Debt Resolution vs Debt Consolidation: Key Differences

Need Help Reviewing Your Account?

Contact UsDebt rarely shows up as a single, simple problem. It builds quietly. A missed payment here, a growing balance there, and suddenly you’re dealing with terms like “debt consolidation” and “debt settlement” without a clear sense of what they actually mean for you.

And you’re not alone in that confusion. According to Yahoo Finance, U.S. household debt crossed $18.8 trillion in Q2 2025, with credit card balances alone reaching record highs. As debt levels rise, so does the number of people trying to figure out the right way to manage or resolve it.

The challenge is that these options are often presented as interchangeable, when in reality, they apply to very different situations. Choosing the wrong one can waste time, delay action, or make things feel more complicated than they need to be.

In this blog, we’ll break down the difference between debt consolidation and debt resolution, how each one works, and how to understand which path actually fits your situation so you can move forward with clarity.

Key Takeaways

- Debt consolidation and debt resolution are not interchangeable, as they apply to completely different stages of debt and financial situations.

- Consolidation is typically used to manage multiple active debts, while resolution focuses on closing accounts that are already past due or in collections.

- Eligibility plays a major role, since consolidation depends on credit approval, whereas resolution is based on the status of the existing account.

- The right option depends on your current position, not preference, and choosing incorrectly can delay progress or limit available solutions.

- Taking early, informed action and understanding your account clearly can make the entire process more manageable and less stressful.

Debt Settlement and Debt Consolidation Defined

Both debt resolution and debt consolidation are ways to deal with debt, but they apply to very different situations. One focuses on managing multiple active debts, while the other deals with accounts that have already fallen behind.

Understanding how each works helps you identify which option is actually relevant to your current situation.

What is Debt Resolution?

Debt resolution, often used interchangeably with debt settlement, is a strategy for dealing with an existing debt by working toward an agreement with creditors.

In practice, that means asking a creditor to accept less than the full balance owed, sometimes through a lump-sum payment or a series of installments. This approach is typically considered for accounts that are already significantly past due, and it can have a damaging effect on credit history.

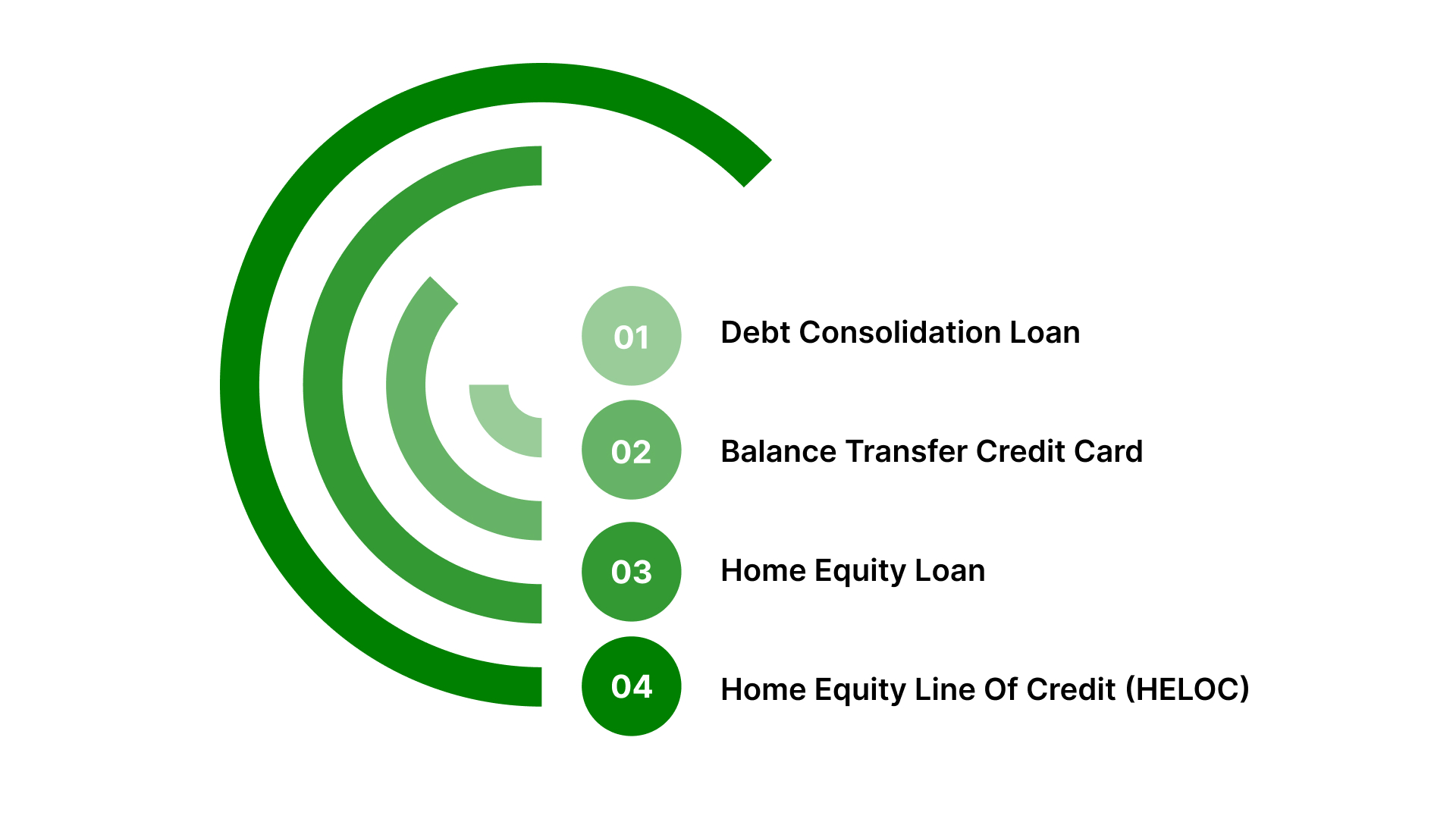

Common Ways Debt Consolidation Is Structured

Debt consolidation can take different forms depending on your financial profile and what you qualify for. Each option works slightly differently, especially in terms of access, risk, and repayment structure.

Here are the most common ways people consolidate debt:

- Debt consolidation loan (personal loan): This is one of the most widely used options. A personal loan is taken to pay off existing debts, leaving you with a single monthly payment.

- Typically offers lower interest rates than credit cards

- Comes with fixed repayment terms, usually between one to seven years

- Works best for individuals with stable income and fair to good credit

- Balance transfer credit card: This involves moving existing credit card balances to a new card with a low or 0% introductory interest rate.

- Introductory APR periods can last up to 21 months

- Helps reduce interest temporarily while paying down principal

- Requires discipline, as high interest rates may apply after the promotional period ends

- Home equity loan: Available to homeowners, this option allows you to borrow against the equity in your property.

- Usually comes with lower, fixed interest rates

- Offers structured repayment terms

- Carries a significant risk, as your home is used as collateral

- Home equity line of credit (HELOC): Similar to a home equity loan, but works more like a revolving credit line.

- You can borrow as needed up to a set limit

- Interest is charged only on the amount used

- Payment flexibility is higher, but so is the risk if repayments are not maintained

Each of these options depends on approval, financial standing, and access to credit. That’s why they are typically considered earlier, before accounts become significantly past due.

Where this applies:

- When accounts are already past due

- When a creditor or collections agency has reached out

- When managing the original debt directly is the priority

Also read: Debt Resolution Programs: How They Work and What to Expect

What is Debt Consolidation?

Debt consolidation is the process of combining one or more existing debts into a new loan or credit card, ideally with a lower interest rate.

Instead of negotiating with creditors to reduce the amount owed, consolidation rolls multiple balances into one new payment and one new lender. It is generally better suited to people who have good or excellent credit and are still in a position to qualify for new credit.

How debt consolidation typically works:

- Multiple debts (credit cards, loans) are combined

- A new loan is used to pay off those balances

- You make one monthly payment instead of several

- The new loan may come with different interest terms

- Approval often depends on your credit profile

Where this applies:

- When you are still managing active accounts

- When you qualify for a new loan or credit line

- When the goal is to simplify payments, not resolve past-due balances

Here's a table to quickly follow through:

It’s important to note that consolidation may not be available or effective once accounts are already in collections. In those cases, focusing on resolving the existing account becomes the more practical next step.

Pros and Cons of Debt Consolidation and Debt Resolution

Both options can be useful in the right situation, but they solve different problems. Looking at the advantages and limitations side by side can help you avoid choosing a path that doesn’t fit where you currently stand.

Debt Consolidation Pros and Cons

Debt consolidation is often seen as a way to organize finances, but it comes with conditions and trade-offs that are important to consider.

Debt Resolution Pros and Cons

Debt resolution focuses on addressing existing obligations, especially when accounts are already past due. It offers a more direct path to closure, but it also requires active participation.

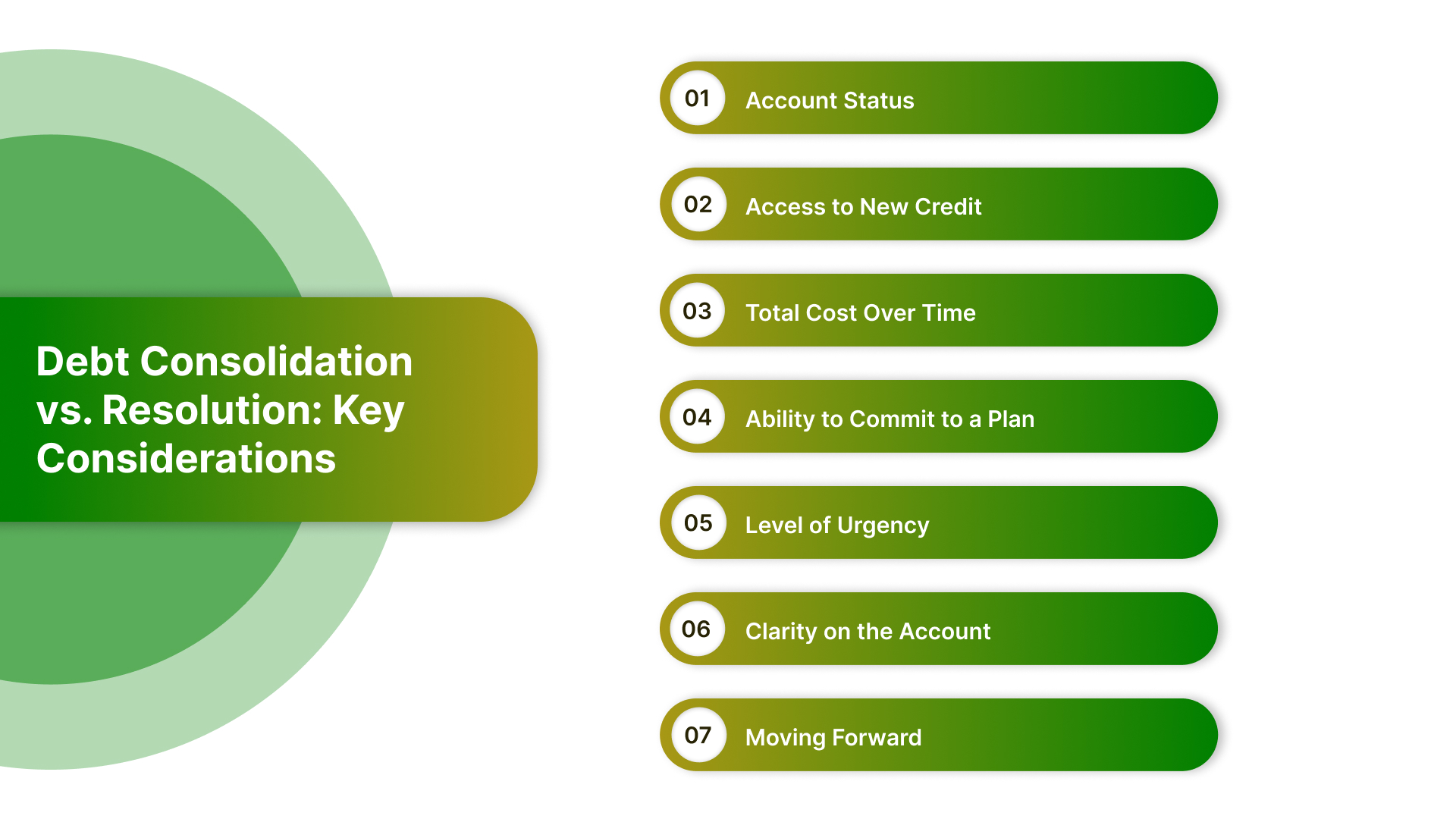

What to Consider Before Choosing Between Debt Consolidation and Debt Resolution

Choosing between these two is less about preference and more about where your debt stands right now. Many people look at both options side by side without realising that only one may actually apply to their situation.

Before moving forward, it’s worth stepping back and assessing a few key factors that directly affect what’s possible and what makes sense:

Where Your Accounts Currently Stand

This is the first and most important filter.

- If your accounts are still active and payments are up to date, consolidation may still be an option

- If payments have been missed and the account is already past due or in collections, resolution becomes more relevant

The stage of your debt determines not just the option, but the outcome you can realistically expect. Trying to apply the wrong solution at the wrong stage often leads to delays or rejection.

Your Access to New Credit

Debt consolidation depends heavily on whether you can qualify for a new loan or credit line.

- Lenders look at your credit score, income stability, and existing obligations

- If your credit profile has already been affected by missed payments, approval may be limited

- Even when approved, the terms may not always be favourable

If access to credit is restricted, options that rely on new borrowing may not be practical.

The Total Cost Over Time

Not all solutions reduce what you pay. Some simply restructure it.

- Consolidation can lower monthly payments but extend the repayment period

- Lower monthly payments may mean paying more interest over time

- Resolution focuses on closing the account, but timelines and amounts depend on the repayment approach

Also read: Debt Mediation and Repayment Strategies: A Clear Guide

Looking only at the monthly payment without considering the full cost can be misleading.

Your Ability to Commit to a Plan

Both options require consistency, just in different ways.

- Consolidation requires steady monthly repayments over a fixed term

- Resolution requires active follow-through, including reviewing the account and sticking to agreed payments

If the repayment plan doesn’t match your current financial capacity, it becomes difficult to sustain.

The Level of Urgency in Your Situation

Timing plays a bigger role than most people expect.

- If an account has been outstanding for a while, delaying action can make things more complex

- Addressing the account early can open up more structured and manageable options

- Waiting too long may limit flexibility and increase pressure

Taking a clear, informed step early often leads to better outcomes than postponing the decision.

Clarity on the Account Itself

Before choosing any path, you should fully understand the account in question.

- Confirm the original creditor and the amount owed

- Review any communication you’ve received

- Make sure the information is accurate before taking action

This step is often overlooked, but it sets the foundation for everything that follows.

What Moving Forward Actually Looks Like?

Finally, consider what each option leads to.

- Consolidation leads to a new repayment structure that replaces your existing debts

- Resolution leads to closing a specific outstanding account through a defined process

One reorganizes your finances. The other brings a situation to a close.

The right choice becomes clearer once you look at your situation objectively. Instead of trying to fit into a solution, focus on what applies to where you are right now and what helps you move forward with the least friction.

Conclusion

Sorting through debt options can feel more complicated than it needs to be, especially when different terms seem to point to the same solution. The real difference comes from understanding what applies to your situation and what actually moves things forward.

If your account is being handled by The Forest Hill Management, you have access to clear information, structured repayment options, and a secure way to take action at your own pace. The goal is not to add pressure, but to give you a straightforward path to resolve what’s outstanding.

Take the first step toward financial freedom.

FAQs

1. Can I switch from debt consolidation to debt resolution later if needed?

Yes, but it depends on how your situation changes. If accounts become past due or you’re unable to maintain consolidation payments, resolution may become the more practical next step.

2. Does choosing one option lock me out of other financial options in the future?

Not necessarily. However, each choice can affect your financial profile differently, which may influence what options are available to you later on.

3. How do I know if a solution is realistic for my situation?

The most reliable way is to look at your current account status, your ability to qualify for credit, and whether you can sustain the repayment structure over time.

4. Is it better to act immediately or take time to compare options?

A short review is helpful, but delaying action for too long can reduce flexibility, especially if the account is already past due or progressing through collections.

5. What should I do if I’m unsure which option applies to me?

Start by reviewing your account details and confirming where it stands. Once you have clarity on that, the appropriate path usually becomes much easier to identify.