Fundamentals of Debt Portfolio Composition for Creditors

Transform Your Financial Future

Contact UsEvery receivable portfolio carries its own mix of risk and recovery potential, but not every institution understands how that mix affects results. According to S&P Global (2025), recovery rates for stressed U.S. auto-loan receivables ranged between 67% and 75% of their original exposure.

This serves as a clear reminder that portfolio structure has a direct impact on performance. Knowing your portfolio composition is essential. It defines a portfolio’s value, shapes pricing strategy, and determines how consistently receivables perform over time.

This guide explains what portfolio composition is, how to analyze it, and why lenders and debt collectors rely on it to manage receivables with precision and compliance.

At a glance:

- Portfolio composition defines structure and value. It outlines how receivables are distributed by product type, balance, delinquency, and geography. You can get a clear view of a portfolio’s risk and recovery potential with composition analysis.

- Segmentation transforms data into insight. Dividing portfolios into behavioral, risk-based, or product-level categories helps institutions identify patterns, forecast outcomes, and allocate resources effectively.

- Accurate analysis drives better decisions. Regular analysis of composition supports fair valuation, informed acquisitions, and more predictable recovery strategies across all stages of the debt lifecycle.

- Weaknesses often stem from data or concentration risks. Poor data quality, limited diversification, and outdated models are common pitfalls that can distort portfolio value and compliance accuracy.

- Strategic application ensures long-term stability. Using composition insights to guide acquisition, rebalancing, and recovery decisions helps institutions maintain balanced portfolios and sustainable performance.

What Is Portfolio Composition?

Portfolio composition refers to the structural breakdown of a receivable portfolio. It is the way its debts are distributed by type, size, age, and security. It reveals how risk, recovery potential, and value are spread across the accounts that make up the whole.

Portfolio composition can help you evaluate what a portfolio is truly worth, how stable its performance may be, and what kind of management approach it requires.

These are the key elements in portfolio composition:

- Account Type and Product Mix

- Identifies the kinds of receivables included, such as consumer credit, small business loans, credit cards, auto loans, or utilities. Each type carries different levels of volatility, default behavior, and recovery cost.

- Delinquency and Charge-Off Age

- Tracks the timeline of overdue accounts and their stage of delinquency (for example, 30, 60, or 90+ days past due). The older the account, the lower its expected recovery value and the higher its risk.

- Balance Distribution and Concentration

- Shows how receivables are weighted across accounts. For instance, are most balances small and dispersed or concentrated in a few significant exposures? The concentration of accounts increases portfolio sensitivity to individual defaults.

- Geographic and Demographic Spread

- Evaluates how borrower characteristics or location impact repayment. Broader geographic and demographic diversity reduces systemic risk tied to local or sector-specific conditions.

- Collateralization and Security

- Measures how much of the portfolio is secured versus unsecured. Secured assets offer higher recovery potential and influence overall portfolio valuation.

- Historical Recovery Performance

- Assesses how similar portfolios or prior vintages performed in recovery. Strong historical performance often signals predictable cash flow and better pricing potential.

A well-defined portfolio composition provides a clear picture of what drives portfolio behavior. It reveals the amount owed, the likelihood, timing, and cost of repayment.

Understanding these elements is only the first step. The next step is to realize why portfolio composition matters in debt management. In the next section, we examine how these structural details influence valuation, compliance exposure, and long-term recovery outcomes.

Suggested Read: What is Credit Management? A Complete Guide

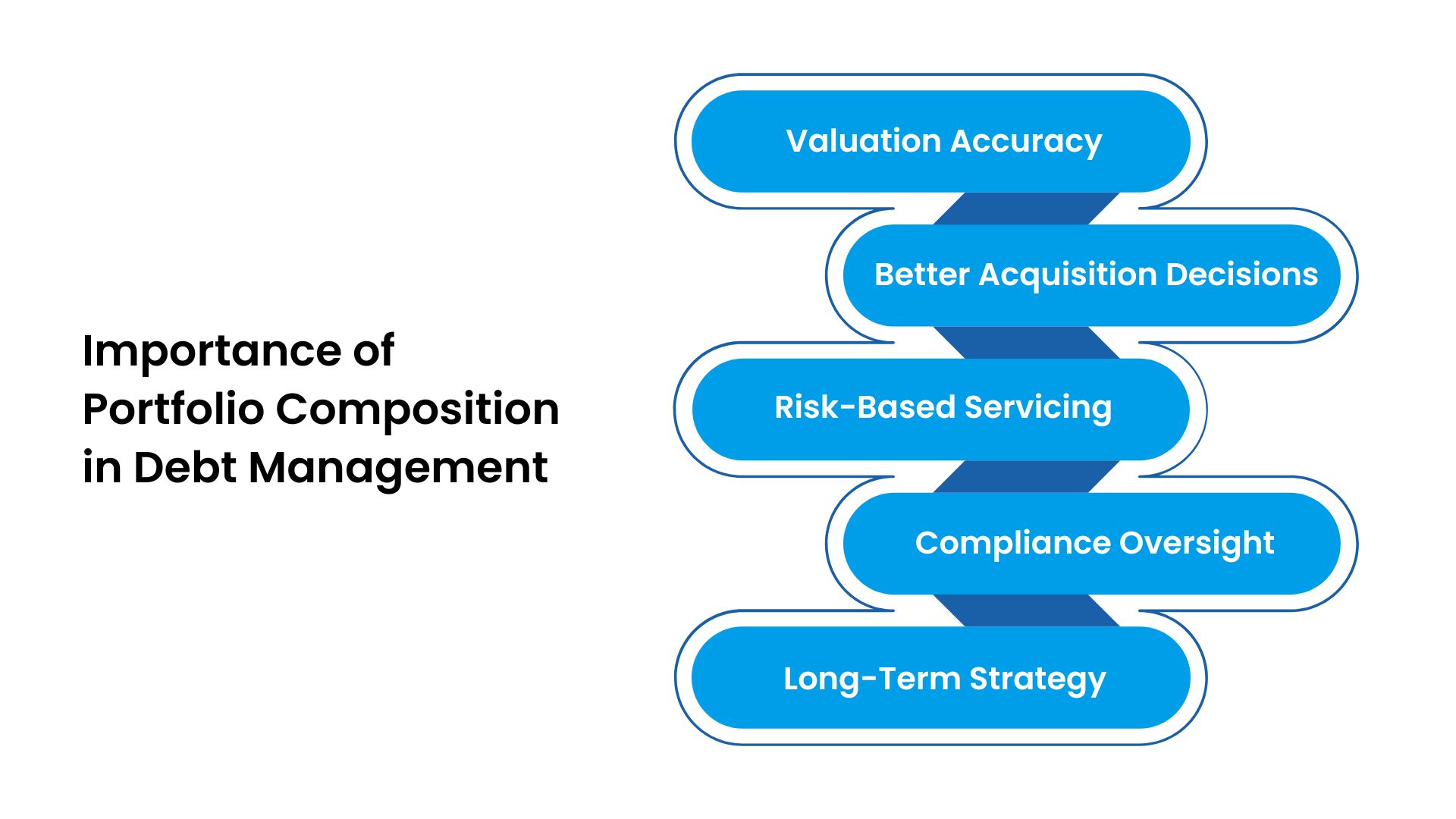

Importance of Portfolio Composition in Debt Management

Portfolio composition is a decision-making tool. For lenders, investors, and creditors, understanding how a portfolio is built helps determine how it should be managed, priced, and optimized.

When composition is mapped accurately, it gives institutions control over risk, compliance, and recovery outcomes instead of leaving those factors to chance.

This is how portfolio composition strengthens debt management:

- Improves Valuation Accuracy: A clear view of balance distribution, account age, and security status allows lenders to calculate fair value based on realistic recovery expectations—not assumptions.

- Supports Better Acquisition Decisions: Creditors can identify underperforming portfolios or segments before purchase. This can prevent overvaluation and align the acquisition strategy with the actual recovery potential.

- Enables Risk-Based Servicing: By segmenting accounts according to delinquency, product type, or geography, companies can tailor recovery strategies and resource allocation more effectively.

- Enhances Compliance Oversight: Understanding portfolio composition helps institutions identify areas with elevated regulatory exposure and apply the proper frameworks for documentation and data security.

- Guides Long-Term Strategy: Composition analysis reveals which segments generate steady returns versus those that require restructuring, enabling more predictable performance and portfolio rebalancing.

Forest Hill Management helps clients apply these insights through precise portfolio analysis, acquisition support, and compliance-driven oversight. Our specialists combine financial modeling with regulatory understanding to ensure every receivable asset is priced and managed for performance. Contact us today to improve valuation accuracy.

In the next section, we examine how structured segmentation converts raw debt data into an actionable strategy.

Suggested Read: How to Win Debt Collection Disputes: A Complete Step-by-Step Guide

Portfolio Segmentation Models in Debt Composition

Segmentation is the process of dividing receivables into meaningful groups based on shared characteristics. Well-designed segmentation models allow institutions to identify high-yield segments, minimize losses, and allocate resources more efficiently.

These are the most commonly used models in debt portfolio management.

1. Behavioral Segmentation

Behavioral segmentation categorizes receivables based on how borrowers respond to repayment obligations. It helps institutions predict repayment likelihood and tailor collection strategies accordingly.

Key indicators often include:

- Payment Activity: Frequency or recency of payments after delinquency.

- Communication Response: Engagement with reminders or settlement offers.

- Settlement Patterns: Willingness to negotiate partial or full repayment.

For instance, a lender may find that borrowers making partial payments within 60 days of delinquency are 2.5x more likely to settle. Using this insight, the company can prioritize those accounts for early, personalized outreach.

2. Risk-Based Segmentation

This model classifies receivables based on credit exposure, probability of default, and expected loss. It helps lenders assign resources according to risk level and comply with frameworks such as IFRS 9 or CECL.

Key factors include:

- Credit Risk Score: Quantifies default probability.

- Loss Given Default (LGD): Measures the expected unrecoverable amount.

- Exposure at Default (EAD): Determines potential financial impact.

Using this segmentation, a company can apply aggressive recovery strategies to high-risk segments while maintaining cost efficiency across stable portfolios.

3. Demographic and Geographic Segmentation

Demographic and geographic segmentation divides receivables by borrower characteristics or regional trends. This helps identify variations in repayment behavior resulting from differences in income levels, employment sectors, or local economic conditions.

Typical segmentation criteria include:

- Region or State: Differences in regulation or payment culture.

- Income and Occupation: Correlation between income stability and recovery rate.

- Market Exposure: Concentration risk within a single demographic group.

For example, a debt collector can adjust pricing or collection strategies based on stronger repayment performance in specific states or customer segments.

4. Product or Asset-Type Segmentation

This model organizes portfolios according to the nature of the underlying receivable, such as auto loans, credit cards, or small business accounts. Each product type carries its own recovery pattern and regulatory environment.

Segmentation categories typically include:

- Asset Class: Consumer, commercial, or utility receivables.

- Servicing Complexity: Effort and cost to manage recoveries.

- Regulatory Requirements: Specific compliance standards by asset type.

By segmenting at the product level, institutions can design specialized strategies for each asset category, improving both compliance and recovery predictability.

5. Performance Segmentation

Performance segmentation divides receivables into performing, reperforming, and nonperforming categories. This method is essential for valuation and acquisition decisions, helping investors determine how much of a portfolio remains viable.

Key segmentation points include:

- Repayment Consistency: Timeliness and completeness of payments.

- Historical Behavior: Prior default or rehabilitation trends.

- Recovery Expectation: Likelihood of future repayment.

For example, identifying accounts that recently reentered payment plans allows investors to price those assets more favorably, balancing risk and opportunity.

Segmentation enables lenders to move beyond “what they hold” to “how it behaves” and “where value can be unlocked.”

In the next section, we examine how segmentation models are applied to real portfolio data to forecast recoveries, calculate fair value, and enhance compliance oversight.

Suggested Read: Understanding Objectives and Importance of Capital Markets

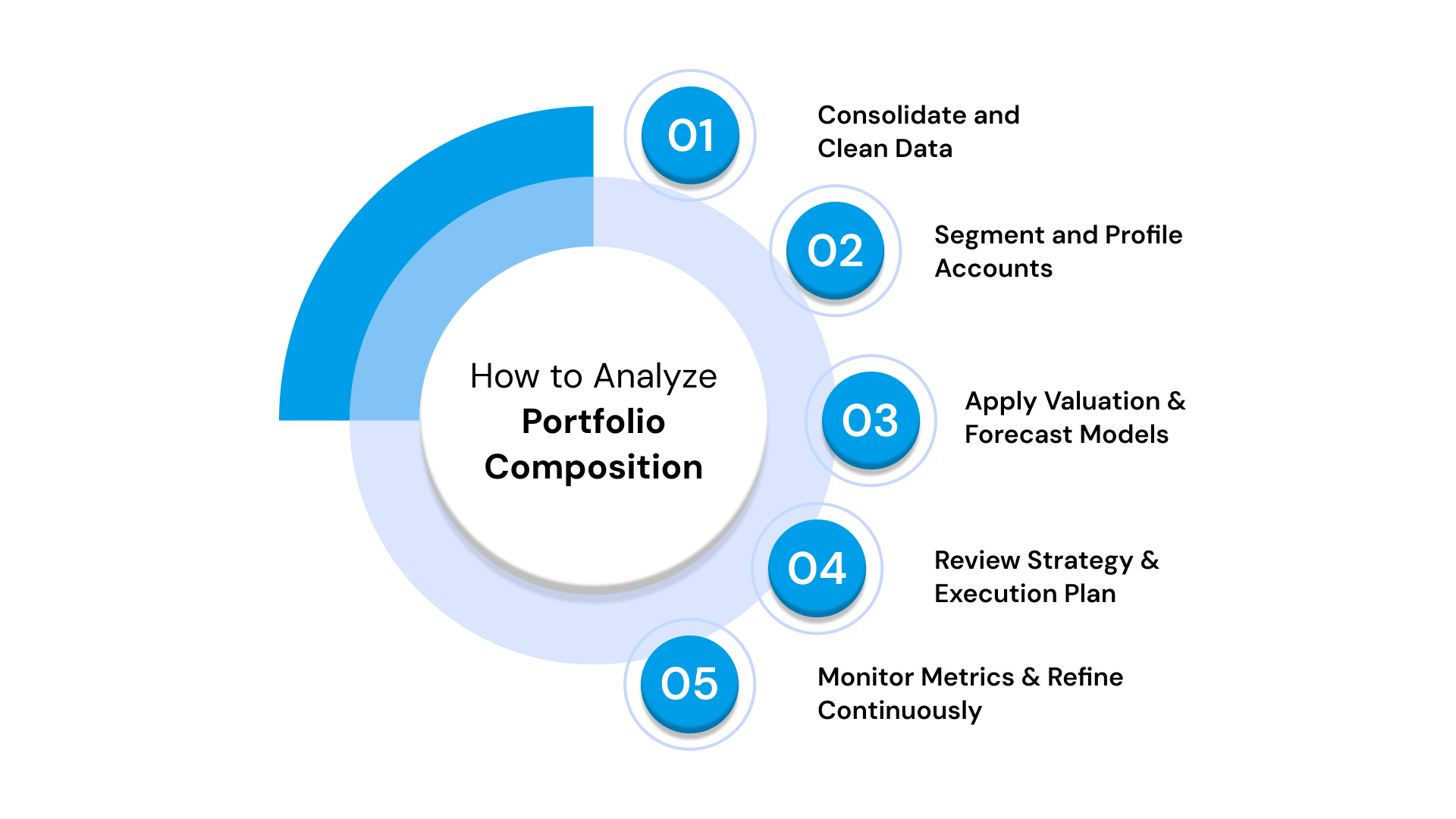

How to Analyze Portfolio Composition

An industry survey by McKinsey & Company and the International Association of Credit Portfolio Managers found that over 60% of institutions have increased their use of advanced data and analytics for credit-portfolio management in the past two years.

You can reap the benefits of portfolio composition analysis, too. All you need to do is follow these key steps:

- Consolidate and Clean Data: Combine all account-level details (balances, age, debtor history) into a unified dataset, and remove duplicates or invalid entries.

- Segment and Profile Accounts: Use criteria like product type, delinquency stage, and geography to group accounts and assess risk-return characteristics.

- Apply Valuation and Forecast Models: Estimate recovery potential, fair value, and expected credit loss (ECL) using historical and predictive data.

- Review Strategy and Execution Plan: Decide on hold, restructure, sell, or external service segments based on model results and operational capacity.

- Monitor Metrics and Refine Continuously: Track recovery rate, write-off ratio, and portfolio yield, and adjust modeling assumptions or strategy as behavior evolves.

This step-by-step approach ensures you move from data to insight to action. In the following section, we look at how composition and analysis translate into operational impact.

Suggested Read: Portfolio Revision: Why it’s Essential and How to Do it?

Applications of Portfolio Composition Across the Debt Lifecycle

By applying composition insights across the debt lifecycle, you can anticipate market shifts, optimize asset allocation, and strengthen portfolio resilience. In a volatile credit environment, a strategy built on composition insight leads to better timing, smarter pricing, and stronger returns.

This is how product composition can be useful to you:

- Portfolio Origination and Structuring: Composition data enables institutions to design lending portfolios that align with their risk appetite, capital requirements, and regulatory limits. It enables leaders to shape a product mix that supports long-term balance-sheet strength rather than short-term yield.

- Dynamic Portfolio Rebalancing: By monitoring how composition evolves, such as a rising share of nonperforming assets or regional concentration, you can rebalance early, shifting exposure before performance declines.

- Capital and Liquidity Planning: Composition informs funding allocation, liquidity buffers, and provisioning levels under frameworks like CECL and Basel III. Understanding asset quality helps align capital with real risk.

- Data-Driven Recovery Planning: Segmentation and composition trends reveal where to apply intensive recovery strategies versus automated solutions—enabling smarter cost control and resource efficiency.

- Investor and Stakeholder Reporting: Transparent reporting on portfolio composition builds confidence among investors, regulators, and rating agencies by linking financial performance to measurable structural data.

Forest Hill Management will work with you to operationalize these strategies. We can turn these composition metrics into portfolio-wide actions. Our team integrates analytical insights into acquisition, rebalancing, and recovery strategies that strengthen both compliance posture and performance consistency. Get in touch with us today.

Suggested Read: Nature and Scope of Investment Analysis Explained

Common Weaknesses in Portfolio Composition

Weaknesses in portfolio composition often appear gradually. These structural issues can distort valuation, increase recovery costs, and limit portfolio scalability.

You need to recognize and address the following challenges early:

1. Data Integrity and Incomplete Records

Challenge: Missing or inconsistent data skews recovery forecasting and valuation accuracy. Without reliable account-level details, institutions struggle to evaluate true portfolio performance.

Fix: Implement automated data validation and reconciliation systems before analysis. Regular data audits and digital documentation trails strengthen reliability and compliance reporting.

2. Overconcentration of Asset Types

Challenge: Heavy exposure to a single asset class, region, or borrower group increases systemic risk. Market shifts or localized economic events can disproportionately affect performance.

Fix: Utilize diversification thresholds within the portfolio strategy to limit exposure by geography, sector, or product. Rebalancing ensures a stable mix aligned with institutional risk appetite.

3. Outdated Recovery and Risk Models

Challenge: Static or outdated risk models fail to reflect current debtor behavior, inflation, or credit conditions. This leads to inaccurate forecasts and poor strategic timing.

Fix: Update recovery and valuation models quarterly, incorporating machine learning or behavioral analytics to capture real-time performance indicators.

4. Inconsistent Compliance Tracking

Challenge: When portfolios expand across regions or asset types, maintaining uniform compliance standards becomes complex. Minor oversights can escalate into costly violations.

Fix: Integrate compliance frameworks directly into portfolio segmentation and servicing workflows, ensuring consistent audit readiness and legal adherence across all segments.

5. Lack of Predictive Monitoring

Challenge: Relying solely on historical data limits foresight. Institutions miss early signals of underperformance or upcoming stress points.

Fix: Deploy predictive dashboards that highlight delinquency trends, segment stress levels, and portfolio correlations—allowing preemptive adjustments before losses intensify.

The solution lies in transforming composition data into a living framework. Forest Hill Management can help you continuously evolve in response to portfolio behavior, regulatory changes, and market shifts.

The next section examines how structured analysis, compliance integration, and active oversight work together to create resilient, high-performing portfolios founded on transparency.

Turn Strategy into Execution with Forest Hill Management

At Forest Hill Management, we specialize in turning debt portfolio analysis into measurable results. We help lenders, investors, debt collectors, and other financial institutions convert raw receivable data into actionable strategies.

Our approach combines analytical precision, operational control, and regulatory insight. We bridge the gap between knowing your portfolio and managing it strategically. Through continuous analysis, segmentation, and performance tracking, we ensure every decision is aligned with long-term objectives.

These are a few reasons to choose us:

- Data-Led Decision-Making

- We translate portfolio composition into clear financial insight, helping clients price, acquire, and manage receivable assets with measurable confidence.

- Customized Analytical Frameworks

- Our solutions are tailored to each client’s portfolio structure, ensuring that analysis, forecasting, and compliance processes fit unique operational realities.

- Integrated Compliance Oversight

- Compliance is embedded at every stage, from data intake to servicing, to reduce regulatory exposure and strengthen audit readiness.

- Operational Optimization

- We streamline workflows, align technology with portfolio type, and enhance team productivity through data-backed segmentation strategies.

- Lifecycle-Based Strategy

- Our methodology spans the full debt lifecycle—acquisition, servicing, recovery, and exit—so clients maintain consistency, transparency, and value across all stages.

At Forest Hill Management, portfolio composition is not just a diagnostic exercise. It is a strategy for sustainable performance. By merging data science with regulatory expertise, we enable organizations to move from analysis to execution with confidence.

Conclusion

Product composition reveals the true structure of a receivable portfolio. It helps institutions identify risk concentration, forecast recoveries accurately, and comply with evolving regulatory expectations. Whether you are acquiring, servicing, or selling debt, a clear view of composition ensures that every decision is strategic and defensible.

Forest Hill Management can help you bring this clarity to life. Our team combines data intelligence and compliance expertise to transform static portfolio data into measurable performance outcomes. We align analysis with execution to ensure that every receivable asset is managed for value, compliance, and control.

Start managing your receivables with foresight and measurable performance today. Speak to our financial advisor.

Frequently Asked Questions

1. How often should portfolio composition be reviewed or updated?

Portfolio composition should be reviewed at least quarterly for active portfolios and before any major transaction, such as an acquisition or sale. Market conditions, borrower behavior, and regulatory changes can shift portfolio dynamics quickly—frequent reviews help institutions stay ahead of risk.

2. What tools or technologies are most effective for analyzing portfolio composition?

Advanced analytics platforms, AI-based segmentation tools, and data visualization dashboards like Power BI or Tableau are commonly used. Many institutions also integrate predictive modeling tools and automated validation systems to improve accuracy and reduce manual workload.

3. How does portfolio composition affect regulatory capital requirements?

Under frameworks such as Basel III and CECL, composition directly impacts the amount of capital that must be reserved for potential losses. Portfolios with higher-risk segments, like unsecured or delinquent accounts, require greater provisioning, while diversified portfolios may qualify for lower reserves.

4. Can portfolio composition help identify new investment opportunities?

Yes. Composition analysis can reveal underexposed segments or regions with strong recovery trends. Lenders and investors often use this insight to expand selectively—targeting asset types or borrower groups that deliver stable yields with manageable risk.

5. What are the biggest challenges in maintaining accurate portfolio composition data?

Common challenges include inconsistent data formatting from multiple sources, a lack of real-time updates, and incomplete account-level documentation. Establishing a centralized data system and standardized reporting framework can significantly improve accuracy and compliance readiness.