7 Levels of Financial Freedom for People Managing Debt

Transform Your Financial Future

Contact UsFor many Americans, financial freedom feels out of reach because debt and rising living costs make it nearly impossible to get ahead. A 2025 PNC Bank report found that 67% of full-time U.S. workers live paycheck to paycheck, meaning two-thirds of earners have little to no buffer once their monthly expenses are paid.

But financial freedom is not just for the debt-free or the wealthy. Even if you are managing loans, credit card bills, or overdue payments, progress is still possible. Each step you take toward clarity, control, and consistency brings you closer to independence and peace of mind.

In this guide, we will break down the seven levels of financial freedom, showing how to climb from debt and uncertainty toward long-term stability and confidence.

Quick look:

- Debt can be a beginning, not an end. It often becomes the trigger for financial awareness and the first step toward regaining control.

- Financial freedom is a gradual process. Progress happens through defined levels, from basic clarity to full independence. Each level is built on consistency and planning.

- Knowing your freedom number provides direction. Using the Rule of 25 helps you estimate how much you need invested to live comfortably without relying on income.

- Strategic methods accelerate progress. Techniques such as hybrid repayment ladders, expense optimization, and micro-savings help build momentum toward stability and growth.

- Sustained progress requires structure. Automation, regular reviews, and steady habits transform debt management into a long-term system for financial resilience.

Debt as a Starting Point for Financial Freedom

“You must gain control over your money or the lack of it will forever control you.”

— Dave Ramsey

Debt can be the catalyst that forces a closer look at spending habits, savings discipline, and long-term goals. Instead of viewing it as a permanent setback, think of debt as the first step toward financial awareness and control.

This is how debt has already brought you to the starting line:

- Debt can teach discipline. It encourages you to budget, prioritize payments, and become more intentional about money.

- It reveals financial blind spots. Managing debt exposes where money leaks occur and where lifestyle changes are needed.

- It builds resilience. Facing and resolving debt strengthens financial habits that last beyond repayment.

- It turns awareness into action. Once you confront debt, you begin taking measurable steps toward independence.

- It marks the start of growth. Every payment made, every expense tracked, brings you closer to long-term stability.

When you change how you see it, debt becomes less about what you owe and more about what you learn. Understanding this shift is the foundation for climbing the seven levels of financial freedom.

Suggested Read: How to Effectively Manage and Reduce Debt

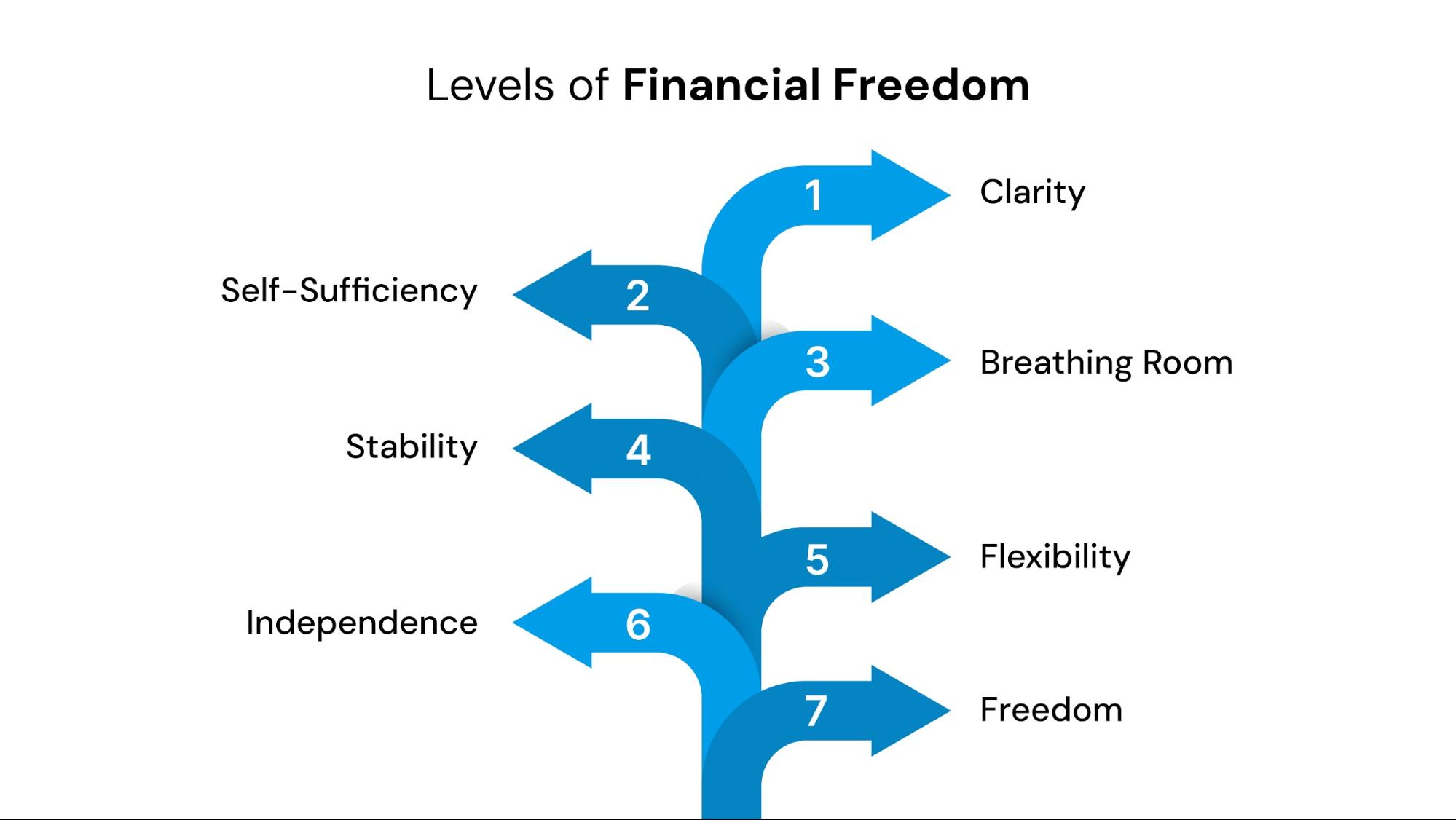

The 7 Levels of Financial Freedom (Even If You’re in Debt)

The concept of seven levels of financial freedom, popularized by Grant Sabatier, charts a path from financial survival to long-term abundance. While originally designed for wealth-building, this model is equally relevant for individuals managing debt.

As CNBC reports, “Half of working Americans are on Level 2 (Self-Sufficiency).” That means millions are still in the early stages. They are working hard, covering essentials, and trying to stay afloat.

If you are dealing with debt, this framework can serve as a practical roadmap.

Level 1: Clarity

You begin by understanding your financial reality: how much you earn, how much you owe, and how you spend. At this stage, you are no longer avoiding your situation. This is the foundation for all progress when managing debt and building freedom.

Actions to take to gain financial clarity:

- List all your income sources, monthly expenses, and outstanding debts.

- Calculate your total debt and your monthly minimum payments.

- Set one small goal — for example, reduce one recurring expense or make one extra payment this month.

When you take these steps:

You move from uncertainty to awareness. The anxiety that comes from “not knowing” begins to fade, and you can finally see the numbers clearly. With that clarity, you gain the power to plan, which is the first real step toward financial control.

Level 2: Self-Sufficiency

At this stage, you are earning enough to cover your basic needs, such as rent, food, utilities, and essential bills. You do not need to rely on others or fall behind. You may still have debt, but you are keeping up with payments and no longer living in constant crisis.

Actions to take to build self-sufficiency:

- Prioritize essential expenses over discretionary spending.

- Create a basic monthly budget to ensure your income consistently exceeds expenses.

- Set up auto-payments for minimum debt obligations to avoid late fees or penalties.

- Avoid taking on any new debt until you have a steady cash flow.

When you take these steps:

You establish the foundation of financial stability. Living within your means brings peace of mind and the ability to start planning for savings. Even if you are still living paycheck to paycheck, consistent budgeting helps you transition from surviving to managing. This shift marks real progress toward financial freedom.

Level 3: Breathing Room

This is where you move beyond covering the basics. You start creating space in your budget. You are no longer just meeting minimum payments; you are paying down debt strategically and setting money aside for short-term needs.

The focus here is control. Understanding that every dollar you direct with intention brings you closer to independence.

Actions to take to create breathing room:

- Identify high-interest debts and target them using a structured payoff method (snowball or avalanche).

- Track discretionary expenses to find at least one area to cut back each month.

- Put a small buffer (even $100 or $200) in a separate savings account to reduce reliance on credit cards.

When you take these steps:

You begin to experience relief. Your money is no longer entirely consumed by bills, and you finally have a little room to breathe. Each small surplus you create signals progress toward control, and every month, that breathing room grows into confidence.

Level 4: Stability

One-third of Americans lack an emergency savings fund, and nearly 29% report they are unable to cover an unexpected expense of just $400.

At this stage, your goal is to stop living one emergency away from financial stress. Building an emergency fund becomes essential.

Actions to take to build stability:

- Start an emergency fund, aiming for $500 first, then one month’s expenses.

- Keep your emergency savings separate from your checking account to avoid the temptation to spend.

- Continue paying down debt, but prioritize savings for true emergencies.

- Review and adjust your insurance coverage to minimize future financial risks.

When you take these steps:

You shift from reaction to preparation. Instead of panic when a car repair or medical bill appears, you have a plan and a cushion. This stability does not erase debt, but it protects your progress and creates the emotional calm that allows you to think long-term.

Level 5: Flexibility

You now have consistent cash flow, manageable debt, and growing savings. Your credit is improving, and you are beginning to look ahead.

This is not just for next month’s bills, but also for future goals, such as retirement, education, or homeownership. Financial security means your systems are functioning properly, even when life becomes unpredictable.

Actions to take to strengthen financial security:

- Grow your emergency fund to cover three to six months of living expenses.

- Continue improving your credit score by paying bills on time and reducing your credit card utilization.

- Automate savings and debt payments to ensure consistency.

- If your situation allows, and after high-interest debt is under control, consider small investments (such as employer retirement plans or low-cost index funds).

When you take these steps:

You transition from financial survival to strategic planning. Money stress no longer dictates your daily life, and you make decisions with foresight, not fear. Every automated payment and planned deposit pushes you closer to true independence and freedom of choice.

Level 6: Independence

Independence means your money decisions are driven by choice, not necessity. You have built systems that sustain themselves. Your savings grow automatically, debt is under control, and your emergency fund provides true protection. Your financial obligations no longer define you; instead, you are shaping your future on your own terms.

Actions to take to achieve independence:

- Pay off all remaining high-interest debt and maintain low or zero balances on credit cards.

- Expand income streams through side work or other additional income; where appropriate and after repayment stability, you may explore modest investment growth.

- Reinvest savings into assets that generate long-term growth.

- Set clear, purpose-based goals, such as travel, career flexibility, or early retirement.

When you take these steps:

You gain freedom from paycheck dependence. Money becomes a tool, not a trap. You can afford to take calculated risks, such as switching jobs, starting a business, or pursuing personal goals. This is because your financial foundation is secure. Independence gives you control over time, not just money.

Level 7: Freedom

This is the highest level. This is where financial decisions are guided by purpose rather than pressure. You have no high-interest debt, strong savings, and assets positioned for growth (should you choose to invest), while continuing to manage risk. True freedom is not about having unlimited wealth; it is about having the flexibility to live life on your own terms, without financial fear.

Actions to take to maintain freedom:

- Continue to budget mindfully, even when income exceeds expenses.

- Diversify investments to protect long-term wealth.

- Revisit your goals regularly to ensure your financial decisions align with your values.

- Give back through charitable contributions, mentorship, or financial education for others.

When you take these steps:

You move from financial independence to fulfillment. Money no longer dictates your decisions; it supports them. At this level, financial freedom means peace of mind, confidence in your future, and the ability to create a positive impact beyond yourself.

When managing debt, you don’t have to go it alone. The Forest Hill Management offers structured and personalized repayment solutions, focusing on flexible payment plans, clear communication, and secure systems. So contact us today and learn more.

Suggested Read: Does Debt Consolidation Affect Buying a Home?

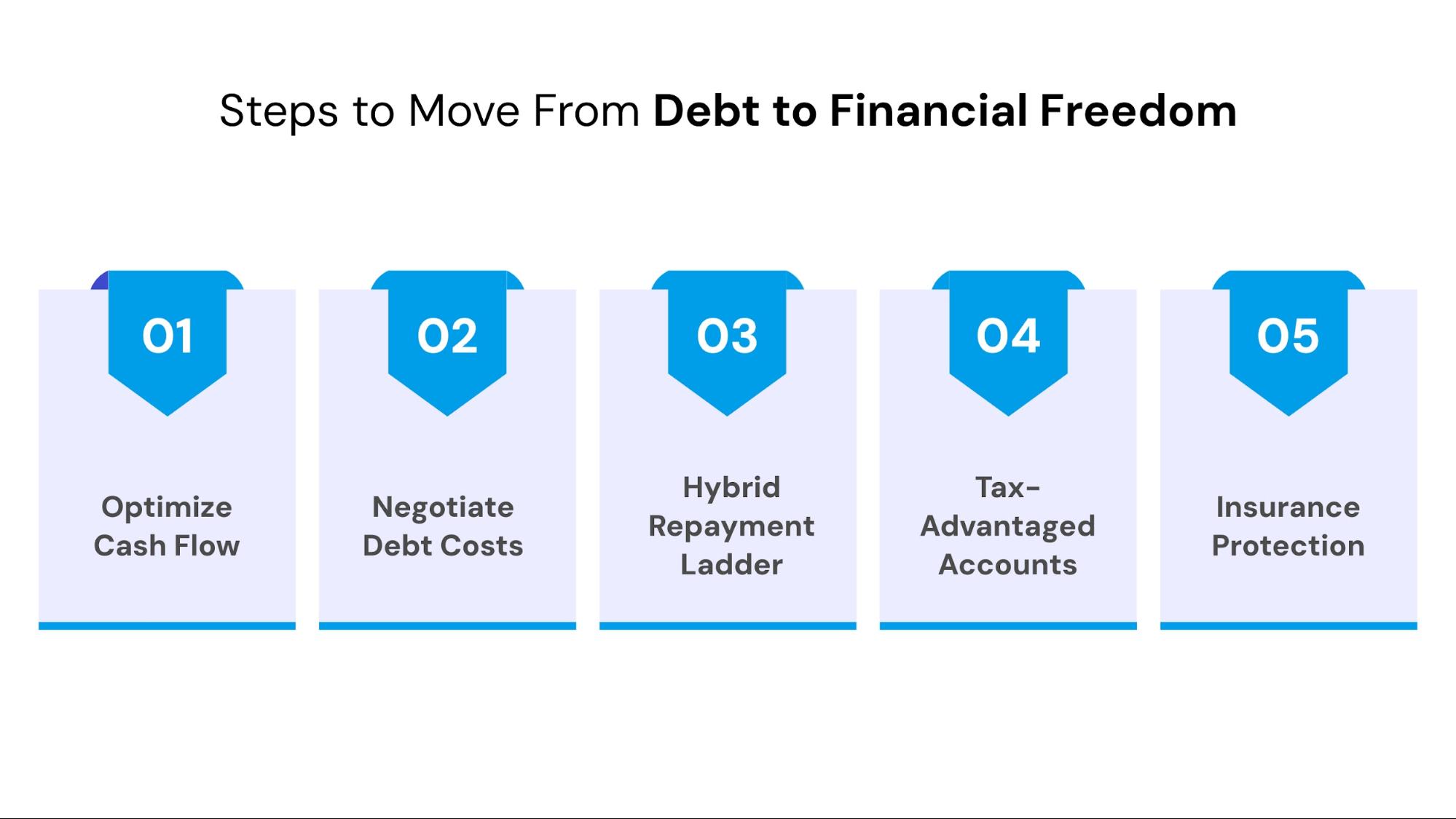

Steps to Move From Debt to Financial Freedom

The FIRE (Financial Independence, Retire Early) movement often feels out of reach for people still paying off debt. However, its principles of purposeful spending, aggressive debt reduction, and strategic saving apply to anyone seeking financial control.

You do not need to retire early to adopt the FIRE mindset; you just need to direct every dollar toward freedom instead of frustration.

These steps will help you get closer to financial freedom:

- Optimize Cash Flow, Not Just Income: Structure your budget around pay periods and assign every dollar a job. Reduce unnecessary recurring costs and redirect those funds to debt repayment or savings.

- Negotiate the Cost of Debt: Contact creditors to lower interest rates or fees, and explore hardship or consolidation options that make repayment more manageable.

- Use a Hybrid Repayment Ladder: Pay off small debts first to build momentum, then focus on high-interest balances to save money in the long term. Reapply freed-up funds to the next target.

- Leverage Tax-Advantaged Accounts: If available, claim employer retirement matches and use HSAs or IRAs for long-term growth while reducing taxable income.

- Protect Progress with Smart Coverage: Maintain insurance policies that safeguard against financial setbacks from emergencies, such as disability, health, or auto coverage.

When you apply these steps consistently, your financial system starts to work for you instead of against you. The next section explores specific strategies and practical tools that can turn these steps into measurable progress toward true financial freedom.

Suggested Read: What Are Installment Loans and How Can They Help Pay Debt?

Smart Strategies to Fast-Track Your Financial Freedom

Financial freedom has a number, and you can calculate it. Using the Rule of 25, multiply your annual expenses by 25 (or monthly by 300) to find how much you need invested to live comfortably without relying on a paycheck.

For example, if you spend $3,000 a month, your target is about $900,000.

It may sound ambitious, but reaching it starts with small, strategic steps that help you earn more, save faster, and make your money work harder, even while managing debt.

Here are five proven strategies to get there faster:

- Debt Stacking with Income Layering

Combine the snowball and avalanche repayment methods with income “layers”, such as side gigs, tax refunds, or bonuses, directed entirely to principal reduction. This compounds progress and reduces total interest paid dramatically.

- Cashflow Conversion Strategy

Treat every expense as an investment test. Convert non-essential recurring costs (such as subscriptions, dining out, and impulse buys) into cash flow savings redirected to high-yield accounts or index funds. Each $50 saved monthly equals over $9,000 in ten years at a 6% annual growth rate.

- Investment Recycling Method

Once debt is under control, channel your old debt payments directly into automatic investments. Start small with ETFs, 401(k)s, or robo-advisors. But make the transition seamless. What once drained your finances now builds your freedom.

- Micro-Saving Automation

Use apps or automatic bank features to round up every purchase and invest the difference. The small change effect builds consistent micro-investments without lifestyle cuts. Invisible effort, visible results.

- The 50/30/20 Freedom Split

Redefine the classic rule: allocate 50% to essentials, 30% to financial goals (such as debt, savings, and investments), and 20% to lifestyle. This keeps the balance and ensures your “future self” always gets paid first.

Each of these strategies transforms your approach to money from passive spending to intentional building. And when managing debt feels overwhelming, Forest Hill Management can help you put these methods into motion.

How Forest Hill Management Supports Every Level of Financial Freedom

Forest Hill Management supports individuals managing outstanding debts through flexible, secure, and compliant repayment solutions.We believe in ethical, transparent, and technology-driven receivables management that allows people to move steadily toward financial stability and independence.

This is how we support your journey:

- Personalized Payment Plans: Tailored repayment solutions designed around your income, lifestyle, and financial goals. It is never a one-size-fits-all approach.

- Flexible Repayment Options: Online and phone-based payments make it simple to stay consistent, without adding pressure or confusion.

- Clear, Transparent Communication: Regular updates and clear account information ensure you always know where you stand and what comes next.

- Secure, Compliant Processes: Every interaction and payment follows strict data and regulatory standards, giving you confidence and peace of mind.

- Dedicated Customer Support: A team of professionals who guide you through repayment with understanding and accountability, instead of judgment.

With Forest Hill Management, managing debt is about rebuilding financial confidence. Our approach helps you stay on track at every level, converting the repayment process into a structured step toward lasting financial freedom.

Conclusion

Reaching financial freedom requires discipline, clarity, and consistency through each repayment. Every time you make a payment, set aside savings, or avoid new debt, you move closer to stability and control. The path may be gradual, but with focus and structure, it leads to real independence and peace of mind.

At Forest Hill Management, we understand that financial freedom starts with taking back control. Our personalized repayment plans, flexible payment options, and transparent communication make it easier to manage debt while rebuilding confidence in your financial future.

Regain control, rebuild stability, and rediscover financial freedom by starting now. Contact us to create a plan that fits your goals.

Frequently Asked Questions

1. Can I start investing while I still have debt?

Yes, you can, but only after covering essentials and minimum payments. Once high-interest debts (like credit cards) are under control, it makes sense to invest small, consistent amounts in low-cost funds or employer-matched retirement accounts.

2. How do I decide whether to save or pay off debt first?

A balanced approach works best. Focus on clearing high-interest debt first while maintaining a small emergency fund (around $500–$1,000). This prevents you from going deeper into debt when unexpected expenses arise.

3. How long does it usually take to reach financial freedom?

It depends on income, debt amount, lifestyle, and consistency. Most people can move from financial instability to basic independence within 5–10 years of structured planning and disciplined debt repayment.

4. Will paying off debt improve my credit score immediately?

It improves gradually. On-time payments, lower credit utilization, and fewer open balances will steadily raise your score over several months. Avoid closing old accounts too quickly, as they help maintain your credit history length.

5. What are the four pillars of financial freedom?

They are earning, saving, investing, and protecting. Together, these pillars help you generate income, grow wealth, and safeguard your finances by creating long-term stability and control over your financial future.

6. What is the 70/20/10 rule for money?

It divides your income into 70% for essentials, 20% for savings or debt repayment, and 10% for giving or personal growth, promoting balance between living comfortably today and planning for tomorrow.