How to Negotiate with Debt Collectors for Settlement

.jpg)

Need Help Reviewing Your Account?

Contact UsMost people don’t expect to have a conversation with a debt collector, and when it happens, the first instinct is usually uncertainty. A few questions come up at once. Is this something I can negotiate? Do I have to pay the full amount? What happens if I get this wrong?

That uncertainty is more widespread than it seems. According to the CNBC, about 1 in 5 Americans has a debt in their collections report, which means millions of people are navigating the same questions around repayment and settlement.

What most people are not told is that debt settlement is not about pushing back or trying to “win” a negotiation. It is a structured process with clear steps. Once you understand how it works, what to verify, what to agree on, and what to avoid, it becomes far more manageable.

In this blog, you will learn how to settle debt with a collection agency step by step, what to keep in mind before agreeing to anything, and how to approach the process in a way that is clear, practical, and aligned with your situation.

Key Takeaways

- Debt settlement is a structured process that starts with verifying the debt, not negotiating the amount, ensuring you are working with accurate and legitimate information.

- Your financial position should guide the settlement, as realistic and sustainable commitments are more effective than aggressive or rushed agreements.

- Settlement agreements must always be documented in writing, clearly stating the amount, terms, and confirmation that the debt is fully resolved.

- Proper documentation and secure payment methods are essential to protect yourself and avoid disputes even after the payment is completed.

- Understanding credit impact, tax implications, legal timelines, and your rights helps you approach settlement with clarity and avoid costly mistakes.

What Debt Settlement with a Collection Agency Means?

Debt settlement with a collection agency is a structured resolution process where an outstanding account is reviewed, verified, and resolved based on mutually agreed terms.

In practical terms, settlement means closing a debt. This agreement is not arbitrary. It depends on factors like the age of the debt, your financial situation, and the agency’s ability to verify and service the account. Regulatory guidance from Consumer Financial Protection Bureau makes it clear that the process must be transparent, documented, and compliant at every step.

Only after these steps does the conversation move toward resolution. At that point, settlement typically takes one of two forms:

- Lump-sum settlement, where a reduced amount is paid in one transaction

- Structured repayment, where the balance is resolved through agreed installments

The key outcome in both cases is the same: the account is considered resolved once the agreed terms are fulfilled, and this must always be confirmed in writing before any payment is made.

Also read: How to Keep Your Debt Resolutions in 2026

It is also important to understand that settlement is not always about paying less. In many cases, especially with verified and active accounts, the focus is on creating a realistic and manageable path to closure, rather than delaying the situation further.

How Does a Collection Agency Help in the Settlement Process?

A collection agency’s role is often misunderstood as purely recovery-driven, but in practice, it also functions as a structured intermediary between the original creditor and the consumer.

- They provide verified account information and clarity: A collection agency is responsible for supplying accurate details about the debt, including the original creditor, balance, and account history. This helps you understand exactly what you are resolving.

- They ensure the process follows regulatory standards: Under laws like the Fair Debt Collection Practices Act (FDCPA), agencies must communicate clearly, avoid misleading practices, and respect your rights throughout the process.

- They offer structured resolution options: Instead of leaving the account unresolved, agencies can outline repayment options that align with your financial situation, including settlement discussions or payment plans.

- They document and formalize agreements: Any settlement must be clearly defined in writing, including the amount, terms, and confirmation that the agreement satisfies the debt. This ensures both clarity and accountability.

- They provide a clear path to account closure: Once the agreed terms are met, the agency confirms that the account is resolved, helping you move forward without lingering uncertainty.

Also read: How to Create an Effective Debt Repayment Plan

Debt settlement, when approached correctly, is not about pressure or quick decisions. It is about moving from an open-ended obligation to a defined resolution, with clarity on what is owed, what will be paid, and what happens next.

Step-by-Step Process to Settle Debt with a Collection Agency

Settling a debt with a collection agency is a structured process that involves verification, financial planning, and clear documentation. The goal is to resolve the account in a way that is accurate, final, and properly recorded.

Many people make mistakes by rushing into payment discussions without understanding the account or their own financial position. A step-by-step approach ensures that you stay in control and avoid outcomes that create further complications.

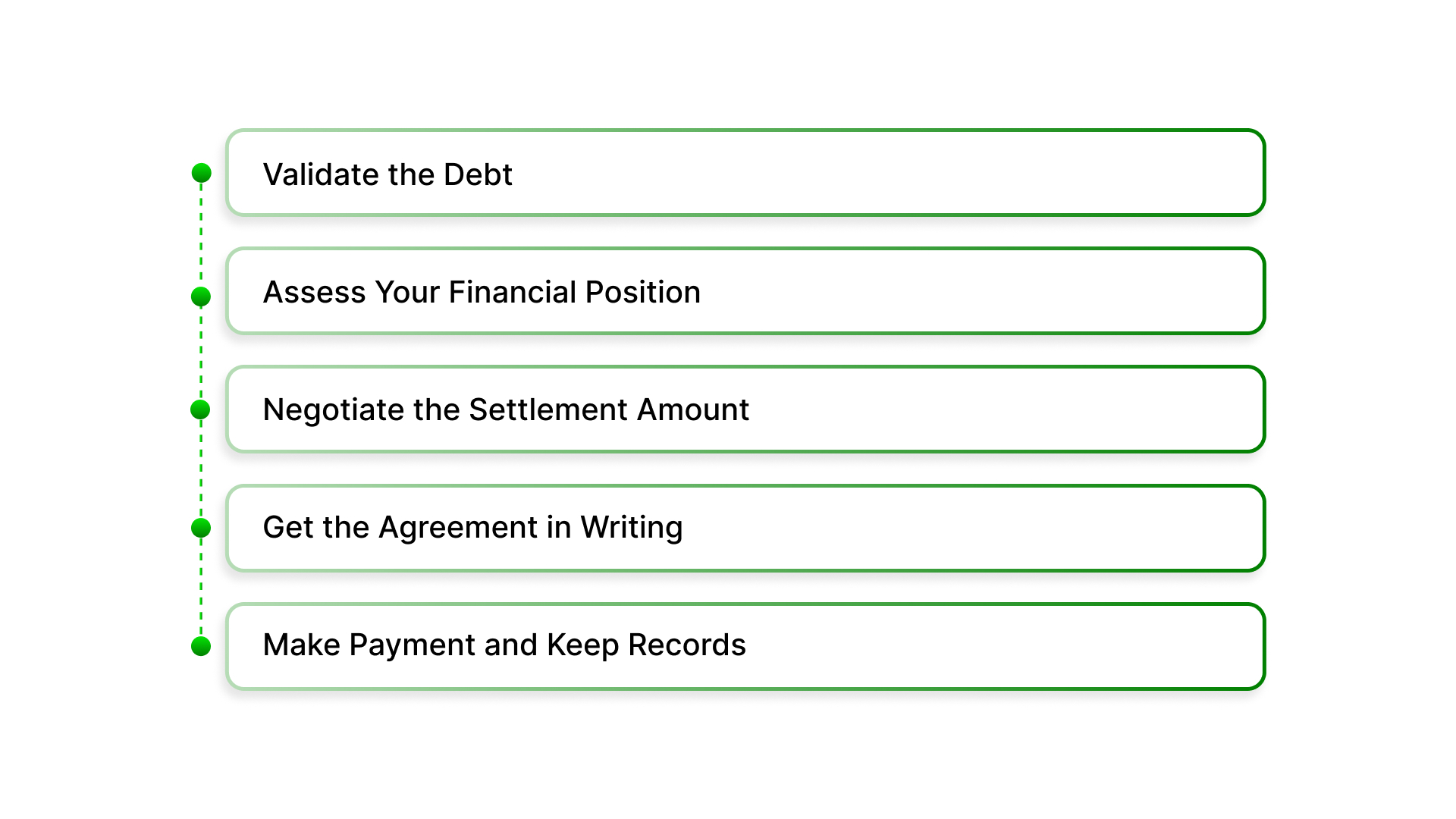

Step 1: Validate the Debt Before Anything Else

Before discussing payment or settlement, the first step is to confirm that the debt is legitimate and correctly reported. This is not optional. It is your right and your protection.

- Request a written validation notice from the agency: This should include the original creditor, total balance, and key account details. You are entitled to this information before taking any action.

- Confirm ownership and the right to collect: The agency must be able to show that they are authorized to collect the debt, either as the assigned collector or current owner of the account.

- Review the amount carefully, including prior adjustments: Ensure that any payments, insurance adjustments, or corrections have already been applied so you are not negotiating on an inflated balance.

- Use your right to dispute if anything is unclear: If the details do not match your records, you can pause the process and request clarification before proceeding further.

This step ensures that you are resolving a legitimate and accurate obligation, not acting under uncertainty.

Step 2: Assess Your Financial Position Realistically

Once the debt is verified, the next step is to determine what you can actually afford. Settlement only works if it is based on realistic numbers, not assumptions.

- Evaluate whether a lump-sum payment is possible: A one-time payment may lead to quicker resolution, but it should only be considered if it does not create additional financial strain.

- Determine a realistic monthly repayment capacity: If a lump sum is not feasible, structured payments can be discussed, but they must align with your income and essential expenses.

- Base decisions on actual numbers: Use your budget to define what you can commit to, rather than guessing or reacting under pressure.

- Avoid overcommitting to close the account quickly: Agreements that are difficult to maintain can lead to missed payments and restart the process.

A clear financial position strengthens your negotiation and ensures that any agreement you enter is maintainable.

Also read: Steps to Become Debt-Free: A Clear Financial Path

Step 3: Negotiate the Settlement Amount

Settlement is a negotiation, but it is also influenced by factors such as the age of the debt, its size, and the collector’s position.

- Understand typical settlement ranges: Many settlements fall between 30% to 80% of the total balance, depending on the situation. Older debts or accounts with lower recovery likelihood may settle for less.

- Start with a lower but reasonable offer: Beginning in the 30% to 50% range allows room for negotiation while still presenting a serious intent to resolve the account.

- Adjust based on response and context: The final amount is often a result of back-and-forth discussion, so flexibility within your limits is important.

- Clarify that the settlement resolves the full balance: Ensure that the agreed amount satisfies the entire debt and that no remaining balance will be pursued later.

Negotiation is not about getting the lowest number possible. It is about reaching a final, enforceable resolution.

Step 4: Get the Agreement in Writing Before Paying

This is one of the most critical steps, and one of the most commonly overlooked. Verbal agreements do not protect you.

- Ensure the agreement includes all key details: This should cover the settlement amount, payment schedule, due dates, and confirmation that the account will be considered resolved.

- Look for explicit language about account closure: The document should clearly state that the agreed payment satisfies the debt in full.

- Do not rely on verbal assurances or informal communication: Without written confirmation, there is no guarantee that the terms will be honored or recorded correctly.

- Review the document carefully before proceeding: Take time to ensure everything aligns with what was discussed and agreed upon.

Without written confirmation, there is no enforceable record of the agreement, which can lead to disputes even after payment.

Step 5: Make Payment Securely and Keep Complete Records

Once the agreement is finalized, the focus shifts to completing the transaction safely and maintaining documentation.

- Use secure and traceable payment methods: Payments should be made through official channels that provide confirmation, avoiding informal or unverifiable methods.

- Avoid sharing unnecessary financial access: Do not provide full banking credentials or open-ended authorization. Limit access to the specific transaction.

- Keep detailed records of everything: Maintain copies of the agreement, payment receipts, confirmation emails, and any related communication.

- Verify that the account is updated after payment: After completing the payment, check that the account reflects the agreed resolution and that no further action is required.

Proper documentation ensures that your settlement is not only completed, but also protected.

If your account is being managed by The Forest Hill Management, the process is designed to be clear, structured, and respectful of your situation. You are provided with accurate account information, transparent communication, and defined repayment options so you can make informed decisions without uncertainty.

Rather than navigating the process on your own, you have a point of contact to clarify details, understand your options, and move toward resolution in a way that fits your financial position.

Important Things to Know Before Settling Debt

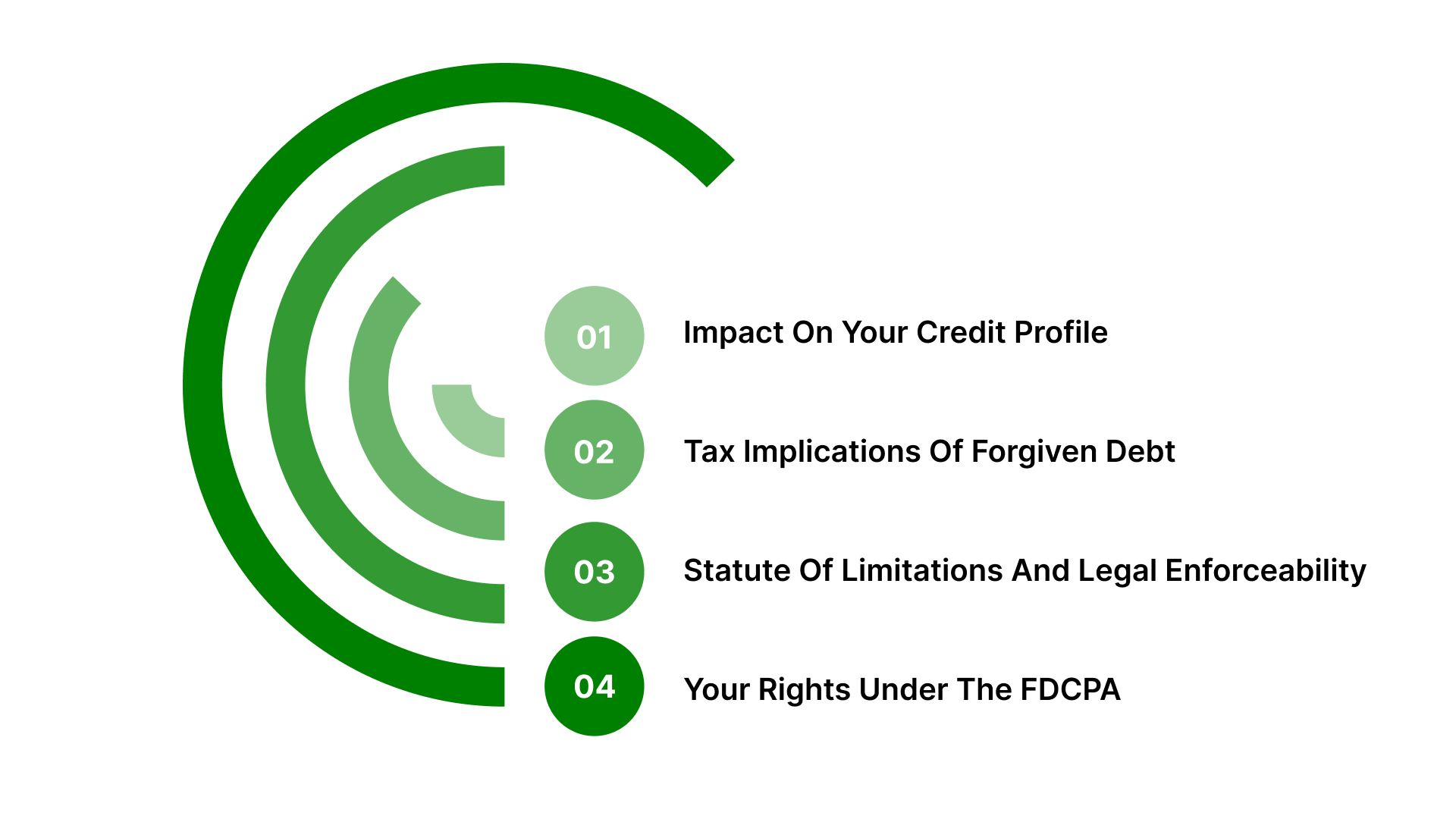

Debt settlement is not just a financial decision. It also comes with credit, legal, and tax implications that can affect you beyond the immediate resolution. Before agreeing to any terms, it is important to understand how each of these factors plays a role so you can move forward with clarity and avoid unintended consequences.

Impact on your Credit Profile

Settling a debt does not affect your credit the same way as paying it in full, and the account may be marked as “settled” rather than “paid in full,” which can influence how it appears in your credit history.

While it is not a neutral outcome, it is generally more favorable than leaving the debt unpaid or in collections. Over time, its impact depends on your overall credit behavior and how you manage other financial obligations moving forward.

Possible Tax Implications of Forgiven Debt

If a portion of your debt is forgiven during settlement, it may be treated as taxable income by the Internal Revenue Service (IRS). You may receive a Form 1099-C reflecting the canceled amount, which could be included in your taxable income for that year.

However, there are exceptions in certain cases, such as financial hardship or insolvency, where the forgiven amount may not be taxed if properly documented.

Statute of limitations and legal enforceability

Debt is subject to a statute of limitations that varies by state, meaning older debts may become “time-barred” and no longer legally enforceable through court action.

It is important to verify the age and status of the debt before making any payment, as even a small payment or acknowledgment can reset this timeline and potentially reopen the possibility of legal action.

Your Rights under the FDCPA

Under the Fair Debt Collection Practices Act (FDCPA), you are protected from harassment, misleading statements, and unfair collection practices.

Collectors are required to provide accurate information, clearly identify the debt, and communicate in a respectful and transparent manner. You also have the right to request written validation and dispute the debt if something does not appear correct.

Understanding these aspects ensures that settling a debt is not just about reaching an agreement, but about doing so in a way that is informed, protected, and aligned with your broader financial situation.

Conclusion

Debt settlement often feels uncertain at the start because the process is not always explained clearly. Once you understand how to verify the account, assess what you can afford, and formalize the agreement properly, the situation becomes much more straightforward.

This is not about negotiating aggressively or trying to reduce a number without context. It is about reaching a resolution that is accurate, documented, and realistic for your situation. When each step is handled correctly, you move from uncertainty to closure without unnecessary setbacks.

If your account is being managed by The Forest Hill Management, you are not expected to navigate this process alone. With clear account details, transparent communication, and structured repayment options, you have a defined path to resolve your balance in a way that works for you.

Take the first step toward financial freedom.

FAQs

1. Can I negotiate with a collection agency more than once on the same debt?

Yes, in some cases, negotiations can continue or be revisited if circumstances change, but this depends on the agency’s policies and the status of the account.

2. Will settling a debt stop all communication from collectors immediately?

Once a settlement agreement is completed and the account is resolved, communication typically stops, but it is important to confirm closure in writing.

3. Can I handle debt settlement on my own without third-party help?

Yes, many people handle settlement directly by following the correct steps, as long as they understand their rights and document everything properly.

4. What happens if I miss a payment after agreeing to a settlement plan?

Missing a payment can void the agreement, depending on the terms, and may restart the collection process or change the settlement conditions.

5. Is it better to settle one debt at a time or multiple debts together?

Focusing on one account at a time is often more manageable, as it allows you to fully resolve each debt without overextending your financial capacity.