What Are Installment Loans and How Can They Help Pay Debt?

Transform Your Financial Future

Contact UsManaging debt can feel overwhelming, especially when you are juggling multiple bills and high-interest rates. With U.S. consumer debt reaching $17.57 trillion in Q3 2024, many households are seeking predictable and manageable repayment options to avoid spiraling into revolving balances.

If you are struggling to keep up with payments, you are not alone in considering installment financing for repaying your debts. But is this the right choice for you? In this blog, we will explore what installment loans are, how they work, and whether they can help you manage and pay off your debt effectively.

Brief breakdown:

- Installment financing is a type of loan where you borrow a fixed amount of money and repay it in equal, scheduled installments over a set period.

- Understanding how installment loans work helps you make informed decisions when managing or consolidating debt, preventing costly mistakes, and ensuring manageable payments.

- Personal loans, auto loans, mortgages, and student loans are common types of installment loans. These are designed for specific purposes, such as buying a car, a home, or financing education.

- In installment financing, you will receive a lump sum upfront, with fixed monthly payments that include both principal and interest. The loan term is agreed upon in advance, ensuring predictable payments.

- Timely payments on installment loans can improve your credit score by reducing credit utilization and adding to your positive payment history, while missed payments can hurt your score.

What Are Installment Loans and How Do They Work?

An installment loan is a financial product for a specific amount of money. You will need to repay it over time in fixed, equal payments. These loans offer borrowers a predictable repayment schedule, which makes it more manageable compared to revolving credit options.

Installment financing can be used for various financial needs. They come with both short- and long-term repayment options depending on the amount borrowed and the loan terms.

Types of Installment Loans

These are the most common types of installment loans, each with unique characteristics based on the purpose of the loan and repayment terms:

- Personal Loans: These loans are typically unsecured. They can be used for unexpected bills, debt consolidation, home improvements, medical emergencies, and other similar expenses.

- Auto Loans: Car loans are designed to help borrowers purchase a car or other vehicles. They are secured loans against the car.

- Mortgages: These are long-term loans used for purchasing a house, often with lower interest rates but extended repayment periods.

- Student Loans: Borrowed for educational expenses, often offering deferred payments until after graduation with specific repayment options.

Breaking Down Installment Financing

When you take out an installment loan, you basically agree to fixed installments each month for a set period. Here's how they generally work:

- Loan Amount: You receive the full loan amount upfront.

- Fixed Payments: The loan is paid back in equal monthly payments that include both the loan principal and interest.

- Interest Rate: The rate you pay depends on your credit profile and the loan type.

- Repayment Terms: The term of the loan can vary from a few months to several years, depending on the loan and lender.

- Predictability: With fixed payments, installment loans provide the stability needed for easier financial planning.

Installment loans are great because they offer a structured way to manage your debt. But can they be used to consolidate multiple debts? In the next section, we will explore how installment financing can help your debt repayment process and whether it’s the right solution for consolidating existing debt.

Suggested Read: Consumer Impact Recovery and Debt Collection Guide

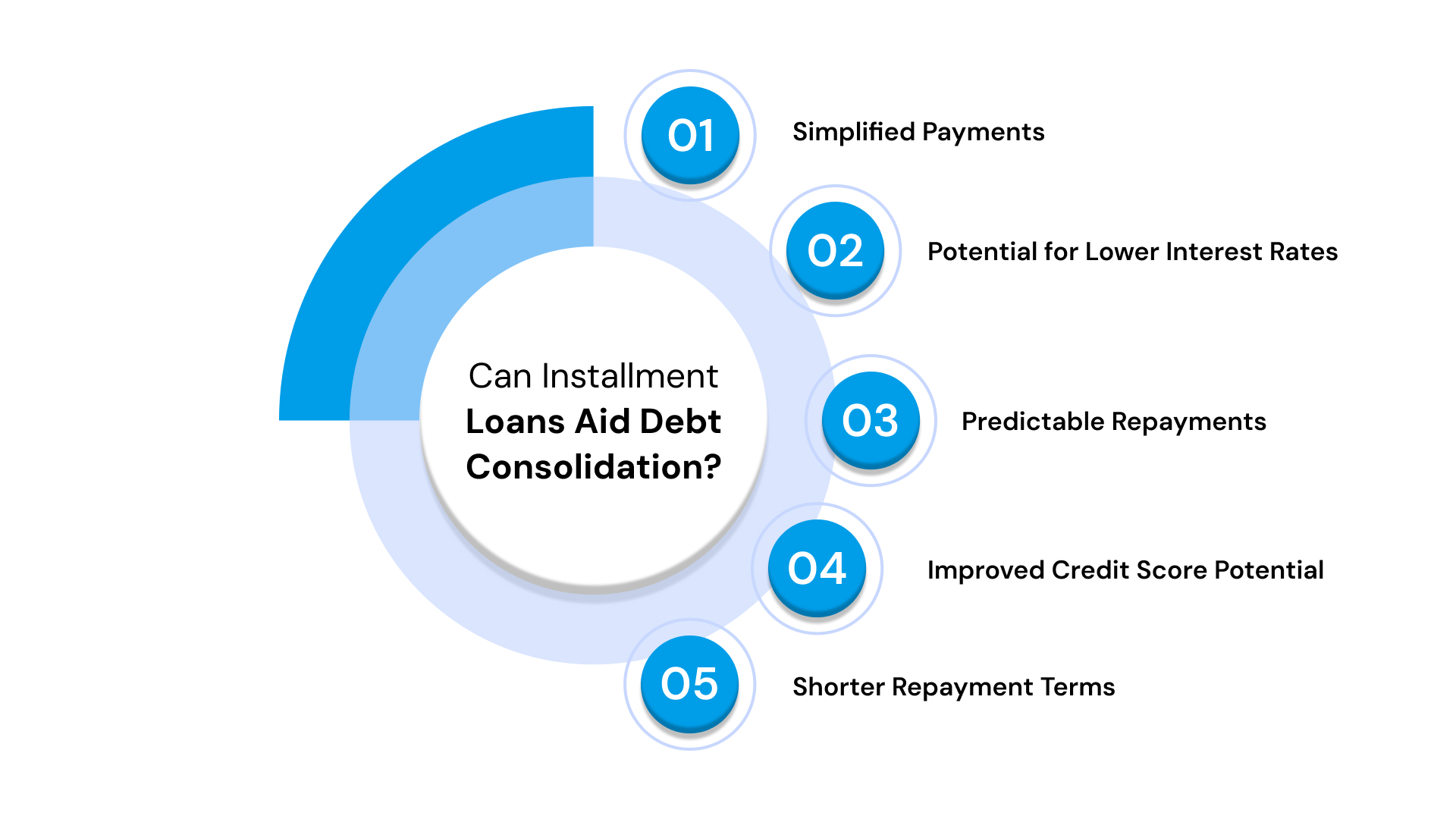

Can Installment Financing Help With Debt Consolidation?

Debt consolidation places multiple debt payments into a single, manageable monthly installment. By consolidating multiple outstanding debts into a single loan, you can simplify the repayment process. You can stay on top of your installments without having to manage multiple payment deadlines.

Here's how installment financing can assist in debt consolidation:

- Simplified Payments: Combine multiple high-interest debts into one fixed monthly payment.

- Potential for Lower Interest Rates: Consolidating debt into a low-interest personal loan can help reduce costs in the long run. This is especially true if you are consolidating credit card or payday loan debt.

- Predictable Repayments: Fixed monthly payments allow you to plan your budget more effectively and avoid the unpredictability of revolving credit.

- Improved Credit Score Potential: Successfully consolidating and paying off debt reduces the credit utilization ratio and avoids missed payments.

- Shorter Repayment Terms: Consolidating your debt into a shorter term than your original debts allows you to pay off your debt faster and save on interest.

While installment financing can be an effective solution for consolidating debt, it’s important to carefully weigh the pros and cons of using another loan to clear your overdue debt.

In the next section, we will look into the disadvantages of clearing your debt with an installment loan.

Cons of Clearing Your Overdue Debt with Another Loan

When considering taking out another loan to clear overdue debt, it’s essential to evaluate both the benefits and the risks. While this approach can potentially simplify your finances, it also comes with its own set of challenges.

These are the disadvantages of using an installment loan to clear overdue debt:

- Additional Debt: Taking on an installment loan adds more debt, potentially leading to a cycle of borrowing.

- Longer Repayment Terms: Extending your repayment period can increase the total amount paid in interest over time.

- Missed Payments: Missing payments can negatively impact your credit score, making future borrowing more difficult.

- Potential Fees: Some installment loans come with hidden fees or penalties. You need to be careful not to increase the overall cost of borrowing.

- Doesn't Address Underlying Financial Issues: An installment loan doesn't solve the root cause of debt, like overspending or poor financial habits.

The Verdict: A Gray Area

While consolidating overdue debt with another loan can be helpful in some situations, the verdict is not always clear-cut. It can be an effective solution for simplifying payments and potentially reducing your interest rate, but it also comes with risks such as taking on additional debt or extending your repayment timeline. Ultimately, the decision depends on your unique financial situation and the terms of the loan you are considering.

At Forest Hill Management, we understand that managing overdue debt can be overwhelming. That’s why we offer personalized portfolio management solutions designed to help you get back on track. Contact our financial advisors today to create a customized debt repayment plan that eases your situation.

Impact of Installment Loans on Credit Score

When considering installment loans, borrowers often worry about how these loans will affect their credit score. While installment loans can be an effective tool for managing debt, they have a significant impact on your credit profile, both positively and negatively.

These are a few ways installment financing affects credit rating:

- Positive Impact on Credit Mix: Having a variety of credit types (e.g., credit cards, installment loans, mortgages) is favorable for your credit score. An installment loan can go a long way in diversifying your credit mix and improving your credit score over time.

- Timely Payments Can Improve Your Score: Making on-time payments on any borrowing will help you create a positive payment history. Timely payments account for 35% of your credit score calculation.

- Lower Credit Utilization: Paying off high-interest revolving debt (such as credit cards) with an installment loan can reduce your credit utilization ratio. TransUnion advises keeping credit utilization balances below 30% to improve your overall score.

- Hard Inquiry Impact: Applying for an installment loan creates a hard inquiry. These may temporarily lower your credit score. However, the impact of a single hard inquiry is usually minimal and short-term.

- Debt-to-Income Ratio: If your installment loan increases your overall debt load, it could negatively affect your debt-to-income ratio, making it harder to secure additional credit in the future.

Is Installment Financing Wise for Credit-Challenged Borrowers?

For credit-challenged borrowers, installment loans can provide an opportunity to rebuild credit, mainly when used to consolidate high-interest debts. However, it’s essential to assess whether the loan terms are manageable. Be careful not to take on more debt than you can handle.

In the next section, we will explore how to use installment loans responsibly without overextending yourself.

Suggested Read: What Happens If You Miss a Payment on Consumer Easy Credit?

Use Installment Loans Without Overextending Yourself: Tips

Installment loans procured for the right reasons with favorable terms can help manage debt. But they can also lead to financial strain if not used wisely. To avoid overextending yourself, it's essential to approach installment loans with a clear plan and realistic expectations. By ensuring that your loan terms align with your financial goals, you can avoid falling into deeper debt.

These are a few tips on using installment financing responsibly:

- Assess Your Budget Before Borrowing: Make sure the monthly loan payment fits comfortably into your budget without stretching your finances too thin. Ensure you can continue paying for other necessary expenses.

- Only Borrow What You Need: It’s tempting to borrow more than necessary, but borrowing only the amount you need will help reduce interest costs and make the loan easier to manage.

- Keep Loan Terms Short if Possible: Shorter loan terms mean higher monthly payments, but they can save you money in the long run by reducing the total interest paid.

- Prioritize Paying Off High-Interest Debt: Use an installment loan to pay off credit cards and other high-interest debt. This will help you save money on interest over time.

- Set Up Automatic Payments: Avoid missed payments by setting up automated bank account deductions. This way, you can stay on track and avoid late fees.

While installment financing may seem like a solution, it’s not always necessary, and it may not be the best option for everyone. At Forest Hill Management, we understand the challenges you are facing with debt, and we are here to help you explore alternatives that can better suit your financial situation. We offer flexible repayment options tailored to your budget. Call us today for options that align with your goals and ability to repay.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

Alternatives to Installment Financing for Debt Management

Installment loans are just one of the many solutions available. Depending on your financial situation, there are other alternatives that may offer more flexibility, lower costs, or be better suited to your needs.

These are a few other options to take care of your debt:

- Credit Counseling: Credit counselors are professionals and can help you create a debt management plan (DMP). You can use this to negotiate with creditors for lower interest rates or reduced payments.

- Debt Settlement: This option involves negotiating with creditors to settle your debt for less than you owe, typically through a lump-sum payment. However, this alternative may have a negative effect on your overall credit score.

- Balance Transfer Credit Cards: You should think about transferring any credit card balances to a card with a 0% introductory APR. This will help you pay off your debt faster by saving the money you would have otherwise spent on paying the high interest rates.

- Home Equity Loans or Lines of Credit (HELOCs): If you own a home, there is always the option to take out a HELOC. Tap into this equity to secure a lower-interest loan or line of credit. But you need to understand that this puts your home at risk.

- Personal Bankruptcy: While a last resort, filing for bankruptcy can help eliminate or restructure debt. A significant drawback is that bankruptcy has serious long-term consequences on your scores.

Before choosing an installment loan or any of these alternatives, it’s important to fully understand the terms, potential risks, and how they fit into your overall financial plan. In the next section, we will cover the key considerations to keep in mind before committing to an installment loan.

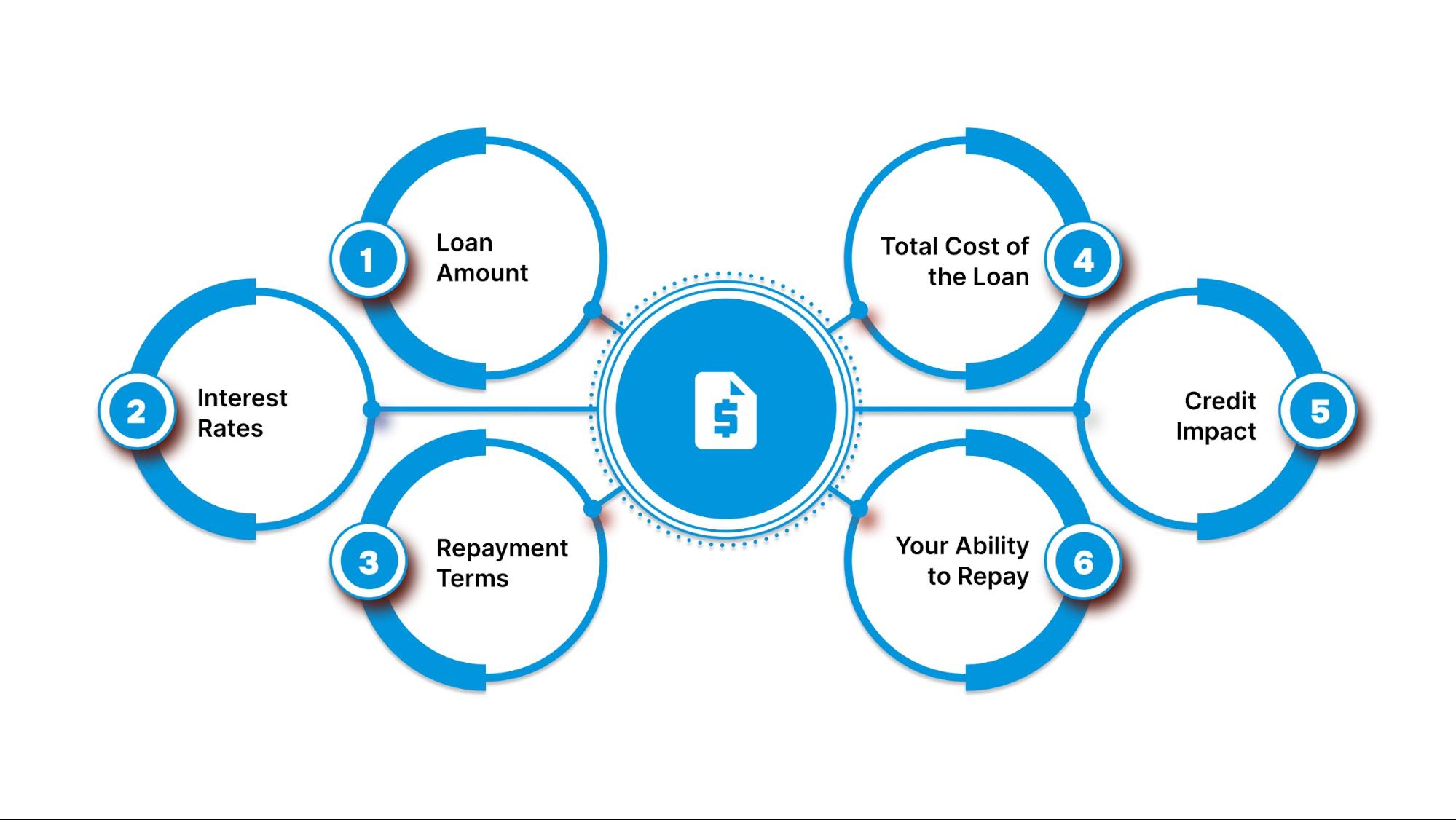

Key Considerations Before Committing to an Installment Loan

Taking out an installment loan can be a helpful solution for managing debt, but it’s not a decision to be made lightly. Before committing to this type of loan, it's essential to assess whether it's the right choice for your financial situation. By carefully evaluating the loan terms and your ability to repay, you can avoid taking on more debt than you can manage.

These are a few things you need to consider before applying for installment financing:

- Loan Amount: Ensure that you only borrow what you truly need. If you borrow more than necessary, you risk incurring unnecessary interest costs.

- Interest Rates: Compare the interest rate on the installment loan with your current debts. A lower rate could save you money, but make sure the terms are clear and competitive.

- Repayment Terms: Understand the length of the loan. You need to know how the monthly payments change your budget. Ensure that you can comfortably meet the repayment schedule.

- Total Cost of the Loan: Consider the total cost of the loan, including interest and any fees, to determine if it’s worth taking out in comparison to other debt management options.

- Credit Impact: While installment loans can help improve your credit score if paid on time, they can also negatively impact it if you miss payments. Make sure you are ready to commit to the repayment plan.

- Your Ability to Repay: Assess your current financial situation and future stability. Taking out a loan while in a tight financial spot could lead to further stress and debt.

If you are feeling uncertain about whether an installment loan is the right path, Forest Hill Management can help. Our helpful finance experts will work with you to assess your debt situation and create a strategy that best fits your financial needs.

In the next section, we will explore how Forest Hill Management can support you in managing your debt with confidence and finding a solution that works for you.

Get the Right Help to Manage Your Debt with Confidence

Managing debt can feel overwhelming, especially when the available options seem too complex or out of reach. At Forest Hill Management, we understand the financial stress that comes with mounting debt, and we are here to help you navigate your options with confidence.

Our personalized approach and expert guidance can provide the clarity and support you need to take control of your financial future.

These are a few ways we support debt repayment:

- Personalized Debt Solutions: We don’t offer one-size-fits-all solutions. Our team begins by analyzing your financials to develop a personalized repayment plan structured to your unique financial situation.

- Compliance and Transparency: We ensure that all our practices align with industry standards and regulations, so you can trust that you only receive ethical, transparent assistance.

- Financial Education and Guidance: We provide you with the knowledge you need to make informed decisions. Our experience can help you avoid common pitfalls and build a strong foundation for future financial success.

- Dedicated Support: Our team is available to answer questions, provide updates, and guide you every step of the way, ensuring that you never feel alone in the process.

- Debt Ownership and Management: As debt owners, we take on the responsibility of managing your debt. We ensure that your debt is handled efficiently and in alignment with your repayment capabilities.

At Forest Hill Management, we believe that everyone deserves an opportunity to regain control of their finances. Whether you are dealing with overdue debt or struggling to make ends meet, we are here to help you develop a clear, actionable plan for debt relief.

Conclusion

Installment financing can be a valuable tool for paying off debt, especially when you need to consolidate multiple obligations into a single, predictable monthly payment. However, taking out another loan means adding more debt to your financial plate, which may not always be the best solution for everyone. It’s essential to consider whether you truly need another loan or if there are better alternatives available.

Forest Hill Management helps people manage their debt without needing to take on additional loans. We work with you to create a personalized, easy-to-manage repayment plan. Our team is here to help you regain control and set a clear path toward financial stability.

Take the stress out of your financial journey. Contact us today to find a repayment strategy that works.

Frequently Asked Questions

1. Are Installment Loans Different From Unsecured Personal Loans?

Installment loans involve fixed payments over a set period, while personal loans can be used for various purposes, often with flexible repayment terms. Installment loans have a fixed structure, making budgeting easier.

2. Is an Installment Loan the Same as a Line of Credit?

No, an installment loan provides a lump sum with fixed repayments, while a line of credit offers flexible borrowing with a credit limit and variable payments based on usage, offering more flexibility.

3. What Are the Common Eligibility Requirements for Installment Loans?

Eligibility for an installment loan depends on factors like credit score, income, and debt-to-income ratio. The creditor you apply to will assess your ability to repay before approving the loan.

4. Can Installment Loans Be Repaid Early?

Yes, most installment loans can be repaid early without penalties. However, some loans may have prepayment fees, so it’s important to review the terms before making extra payments.

5. Are Installment Loans Secured or Unsecured?

Installment loans can be both secured and unsecured. Secured loans require collateral (e.g., home or car), while unsecured loans do not, but may come with higher interest rates due to the lack of collateral.

6. What Happens If I Can’t Make My Installment Loan Payment?

If you miss a payment, the lender may charge late fees and report the missed payment to credit bureaus, damaging your credit score. It’s important to contact the lender if you face difficulties.

7. Can I Get an Installment Loan with Bad Credit?

Yes, but the terms may not be as favorable. Creditors tend to charge higher interest rates in case of bad credit scores. They may also require a co-signer or collateral to secure the loan.