Guide to Debt Portfolio Analysis: Definition and Compliance

Need Help Reviewing Your Account?

Contact UsBad debt is growing faster than many companies can track. Recent data shows the global market for bad-debt forecasting tools is already worth over US $1.8 billion and is expected to reach US $5.6 billion by 2033. That growth is not driven by optimism, but by necessity.

Every debt portfolio now carries two responsibilities: accurate analysis and regulatory compliance. Knowing what a portfolio is truly worth, how much risk it carries, and whether it meets legal and reporting standards has become a full-time discipline.

For lenders, investors, and servicing firms, this discipline defines profitability, transparency, and trust. This guide breaks down the portfolio analysis definition, explains why it matters, and outlines how compliance fits into every stage.

Quick look:

- Debt portfolio analysis is the foundation of financial control. It helps institutions understand the composition, value, and risk of their receivables, turning scattered account data into actionable financial insight.

- A structured process ensures accuracy and compliance. From data aggregation and segmentation to valuation, forecasting, and monitoring, each step ensures portfolios are managed with transparency and regulatory discipline.

- Management style shapes portfolio outcomes. Active, passive, or hybrid approaches define how frequently portfolios are reviewed, adjusted, and optimized for performance and compliance stability.

- Compliance is non-negotiable. Adhering to frameworks like FDCPA, GLBA, and GDPR safeguards data integrity, protects consumer rights, and preserves institutional reputation.

- Sustainable debt portfolio management requires continuous oversight. Regular reviews, data validation, and adaptable strategies help institutions maintain accuracy, reduce risk, and ensure long-term portfolio stability.

What Is Debt Portfolio Analysis?

Debt portfolio analysis is the structured process of evaluating all receivable or debt assets to understand their composition, risk, and recoverable value. It helps institutions measure performance, forecast recoveries, and maintain compliance with accounting and regulatory standards.

As the United Nations Conference on Trade and Development (UNCTAD) explains,

“Debt portfolio analysis examines the nature, composition and structure of an existing debt portfolio, reviewing past trends over a given period of time.”

- (UNCTAD DMFAS Programme)

At its core, the process converts large volumes of financial data into a clear picture of portfolio health. It reveals which assets are performing, which are risky, and how overall value can be protected or improved.

These are the key components:

- Portfolio Composition: Examines the mix of receivable types, such as consumer loans, credit cards, auto loans, and business credit. It distinguishes between performing, reperforming, and non-performing assets. A balanced composition reduces volatility and improves the predictability of returns.

- Aging and Delinquency Trends: Tracks how long accounts have been outstanding and how payment behavior changes over time. Aging analysis helps identify high-risk segments, project recovery potential, and plan collection strategies.

- Valuation Metrics: Determines the portfolio’s fair value and expected recovery rates based on factors such as payment history, charge-off age, and debtor profiles. It applies accounting models, such as Expected Credit Loss (ECL) under IFRS 9 or amortized cost under US GAAP.

- Risk Concentration: Evaluates how exposure is distributed across borrowers, geographies, or industries. A high concentration in one segment increases systemic risk; diversification protects overall performance.

- Data Integrity and Reporting Frameworks: Ensures data accuracy, consistency, and traceability. Strong reporting systems support investor confidence, regulatory compliance, and transparent performance audits.

Debt portfolios are financial assets that can be bought, sold, and traded like any other investment. Each portfolio represents a stream of future cash flows, and its market value depends on how reliably those cash flows can be expected to be realized.

Forest Hill Management specializes in helping clients unlock that value through accurate portfolio assessment, acquisition support, and ongoing performance management. Our team combines financial analysis with compliance oversight to ensure every receivable asset is priced, monitored, and serviced with precision. Contact us to start improving your portfolio returns today.

Terms in Debt Portfolio Analysis and Compliance

For quick reference, here are the essential terms and concepts used throughout this guide. Each plays a critical role in understanding how debt portfolios are analyzed, valued, and managed within compliance frameworks.

All this theory is useful, but how does it translate to your organization? What practical role does portfolio analysis play for lenders, servicers, and investors? Let us explore that next in the next section.

Suggested Read: Portfolio Revision: Why it’s Essential and How to Do it?

Why Do Debt-Related Companies Need Portfolio Analysis?

Portfolio analysis turns raw account data into something far more valuable—strategic insight. It provides lenders, investors, and servicers with a clear view of where value lies. It identifies risks that require attention and enables informed decisions across acquisition, management, and recovery.

For example, a recent study found that decision-tree models used in receivable classification achieved over 85% accuracy in predicting repayment patterns.

When done correctly, it transforms credit management from a reactive process into a data-driven performance strategy. These are the top benefits of performing a portfolio analysis:

- Informed Valuation: Helps determine the true worth of receivable assets by combining recovery forecasts, charge-off history, and fair-value accounting models. This prevents overpaying for portfolios and supports better pricing decisions.

- Enhanced Risk Visibility: Identifies which borrower segments, geographies, or product types carry the most exposure. This allows risk teams to rebalance portfolios before losses materialize.

- Optimized Recovery Strategies: Guides operational teams on where to focus collection efforts by highlighting high-probability accounts, optimal recovery timelines, and cost-efficient channels.

- Compliance and Audit Readiness: Ensures that all portfolio activities align with regulatory frameworks such as FDCPA, GLBA, and IFRS 9. Transparent documentation reduces legal exposure and builds stakeholder confidence.

- Performance Monitoring and Forecasting: Establishes measurable performance indicators, such as recovery rate, Days Sales Outstanding (DSO), and delinquency ratio, that can be tracked to improve long-term portfolio performance.

- Investor and Stakeholder Confidence: Provides decision-makers with consistent, verifiable data for building trust with investors, auditors, and regulators alike.

All of this matters because debt portfolios are living assets. Their value changes with time, behavior, and compliance performance. Without systematic analysis, even a strong receivable book can lose value quietly through untracked defaults or regulatory lapses.

Now that you know what portfolio analysis can achieve for your debt collections and investment decisions, the next step is understanding how the process actually works.

Suggested Read: Importance of Licensing for National Collection Agencies

The Process of Debt Portfolio Analysis

A strong debt portfolio analysis does not begin with assumptions; it begins with data. Every account record, no matter how small, holds insight into payment behavior, recovery probability, and long-term asset value. The challenge lies in turning that raw data into actionable direction.

Below is a detailed look at how a structured debt portfolio analysis typically unfolds:

1. Data Aggregation and Cleansing

The process begins by consolidating all receivable data—balances, delinquency age, payment history, collateral details, and borrower demographics into a single, unified dataset. Cleansing removes duplicates, fills data gaps, and validates entries for accuracy and completeness. This step ensures the analytics that follow are based on reliable inputs, not assumptions.

Once data aggregation is complete, the next step is segmentation, grouping accounts by shared risk or behavior.

2. Segmentation and Risk Profiling

Once data is clean, accounts are segmented into logical groups such as product type (auto, credit card, small business), risk grade, region, or charge-off age. Each segment is then profiled for payment likelihood, historical recovery, and regulatory exposure.

3. Valuation and Forecasting

At this stage, advanced statistical models and accounting standards, such as Expected Credit Loss (ECL) under IFRS 9 or fair value measurement under US GAAP, are applied. Forecasting estimates the present value of future cash flows, incorporating recovery curves, discount rates, and write-off probabilities. The result is an accurate view of the portfolio’s market worth and performance potential.

4. Strategy Formulation and Execution

Insights from the valuation stage guide actionable decisions—whether to hold, restructure, outsource servicing, or sell portions of the portfolio. Strategies are developed for each segment, aligning recovery targets, operational resources, and compliance requirements. Execution might involve automation in low-risk segments and manual handling for complex or high-value accounts.

5. Monitoring and Continuous Refinement

Finally, performance metrics such as Recovery Rate, Days Sales Outstanding (DSO), and Portfolio Yield are tracked regularly. Ongoing monitoring ensures that changes in debtor behavior or market conditions trigger timely strategic adjustments. Periodic compliance audits and stress tests help maintain both financial accuracy and regulatory integrity.

Forest Hill Management integrates each of these steps into a unified analytical framework. Our team ensures data accuracy at the source, interprets valuation metrics through a compliance lens, and continuously adjusts strategy based on live performance data. Learn more about how we can help you in our FAQs.

Now that you understand how portfolio analysis works in practice, the next step is to see how different management styles can shape your long-term outcomes.

Suggested Read: Understanding the Phases of the Portfolio Management Process

Types of Debt Portfolio Management

Every receivable portfolio operates under a management style that defines how decisions are made, how often strategies are adjusted, and how actively performance is monitored.

Much like investment portfolios, debt portfolios require a structured management approach to balance return, risk, and regulatory control. The chosen management type influences everything from how quickly defaults are addressed to how compliance responsibilities are distributed within an organization.

These are the primary types of debt portfolio management:

- Active Management

Involves continuous monitoring, revaluation, and tactical decision-making. Managers frequently adjust recovery strategies, pricing models, and portfolio composition based on market changes, debtor behavior, or new compliance requirements. This approach suits portfolios with volatile performance or high-risk exposure.

- Passive Management

Focuses on stability and predictable returns. Portfolios are held with minimal intervention, relying on steady repayment behavior and long-term value. Passive management works best for low-risk or mature portfolios with consistent payment patterns and established controls.

- Hybrid Management

Combines active oversight with long-term positioning. Institutions may actively manage high-risk or newly acquired segments while maintaining passive management for stable portfolios. This model provides flexibility, which is essential for balancing profitability with operational efficiency.

Flexibility in management style is only part of the equation. Institutions must also determine who holds decision-making authority.

Discretionary vs. Non-Discretionary Management

In discretionary management, the portfolio manager, such as Forest Hill Management, is given full authority to make operational and strategic decisions. This includes debt restructuring, asset sales, or compliance adjustments. This setup ensures rapid execution and professional oversight.

In contrast, non-discretionary management keeps decision-making power with the client, while the manager provides analysis, reporting, and recommendations. This model is common among institutional investors that prefer retaining final control over portfolio actions.

In debt management, performance means little without compliance. You need to understand the necessary regulations and frameworks that can impact your portfolio oversight.

Suggested Read: Steps to Economically Profitable Portfolio Acquisitions

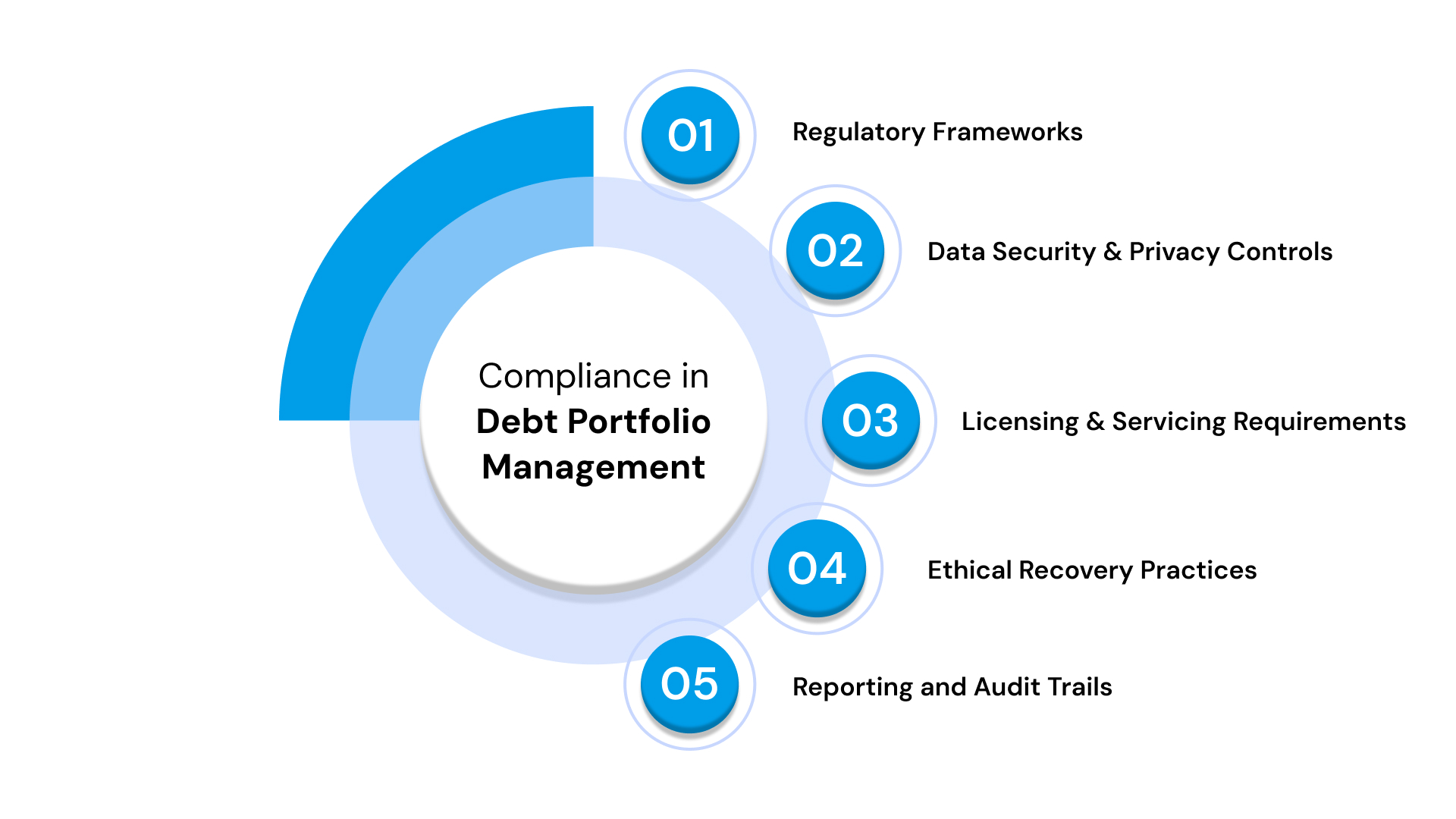

Compliance in Debt Portfolio Management

Every collection, valuation, and transfer of receivables must follow laws that protect data privacy, consumer rights, and investor transparency. Compliance is about maintaining the integrity of financial reporting and building trust with regulators, investors, and clients.

These are the key areas of portfolio analysis compliance:

- Regulatory Frameworks

Adherence to laws such as the Fair Debt Collection Practices Act (FDCPA), Gramm–Leach–Bliley Act (GLBA), and General Data Protection Regulation (GDPR) for international transactions. These standards govern how receivables are collected, processed, and reported.

- Data Security and Privacy Controls

Implementation of encryption, restricted data access, and secure transmission systems in compliance with PCI DSS and other security standards. Protecting debtor data is both a legal requirement and an ethical obligation.

- Licensing and Servicing Requirements

Ensuring all servicing and recovery activities are carried out by licensed professionals and agencies authorized within their jurisdictions. Non-compliance here can invalidate collections or result in legal action.

- Ethical Recovery Practices

Upholding consumer protection standards by avoiding aggressive or misleading collection tactics. Compliance ensures recovery efforts remain lawful, transparent, and reputation-safe.

- Reporting and Audit Trails

Maintaining accurate documentation of account activity, valuation adjustments, and payment histories for internal audits and external reviews. This transparency strengthens institutional governance and investor confidence.

Compliance may feel procedural, but it is deeply strategic. A single oversight, such as a misclassified account or unverified third-party data feed, can expose an entire portfolio to legal and financial risk.

This brings us to the next section, where we examine how minor lapses in analysis or compliance controls can result in substantial operational and reputational harm.

Suggested Read: Portfolio Expansion Strategies Through Acquisition

Vulnerabilities in Debt Portfolio Assessment

Even the most sophisticated analysis can fall short if a single assumption or dataset is flawed.

Consider this example: a mid-sized debt buyer acquires a multi-million-dollar receivable portfolio based on outdated payment data. Six months later, actual recoveries fall 30% below projections because several large accounts were already written off by the originator.

The result? Overvaluation, compliance exposure, and investor distrust—all due to gaps in verification and reporting.

Such scenarios highlight why accuracy, validation, and governance are the foundation of debt portfolio assessment.

Table showing common errors and the corrective measures that prevent them.

Even minor weaknesses in portfolio assessment can cascade into significant financial and legal consequences. The key is prevention—building assessment frameworks that are resilient, transparent, and adaptable.

Use these best practices across all stages of the debt portfolio assessment:

- Verify all data sources before integration.

- Update risk and valuation models quarterly.

- Audit compliance documentation routinely.

- Stress-test recovery projections under multiple economic scenarios.

- Maintain transparency with investors and regulators.

- Use predictive analytics for early risk detection.

When accuracy, compliance, and foresight converge, vulnerabilities become opportunities for control and optimization. This is where a trusted partner makes all the difference. You need a firm that can unify analytics, compliance, and strategy. Forest Hill Management bridges these elements to deliver secure, high-performing debt portfolios.

Debt Portfolio Management for Long-Term Stability

At Forest Hill Management, we believe debt portfolios deserve the same strategic attention as any other investment class. Our role is to help financial institutions, investors, and service providers turn receivables into reliable, compliant, and high-performing assets.

We bring together financial analysis, regulatory oversight, and technology-backed processes to ensure that every portfolio, whether performing or distressed, is managed with accountability.

Forest Hill Management’s framework is built on the same principles discussed throughout this guide: data integrity, valuation accuracy, compliance, and long-term portfolio resilience. By integrating these pillars, we create a measurable impact for clients managing complex receivable assets.

These are our core services:

- Portfolio Analysis and Valuation

We assess receivable portfolios for performance, risk, and fair value, using advanced modeling to forecast recoveries and inform acquisition decisions.

- Portfolio Acquisitions and Transitions

We support the seamless purchase or transfer of debt portfolios, ensuring due diligence, data verification, and compliance with regional and international standards.

- Compliance and Regulatory Management

We embed legal, ethical, and data protection frameworks into every step of debt servicing, ensuring alignment with FDCPA, GLBA, GDPR, and other governing bodies.

- Performance Monitoring and Reporting

We track key performance indicators across recovery, valuation, and compliance, providing clients with transparent, data-backed insights for better decision-making.

Every portfolio tells a story of value, responsibility, and recovery potential. Our job is to make that story sustainable.

We provide simple portfolio acquisitions to ease the burden on businesses with delinquent accounts, while offering portfolio holders a fair and compliant way to settle their obligations. Through disciplined analysis and ethical management, we help institutions turn receivables into long-term financial assets built for stability.

Conclusion

As regulatory expectations tighten and recovery patterns become more unpredictable, understanding the true value and risk of receivable assets has become a critical component of financial stability. Yet, managing these portfolios in-house demands constant oversight, regulatory fluency, and advanced analytics that few organizations can sustain on their own.

Outsourcing debt portfolio management to a specialized partner allows businesses to maintain focus on their core operations. This is while ensuring the assets are analyzed, valued, and recovered with accuracy and compliance.

Forest Hill Management provides that level of expertise. We combine financial intelligence, technology-driven oversight, and a strong compliance framework to help clients manage receivables as strategic investments. Speak to our advisors today to explore personalized debt portfolio solutions built around accuracy, compliance, and performance.

Frequently Asked Questions

1. What types of organizations benefit most from debt portfolio management?

Debt portfolio management benefits any organization that holds or acquires receivables, such as banks, credit unions, private lenders, collection agencies, utility providers, and investors in distressed assets. It helps them recover funds more efficiently, stay compliant, and make better acquisition or divestment decisions.

2. How often should a debt portfolio be reviewed or revalued?

Most institutions conduct a quarterly review for high-volume or high-risk portfolios and an annual revaluation for stable or passive ones. However, any major change—such as shifts in interest rates, regulation, or recovery trends—should trigger an interim review to maintain fair-value accuracy.

3. What role does technology play in portfolio analysis and compliance?

Modern portfolio analysis relies heavily on technology. Predictive analytics, AI-driven segmentation, and automated audit trails make it possible to assess risks faster, detect compliance issues earlier, and generate transparent reporting for regulators and investors.

4. Can a company sell only part of its debt portfolio?

Yes. Many institutions opt for partial portfolio sales to free up liquidity or reduce exposure to specific risk segments. Forest Hill Management assists clients in structuring such transactions, ensuring that asset valuation, data integrity, and compliance requirements are met during the transition.

5. What are the indicators of a strong debt portfolio management partner?

Key indicators include transparent reporting, data security compliance (PCI DSS, GDPR), proven analytical capability, regulatory experience, and clear recovery performance metrics. A strong partner, such as Forest Hill Management, also prioritizes ethical collection practices and long-term portfolio sustainability.