Does Debt Consolidation Affect Buying a Home?

Transform Your Financial Future

Contact UsConsolidating debt can feel like a significant step toward regaining control. According to Experian’s 2024 Consumer Debt Study, personal loan balances, which are often used for debt consolidation, totaled $555.2 billion.

Many individuals worry that lenders may view consolidated debt cautiously or that their credit profile might appear less stable than before. These concerns are understandable since financial transitions can sometimes blur the next steps.

Debt consolidation does not close the door on buying a house. It simply alters the terrain slightly. In the sections that follow, we will explain five key aspects you can expect after consolidation and how to prepare well to minimize the impact.

Quick look:

- You can take on a mortgage after debt consolidation, but lenders may view your credit and debt profile differently. This can affect approval timelines and terms.

- Debt consolidation tends to result in a temporary dip in credit scores due to new accounts or credit inquiries, but maintaining on-time payments helps rebuild them steadily.

- Your debt-to-income ratio can change as monthly obligations are adjusted, and lenders use this metric to determine how much mortgage you can responsibly afford.

- Consolidating debt into a mortgage or taking on new loan terms can lower monthly payments, but it may increase total interest over time and extend your repayment period.

- Being aware of these factors allows you to plan ahead, manage your finances carefully, and make informed decisions as you work toward homeownership.

What is Debt Consolidation and When Does It Make Sense?

Debt consolidation involves combining multiple debts you hold into a single loan or payment plan. This is to make it easier to manage monthly obligations and potentially lower interest costs. You can consolidate debt through several options, such as personal loans, balance transfer credit cards, or home equity loans.

These are a few situations when you may want to consider debt consolidation:

- Multiple debts with high interest rates

- Difficulty keeping up with several monthly payments

- Desire to simplify finances and reduce stress

- Ability to commit to a consistent repayment plan

The next step is understanding how this change can affect your plans for buying a home. Let’s explore five ways debt consolidation can shape the home-buying process.

Suggested Read: Calculating Financial Freedom Number using Passive Income Formula

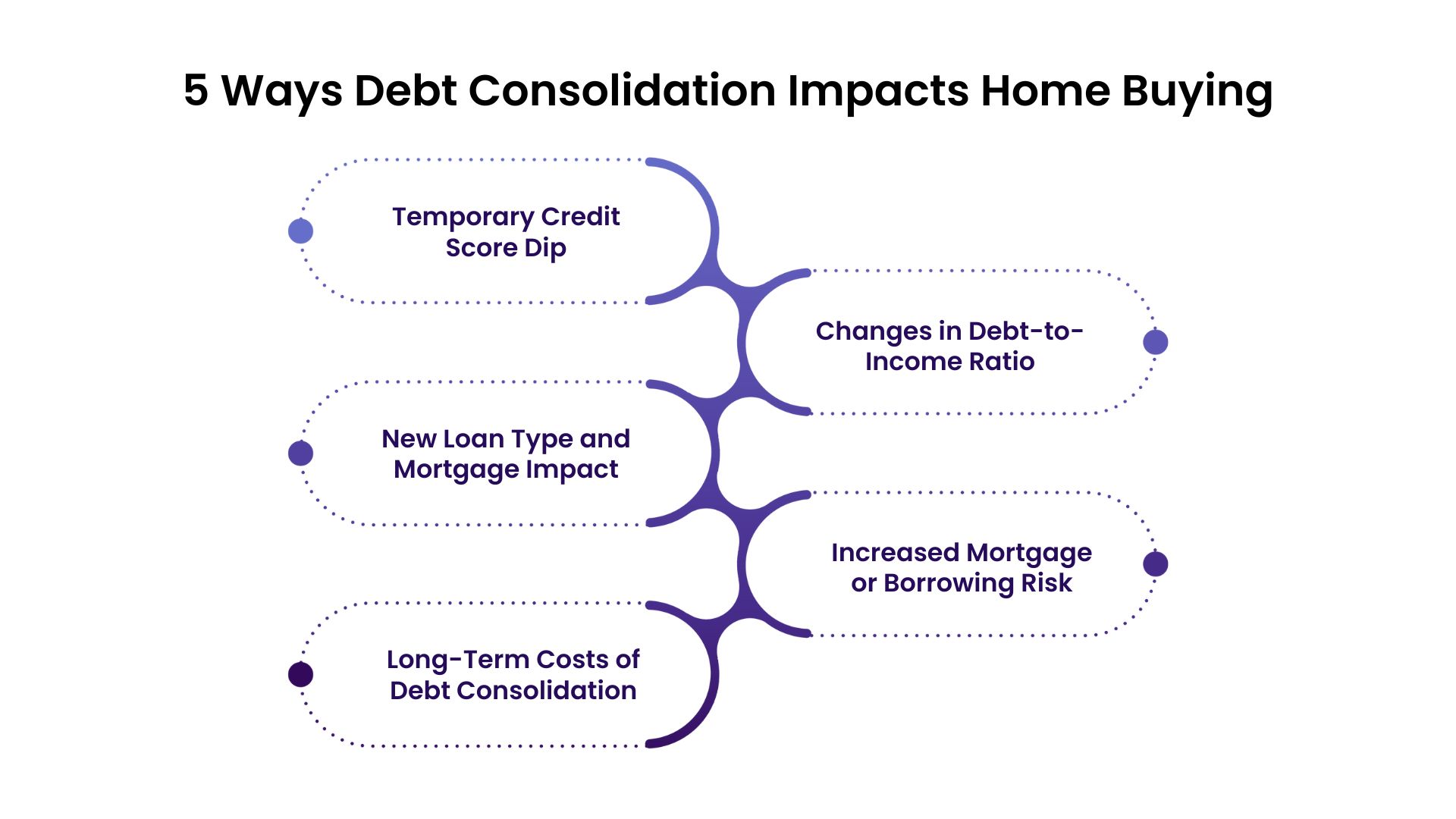

5 Ways Debt Consolidation Affects Buying a Home

Consolidating debt can simplify day-to-day finances, but it also introduces changes that may impact the home-buying process. Understanding these effects helps you plan and make informed decisions.

The following points break down what to expect, giving you a clearer picture of how consolidation interacts with mortgage planning.

1. Temporary Dip in Credit Score

When you consolidate debt, your credit score may experience a temporary dip. This is a normal part of the process and typically rebounds as you continue to manage your finances responsibly.

Key points:

- Hard Inquiries: Applying for a new loan or credit card to consolidate debt often involves a hard credit inquiry, which can cause a slight, short-term decrease in your credit score.

- Credit Utilization: Consolidating credit card balances into a personal loan can negatively affect your credit utilization ratio, but this may lead to an improvement in your credit score over time.

- Account Closures: Closing credit card accounts after consolidation can reduce your overall available credit, which may temporarily affect your credit score.

- Payment History: Consistently making on-time payments on your new consolidation loan can positively impact your credit score over time.

While these changes can affect your credit score in the short term, maintaining good financial habits will help improve your credit profile in the long run.

2. Changes in Your Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) will be used by lenders to see how comfortably you can manage monthly payments relative to your income. Keeping a balanced DTI helps demonstrate financial responsibility and improves your mortgage prospects.

Key points:

- DTI Calculation: Total all your monthly debt obligations, including credit cards, personal loans, auto loans, and any existing mortgage. Divide this figure by your gross monthly income. This shows lenders the proportion of income already committed to debt.

- Impact of Consolidation: Combining multiple debts into a single loan can lower your monthly payments, which may reduce your DTI. A lower DTI signals to lenders that your finances are under control and you can handle a mortgage payment responsibly.

- Behavior Matters: Simply consolidating is not enough. Consistently making on-time payments after consolidation further demonstrates reliability and financial discipline.

- Other Factors: Lenders also consider savings, employment stability, and credit history alongside DTI. A well-managed DTI is just one piece of the approval puzzle.

According to Wells Fargo, a DTI ratio of 35% or less is generally considered ideal, though ratios up to 49% may be acceptable depending on other factors.

Suggested Read: When Does the Collection Process Begin for Overdue Balances

3. New Loan Type / Terms May Affect Mortgage Options

When you consolidate debt, the new loan you take on can change how lenders assess your finances. This doesn’t block homeownership, but it can influence what mortgage options are available and how quickly you qualify.

Key points:

- Loan Type Matters: Secured loans (like using home equity) may tie debt to an asset, while unsecured personal loans don’t. Lenders may view secured debt differently, which can affect mortgage considerations.

- Monthly Payment Changes: Longer-term consolidation loans can lower monthly payments, improving short-term affordability, but lenders also look at total debt levels when evaluating mortgage eligibility.

- New Credit History: Opening a consolidation loan creates a new account. Lenders notice recent accounts when reviewing your credit profile, though timely payments can quickly build positive history.

- Balancing Multiple Debts: If some debts remain separate, lenders may count them alongside the consolidated loan, influencing your overall debt picture and mortgage options.

Understanding how a new consolidation loan interacts with mortgage assessments helps you plan realistically. It’s about recognizing changes and preparing accordingly, rather than avoiding consolidation altogether.

4. Increased Mortgage or Borrowing Risk

Consolidating debt can change your overall financial picture, and lenders may assess your ability to take on a mortgage differently afterward. While consolidation often helps manage payments, it can temporarily make your debt profile appear larger or more complex.

Key points:

- Higher Total Debt on Record: Combining debts may increase the total balance reported on your credit report, which lenders consider when assessing affordability.

- Secured vs. Unsecured Considerations: If consolidation involves a secured loan, like using home equity, the debt is tied to an asset. Lenders will note this in mortgage applications, as it adds a layer of responsibility and risk.

- Short-Term Credit Adjustments: Opening a new loan changes your credit profile, which can slightly influence mortgage interest rates or terms until a payment history is established.

- Importance of Consistent Payments: Maintaining regular, on-time payments on consolidated debt reassures lenders that you can handle future obligations, helping reduce perceived risk over time.

While consolidation can temporarily alter how lenders view your finances, careful management of payments helps mitigate this effect. Understanding these shifts allows you to plan your mortgage application more effectively.

Forest Hill Management offers flexible repayment plans and secure online payment options, making it easier to stay consistent with debt obligations. We can help you build the financial stability lenders look for when reviewing mortgage applications. Make a payment today and improve your debt situation.

5. Longer-Term Costs and Trade-Offs of Debt Consolidation

While consolidating debt can simplify payments, it may also change the total cost of borrowing. Lower monthly payments sometimes come with longer repayment terms, which can increase interest paid over time or introduce additional fees. Knowing these trade-offs helps you plan realistically for homeownership.

Key points:

- Extended Repayment Terms: A longer loan term reduces monthly payments. However, longer term also means an increase in the total interest paid. Lenders factor this into your mortgage application to assess ongoing affordability.

- Potential Fees and Closing Costs: Some consolidation loans, especially home equity loans or refinances, may include origination fees, appraisal costs, or other upfront charges. These costs do not prevent homeownership but can affect short-term finances.

- Impact on Monthly Budget: Lower payments improve short-term cash flow, but it’s important to account for the cumulative cost over the life of the loan to avoid surprises.

- Strategic Planning: Understanding the full cost helps you choose consolidation options that align with both debt management and future mortgage goals.

Being aware of these trade-offs allows you to make informed decisions and maintain control over your finances. Consolidation can simplify your life, but having a complete understanding of the situation ensures you are prepared for the months and years ahead.

Suggested Read: Impact of New Medical Debt Rules on Collections

What Happens When You Roll Your Existing Debt Into a Home Loan?

Rolling existing debt into a mortgage means including your outstanding obligations, such as credit cards, personal loans, or other balances, into the new home loan. Essentially, your mortgage covers not only the cost of your home but also pays off prior debts, resulting in a single monthly payment.

Consider the following points before deciding if this strategy is right for you:

- Single Payment Convenience: Instead of managing multiple payments, your consolidated debt is now part of your mortgage, making budgeting simpler.

- Longer Repayment Term: Since mortgages typically span 15–30 years, the monthly payment on your consolidated debt may be lower, but total interest paid over time will increase.

- Impact on Loan Amount & LTV: Rolling debt into your mortgage increases the loan balance, which can affect your loan-to-value ratio and potentially influence lender terms.

- Interest Rates: Mortgage interest rates may be lower than credit card rates, but they apply over a longer period. Understanding this trade-off is crucial for planning.

- Credit Considerations: Lenders assess both the total debt and your repayment history. A higher mortgage balance might influence your mortgage approval and interest rate, even if your monthly payments are more manageable.

Understanding how rolling debt into a mortgage can help you make informed decisions. But there are still other factors that can influence your approval. Let’s take a closer look at these in the next section.

Suggested Read: How To Pay Debt in Credit Collection Services

Other Factors That Influence Mortgage Approval

Even after consolidating debt, lenders consider a variety of other factors when evaluating mortgage applications. Understanding these elements helps you plan effectively and avoid surprises along the way.

Keeping these elements in mind makes it easier to plan your next steps with confidence:

- Down Payment & Cash Reserves: Lenders look for sufficient funds for a down payment and emergency reserves. A solid cushion demonstrates financial responsibility and reduces risk in their eyes.

- Credit History & Behavior: Beyond scores, lenders review your full credit history, including payment patterns and account longevity. Consistently managing debt and avoiding missed payments builds trust.

- Employment Stability: A steady income reassures lenders that you can handle monthly mortgage obligations. Frequent job changes or gaps in income may require additional explanation.

- Type of Mortgage / Loan Programs: Certain loan types (e.g., FHA, VA, or other government-backed programs) may have more flexible criteria for applicants managing debt. Knowing your options helps you select the best fit.

- Loan-to-Value Ratio (LTV) & Home Equity: If you used home equity for consolidation, your remaining equity or LTV will affect lender decisions. Maintaining a reasonable balance can help improve approval chances.

- Regulatory & Lender Policies: Different lenders have unique underwriting standards, including DTI limits and credit score minimums. These policies can help you target lenders aligned with your situation.

Understanding these factors helps you see the bigger picture as you prepare for a mortgage. In the next section, we list the strategies that can help you strengthen your financial profile.

Suggested Read: What Happens If You Miss a Payment on Consumer Easy Credit?

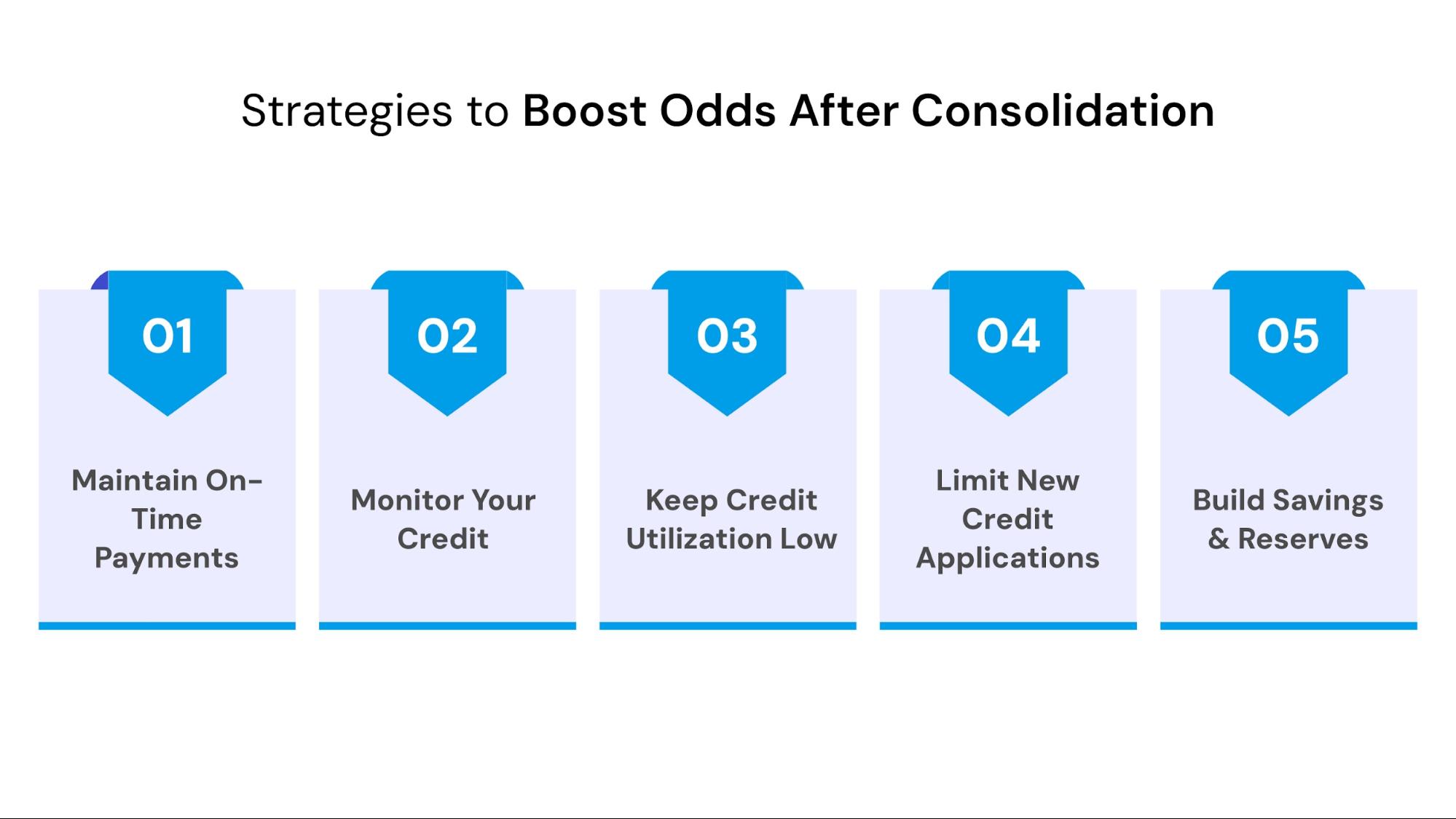

5 Strategies to Improve Your Odds After Consolidation

While debt consolidation helps simplify payments, taking a few additional steps can improve your chances of mortgage approval. These are:

- Maintain On-Time Payments: Consistently paying your consolidation loan on time builds positive credit history.

- Monitor Your Credit: Regularly check your credit reports for accuracy and progress.

- Keep Credit Utilization Low: Avoid high balances on remaining credit cards. Low utilization demonstrates responsible credit management.

- Limit New Credit Applications: Avoid opening new accounts before applying for a mortgage, which could trigger hard inquiries.

- Build Savings & Reserves: Even small savings improve your financial profile and show readiness for homeownership.

Managing debt while planning for a home can feel overwhelming, but you are not alone. Forest Hill Management works with you to create repayment plans structured around your unique situation. By staying consistent with your plan, you can take control of your debt and move closer to your goal of homeownership with confidence. Contact us for custom repayment plans today.

Signs You May Not Be Ready to Buy Just Yet

Even after consolidating debt, there are situations where it might be wise to hold off on buying a home. Recognizing these signs early can help you avoid unnecessary stress and make sure you are financially prepared when the right opportunity arises.

These are a few things to watch for:

- Unstable Income or Employment: Frequent job changes, inconsistent income, or recent employment gaps can make mortgage approval more challenging.

- High Debt Levels Relative to Income: If your debt obligations still consume a large portion of your income, it may be difficult to comfortably afford mortgage payments.

- Limited Savings or Emergency Funds: Without sufficient savings for a down payment, closing costs, or unexpected expenses, buying a home may put a strain on your finances.

- Recent Credit Changes: If you recently consolidated debt or opened new accounts, lenders may want to see several months of consistent repayment before approving a mortgage.

- Financial Stress or Inconsistency: Struggling to manage day-to-day expenses or keep up with payments may indicate it’s better to stabilize finances before taking on a mortgage.

If any of these signs sound familiar, it’s a good time to focus on building a repayment plan that works for you. Forest Hill Management can help by creating structured, manageable repayment options that support your long-term goals and keep you moving toward homeownership at a pace that makes sense.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

Access Flexible Repayment Plans That Support Your Long-Term Goals

Managing debt while planning for a home can feel overwhelming, but you don't have to tackle it alone. Forest Hill Management specializes in helping individuals regain control of their finances through structured, flexible repayment plans tailored to each person’s situation.

Our goal is to make debt management straightforward, secure, and supportive of your long-term goals. This is how we can help:

- Personalized Repayment Plans: We design plans that fit your income and lifestyle, ensuring payments are manageable and realistic.

- Secure Online Payment Options: Pay conveniently and safely, with a system that tracks your progress and gives you peace of mind.

- Flexible Scheduling: Adjust payment dates or amounts where possible to accommodate life changes without losing momentum.

- Clear Guidance: We provide expert advice on navigating collections, helping you understand your obligations and options at every step.

- Supportive Approach: Our team works with you, not against you, ensuring that every step you take is practical, achievable, and empowering.

With Forest Hill Management by your side, managing debt becomes less stressful and more purposeful. By staying consistent with a plan customized just for you, you can confidently work toward homeownership and other long-term financial goals—one step at a time.

Conclusion

Debt consolidation can be a helpful tool for managing multiple obligations. Still, it can also make home buying feel complicated and overwhelming. This is especially true if you are unsure how your debt, credit, or monthly payments will affect mortgage approval.

Many people struggle to stay consistent with payments when planning for a major financial step, which can add stress and uncertainty. Forest Hill Management makes debt repayment simple. With structured repayment plans tailored to your situation, we help you manage debt in a manageable and predictable way.

Gain the clarity and stability you need to focus on long-term goals, such as homeownership. Take control of your debt today by creating a plan that works for you. Reach out to us for a more confident financial future.

Frequently Asked Questions

1. Can I consolidate debt if I have a low credit score?

Yes, there are consolidation options available for individuals with lower credit scores, though interest rates or loan terms may vary. Exploring secured vs. unsecured options can help you find a solution that fits your situation.

2. Will consolidating debt affect my ability to get other types of loans besides a mortgage?

Debt consolidation may temporarily alter your credit profile, which lenders consider for personal, auto, or student loans. Maintaining consistent payments after consolidation can help mitigate any short-term effects.

3. Are there risks in using a home equity loan for debt consolidation?

Using home equity to pay off debt can lower monthly payments, but it also ties the loan to your property. Missing payments could put your home at risk, so careful planning is essential.

4. Can consolidating debt improve my monthly cash flow?

Yes, consolidating multiple high-interest debts into a single loan with lower payments can improve monthly cash flow, making budgeting easier and reducing financial stress.

5. How long should I wait after consolidating debt before applying for a mortgage?

While it depends on your specific financial situation, many experts recommend demonstrating several months of consistent repayment before applying for a mortgage to show stability and reliability to lenders.