenders really look for, and how you can calculate the impact of credit scores on loans before signing any agreement.

Let's start with the basics:

- Credit scores influence more than just loan approval. They determine your interest rates, credit limits, and even how flexible your repayment terms can be.

- A FICO® Score is the model most lenders use. It is based on five key factors: payment history, credit utilization, length of credit history, credit mix, and new inquiries, each showing how responsibly you manage credit.

- Small score changes can mean big cost differences. Even a 20–30 point increase in your score can lead to lower interest rates and save you thousands of dollars over the life of a loan.

- Debt-to-income ratio matters as much as credit. Keeping your monthly debt payments below 36% of your income helps lenders see that you can manage additional credit comfortably.

- Improving credit takes time, not perfection. Paying bills on time, reducing balances, and avoiding unnecessary credit applications are the simplest ways to build lasting financial stability.

Why Your Credit Score Matters More Than You Think

Your credit score is a three-digit number that reflects how responsibly you manage credit and repay borrowed money. It tells lenders whether you are a reliable borrower and helps them decide your loan terms, credit limits, and interest rates.

The most widely used scoring system is the FICO® Score, developed by the Fair Isaac Corporation. According to Experian, 90% of top lenders utilize FICO scores.

Some credit monitoring apps, such as Credit Karma, use a different model called VantageScore. This is actually why the number you see there might differ slightly from your official FICO Score.

Under the FICO® model, your score is calculated based on five key factors:

- Payment History (35%): This shows how consistently you pay your bills on time. Even one missed or late payment can lower your score because lenders see it as a sign of higher risk.

- Amounts Owed / Credit Utilization (30%): This measures how much of your available credit you are currently using. Keeping your balances below 30% of your total limit helps you appear more financially responsible.

- Length of Credit History (15%): The longer your accounts have been open, the better. A long, stable credit history demonstrates experience managing debt.

- Credit Mix (10%): Having a variety of credit types can improve your score. It shows lenders you can manage different forms of credit effectively.

- New Credit (10%): Each time you apply for new credit, there is a huge possibility of a hard inquiry appearing on your report. Too many inquiries within a short time may make you look financially overextended.

Together, these components form a clear picture of your financial trustworthiness, not your personal worth. A lower score does not define who you are. It simply highlights areas where you can take small, consistent steps toward stronger financial health.

Now that you understand what your credit score represents, the next step is learning how it affects the loan offers you receive.

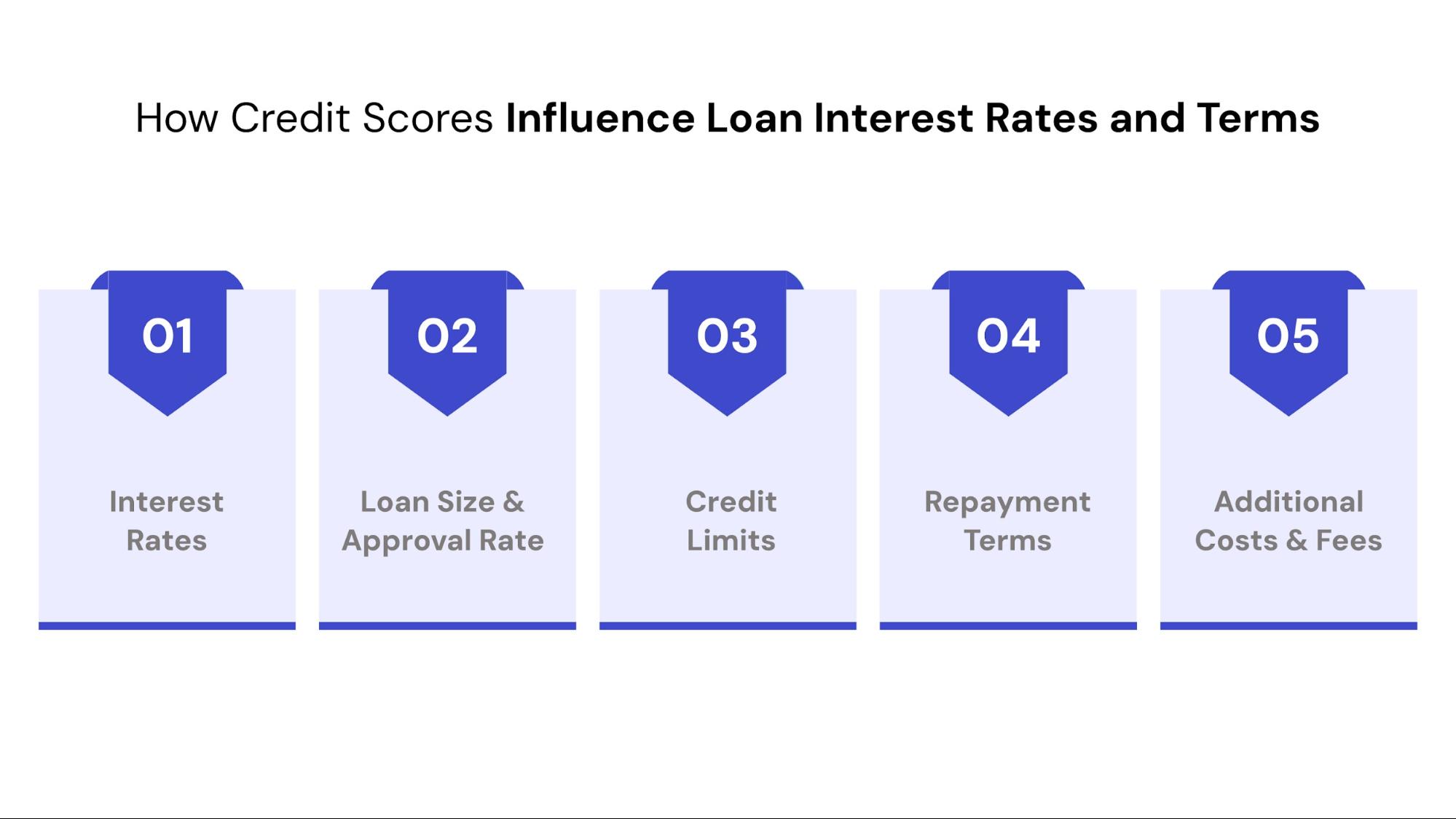

How Credit Scores Influence Loan Interest Rates and Terms

Your credit score plays a major role in shaping how lenders evaluate your applications and what terms you are offered.

According to the Consumer Financial Protection Bureau (CFPB), “Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products.”

A higher score can open the door to lower interest rates, higher limits, and more favorable repayment options, while a lower score can mean higher costs or limited access to credit.

These are a few ways credit scores can impact your loan terms:

1. Interest Rates

Lenders view your credit score as a reflection of risk. The higher your score, the less risk they perceive, which often translates to lower interest rates.

- Example: A borrower with a 780 FICO Score might get a 6% APR, while someone with a 620 could face 12% on the same loan.

- You should reflect on the fact that tiny differences in interest rates can potentially lead to thousands in extra payments over the loan’s lifetime.

- This difference reflects lenders’ confidence in your ability to repay on time.

2. Loan Amount and Approval Odds

Your credit score also determines whether you can borrow at all. These are a few things you should consider:

- Higher scores typically lead to larger loan approvals and more flexible limits.

- Lower scores might result in smaller loan offers or requests for co-signers.

- Example: A strong credit profile can help you qualify for a $25,000 auto loan, while a fair score might limit approval to $10,000 or less.

3. Credit Limits

For revolving credit, such as credit cards, your score affects both the limit and the interest rate you receive.

- Excellent credit can earn higher credit limits and lower annual percentage rates (APRs).

- Weaker credit usually means lower limits and higher interest charges to offset perceived risk.

- Responsible use of existing credit helps increase your limit over time.

4. Repayment Terms

Lenders often use your score to determine how flexible they can be with repayment schedules.

- A higher score may qualify you for longer terms and smaller monthly payments.

- Borrowers with lower scores may face shorter repayment windows or stricter conditions.

- Example: A 750-score borrower may get a 60-month auto loan, while a 620-score borrower might only qualify for 36 months.

5. Additional Costs and Fees

Beyond interest, your score can affect other loan-related expenses.

- Lower credit scores often trigger higher down payments or origination fees.

- You may also face higher insurance premiums in certain states where credit is a factor.

- These costs reflect how lenders and insurers balance their perceived risk.

At Forest Hill Management, we are here to make repayment simpler. We provide secure online payment options, flexible repayment arrangements, and personalized support to help you manage your account responsibly and reduce financial stress. Make a payment today and come a step closer to improving your credit score.

Suggested Read: Essential Personal Finance Tips for Beginners

Estimating the Loan Impact of Your Credit Score

Understanding how your credit score affects loan terms can help you make more confident decisions about borrowing. Even minor improvements in your score can make a meaningful difference in the long run, and that is something within your control.

Step 1: Check Your Credit Score Before You Apply

Before estimating your loan costs, start by determining your current credit standing. You can check your score through Experian, Equifax, or TransUnion, or by using trusted credit monitoring tools.

Viewing your own credit score is a soft inquiry, which will not affect your score. Look for small errors like old accounts or incorrect payment details. Fixing these can give your score a natural boost. Checking regularly helps you see your progress and prepare for upcoming financial decisions.

Step 2: Compare Loan Scenarios Side by Side

Different credit score ranges can change your borrowing costs more than you might expect. Here is an example of how your score could affect a $10,000 personal loan:

- Example:

As you can see, a difference of even 100 points in your credit score can mean paying thousands more in interest. Improving your score, even by a small amount, can open doors to more affordable options over time.

Step 3: Look Beyond the Numbers

Your credit score matters, but it is only one part of your financial picture. Lenders also consider other aspects that can work in your favor.

- Debt-to-Income Balance: This shows how much of your income goes toward existing debt. Keeping it balanced helps lenders see that you can manage new payments comfortably.

- Steady Income and Employment: Consistency tells lenders that you are dependable. This is something that you need to show through years of responsible work.

- Positive Trends: Improvement matters more than perfection. A growing score indicates effort and progress, which lenders take notice of.

- Loan Type and Purpose: Some loans, like auto or personal loans, may weigh credit factors differently. Understanding this helps you prepare better.

- Collateral (for secured loans): If you are applying for a secured loan, offering collateral such as savings or a vehicle can sometimes make approval easier.

When you look at these factors together, your score becomes less intimidating. It is simply one part of a bigger story that reflects your financial journey and growth.

But before you can take action, you need to know where your score stands. Is it strong enough to unlock better offers, or is it holding you back from the financial relief you deserve? Let’s walk through what counts as a “good” score and how you can check yours today—quickly, securely, and without hurting your credit.

Suggested Read: How to Diversify Your Income Streams Successfully

Is Your Credit Score in the Safe Zone?

Your credit score is not fixed. It moves with your financial habits. Checking it regularly helps you stay informed and make proactive choices before applying for new credit.

You can check your credit score through several reliable U.S. platforms:

- AnnualCreditReport.com: The only federally authorized website that provides free weekly access to your credit reports from Experian, Equifax, and TransUnion.

- Experian, Equifax, and TransUnion websites directly: Each bureau may show slight score differences, but all are accurate reflections of your credit history.

- Credit Karma or Credit Sesame: These free apps display your VantageScore, which may differ slightly from your FICO® Score, but still offer valuable insight into your overall credit health.

Remember, checking your own credit score is a soft inquiry — it will not hurt your score. In fact, regular monitoring is a healthy financial habit that helps you notice trends early and make informed choices.

Further Insight: Is 698 a Good Credit Score?

What is a Good Credit Score?

Credit scores typically range from 300 to 850, and lenders group them into categories. Each range tells a different story about your borrowing potential.

Table showing credit score range:

If your score is not where you want it to be, do not lose heart. Improving it takes time, but even small, consistent steps, like paying bills on time and keeping balances low, can help move you into a safer zone.

If your credit score is not where you want it to be, remember that progress often starts with consistency. At Forest Hill Management, we understand that financial setbacks happen. Our role is to help you manage your existing account with clarity and support. Every on-time payment and responsible step forward moves you closer to regaining control of your financial story. Speak to our financial advisors today.

Suggested Read: Debt Settlement Explained: How It Works and If It's a Good Option for You

The Hidden Role of Debt-to-Income Ratio (DTI)

Your debt-to-income ratio (DTI) represents the percentage of your monthly income that goes toward debt payments, including credit cards, loans, and mortgages. Even with a strong credit score, a high DTI can make lenders cautious because it suggests that too much of your income already goes toward existing debt.

A lower DTI signals a healthy financial balance, while a higher one suggests limited flexibility. These are a few key points to keep in mind about your DTI:

- How It Is Calculated: Divide your total monthly debt payments by your gross monthly income, then multiply by 100.

- Ideal Range: Most lenders prefer a DTI below 35%, though some may accept up to 49% depending on the loan type.

- Why It Matters: A lower DTI means you have more income available to manage new payments, giving lenders greater confidence in your repayment ability.

- What It Includes: All recurring monthly debt obligations, such as rent or mortgage payments, car loans, credit cards, student loans, and personal loans.

- What It Excludes: Everyday expenses like groceries, utilities, or insurance premiums are not factored into your DTI calculation.

Example:

If you earn $5,000 per month and pay $1,500 toward debts, your DTI is 30% ($1,500 ÷ $5,000 × 100).

Maintaining a balanced DTI can strengthen your overall lending profile, even if your credit score still needs improvement. It shows that you are handling your financial commitments responsibly. This is a quality lenders view as just as important as your score itself.

Building credit takes time, but every small step improves your chances of qualifying for fairer loan terms. The next step shows steps you can take to improve your credit score and loan terms.

Suggested Read: Calculating Financial Freedom Number using Passive Income Formula

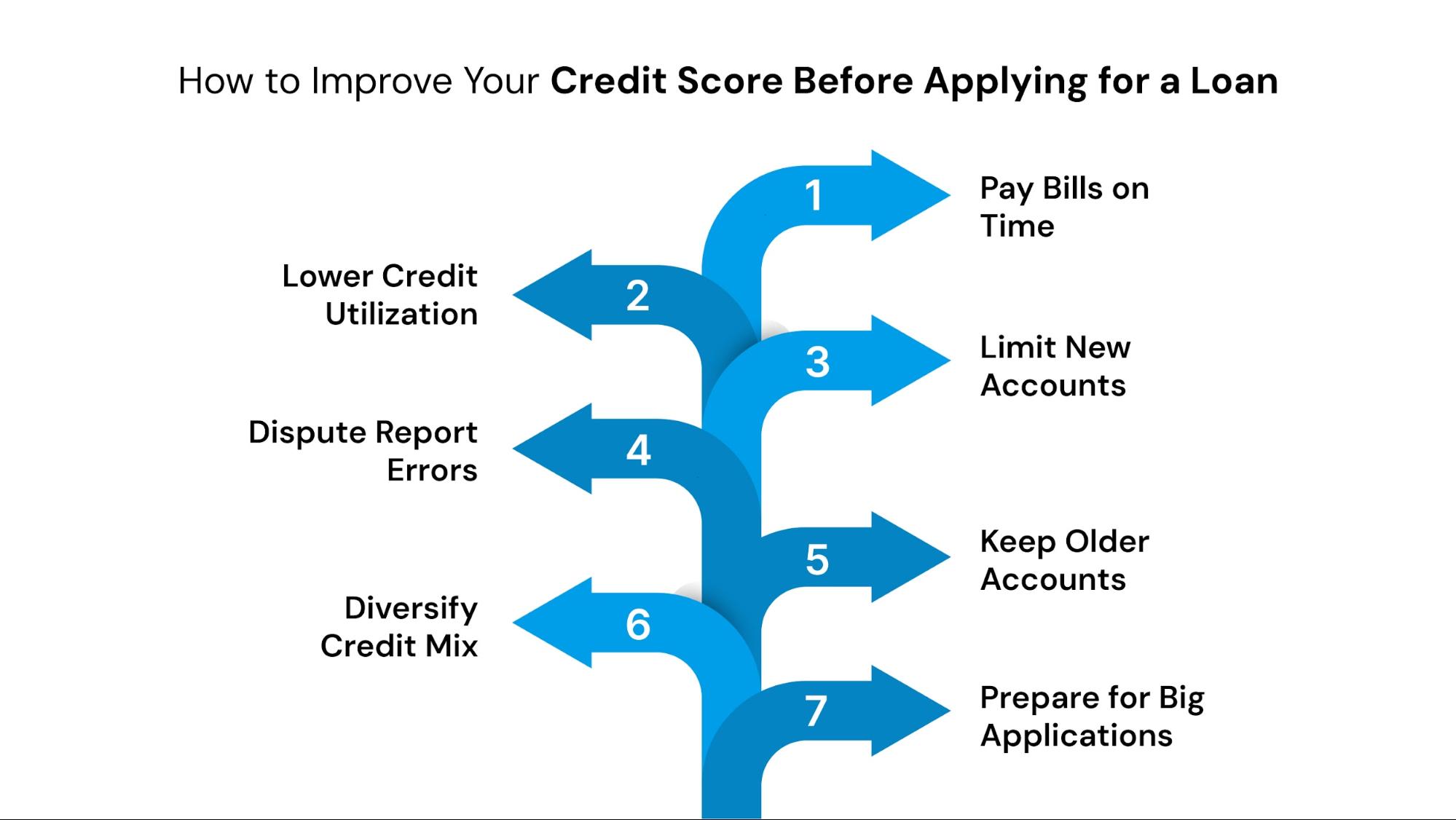

How to Improve Your Credit Score Before Applying for a Loan

Small, steady changes in how you manage credit can make a noticeable difference in a few months. The goal is to show lenders that you can handle credit responsibly, which can lead to better approval odds, lower interest rates, and more flexible terms.

Here are practical ways to strengthen your credit score before you apply for a new loan:

- Pay Bills on Time: Payment history makes up the largest portion of your FICO® Score. Setting reminders or automating payments ensures you never miss a due date. Even one late payment can have a lasting effect.

- Reduce Credit Utilization: Try to use less than 30% of your total available credit. Paying down balances and keeping older cards open (even if unused) can lower your utilization ratio and improve your score.

- Avoid Opening Too Many Accounts at Once: Each new credit application triggers a hard inquiry that can slightly reduce your score. Apply only when necessary, and space out applications to minimize impact.

- Dispute Errors on Your Credit Report: Review your credit reports from Experian, Equifax, and TransUnion for any inaccuracies. Even a small reporting mistake, like an outdated balance, can affect your score, so it is worth correcting early.

- Keep Older Accounts Open: The length of your credit history helps build trust with lenders. Closing old accounts shortens that history and can raise your utilization percentage, both of which may lower your score.

- Diversify Your Credit Mix: Having a combination of credit types, such as a credit card, car loan, or installment account, demonstrates your ability to manage different forms of debt responsibly.

- Plan Ahead for Big Applications: If you are planning a major loan, like a mortgage or auto loan, start improving your score at least three to six months in advance. This gives positive changes time to register with credit bureaus.

Each of these steps shows lenders a pattern of responsible behavior, something that weighs heavily in your favor when you apply for new credit. Now that you know how to improve your score, let us look at common misconceptions that could be holding you back.

Further Insight: How to Win Debt Collection Disputes: A Complete Step-by-Step Guide

Credit Score Myths That Could Be Costing You

Misunderstanding how credit scores work can lead to habits that unintentionally lower your score or prevent it from improving. Clearing up these myths can help you focus on the actions that truly make a difference in your financial progress.

Here are some of the most common credit score myths and the truth behind them:

1. Myth: Checking Your Credit Hurts Your Score

Checking your own credit is considered a soft inquiry and does not affect your score. Only hard inquiries, made when you apply for credit, can cause a slight, temporary dip. Regularly checking your score helps you track progress and catch errors early.

2. Myth: You Should Carry a Balance to Build Credit

Carrying a balance from month to month does not help your score. It just costs you interest. Paying your credit card in full and on time is what strengthens your score, showing that you can manage credit responsibly.

3. Myth: Closing Old Accounts Improves Your Score

Closing old credit cards can actually lower your score because it reduces your total available credit and shortens your credit history. Keep older accounts open, even if you use them rarely, to maintain your positive credit length.

4. Myth: Paying Off Debt Erases It From Your Report Immediately

Paying off debt is always a positive step, but accounts remain on your report for a period of time. This can range from up to seven years for some loans. What matters is that they are marked “paid” or “closed in good standing.”

5. Myth: All Credit Scores Are the Same

Different scoring models exist, such as FICO® and VantageScore, and they can produce slightly different numbers. Most lenders rely on FICO, while free apps like Credit Karma show VantageScores for monitoring purposes.

Believing these myths can lead to frustration and confusion, especially when you are doing your best to make progress. The truth is, building credit takes time, awareness, and a clear understanding of how your actions are measured.

Now that you know what to focus on, and what to ignore, let us talk about how Forest Hill Management helps individuals already working toward financial stability manage their existing accounts with confidence.

When Debt Feels Overwhelming, Know Your Options

Debt can be stressful, especially when it feels like you are doing everything right, yet progress still seems slow. The truth is, many people find themselves in the same position at some point in their lives. What matters most is knowing that you have options and support systems designed to help you move forward at a manageable pace.

At Forest Hill Management, our goal is to make repayment more transparent and less stressful. We understand that every financial situation is unique, which is why we offer solutions that make managing your balance simpler, safer, and more personal.

Here is how we help:

- Flexible Repayment Terms: We work with you to find a repayment schedule that fits your financial circumstances, helping you stay consistent without added strain.

- Secure Online Payments: Our digital platform allows you to make payments easily and safely, giving you peace of mind with every transaction.

- Personalized Financial Guidance: Our advisors are here to answer questions and help you better understand your repayment options, so you can make confident decisions.

- Clear Communication: You always know where your account stands. We keep things transparent, simple, and respectful.

- Supportive Approach: We recognize that financial challenges can happen to anyone, and we are here to assist without judgment or pressure.

At Forest Hill Management, we believe that repayment is not just about closing an account; it is about helping you rebuild financial confidence one step at a time. Each payment you make is progress, and progress, no matter how small, always matters.

Conclusion

When you understand how credit works, you give yourself the power to make informed decisions about borrowing, repayment, and long-term financial stability. Even gradual improvements in your score can open the door to better loan options and greater peace of mind.

Forest Hill Management can make your financial path more manageable. With flexible repayment terms, secure online payment options, and personalized financial guidance, we help you stay on track and move toward lasting financial balance.

Take control of your financial path today. Contact us to explore your repayment options.

Frequently Asked Questions

1. What Is the Fastest Way to See a Positive Change in My Credit Score?

The quickest improvement usually comes from paying down existing balances and making all payments on time. Lowering your credit utilization ratio — the amount of credit you use compared to your limit — can raise your score within a few billing cycles.

2. How Often Should I Review My Credit Report?

It is wise to review your credit report from each major bureau — Experian, Equifax, and TransUnion — at least a few times a year. You can access all three for free through AnnualCreditReport.com, the only federally authorized site for credit reports in the United States.

3. Can Paying Off Debt Improve My Credit Score Right Away?

Yes, though the timing varies. Paying down credit cards or loans can reduce your utilization rate and raise your score within a month or two. Updates from creditors typically appear after the next reporting cycle.

4. What Should I Do If I Find an Error on My Credit Report?

If you notice incorrect information, such as an outdated balance or a payment marked late by mistake, contact the credit bureau that reported it. Correcting errors ensures your score accurately reflects your financial behavior.

5. How Long Does It Take to Rebuild Credit After Financial Setbacks?

Credit rebuilding is a gradual process, but consistency makes a difference. With steady on-time payments, low balances, and limited new inquiries, many people begin seeing meaningful improvement within six to twelve months. Over time, those small habits lead to lasting credit strength.