How to Get Ahead Financially: Tips for U.S. Borrowers

Transform Your Financial Future

Contact UsManaging money can feel overwhelming when rising living costs and existing debt start competing for the same paycheck. In fact, recent surveys show that 69% of young adults say building financial stability today feels harder than it did for previous generations, largely because of higher living expenses and growing debt obligations. If you’re dealing with unpaid bills, credit card balances, or financial pressure that seems difficult to manage, it’s easy to feel stuck.

The good news is that financial progress rarely requires drastic changes overnight. With the right information and a few practical steps, you can begin improving your situation and regain a sense of control over your finances.

In this blog, we’ll walk through practical ways to get ahead financially in 2026. You’ll learn how to organize your finances, reduce financial pressure from debt, and build habits that help you move toward greater financial stability.

Key Takeaways

- Financial progress often feels difficult when debt, interest charges, and everyday expenses compete for the same income, but understanding these pressures is the first step toward regaining control.

- Getting ahead financially does not mean eliminating all debt overnight. It usually begins with clarity about your accounts, consistent repayment habits, and better organization of your finances.

- Small financial habits can make a meaningful difference over time, such as reviewing your spending regularly, reducing unnecessary expenses, and avoiding reliance on minimum payments alone.

- Preparing for financial setbacks helps protect your progress. Building a modest emergency fund and planning for irregular expenses can prevent new debt during unexpected situations.

- Clear communication and organized financial records can make resolving debt easier, helping you understand your options and move toward a more stable financial future.

Why Debt Can Make Financial Progress Feel Difficult?

When you are trying to move forward financially while managing debt, progress can feel slower than expected. Even when you are making payments regularly, balances may not seem to decrease as quickly as you hoped. This can create the sense that you are working hard financially but not actually getting ahead.

Several factors explain why debt can make financial progress feel difficult:

Interest Charges Slow Down Balance Reduction

Many types of consumer debt include interest charges that continue accumulating over time. Financial cards, personal loans, and other forms of borrowing often carry interest rates that increase the total amount you must repay.

If a payment is missed or delayed, additional fees may be added to the account, which can make repayment take longer.

Multiple Financial Responsibilities Compete for Your Income

Rent, groceries, and transportation are unavoidable costs, which means the money available for debt payments may be limited each month. Medical bills, car repairs, or changes in employment can quickly affect your ability to keep up with payments.

Without emergency savings, even small financial surprises can push debt further out of reach.

Financial Stress Affects Decision-Making

Surveys consistently show that money remains one of the leading causes of stress in the United States, with nearly half of adults reporting that financial concerns affect their overall well-being.

Financial stress can make reviewing accounts or discussing repayment feel overwhelming, leading many people to delay financial decisions. When immediate pressures take priority, long-term goals can feel distant, even though steady steps can still move you forward.

Credit Score Impact Can Limit Financial Options

When debt remains unpaid or accounts fall behind, it can affect your credit profile. A lower credit score may make it harder to qualify for lower interest rates, refinancing options, or new lines of credit that could otherwise help manage existing balances.

This can create a cycle where fewer financial options are available, making it more difficult to restructure or simplify outstanding obligations.

Uncertainty About Account Details Creates Delays

When someone is dealing with multiple accounts or older balances, it is not always clear how much is owed, who currently manages the account, or what repayment options are available. That uncertainty can make it difficult to decide what step to take next.

Without clear information about balances, payment history, or available repayment arrangements, people may postpone taking action simply because the situation feels unclear.

What Does Getting Ahead Financially Really Mean?

When you are dealing with debt, getting ahead financially does not mean eliminating every balance overnight. For most people, it means creating stability first. That starts with understanding your financial obligations, keeping payments organized, and making steady progress toward reducing what you owe.

Financial well-being is often measured less by wealth and more by financial control. Managing this debt usually involves several practical shifts:

Understanding Your Financial Starting Point

Progress becomes possible only when you have a clear picture of your financial situation. This includes knowing how much you owe, which accounts require attention, and what your monthly income realistically supports.

- Reviewing outstanding balances and payment obligations: Knowing the total amount owed and the accounts involved helps remove uncertainty and allows you to prioritize repayment decisions.

- Tracking monthly income and essential expenses: Financial planners often recommend starting with a simple cash-flow review to understand how much income remains available after covering essential living costs.

- Identifying where financial pressure is coming from: Understanding which obligations are creating the most strain can help you focus your attention where it matters most.

Clarity at this stage is often the first step toward financial progress.

Building Consistent Progress Rather Than Quick Fixes

Many people believe they need large payments or sudden financial changes to move forward. In practice, consistent small improvements often produce stronger long-term results.

- Regular payments gradually reduce balances: Even modest payments made consistently can lower balances over time and improve financial stability.

- Avoiding new financial strain while resolving existing obligations: Maintaining steady progress without creating additional debt is often more sustainable than trying to resolve everything immediately.

- Creating predictable financial routines: Scheduled payments and organized account management reduce uncertainty and help maintain progress.

Financial stability is typically built through consistency rather than sudden changes.

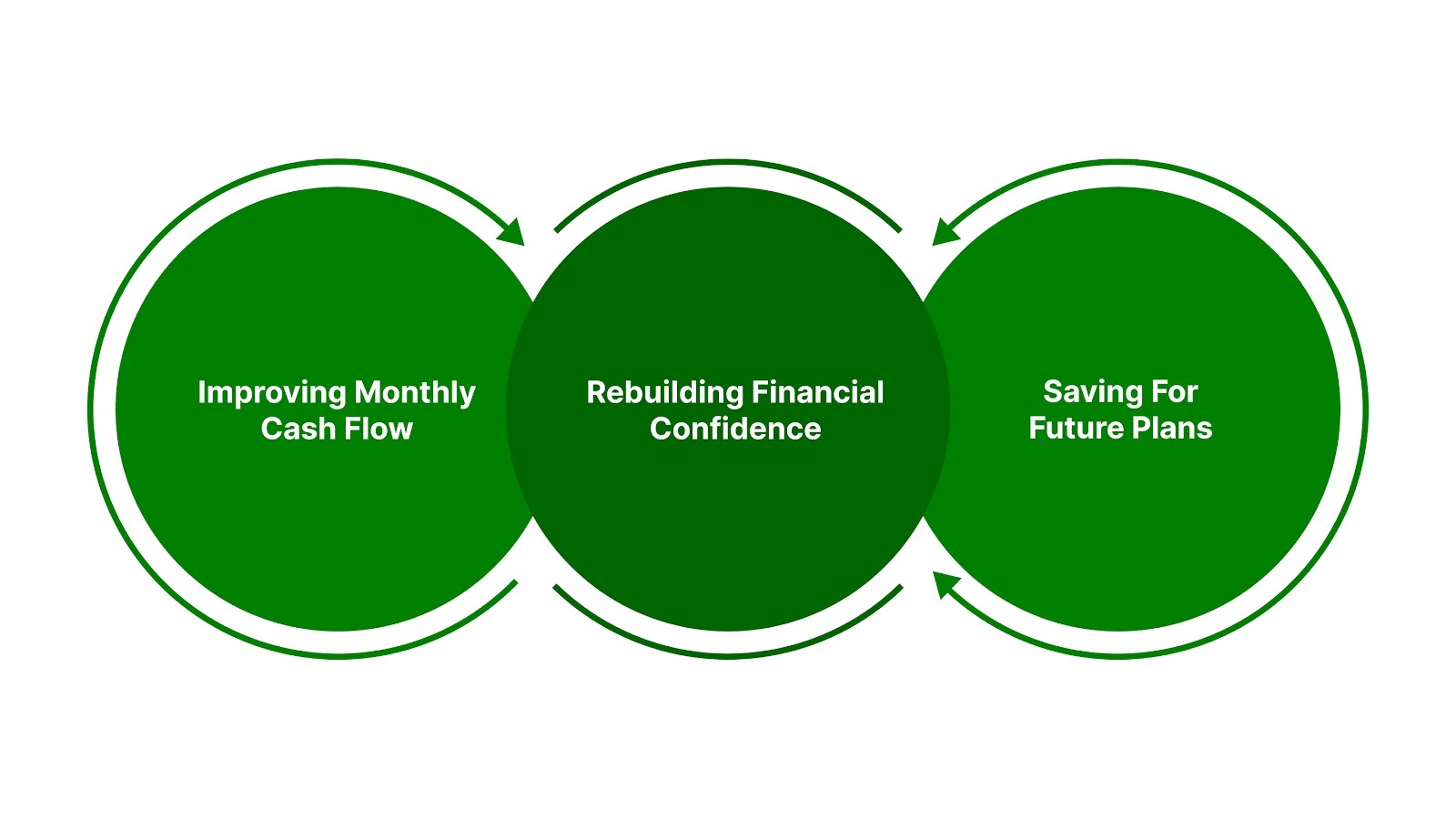

Restoring Financial Flexibility Over Time

Another important part of getting ahead financially is regaining flexibility in your monthly finances. When debt payments decrease or become more manageable, people often regain the ability to plan for the future.

- Improving monthly cash flow: As balances are reduced or repayment plans become clearer, more income becomes available for other priorities.

- Rebuilding financial confidence: Seeing steady progress can reduce financial stress and encourage better long-term financial habits.

- Creating space for savings and future goals: Once immediate financial pressure decreases, it becomes easier to begin building emergency savings or planning ahead.

Financial progress does not always happen quickly, but steady improvements often lead to greater stability over time.

The Role of Clear Account Communication

For individuals managing past-due accounts, getting ahead financially also depends on having accurate information about their obligations. When account details are unclear, it can be difficult to decide what step to take next.

Structured account management helps by providing:

- Clear records of balances and payment activity

- Accurate documentation of account ownership and details

- Secure communication channels for discussing repayment options

- Transparent pathways toward resolving outstanding balances

When financial information is organized and easy to review, people can make more confident decisions about how to move forward.

Suggested Read: Essential Personal Finance Tips for Beginners

Getting ahead financially does not require perfect circumstances. It begins with clarity, consistent steps, and access to accurate information about your accounts. For individuals managing outstanding balances, these elements can turn financial uncertainty into a practical path toward stability.

If you're tired of feeling overwhelmed by debt, The Forest Hill Management specializes in creating personalized repayment plans that align with your unique financial situation. Our team will work with you to build a strategy that not only helps you stay on track but also fosters long-term financial stability.

10 Actionable Tips to Get Ahead Financially in 2026

Financial progress rarely happens overnight, especially if you are already managing debt or overdue balances. Getting ahead financially usually means building better financial habits, reducing pressure from existing obligations, and creating small but consistent improvements in your financial stability.

Here are 10 practical steps that can help you move forward one step at a time:

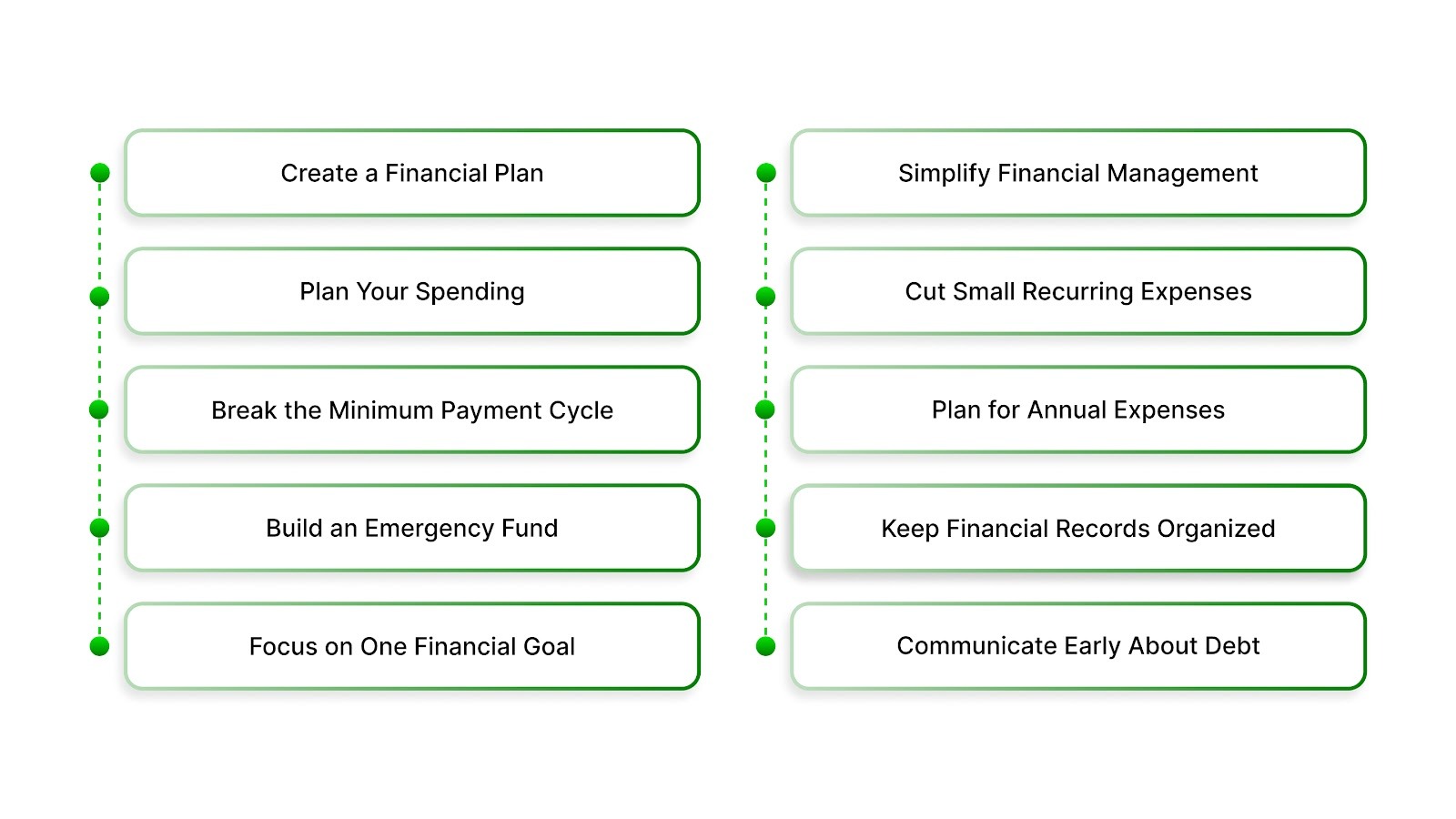

1. Start With a Clear Financial Plan

Many people underestimate how much clarity alone can improve financial decisions. When you see all your financial obligations in one place, it becomes easier to prioritize what needs attention first.

- Create a simple list of every account you owe: Include the creditor name, balance, monthly payment, and interest rate if available. Seeing this information in one place removes uncertainty and helps you understand the true scale of your obligations.

- Review the last 90 days of spending activity: Bank and card statements often reveal patterns that daily spending hides, such as recurring subscriptions, frequent small purchases, or categories where costs quietly increase.

- Identify the difference between income and required expenses: Calculating what remains after housing, utilities, groceries, and transportation helps determine how much money can realistically go toward improving your financial situation.

Clarity is often the first step toward financial stability because it replaces uncertainty with information you can act on.

2. Shift From Reactive Spending to Planned Spending

Financial pressure often grows when spending decisions happen without a plan. Moving toward planned spending can immediately reduce financial stress.

- Decide how much money each category should receive before the month begins: Allocating funds to housing, food, transport, and other categories first helps ensure essential expenses are always covered.

- Set flexible limits for discretionary categories: Instead of eliminating spending on dining, entertainment, or hobbies, set realistic limits that allow you to maintain balance without overspending.

- Review spending weekly rather than monthly: Checking in once a week helps catch overspending early before it affects your entire monthly budget.

Planning spending ahead of time helps prevent financial surprises.

3. Break the Minimum Payment Cycle

One of the biggest barriers to financial progress is relying only on minimum payments for revolving debt.

- Understand how minimum payments are calculated: Many minimum payments cover mostly interest, meaning only a small portion actually reduces the balance.

- Add even small additional amounts to payments when possible: Increasing a payment by $25 or $50 can significantly reduce the time required to repay certain balances.

- Apply extra payments consistently to the same account: Concentrating additional payments on one balance at a time helps create visible progress and momentum.

Breaking the minimum payment cycle can dramatically shorten the time it takes to regain financial control.

4. Protect Yourself From Financial Setbacks

Unexpected expenses are one of the most common reasons people fall deeper into debt. When there is no financial cushion, even a small emergency can force you to rely on credit cards or loans, which can increase balances and interest costs.

- Start building a small emergency reserve: Begin by setting aside a modest amount of money specifically for unexpected expenses. Even saving a few hundred dollars can help cover sudden costs like car repairs, medical bills, or urgent home fixes without relying on new borrowing.

- Save gradually rather than waiting for large deposits: Instead of waiting until you have extra money available, build the habit of saving small amounts regularly. Setting aside a small portion from each paycheck or saving a fixed amount each week can slowly grow a reliable financial cushion.

- Use emergency funds only for genuine disruptions: An emergency fund should be reserved for unexpected situations that affect your financial stability, such as job interruptions or urgent repairs. Avoid using it for routine spending so that the money remains available when you truly need it.

A financial buffer helps protect the progress you are making toward financial stability.

5. Focus on One Financial Improvement at a Time

Trying to solve every financial challenge at once can quickly become overwhelming. A more effective approach is to focus on one meaningful improvement at a time and build momentum from there.

- Choose one priority goal for the next few months: Identify a single financial objective that would make the biggest difference in your situation, such as reducing a specific balance, catching up on payments, or building a small emergency savings fund.

- Direct your available financial energy toward that goal: Concentrating your efforts allows you to make measurable progress rather than spreading your resources across too many priorities at once.

- Move to the next goal only after the first becomes manageable: Once your initial goal is under control, shift your focus to the next financial improvement. This step-by-step approach creates steady progress rather than scattered efforts that feel unproductive.

Focused progress often leads to better results than trying to fix everything simultaneously.

6. Reduce Financial Friction in Your Daily Life

Financial mistakes such as missed payments or forgotten bills often happen because managing multiple accounts becomes complicated. Simplifying your financial routines can make managing money much easier.

- Set up automatic payments for minimum balances: Automating essential payments helps ensure your accounts remain current even if life becomes busy or stressful. This can help you avoid late fees and protect your payment history.

- Use calendar reminders for important financial dates: Setting reminders for bill due dates, budget reviews, or financial check-ins can help you stay organized and avoid last-minute stress.

- Centralize financial information in one location: Keeping account numbers, balances, and payment schedules together in a secure place makes it easier to review your finances and stay aware of your obligations.

Reducing friction in your financial routines makes it easier to stay consistent.

Also Read: How to Effectively Manage and Reduce Debt

7. Watch for Small Expenses That Add Up

Many households focus on large financial obligations but overlook smaller recurring expenses that gradually consume a significant portion of income.

- Review subscription services and app charges regularly: Digital subscriptions, streaming services, and mobile apps often renew automatically. Reviewing these charges periodically helps you cancel services you no longer use.

- Check utility and service providers periodically: Costs for services such as internet, insurance, and phone plans can increase over time. Comparing providers occasionally may reveal opportunities to reduce monthly expenses.

- Redirect those savings intentionally: When you reduce or eliminate a recurring expense, consider applying the saved amount toward paying down balances or strengthening your emergency fund.

Small adjustments in spending can create meaningful financial flexibility over time.

8. Prepare for Expenses That Happen Every Year

Some financial pressures arise simply because predictable expenses were not planned for in advance. Preparing ahead can make these costs easier to manage.

- Identify expenses that occur annually or seasonally: Holiday spending, school supplies, travel costs, and insurance renewals are common examples of expenses that occur at predictable times each year.

- Spread these costs across the entire year: Setting aside a small amount each month allows you to prepare for larger expenses without placing sudden pressure on your budget.

- Treat these savings like a regular bill: Consistently contributing to a dedicated savings category ensures the money will be available when the expense arrives.

Planning ahead helps reduce financial surprises and improves stability.

9. Keep Your Financial Information Organized

When you are managing several accounts, staying organized can make a significant difference in how easily you can review and manage your finances.

- Maintain records of payments and account statements: Keeping copies of statements and payment confirmations helps you track your progress and verify that payments are properly recorded.

- Save written communication related to your accounts: Emails, letters, and agreements can clarify payment terms, balances, or repayment arrangements if questions arise later.

- Store financial information securely and accessibly: Using a secure digital folder or organized physical records allows you to quickly locate important information when reviewing your finances.

Clear financial records help prevent misunderstandings and support better financial decisions.

10. Communicate Early When Dealing With Debt

Avoiding conversations about debt can often increase stress and uncertainty. Addressing the situation early can help you better understand your options and move toward resolution.

- Review your account details before discussing repayment: Taking time to understand the balance, payment history, and account status helps you approach discussions with clearer expectations.

- Ask about structured repayment options if you are struggling: In some cases, repayment arrangements can make resolving balances more manageable by spreading payments over time.

- Keep documentation of agreements and payments: Written records provide clarity about repayment terms and help you track your progress as balances are resolved.

Open communication can help transform financial uncertainty into a clearer path forward.

Suggested Read: Is Paying Debt Collection Agencies a Bad Idea?

Taking steps to understand and address outstanding balances can bring greater clarity and confidence to your financial situation.

Take the first step toward financial stability. Contact The Forest Hill Management to review your options and start moving forward.

Conclusion

2026 is your year to break free from financial stress. By taking action today, you can turn the challenges of debt, poor credit, and unpredictable expenses into manageable steps toward a more secure future.

To recap, setting clear goals, tackling debt, automating savings, and staying on top of your credit are essential moves to regain control over your finances. The path to financial freedom is built on small, steady actions, but those actions add up.

Contact our financial advisors at The Forest Hill Management today to get a personalized plan that’s as unique as your financial journey!

FAQs

1. How long does it usually take to improve your financial situation when dealing with debt?

The timeline varies depending on the size of the debt, your income, and the repayment strategy you follow. Many people begin seeing progress within a few months when they consistently track spending, make structured payments, and avoid adding new balances.

2. Should you stop saving while paying off debt?

In many cases, maintaining at least a small emergency savings fund is helpful while paying down debt. Having a financial buffer can prevent unexpected expenses from forcing you to rely on additional borrowing.

3. What is the best way to stay motivated during a long debt repayment process?

Breaking large financial goals into smaller milestones can help maintain motivation. Tracking progress, celebrating small wins, and regularly reviewing improvements in balances or spending habits can make the process feel more achievable.

4. Can improving financial organization really make a difference?

Yes. Simply organizing account information, payment records, and monthly expenses often reduces financial confusion and stress. When your financial information is clear and accessible, it becomes easier to make informed decisions about repayment and budgeting.

5. When should someone seek help managing past-due accounts?

If payments are becoming difficult to manage or balances feel overwhelming, reaching out early can help clarify your options. Understanding the status of your accounts and discussing possible repayment arrangements can make resolving outstanding balances more manageable.