How to Manage and Improve Your Debt-to-Income Ratio

Need Help Reviewing Your Account?

Contact UsThere’s a point where your income stops feeling like it’s yours. You know what you earn, but by the time fixed payments are accounted for, what’s left feels tighter than it should.

That’s where debt-to-income ratio quietly becomes relevant. Not as a formula, but as a reflection of how much of your income is already committed before you’ve made a single decision for the month. When that balance starts to shift, it doesn’t always show up immediately. It builds gradually, through overlapping payments, increasing obligations, and less flexibility over time.

Most people don’t notice it until something forces the question. A financial decision, a new expense, or simply the feeling that things are harder to manage than they used to be.

In this blog, you’ll learn what debt-to-income ratio actually means, what a healthy range looks like, and how to manage and improve it through clear, practical steps.

Key Takeaways

- Debt-to-income ratio shows how much of your monthly income is already committed to debt, making it a practical indicator of financial pressure, not just a lending metric.

- Improving DTI requires working on both sides, reducing monthly debt obligations while increasing or stabilizing your income over time.

- Structured approaches like budgeting, prioritized repayment, and consistent tracking are more effective than quick or aggressive changes.

- A high DTI often results from multiple overlapping obligations rather than a single large debt, which makes clarity and organization essential.

- Taking early, informed action on past-due or collection accounts helps reduce pressure and creates a clearer path toward financial stability.

What Is Debt-to-Income Ratio?

Debt-to-income ratio, commonly referred to as DTI, is a simple way to measure how much of your monthly income goes toward paying debts. It shows the relationship between what you earn and what you are obligated to pay each month.

Rather than looking at your total debt, DTI focuses only on your monthly debt payments. This includes things like credit card payments, loan installments, and housing-related obligations. It does not include everyday expenses such as groceries or utilities.

DTI is often used by lenders, but it is equally useful for you. It gives a clear picture of whether your current debt is manageable or starting to put pressure on your finances.

How to Calculate Your DTI Ratio?

Calculating your DTI ratio is straightforward once you break it into steps. The goal is to compare your total monthly debt payments with your gross monthly income.

Step 1: Add up all your monthly debt payments

Include credit card minimum payments, personal loans, auto loans, student loans, and rent or mortgage payments. Only include fixed debt obligations, not general living expenses.

Step 2: Identify your gross monthly income

This is your total income before taxes and deductions. If your income varies, use a consistent average based on recent months.

Step 3: Divide your total debt by your income

Take your total monthly debt payments and divide them by your gross monthly income to get a decimal value.

Step 4: Convert the result into a percentage

Multiply the result by 100 to express your DTI as a percentage. This percentage represents how much of your income is going toward debt each month.

For example, if your monthly debt payments are $1,500 and your gross monthly income is $4,000, your DTI would be:

1,500 ÷ 4,000 = 0.375 → 37.5%

This means 37.5% of your income is being used to cover debt obligations.

Understanding this number helps you assess where you stand and what kind of adjustments may be needed to improve your financial balance.

What Is Considered a Good Debt-to-Income Ratio?

A “good” debt-to-income ratio is a range that reflects how manageable your debt is compared to your income. In most cases, lower is better because it indicates that a smaller portion of your income is tied up in monthly obligations.

Financial institutions generally use a few standard benchmarks to evaluate DTI:

Below 36% → Healthy and manageable

This range suggests that your debt is well within your income capacity, leaving room for savings and unexpected expenses.

36% to 41% → Acceptable but approaching limits

Debt is still manageable, but there is less flexibility. Any increase in expenses or reduction in income can create pressure.

41% to 45% → High and restrictive

At this level, a significant portion of your income is committed to debt, making it harder to manage other financial responsibilities.

Above 50% → Financial strain

More than half of your income is going toward debt, which often indicates difficulty in maintaining payments consistently.

It is important to note that DTI only accounts for debt payments and does not include everyday living expenses. This means that even a “moderate” DTI can feel overwhelming depending on your overall financial situation.

Why Is a Good DTI Ratio Important?

A good DTI ratio does more than improve your chances of qualifying for credit. It directly affects how manageable your day-to-day finances feel and how much control you have over your money.

- It reflects how much financial pressure you are under: A lower DTI means fewer fixed obligations, which gives you more flexibility to handle unexpected expenses without disruption.

- It helps maintain consistency in payments: When your debt is proportionate to your income, it becomes easier to meet payment deadlines and avoid falling behind.

- It reduces reliance on additional credit: A manageable DTI lowers the need to use new credit to cover existing obligations, preventing further financial strain.

- It improves your ability to make financial decisions confidently: With less of your income tied up in debt, you have more room to plan, adjust, and respond to changes without pressure.

- It supports long-term financial stability: Maintaining a balanced DTI allows you to gradually reduce debt while keeping your overall financial situation stable and predictable.

Also read: Understanding the Importance of Financial Stability

A good DTI ratio is not just a target to reach. It is an indicator that your financial obligations are aligned with your income in a way that is sustainable over time.

How to Manage Debt-to-Income Ratio?

Improving your debt-to-income ratio is not about making one big change. It is about adjusting both sides of the equation over time, reducing what you owe each month while strengthening your income where possible. The most effective approach is structured, consistent, and grounded in what you can realistically maintain.

The strategies below focus on practical actions that directly influence your DTI and help you move toward a more manageable financial position.

1. Reduce Existing Debt Strategically

Lowering your monthly debt obligations is one of the most direct ways to improve your DTI. The key is not just paying randomly, but following a method that creates steady progress.

- Use a structured repayment approach like the avalanche or snowball: The avalanche method focuses on paying off high-interest debts first to reduce overall cost, while the snowball method prioritizes smaller balances to create quick wins. Both approaches work, but consistency matters more than which one you choose.

- Prioritize debts based on impact: High-interest accounts increase your monthly burden over time, while smaller balances can be cleared quickly to simplify your obligations. Choosing the right focus depends on your financial behavior and motivation.

- Stay consistent with payments over time: Irregular or aggressive payments that cannot be maintained often lead to setbacks. A steady reduction in balances is what ultimately improves your DTI.

2. Increase Your Monthly Income

While reducing debt is essential, increasing your income can improve your DTI faster than expected because it changes the ratio from the other side.

- Explore additional income sources where possible: This can include overtime, freelance work, part-time roles, or gig-based income. Even modest increases can improve your overall ratio.

- Use additional income with a clear purpose: Directing extra earnings toward debt repayment or covering fixed obligations helps improve DTI more effectively than increasing discretionary spending.

- Focus on stability rather than short-term gains: Temporary income boosts can help, but consistent and predictable income has a stronger long-term impact on your financial position.

3. Consolidate or Restructure Debt Where Possible

In some cases, restructuring your debt can reduce your monthly obligations, which directly improves your DTI.

- Combine multiple debts into a single payment: Debt consolidation can simplify repayment and, in some cases, lower your monthly payment by extending terms or reducing interest rates.

- Focus on reducing the monthly burden: Since DTI is based on monthly payments, even small reductions in required payments can make a noticeable difference.

- Understand when this option may not apply: If accounts are already past due or in collections, consolidation may not be available. In such cases, the focus shifts to resolving those accounts directly.

4. Avoid Taking on New Debt

Managing DTI also means preventing it from increasing further. New debt adds to your monthly obligations and can quickly offset any progress you make.

- Be cautious about new credit during repayment: Opening new credit accounts increases your monthly commitments, even if the initial balance is small.

- Consider the impact of additional obligations: Every new loan or credit line affects your DTI by increasing the denominator of your monthly payments.

- Focus on stabilizing before expanding: Avoiding new debt is especially important when you are already working to reduce existing obligations or recover from past-due accounts.

5. Build a Budget That Supports DTI Improvement

A budget is what connects your income and debt into a workable system. Without it, improving your DTI becomes inconsistent and difficult to track.

- Track your expenses to understand cash flow clearly: Knowing where your money is going allows you to identify areas where adjustments can be made without disrupting essential needs.

- Redirect available funds toward debt repayment: Even small savings from reduced spending can be allocated toward lowering your monthly obligations over time.

- Align your budget with your actual obligations: A budget that reflects your real expenses and debt commitments ensures that your repayment plan remains sustainable.

6. Recalculate Your DTI Regularly

Improving your DTI is an ongoing process, and tracking it helps you understand whether your efforts are working.

- Calculate your DTI on a regular basis: Reviewing your ratio monthly allows you to see how changes in income or debt are affecting your position.

- Use it as a measure of progress, not pressure: Small improvements over time indicate that your strategy is working, even if the changes feel gradual.

- Adjust your approach based on what you see: If your DTI is not improving as expected, you can revisit your budget, repayment plan, or income strategy to make necessary adjustments.

Also read: Latest Consumer Debt Insights and Strategies

Managing your debt-to-income ratio is ultimately about balance. When your monthly obligations align more closely with what you earn, your finances become easier to manage, and your path toward reducing debt becomes more structured and achievable.

What to Do If Your DTI Is Already High or Unmanageable?

A high debt-to-income ratio is not just a number on paper. It usually shows up as pressure in your day-to-day finances, where a large portion of your income is already committed before the month even begins. When DTI crosses into higher ranges, the problem is not just about improving the ratio. It is about regaining control over your obligations in a structured way.

At this stage, broad advice is not enough. What matters is taking targeted steps that address both the current burden and how it is being managed:

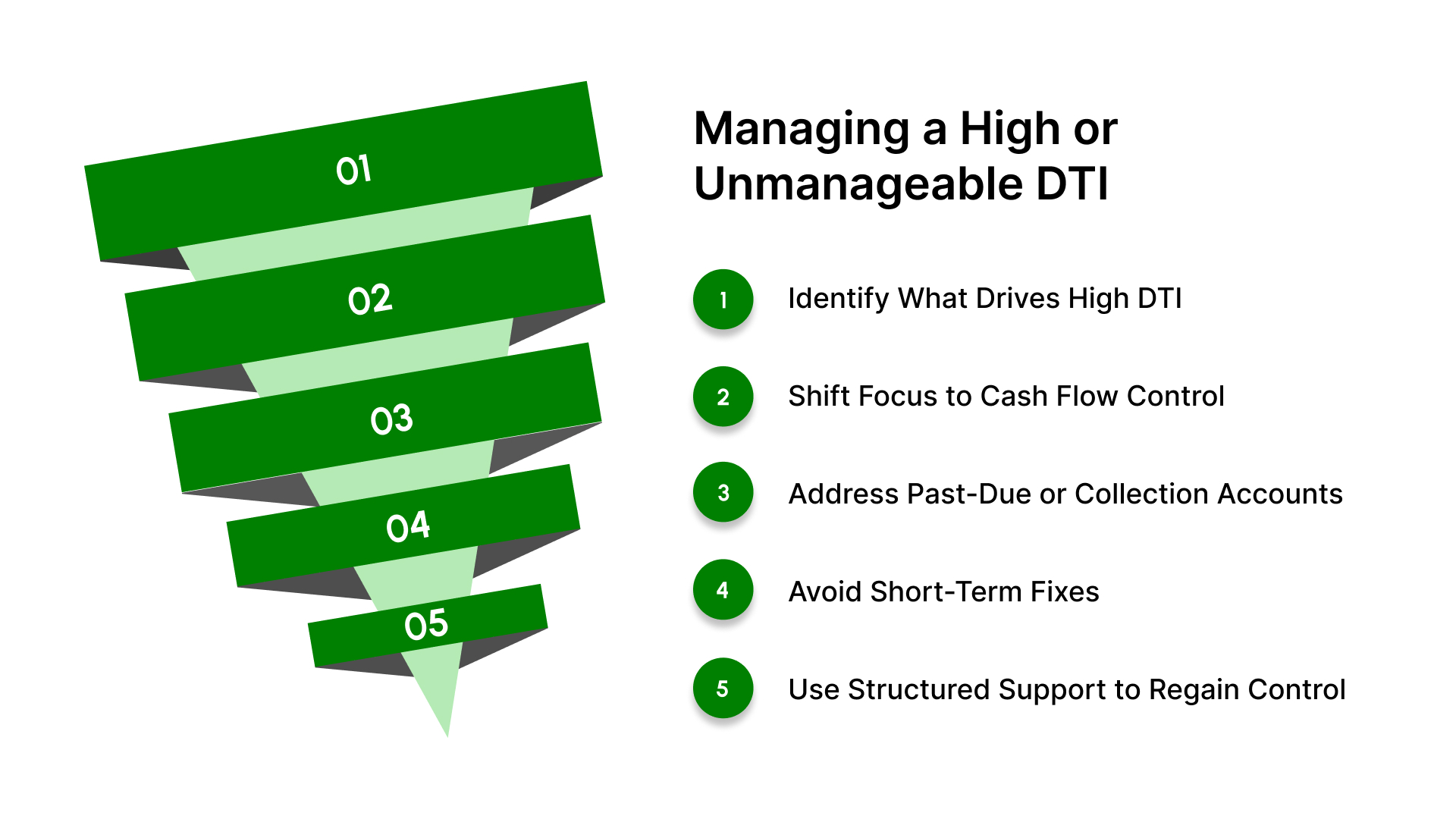

Start by Identifying What Is Driving the High DTI

Before making changes, it is important to understand what is actually pushing your ratio up. In most cases, it is not one large debt, but a combination of multiple obligations that add up.

- Break down your monthly debt payments clearly: List each obligation separately, including credit cards, loans, and any past-due accounts. This helps you see which payments are contributing the most pressure.

- Separate active accounts from past-due or collection accounts: These require different approaches. Active accounts may need restructuring, while past-due balances often require resolution planning.

- Look at payment structure: Two similar balances can have very different monthly impacts depending on interest rates and terms. Focus on what is affecting your monthly cash flow.

Shift Focus from Ratio to Monthly Cash Flow Control

When DTI is high, improving the number itself is a longer process. The immediate goal should be stabilizing your monthly cash flow so that payments become manageable again.

- Prioritize fixed obligations that must be met consistently: This includes housing, essential utilities, and minimum debt payments. Stability at this level prevents further escalation.

- Avoid spreading payments too thin across multiple accounts: Trying to manage everything equally can lead to missed payments. A structured prioritization approach is more effective.

- Create a repayment approach based on what you can sustain: Even if progress is slower, consistency reduces pressure and prevents the situation from worsening.

Address Past-Due or Collection Accounts Directly

If part of your DTI pressure comes from accounts that are already past due, ignoring them will not improve the situation. These accounts need a defined path toward resolution.

- Confirm account details and current status: Understanding who is managing the account and what is owed helps remove uncertainty before taking action.

- Focus on structured repayment rather than quick fixes: A clear plan, even if gradual, is more effective than irregular payments or delays.

- Use your budget to define what is realistically possible: This ensures that any repayment plan fits within your current financial capacity.

If your account is already in collections, having the right structure in place makes a meaningful difference. With The Forest Hill Management, you can review your account details clearly, understand your balance, and explore repayment options that align with your situation. Instead of guessing your next step, you have a defined path to move forward with clarity and consistency.

Be Careful with Short-Term Fixes That Increase Long-Term Pressure

When DTI is high, it can be tempting to rely on quick solutions that seem to reduce immediate pressure but create more obligations later.

- Avoid taking on new credit to manage existing debt: This increases your monthly commitments and can push your DTI even higher over time.

- Be cautious with consolidation if it does not reduce monthly payments: Combining debts only helps if it improves your monthly cash flow, not just simplifies the structure.

- Do not rely on temporary income increases alone: Short-term boosts can help, but they should support a long-term plan rather than replace it.

Use Structured Support to Regain Control

When DTI becomes unmanageable, the process becomes less about optimization and more about guidance and structure.

- Seek clarity on your current obligations and options: Understanding your accounts fully is the first step toward making informed decisions.

- Work toward a repayment path that is clear and consistent: A defined structure reduces uncertainty and makes it easier to follow through.

- Take action instead of delaying decisions: Even a small step forward can shift the situation from reactive to controlled.

Also read: Steps to Improve Your Financial Freedom Resources

A high DTI ratio is not something that improves overnight, but it is something that can be managed step by step. Once you shift the focus from the number itself to the structure behind it, the path forward becomes clearer, more stable, and far more manageable.

Conclusion

A high debt-to-income ratio does not happen overnight, and it does not improve overnight either. It is built over time through multiple obligations, and the way forward is to bring structure back into how those obligations are managed.

Once you understand how your income and debt interact, the focus shifts from reacting to payments to managing them with clarity. Small, consistent changes, whether reducing a balance, adjusting your budget, or restructuring payments, begin to ease the overall pressure.

If your debt is already becoming difficult to manage or is being handled by The Forest Hill Management, you do not have to navigate it alone. With clear account details, structured repayment options, and support designed to help you move forward, the process becomes far more manageable.

Take the first step toward financial clarity.

FAQs

1. Does reducing one loan significantly improve my DTI ratio?

It can, especially if the loan has a high monthly payment. Since DTI is based on monthly obligations, removing even one significant payment can noticeably improve your ratio.

2. Can my DTI increase even if I am making payments regularly?

Yes, your DTI can still rise if your income decreases or if new debt is added, even if you are consistently making payments on existing accounts.

3. Is it possible to have a low DTI but still feel financially stressed?

Yes, because DTI does not account for everyday living expenses. A low ratio may still feel tight if your non-debt expenses are high.

4. Should I focus more on reducing debt or increasing income to improve DTI?

Both matter, but the impact depends on your situation. Reducing high monthly payments can have an immediate effect, while increasing income can improve your ratio more gradually.

5. How quickly can DTI improve once I start taking action?

DTI improvement is gradual and depends on consistency. Small, steady changes in payments or income typically show results over a few months rather than immediately.