How Will Accounts Receivable Appear on Financial Statements?

Transform Your Financial Future

Contact UsWhen you are trying to manage debt, it can feel like you are always one step behind, no matter how hard you try. And you are not alone in that feeling. Aggregate delinquency rates remained elevated in Q3 2025, with 4.5% of all outstanding household debt in some stage of delinquency. This is a clear sign that many people are struggling to stay current.

Short-term fixes may help you get through a moment, but they rarely create lasting relief in your long-term financial management. Long-term financial management strategies offer something more meaningful: structure, predictability, and a path toward real, steady debt reduction.

This guide explores how long-term financial management can help you rebuild control, protect your stability, and move forward with confidence.

In brief:

- Short-term fixes do not create lasting progress. Quick solutions can relieve stress temporarily but rarely reduce debt in a meaningful or sustainable way.

- Long-term financial management systems create stability. Systems built around clarity, control, cushioning, and consistency help make progress predictable and manageable.

- Strategies are most effective when they are simple and consistent. Hybrid repayment ladders, expense smoothing, micro-savings, income layering, and quarterly resets strengthen long-term outcomes.

- Small, consistent actions create real change. Even modest monthly adjustments add up over time and protect you from falling back into reactive financial habits.

- Understanding myths prevents setbacks. Challenging common misconceptions helps you make informed decisions and stay focused on long-term financial health.

Why Do Short-Term Fixes Not Lead to Real Debt Progress

Quick solutions may feel like relief in the moment, but they rarely move you forward. Long-term financial planning gives you pacing, structure, and stability. It gives you a system that helps you navigate debt steadily instead of reacting to every crisis.

As productivity expert Alan Lakein said, “Planning is bringing the future into the present so you can do something about it now.”

Here’s how short-term behaviors keep you stuck:

- Minimum-Only Payments: Slow progress and rising interest overshadow any small wins.

- Skipping or Delaying Bills: One late fee can disrupt your entire monthly budget.

- Using Credit Cards for Essentials: Creates a rolling balance that grows faster than you can pay it off.

- Turning to Payday Loans: This adds high-cost, high-risk debt that traps you in a repayment cycle.

- Relying on Quick Cash Options: It prevents long-term solutions like budgeting, buffers, and structured plans from forming.

The payday loan market alone was valued at USD 35 billion in 2023 and is expected to rise to USD 52.30 billion by 2033, showing how many people rely on short-term fixes that keep them stuck rather than supported.

You can break free from this cycle by stepping back and looking at the bigger picture. The first step is understanding the pillars of long-term financial stability, which we will explore in the next section.

Suggested Read: How Does Debt Consolidation Affect Your Credit Score?

The Four Pillars of Long-Term Financial Stability

Long-term financial stability is about building a foundation strong enough to support steady progress even when life feels unpredictable.

These four pillars work together to give you clarity, control, and resilience, so you can move away from crisis-driven decisions and toward calm, consistent financial improvement.

Here are the pillars that support long-term progress:

- Clarity

Understanding your full financial picture, including income, expenses, balances, and interest rates, helps you make decisions based on facts rather than fear. Clarity removes the guesswork and gives you a clean starting point.

- Control

Control comes from structuring your budget, setting priorities, and assigning every dollar a purpose. When your money has direction, debt stops dictating your choices.

- Cushioning

Small savings buffers protect you from setbacks that usually push people deeper into debt. Even a modest emergency fund creates breathing room during stressful months.

- Consistency

Consistent check-ins and adjustments keep your plan relevant and realistic. Progress becomes smoother when you treat your finances like a routine, not a reaction.

When these pillars are in place, long-term planning begins to feel less like a burden and more like a roadmap. And once the foundation is set, you can start layering strategies that actively reduce debt.

Let’s talk about what those long-term strategies actually look like, and how they work in real life.

Suggested Read: Is 698 a Good Credit Score?

Long-Term Strategies That Actually Reduce Debt

Long-term debt reduction requires creating systems that keep you steady through good months and difficult ones. These strategies strengthen your financial habits and remove the unpredictability that often pushes people deeper into debt.

Strategy 1: The Hybrid Repayment Ladder

A hybrid ladder combines small emotional wins with interest-saving logic. It gives you psychological momentum in the beginning and then shifts your focus to the debts that cost you the most.

This is how to make this strategy work:

- Pay off one or two of your smallest balances for quick progress.

- Redirect those payments toward the highest APR debt.

- Reorder your ladder every few months to reflect changes.

This blend keeps the process motivating while still cutting the cost of interest. When used consistently, it shortens payoff timelines because every cleared balance increases your available cash for the next one.

Strategy 2: Expense Smoothing

Expense smoothing spreads irregular costs across the entire year so they never hit your budget all at once. This removes the stress of large quarterly or annual expenses and helps you avoid using credit for predictable needs.

This is how to smooth out your expenses:

- Convert large annual or quarterly bills into monthly amounts.

- Move that monthly amount into a dedicated sinking fund.

- Use the sinking fund only for the expenses you planned.

This gives you a predictable monthly cash flow, which makes budgeting easier and more accurate. It also prevents sudden financial pressure that often leads to new debt.

Strategy 3: Micro-Saving Systems

Micro-saving allows you to build protection in small, manageable pieces. It helps create a safety cushion without taking money away from debt repayment.

This is how to build steady micro-savings:

- Round up purchases into a savings account.

- Set a small recurring savings transfer each payday.

- Keep the amount low so it fits comfortably into your budget.

You can guide your micro-savings by using the 50/30/20 rule, which recommends allocating 50 percent to needs, 30 percent to wants, and 20 percent to savings and debt combined.

Strategy 4: Income Layering

Income layering adds stability by diversifying how money comes into your household. Even modest additional income can create significant flexibility over the course of a year.

This is how to add practical income layers:

- Choose one reliable side task you can commit to each week.

- Turn a skill or hobby into a small service you offer.

- Ask about overtime, performance incentives, or shift additions.

These additional layers do not have to be large. The power comes from consistency, which slowly increases the amount you can put toward debt without creating strain.

Strategy 5: Quarterly Financial Resets

Quarterly resets help you revisit your plan with a clear mind. Life changes frequently, so your financial strategy should adjust too.

This is what to review during a reset:

- Your total debt and interest costs for the quarter.

- Your current savings buffers and sinking funds.

- Any upcoming expenses that need preparation.

This habit keeps your long-term plan accurate and realistic. It also helps you spot progress you might have missed, which boosts motivation and keeps your strategy aligned with real-life changes.

Working with Forest Hill Management, you get tailored repayment plans designed around your real-life income pattern, not idealised scenarios. Our flexible repayment plans make it easier to stay committed, even when income or expenses shift. Clear communication can help you manage debt with confidence instead of stress. Speak to us today.

Steps to Put Long-Term Planning Into Action

Long-term planning creates results that short-term thinking simply cannot match. For example, imagine a person who frees up just 75 dollars each month by smoothing expenses and adding a small side income.

Over a year, that becomes 900 dollars, and when directed toward high-interest debt, it can shorten repayment timelines by several months. This is how small, steady decisions create meaningful change over time.

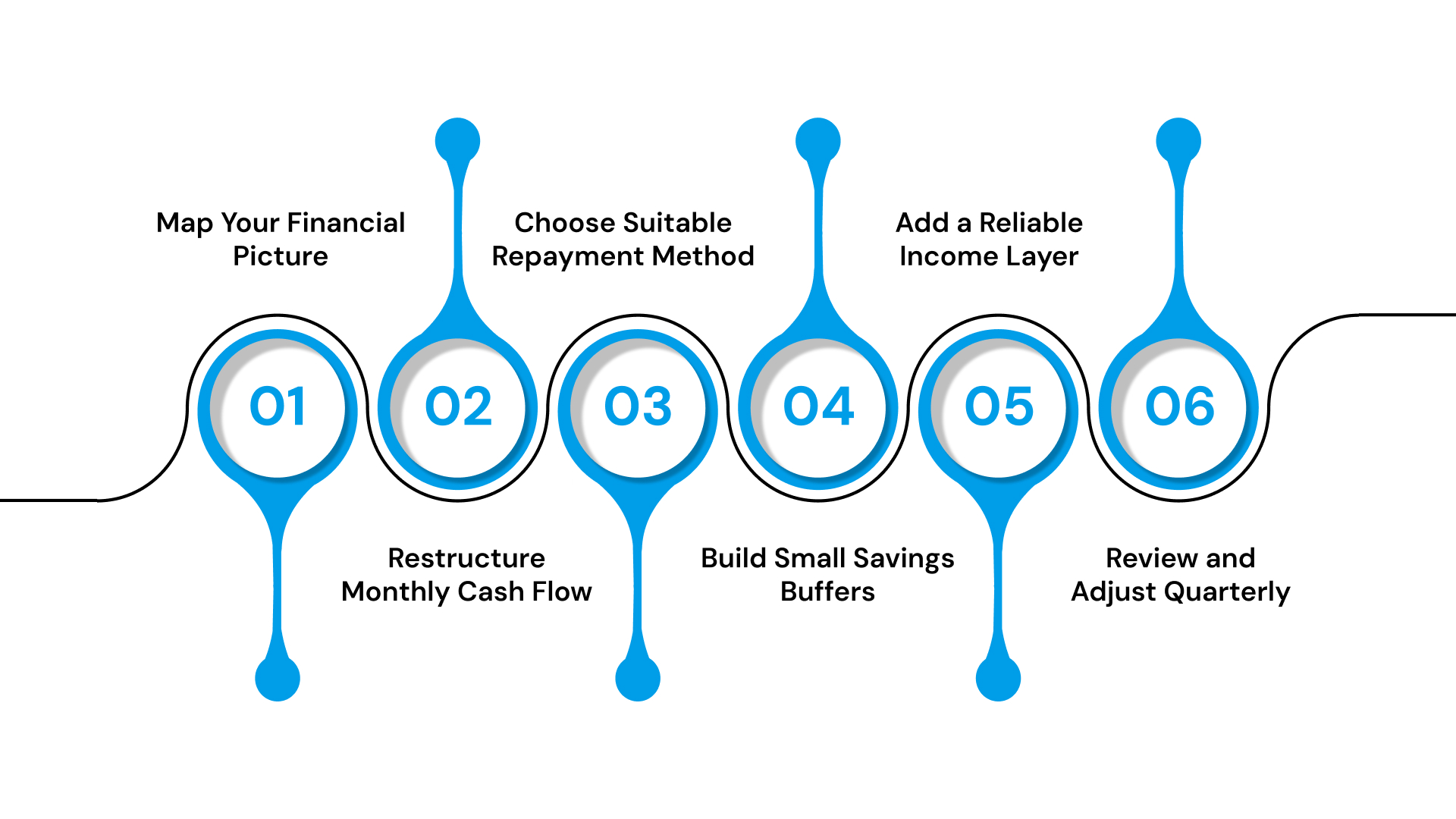

These are the steps that help you turn long-term planning into real progress:

- Map Your Full Financial Picture

List income, expenses, debt balances, interest rates, and due dates. This creates a clean starting point and removes guesswork. Clear information helps you prioritize debts accurately.

- Restructure Your Monthly Cash Flow

Convert annual or irregular expenses into monthly amounts to prevent sudden spikes. Assign each major category a realistic spending limit. This allows your budget to stay consistent throughout the year.

- Choose a Repayment Method That Fits Your Life

Use the hybrid ladder, avalanche, or another structured method that matches your income pattern. A method you can maintain is more effective than one that looks perfect on paper. Consistency matters more than intensity.

- Build Small but Steady Savings Buffers

Create micro-savings for emergencies so your repayment plan stays protected. Even $10 to $25 per paycheck adds up over a year. Buffers prevent setbacks from turning into new debt.

- Add One Reliable Income Layer

Choose an income option you can maintain for at least three months, even if it pays modestly. Layering income provides breathing room and increases your repayment power. Small increases often create large results over time.

- Review and Adjust Every Quarter

Check your debt balances, interest costs, savings, and upcoming expenses. Adjust your plan as your life changes. Quarterly reviews keep your long-term strategy relevant and effective.

Small steps like these build financial momentum that lasts all year. They also reduce uncertainty, which helps you stay calm, consistent, and in control.

In the next section, we look at common setbacks to long-term financial management, so you know what to avoid as you move forward.

Suggested Read: Understanding Medical Bills and Collections: Know Your Rights

Planning Mistakes That Hurt Long-Term Financial Health

Long-term financial planning is most effective when your system is steady, simple, and realistic. Yet many people unintentionally create plans that are too strict, too vague, or too dependent on willpower. Most mistakes are easy to correct once you know what to look for and why they happen.

These are the common mistakes to watch out for:

- Setting Unrealistic Monthly Goals: Goals that require perfection fall apart as soon as life gets unpredictable. Instead, aim for steady progress that you can maintain even in difficult months.

- Ignoring Interest Rate Changes: Interest rates can shift, and that affects your repayment order. Updating your plan regularly ensures you target the debts costing you the most.

- Skipping Savings Entirely: Without a buffer, any small emergency can disrupt your repayment plan. Even modest savings protect your progress and reduce stress.

- Not Adjusting After Life Changes: A plan made six months ago might not match your current income or expenses. Revisiting your strategy helps keep it aligned with your real situation.

- Relying Only on Motivation: Motivation fades, especially during stressful months. Systems like automation and scheduled reviews carry you through low-energy periods.

Most of these pitfalls occur because we have been told to believe in certain ideas about money that simply do not hold up in real life. That brings us to the next section, where we explore the myths about debt management that often keep people stuck.

Myths About Debt Management in the Long Run

A large part of debt stress comes from ideas that sound true but do not reflect real life. As Mark Twain said, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

These myths shape how people approach money, often creating guilt or pressure where none is needed.

Table showing the myths and the reality behind them:

These myths can lead to decisions that feel right in the moment but delay long-term progress. Once you understand the truth behind them, debt becomes easier to manage because you stop fighting yourself and start working with a plan that fits real life.

These tips can help you stay grounded in reality, not the myths:

- Question any rule that makes you feel guilty or ashamed.

- Check whether the advice fits your income, family, and responsibilities.

- Focus on progress over perfection.

- Keep your plan flexible so it can grow with you.

- Give yourself grace during setbacks.

When myths lose their power, long-term planning becomes much easier to follow. This is also where guidance and support make a meaningful difference. Forest Hill Management helps you build structure, clarity, and consistency in your financial path.

How Forest Hill Management Helps You Stay on Track

Long-term financial stability is easier to build when you have steady support instead of trying to navigate everything on your own. Forest Hill Management focuses on clear communication, manageable repayment options, and practical guidance that helps you stay consistent month after month.

Our approach is built on respect, structure, and the understanding that long-term progress requires reliability, not pressure.

This is how we can support your long-term financial journey:

- Personalized Repayment Plans: Your repayment schedule is designed to match your income pattern and household responsibilities so you can stay consistent without feeling overwhelmed.

- Flexible Payment Options: Multiple payment methods give you the freedom to pay in the way that fits naturally with your routine, which supports long-term follow-through.

- Clear and Predictable Communication: We keep you informed with simple, direct updates that help you stay aware of your balance, deadlines, and progress.

- Compassionate Support: Our team listens first and responds with respect. We help you stay on track without judgment, which makes long-term planning easier to maintain.

- Reliable Account Management: We handle your account with accuracy and care so you can focus on your long-term goals rather than the day-to-day details.

Long-term debt management becomes significantly more achievable when you have a team that understands your situation and consistently supports you. With structure and steady guidance, you can make progress at a pace that feels manageable and sustainable.

Conclusion

Long-term financial management requires creating steady habits, clear priorities, and predictable systems that help you stay grounded even when life shifts. When you approach debt with long-term structure instead of short-term pressure, progress becomes calmer, more sustainable, and far more achievable.

Forest Hill Management supports that kind of long-term stability by offering repayment plans that fit real life, not ideal scenarios. Our focus on communication, flexibility, and respectful support helps you stay consistent through every phase of your financial journey.

Explore manageable repayment options that support your long-term goals. Contact us today.

Frequently Asked Questions

1. How do I know if a long-term financial plan is working?

Your plan is working if your debt is decreasing gradually, your savings buffer is growing, and your month-to-month stress is lower. Even small improvements show that your system is doing its job.

2. Should I adjust my plan if my income changes?

Yes. Any change in income should lead to a review of your budget, payment schedule, and savings strategy so your plan stays realistic and sustainable.

3. How can I stay motivated during a long debt repayment timeline?

Break your plan into small milestones and track them visually. Celebrating progress keeps you engaged even when the finish line feels far away.

4. What happens if I cannot follow my plan for a few months?

You can pause, reassess, and restart. Long-term plans are designed to be flexible so they can absorb life changes without losing momentum.

5. Should I prioritize interest rates or balance size when deciding what to pay first?

It depends on your goals. If you want to save the most money over time, prioritize high-interest debt; if you need early wins to stay motivated, start with the smallest balance.

6. What is the 70/20/10 rule money?

The 70/20/10 rule suggests allocating 70 percent of income to living expenses, 20 percent to savings or debt repayment, and 10 percent to charitable giving or personal goals.

7. What is the 10/20/30/40 rule?

The 10/20/30/40 rule divides income into four categories: 10 percent for savings, 20 percent for financial goals or debt, 30 percent for discretionary spending, and 40 percent for essential living costs.