Credit Clearing Explained: Meaning, Benefits, and Real Examples

Transform Your Financial Future

Contact UsCredit clearing helps explain how financial obligations balance out, making it easier to understand what you actually owe and what remains to be paid. It might sound complex, but the concept is simple; it’s about offsetting what is owed and what is due, so only the remaining balance needs payment.

If you manage several bills, owe money to multiple lenders, or handle transactions regularly, understanding credit clearing gives you clarity and control.

It explains how financial systems reduce risk and how similar ideas can guide you in managing your own debts.

Now that you have a broad idea, let’s look at what credit clearing really means and why it matters for both financial institutions and everyday individuals like you.

Key Takeaways

- Credit clearing simplifies complexity. It helps you see the true balance between what you owe and what you’re owed, cutting through confusion.

- It’s more than a banking term. The same principles that make banks efficient can help you manage personal debt with structure and confidence.

- A smart organization brings freedom. When you track and balance your obligations, you gain control, reduce stress, and plan repayment efficiently.

- Support accelerates progress. Professional guidance, like Forest Hill Management’s personalized plans, turns financial pressure into a clear path toward stability.

What Is Credit Clearing?

Credit clearing is the process of balancing or offsetting mutual financial obligations between parties. In simple terms, it allows several transactions to be combined so that only the net difference is paid.

Instead of settling each transaction individually, participants agree to clear multiple debts or credits at once, saving time, effort, and cash movement.

This practice first appeared among banks in London during the eighteenth century when institutions exchanged payment instructions daily. Rather than transfer large sums each time, they compared what each owed and paid only the net amount.

Over time, this became a foundation of modern financial clearing systems that reduce liquidity risks and increase efficiency.

Here’s how it works in principle:

- Two or more parties owe money to each other.

- Each obligation is recorded as a debit or credit.

- The amounts are matched and offset.

- Only the remaining balance is transferred or settled.

You can think of it as the financial equivalent of balancing tabs among friends after a shared dinner. If everyone has paid or received different amounts, credit clearing ensures that only what remains unsettled is exchanged.

While credit clearing originated in banking, the same logic applies to personal finance. Understanding how obligations can offset each other helps you manage debt, make smarter financial choices, and view your credit situation more strategically.

Now that you understand the concept, the next section explains how credit clearing actually works in practice and why it plays a key role in both personal and institutional finance.

Also Read: How To Pay Debt in Credit Collection Service

How Credit Clearing Works (Simple Mechanism Explanation)

Understanding how credit clearing works helps you see how money moves efficiently in financial systems and personal situations. The concept sounds technical, but once broken down, it becomes simple and logical.

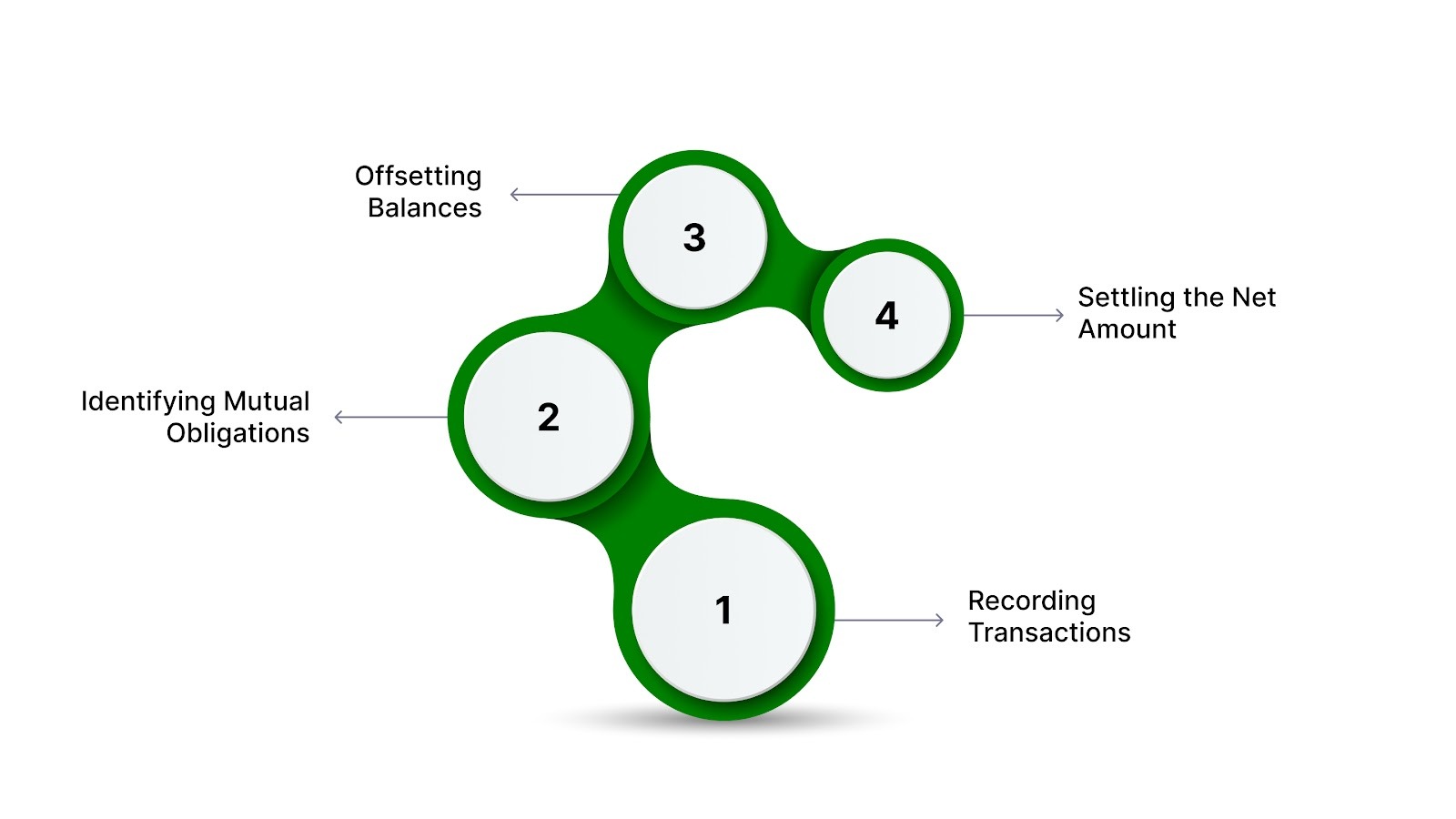

Step-by-Step Overview

1. Recording Transactions

Every transaction between parties is recorded as either a debit (amount owed) or a credit (amount received).

2. Identifying Mutual Obligations

When two or more parties owe each other money, their obligations are compared.

3. Offsetting Balances

The amounts are matched and subtracted from each other. This process leaves a single remaining balance, known as the net obligation.

4. Settling the Net Amount

Only the difference is paid or transferred. This reduces unnecessary transactions and keeps the flow of funds smoother.

Simple Everyday Example

Imagine three people, Alex, Jamie, and Taylor, buy groceries weekly:

Instead of each person paying and collecting separately, the group offsets the debts. After clearing, only the net differences remain. The result is fewer payments, less confusion, and no duplicate transfers.

Why It Matters

In everyday life, this same idea reduces confusion, cuts down on repeated payments, and makes balances easier to manage. For you, the same principle applies when you manage bills, loans, or shared expenses. You simplify repayment and understand exactly what remains outstanding.

Credit clearing highlights how understanding net obligations instead of focusing on every individual payment can improve both efficiency and confidence in managing money.

Credit Clearing vs. Related Terms (Clarifying Confusion)

The phrase credit clearing often gets mixed up with other financial terms. While they sound similar, each serves a different purpose. Knowing the difference helps you make informed financial decisions and use the right strategies for your needs.

1. Credit Clearing vs. Credit Repair

Credit clearing helps with financial flow, while credit repair helps with financial reputation. Both support financial health, but in different ways.

2. Credit Clearing vs. Debt Settlement

Debt settlement can affect your credit depending on how it’s handled, while credit clearing focuses on organizing obligations rather than changing balances.

3. Credit Clearing vs. Credit Counseling

Credit counseling involves working with professionals who guide you on budgeting, repayment planning, and responsible credit use. Credit clearing, however, focuses on balancing financial obligations already recorded.

Key takeaway:

- Credit clearing deals with financial flow and offsetting.

- Credit counseling focuses on financial behavior and education.

4. Why These Distinctions Matter to You

When you understand how these terms differ, you avoid confusion and make better financial choices.

- If your goal is to simplify multiple payments, credit clearing principles help.

- If you want to improve your credit score, credit repair or counseling is more suitable.

- If you are negotiating with lenders, debt settlement strategies might be relevant.

Each tool has its place, and understanding them helps you stay in control of your credit journey.

Also Read: Understanding Debit vs Credit in Accounting

Why Understanding Credit Clearing Matters to You

When you understand how credit clearing works, you see money and obligations in a new way. It helps you manage your finances with greater confidence and reduces unnecessary stress.

1. Brings Clarity to Your Financial Picture

Credit clearing gives you a clear view of what you truly owe.

Instead of focusing on every single transaction, you see your net position. This clarity helps you plan payments better and prevents confusion when dealing with multiple bills or lenders.

2. Helps You Make Smarter Repayment Choices

By thinking in terms of net obligations, you can prioritize payments that make the most impact.

For example:

- You may choose to pay one combined amount instead of many smaller ones.

- You can discuss structured repayment plans that reflect your actual balances.

This approach keeps you organized and prevents duplicate or unnecessary payments.

3. Builds Awareness of Financial Efficiency

Credit clearing shows how efficiency reduces both cost and effort.

In personal finance, it encourages you to:

- Track who owes whom.

- Record payments accurately.

- Use technology to simplify your records.

You gain control, not just over numbers, but over your financial peace of mind.

4. Strengthens Your Financial Understanding

You start viewing your credit health like a professional. The same principles banks use to manage liquidity can guide you to manage personal debt.

This knowledge builds confidence when you interact with creditors, financial advisors, or repayment services.

Understanding credit clearing helps you make informed choices that bring stability and control. Now that you see why it matters, let’s look at how it appears in everyday life.

Also Read: What is Credit Management? A Complete Guide

Real-World Examples of Credit Clearing

Examples make complex ideas simple. While these examples vary in scale, the same principles apply when you’re managing personal debts, bills, or repayment plans. Here are some real-life situations where credit clearing principles apply at different levels, from daily life to large-scale finance.

1. Everyday Example: Friends Sharing Expenses

You and your friends often share costs for meals, trips, or activities. Instead of sending multiple payments back and forth, you track who owes what.

At the end, you calculate who should pay whom. Only the remaining balances are settled.

This small act is a form of credit clearing; everyone’s obligations are balanced, and fewer payments are made.

2. Small Business Example: Supplier and Retailer

A local retailer supplies goods to a café. At the same time, the café sells gift vouchers that the retailer accepts.

Instead of paying each invoice separately, both agree to offset the amounts.

This arrangement keeps both parties liquid and reduces transaction costs.

3. Business Network Example: Community Credit Systems

Some small business networks use mutual credit systems. Each member records what they sell and what they buy.

Balances are updated automatically, and only net differences are settled later. This builds community trust and encourages trade even when cash flow is tight.

4. Institutional Example: Interbank Clearing

In the banking world, financial institutions use credit clearing houses to offset thousands of daily transactions.

Banks calculate what they owe each other and settle only the remaining balance at the end of each day. This process keeps the financial system stable and liquid.

5. Personal Finance Example: Managing Multiple Debts

If you have several credit accounts or personal loans, you can use the idea of credit clearing mentally to track your total obligations.

You can create a single list of what you owe and to whom, then see your total net liability. This practice helps you stay organized and informed before setting up repayment plans.

Limitations and When It Does Not Apply

Credit clearing can simplify financial management, but it is not a universal solution for every credit issue. Understanding its boundaries helps you apply it wisely.

1. Does Not Erase Existing Debts

Credit clearing offsets obligations but does not eliminate them. If you owe money, the obligation remains until you settle it. It helps you manage balances effectively but does not replace repayment.

Tip: Use clearing as a planning tool, not a substitute for action.

2. Does Not Fix Credit Report Issues

Credit clearing does not directly improve or change your credit score. Credit bureaus record payment histories, and clearing only affects how debts are balanced, not how they appear on your report.

If your credit file contains inaccurate entries, credit repair or professional assistance is the right step.

3. Limited Use in One-Way Obligations

Clearing requires mutual obligations; both parties owe or receive something. If you owe money to a lender but they owe nothing back, clearing does not apply.

In that case, you focus on structured repayment instead.

4. Requires Accurate Recordkeeping

The process works best when all obligations are tracked correctly. Missing or incorrect data can lead to confusion instead of clarity.

Maintaining up-to-date records ensures that clearing helps rather than complicates your finances.

5. May Not Reflect Emotional or Behavioral Factors

Credit clearing deals with numbers, not emotions. However, financial stress often includes emotional elements. You may need both logical strategies and emotional support to regain control.

Professionals such as financial advisors or credit counselors can help you handle both sides effectively.

When to Seek Professional Guidance

If you find your credit situation complex or overwhelming, you can seek support from an experienced financial advisory service. A trusted professional helps you understand your obligations, plan realistic repayment strategies, and stay motivated through the process.

You gain structure, clarity, and a plan that matches your financial reality.

Now that you know its benefits and limits, let’s explore how to strengthen your credit health using proven, practical steps actively.

Also Read: Credit Portfolio Management: Ultimate Guide and Strategies

How to Improve Your Credit Health (Actionable Tips)

Credit clearing gives you perspective, but improving credit health requires consistent action. The goal is not perfection; it’s progress through awareness, structure, and discipline.

Below are practical steps you can follow to strengthen your credit health and stay in control of your finances.

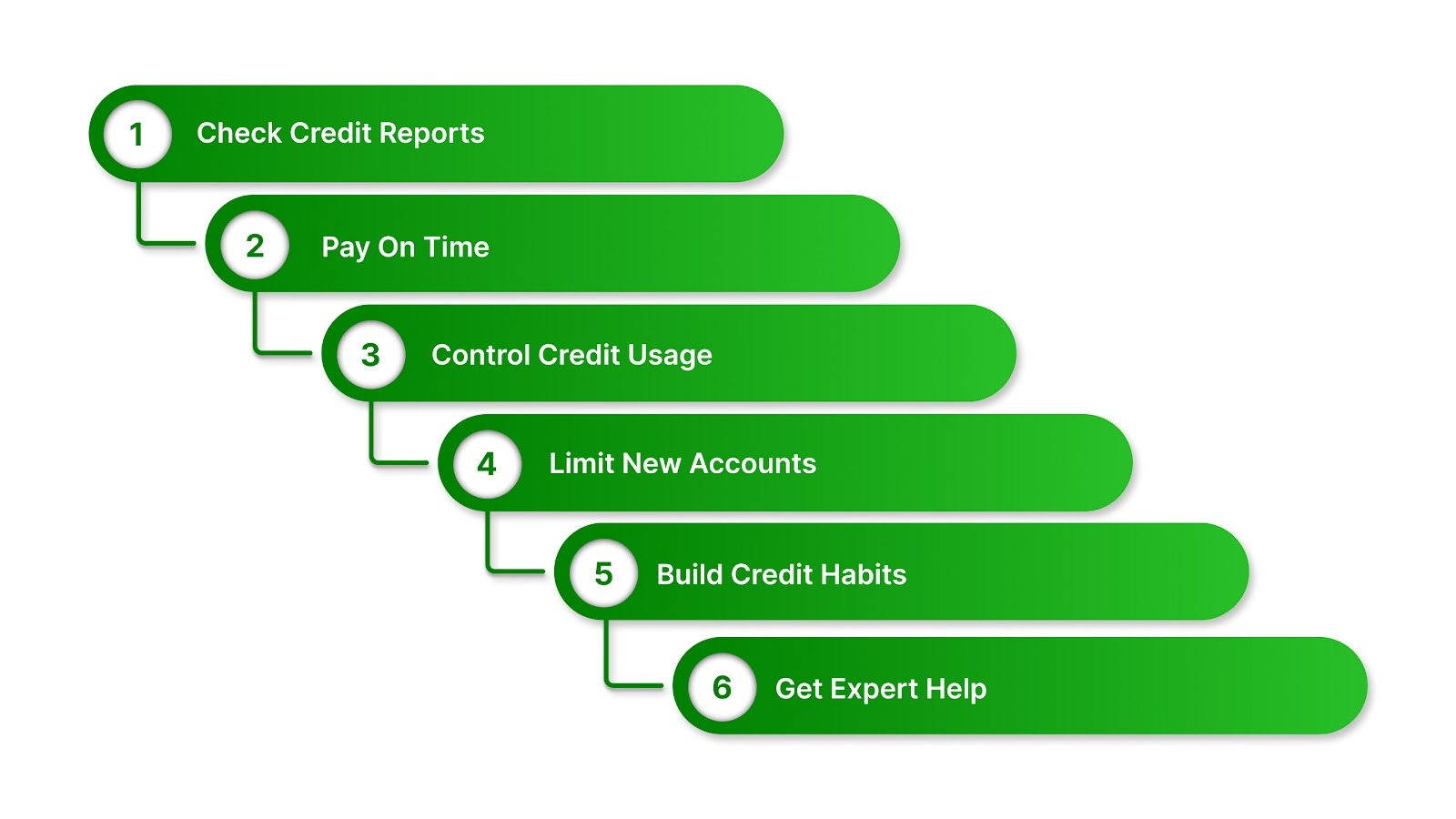

1. Review Your Credit Reports Regularly

Start by checking your credit reports from all three major credit bureaus:

- Equifax

- Experian

- TransUnion

You are entitled to one free report from each bureau every year through AnnualCreditReport.com.

Review these reports for:

- Incorrect balances

- Duplicate accounts

- Outdated or incomplete information

If you find errors, dispute them directly through the credit bureau’s online platform. Accurate data is the foundation of healthy credit.

2. Pay Consistently and On Time

Payment history is one of the biggest factors in your credit score. You can improve it by:

- Setting reminders or automatic payments.

- Paying at least the minimum balance on each due date.

- Avoiding missed or late payments.

Consistency proves reliability. Even small on-time payments help rebuild trust with creditors.

3. Manage Credit Utilization

Credit utilization measures how much credit you use compared to your total available limit. Keep this ratio below 30% whenever possible.

For example, if your credit limit is $1,000, aim to keep your balance below $300. This shows lenders you use credit responsibly.

4. Avoid Opening Too Many New Accounts

Each credit inquiry can temporarily lower your score. Instead of applying for multiple accounts, focus on maintaining your existing ones in good standing. This demonstrates stability and consistent management.

5. Build Positive Credit Habits

Good credit health develops through steady habits. Consider these practices:

- Pay utility or phone bills on time.

- Keep older accounts open to maintain a credit history.

- Monitor your credit score monthly through free online tools.

Every positive action adds weight to your financial credibility.

6. Seek Guidance When Needed

If your debt or repayment situation feels complex, professional guidance can make the process smoother. Financial experts can help you:

- Discuss repayment options with creditors or account managers.

- Build structured repayment plans.

- Regain confidence in managing your obligations.

A professional perspective ensures that your plan fits your unique financial circumstances.

Credit health improves over time. Every correct step, however small, brings you closer to stability and freedom from financial stress.

Now, let’s see how The Forest Hill Management supports this journey with personalized solutions.

Also Read: The Ultimate Guide to Repair Your Credit Fast: 8 Sure Steps for a Stronger Score

The Forest Hill Management’s Role in Helping You Navigate Credit Challenges

Managing debt can feel overwhelming, but the right guidance turns confusion into clarity. The Forest Hill Management helps you regain financial control through professional advice and flexible repayment options that match your situation.

How Forest Hill Management Supports You

- Personalized Guidance: Advisors help you understand your obligations and build a clear, realistic repayment plan.

- Flexible Payment Options: Tailored schedules help you stay consistent without financial strain.

- Secure Online Platform: A safe, easy way to track payments and stay organized from anywhere.

- Stress-Free Support: A team that communicates clearly, offering reassurance and motivation as you move toward financial balance.

With expert support and easy-to-use tools, you can manage credit challenges with confidence and take steady steps toward long-term stability.

Conclusion

Credit clearing gives you a new perspective on how money and obligations work together. It helps you simplify debt management, plan smarter, and regain confidence in your financial decisions.

For banks, it ensures smooth transactions. For you, it means understanding your true financial position and taking control of your future.

If you’re ready to simplify your debt, manage repayments better, and move toward financial freedom, The Forest Hill Management is here to help.

Contact The Forest Hill Management today to get started on your path to financial control and peace of mind.

FAQs

1. What does credit clearing mean for my credit score?

Credit clearing does not directly change your credit score. It helps you understand and manage obligations better, which supports long-term credit health.

2. Is credit clearing the same as credit repair?

No. Credit clearing offsets financial obligations, while credit repair focuses on fixing credit report issues. Both can strengthen your financial position in different ways.

3. Can credit clearing help with multiple debts?

Yes. It helps you see your total balance clearly, avoid duplicate payments, and plan repayment more effectively.

4. Does credit clearing remove debt completely?

No. It simplifies the process but does not erase the debt. You still need to repay what you owe, but in a more structured way.

5. When should I seek professional help?

If your credit situation feels confusing or stressful, reach out for support. A professional advisor helps you create a realistic plan and stay on track.