California Debt Collection Laws: Know Your Rights in 2026

Need Help Reviewing Your Account?

Contact UsIn 2024 alone, consumers filed roughly 207,800 debt-collection complaints nationwide. That number exists because collection activity can significantly affect consumers’ financial and emotional well-being.

California gives you more protection than most places, but protection only works if you know how to use it. That's where California debt collection laws matter, especially when calls start piling up or letters arrive without warning.

These rules exist to rebalance power when money stress already has you on edge. They draw clear lines around contact, honesty, and proof, so you can slow the process down, verify what's real, and respond with control instead of panic.

This article breaks down California's protections, what collectors must disclose, what's illegal, and how to protect yourself while resolving debt.

Key Takeaways

- Knowing your rights lets you control collection, verify debts, and avoid paying under pressure.

- Collectors have limits; spotting harassment or deception early and documenting it protects you.

- Time-barred debt generally cannot be enforced through a lawsuit, but certain actions such as making a payment or acknowledging the debt may affect applicable timelines.

- Written disputes, cease-and-desist letters, and regulatory complaints can stop illegal behavior.

- Clear communication, documented agreements, and secure payments reduce confusion and strengthen your position.

What Makes California Debt Collection Laws Different

Most states rely solely on federal protections. California built something stronger. The Rosenthal Fair Debt Collection Practices Act (RFDCPA) extends beyond what federal law covers. While the federal FDCPA only applies to third-party collectors, California's law includes original creditors, the companies you originally borrowed from.

That means broader oversight, fewer loopholes, and more accountability when someone contacts you about money you owe. If you're dealing with a collection agency or the original lender, California law applies.

That distinction matters when you're deciding whether to push back on unfair contact or demand proof of what you owe.

Who Must Follow California's Debt Collection Laws

California doesn't limit enforcement to one type of collector. The law casts a wide net, which works in your favor when you're trying to figure out who's allowed to do what.

Here's who must comply:

- Third-party collection agencies hired to recover debts

- Debt buyers who purchased your account from the original creditor

- Original creditors collecting on their own outstanding balances

- Attorneys acting on behalf of creditors to pursue collection

Understanding who's bound by these rules helps you recognize when someone steps out of line.

What Debt Collectors Cannot Do in California?

California law defines hard limits on behavior that crosses into harassment, deception, or intimidation. Knowing what's off-limits gives you the language to stop illegal tactics the moment they happen.

1. Threats of Arrest or Jail Time

Unpaid consumer debts such as credit cards or medical bills are civil matters, not criminal charges. If a collector implies otherwise, they're breaking the law. Debtors' prisons don't exist in the U.S., and criminal charges don't apply to civil debt. Threatening arrest is a scare tactic designed to make you act out of fear instead of clarity.

2. Calls Outside Allowed Hours

Your evenings and mornings are protected. Collectors cannot contact you before 8 AM or after 9 PM in your time zone. If they do, document it. Repeated violations show a pattern, and patterns strengthen your case if you decide to file a complaint or pursue legal action.

3. Harassment Through Repeated Contact

California law prohibits using the phone to harass, oppress, or abuse you. That includes calling multiple times a day with no legitimate purpose, leaving aggressive voicemails, or contacting you immediately after you've asked them to stop.

There is no fixed call limit, but intent and context matter, and extreme conduct may also violate Penal Code § 653m, though most cases are handled under civil law.

4. Lying About the Amount You Owe

Collectors must tell you the truth about your balance. Inflating the amount, adding fees that don't exist, or claiming you owe more than the account shows is illegal. If the numbers don't match what you remember or what your records reflect, you have the right to dispute and demand verification.

5. Contacting Your Employer or Family

Collectors can contact third parties only to locate you, not to discuss your debt. They can't tell your boss, coworkers, or relatives that you owe money. If they do, that's a violation. The law protects your privacy and your reputation, even when an account is past due.

Also Read: How a Portfolio Management Service Helps You Stay on Track

Once you know the boundaries, the next question becomes what collectors are required to tell you.

What Collectors Must Tell You in California

California law doesn't just restrict bad behavior; it mandates transparency. Collectors can't stay vague or hide details that affect your ability to respond. They're required to give you specific information upfront, and that information determines whether you challenge the debt, negotiate, or verify before you pay.

Every communication must include:

- The collector's name and the company they represent

- The name of the original creditor who initiated the account

- The exact amount they claim you owe

- A clear statement of your right to dispute the debt within 30 days

- Disclosure if the statute of limitations has expired on the debt

These disclosures aren't suggestions. If a collector skips them, you have grounds to question the legitimacy of the contact and file a complaint.

Understanding Time-Barred Debt in California

Debt doesn't disappear, but the legal power to sue you for it does. California uses statutes of limitations to set deadlines on how long creditors can take you to court. Once that window closes, the debt becomes time-barred.

For written contracts like credit cards and loans, the statute of limitations is four years. For oral agreements, it's two years. Time-barred means a collector can't sue you to force payment. They can still ask, send letters, or call within legal boundaries, but they lose the courtroom as leverage.

In some cases, certain actions such as making a payment or acknowledging the debt may affect applicable legal timelines. That's why verifying the age of a debt before you respond is critical.

Also Read: Debt Mediation and Repayment Strategies: A Clear Guide

Understanding time-barred debt puts the law on your side, but only if collectors follow it. When they don’t, it’s important to know how to respond.

What to Do If a Collector Violates the Law

Violations may require documentation and formal reporting in order to be addressed. If someone crosses a legal line, you have to act. The law gives you tools, but only if you use them while the details are still fresh and provable.

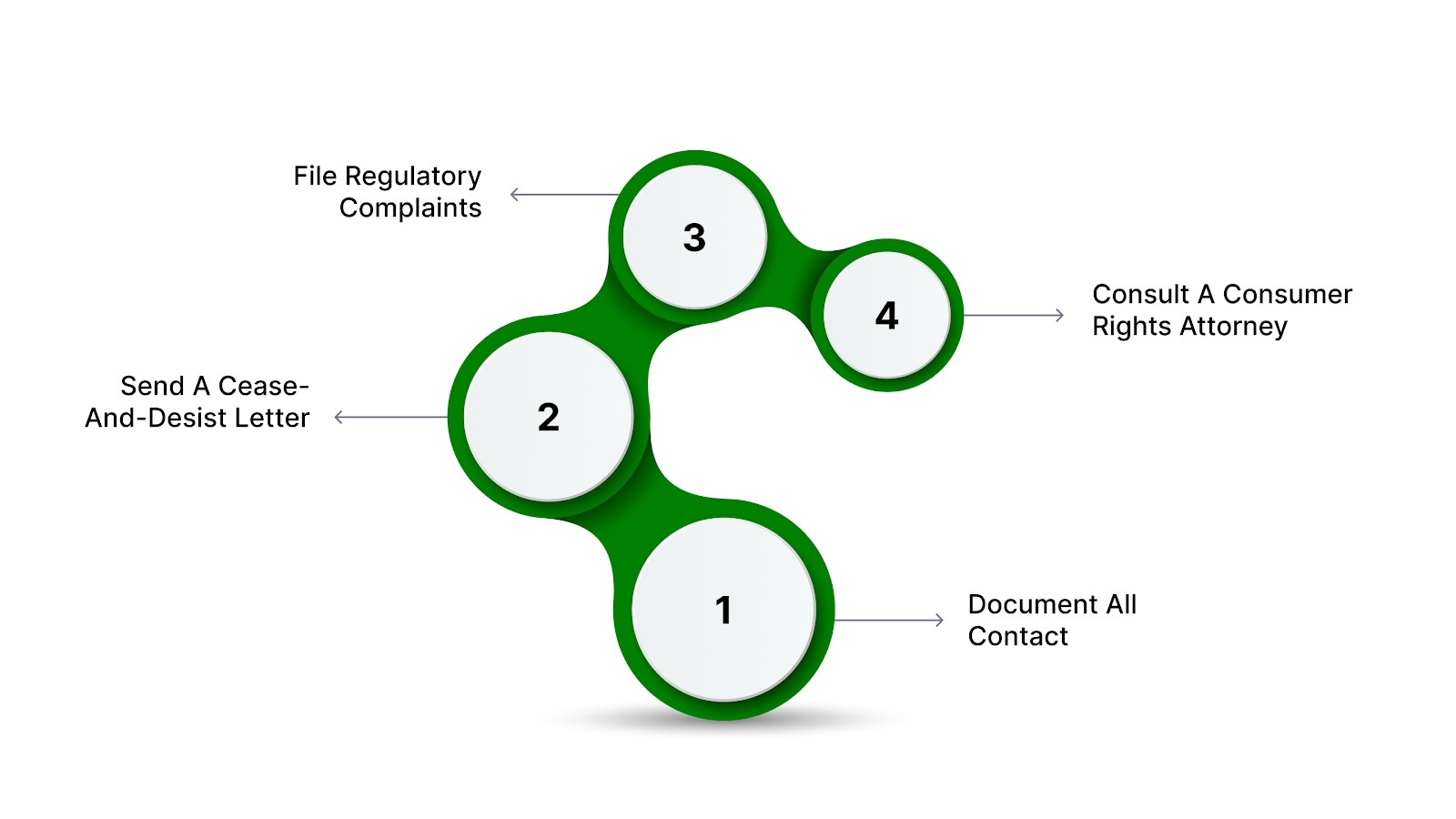

1. Document Everything

Write down the date, time, and content of every call. Save voicemails, letters, and text messages. If they called outside legal hours, threatened you, or lied about the debt, you need a record. Memory fades, but documentation holds up when you file a complaint or speak to an attorney.

2. Send a Written Cease-and-Desist Letter

You can tell a collector to stop contacting you entirely. Send a written letter via certified mail stating you want all communication to cease. Once they receive it, they can only contact you to confirm they'll stop or notify you of specific legal action. It won't erase the debt, but it stops the calls.

3. File Complaints with Regulatory Agencies

Report violations to the California Department of Financial Protection and Innovation (DFPI) and the Consumer Financial Protection Bureau (CFPB). Both agencies track patterns of abuse and can investigate collectors who repeatedly break the law. Your complaint becomes part of a larger record that can trigger enforcement.

4. Consult a Consumer Rights Attorney

Some violations come with financial penalties, and you may be entitled to damages. Attorneys who specialize in consumer protection often work on contingency, meaning you don't pay upfront. A consultation can clarify whether you have a case worth pursuing and what your options are beyond filing complaints.

Taking action when the law is broken shifts the power dynamic back in your direction.

How to Protect Yourself During Collection

Even lawful collection efforts can feel intrusive if you don't control the process. Protecting yourself doesn't mean avoiding debt; it means managing when and how you engage, so you make decisions based on facts rather than pressure.

Here's what helps:

- Never provide payment information unless you initiated the contact

- Request all communication in writing if phone calls feel overwhelming or aggressive

- Keep copies of every letter, notice, and payment confirmation you receive

- Verify the debt’s legitimacy and age before agreeing to any payment arrangement

You're allowed to slow things down, ask questions, and demand proof. Collectors benefit when you act quickly without checking details. You benefit when you take the time to confirm what's accurate and what's not.

Also Read: 6 Steps to Get Out of Debt on a Low Income Fast

Once you know how to protect yourself as a consumer, the next step is understanding how those protections should show up in real interactions with a collection agency.

How These Laws Apply When You're Working With a Collection Agency

California's debt collection laws aren't abstract rules. They shape how real conversations, notices, and payment options should be handled when an account is being managed.

When you work with a collection agency in California, lawful conduct should include:

- Clear identification of the company contacting you and the original creditor

- Honest communication about the balance and the status of the account

- Respect for reasonable communication times and your stated preferences

- No misleading legal pressure or threats that aren't legally allowed

- Secure payment options designed to protect your privacy

At Forest Hill Management, these principles guide how consumer accounts involving California residents are handled. The goal is to reduce confusion, follow applicable state and federal laws, and give you a clear path forward without unnecessary pressure.

Conclusion

California debt collection laws exist because the alternative: unregulated contact, vague disclosures, and pressure-based tactics, caused real harm. The protections you have now didn't appear by accident. They were built to give you leverage when someone else controls the timeline and the tone.

Knowing your rights changes how the process unfolds. You can demand proof, set boundaries, stop illegal contact, and choose when and how you respond. Those aren't small things when stress is already high, and options feel limited.

If you're dealing with collection in California, you're not operating in a vacuum. The law is specific, enforceable, and designed to keep the process fair. Use it. When you're ready to move forward, Forest Hill Management offers secure online payments and secure payment options and clear account information designed to support compliance and transparency.

Contact our team if you need assistance understanding your account or accessing secure payment options.

FAQs

1. Can I negotiate a debt settlement for less than I owe?

Yes, some creditors or collectors may agree to a lump-sum payment that’s lower than your full balance. Settlement agreements are legally binding, so it’s important to get everything in writing and confirm that the creditor reports the account accurately to credit bureaus.

2. How does bankruptcy affect my ability to repay or negotiate debts?

Filing for bankruptcy can pause most collection activity and may discharge certain debts entirely. It also creates a formal repayment plan for remaining obligations, giving you legal protection from creditors while restructuring your finances.

3. Are there tax implications if a debt is forgiven?

Debt forgiven or canceled may be considered taxable income by the IRS in certain circumstances. For example, if a creditor agrees to reduce your balance, the forgiven portion could be reported as income, so it’s wise to consult a tax professional.

4. What is a “debt validation notice” and how is it different from proof of debt?

A debt validation notice is a formal communication a collector must provide when requested, showing the debt exists and detailing the creditor, balance, and your rights. It is slightly different from proof of debt in court, which may require original account statements or contracts.

5. Can debt collectors sue in small claims court, and what should I know?

Collectors can file suits in small claims court if they believe the debt is valid and within the statute of limitations. Small claims courts are generally faster and simpler than higher courts, but you still have the right to defend yourself, request evidence, and negotiate settlements before or during the hearing.