What Is Portfolio Risk? Types, Management & Assessment Guide

Transform Your Financial Future

Contact UsYou work hard for your money. You make careful decisions about what you owe and what you own. But have you ever wondered what could go wrong with your debt obligations or receivables portfolios?

Portfolio risk is the possibility that your investments or debts could lose value or perform poorly. This happens due to market changes, economic shifts, or unexpected life events. Understanding this risk helps you protect what you have built and plan for a more secure future.

This risk affects many aspects of your financial life, including debt obligations and receivables portfolios, as well as investments. The good news is that you can manage it with the right knowledge and strategies.

This guide will explain what portfolio risk means in simple terms. You will learn about different types of risks, how to measure them, and practical ways to protect your financial future.

Key Takeaways:

- All portfolios carry risk in both investments and debt

- Different risk types need different management approaches

- Your risk tolerance guides appropriate strategy selection

- Diversification and asset allocation provide foundational protection

- Regular monitoring and adjustment maintain proper exposure

What Is Portfolio Risk?

Portfolio risk represents the chance that your financial holdings will lose value or fail to meet your expectations. This applies to both your investments and your debt obligations. Think of it as the uncertainty that comes with any financial decision you make.

Every portfolio carries some level of risk. The key is understanding what risks you face and how to manage them effectively.

Portfolio risk measures how much your financial situation could change due to factors outside your control. At its core, it helps you understand potential losses or setbacks.

Two sides of portfolio risk:

- Investment side: Your stocks, bonds, and mutual funds can rise or fall based on market conditions

- Debt side: Your credit cards, loans, and mortgages create obligations that shift with interest rates and income changes

The Risk-Return Relationship

This fundamental principle guides all financial decisions:

- Higher potential returns = Higher risk exposure

- Lower risk investments = Smaller expected gains

- Your goal = Finding the right balance for your situation

Understanding this helps you make informed choices. You can decide how much uncertainty you are comfortable with. You can also plan for different scenarios that might affect your finances.

Portfolio Risk in Different Contexts

Portfolio risk shows up in two main areas of your financial life. Both deserve your attention and careful management.

Investment Portfolio Risk

This covers your savings and investment accounts:

- 401(k) and IRA retirement accounts

- Brokerage accounts with stocks and bonds

- Mutual funds and exchange-traded funds

- Savings accounts and certificates of deposit

What can go wrong:

- Stock prices fluctuate daily based on company performance

- Bond values change when interest rates shift

- Market downturns reduce account balances

- Company failures can eliminate stock value entirely

Debt Portfolio Risk

This involves the money you owe and how you manage it:

- Credit card balances with variable interest rates

- Student loans are affecting the monthly cash flow

- Mortgage payments are consuming a significant income

- Personal loans and other obligations

What threatens stability:

- Rising interest rates increase payment amounts

- Job loss impacts your ability to meet obligations

- Medical emergencies derail repayment plans

- Income fluctuations create cash flow problems

The Connection Between Both

These two types of risk interact in critical ways:

Your overall financial health depends on managing both investment and debt risks. Strong performance in one area can offset challenges in another.

Also Read: Essentials of Business Portfolio Management Strategies

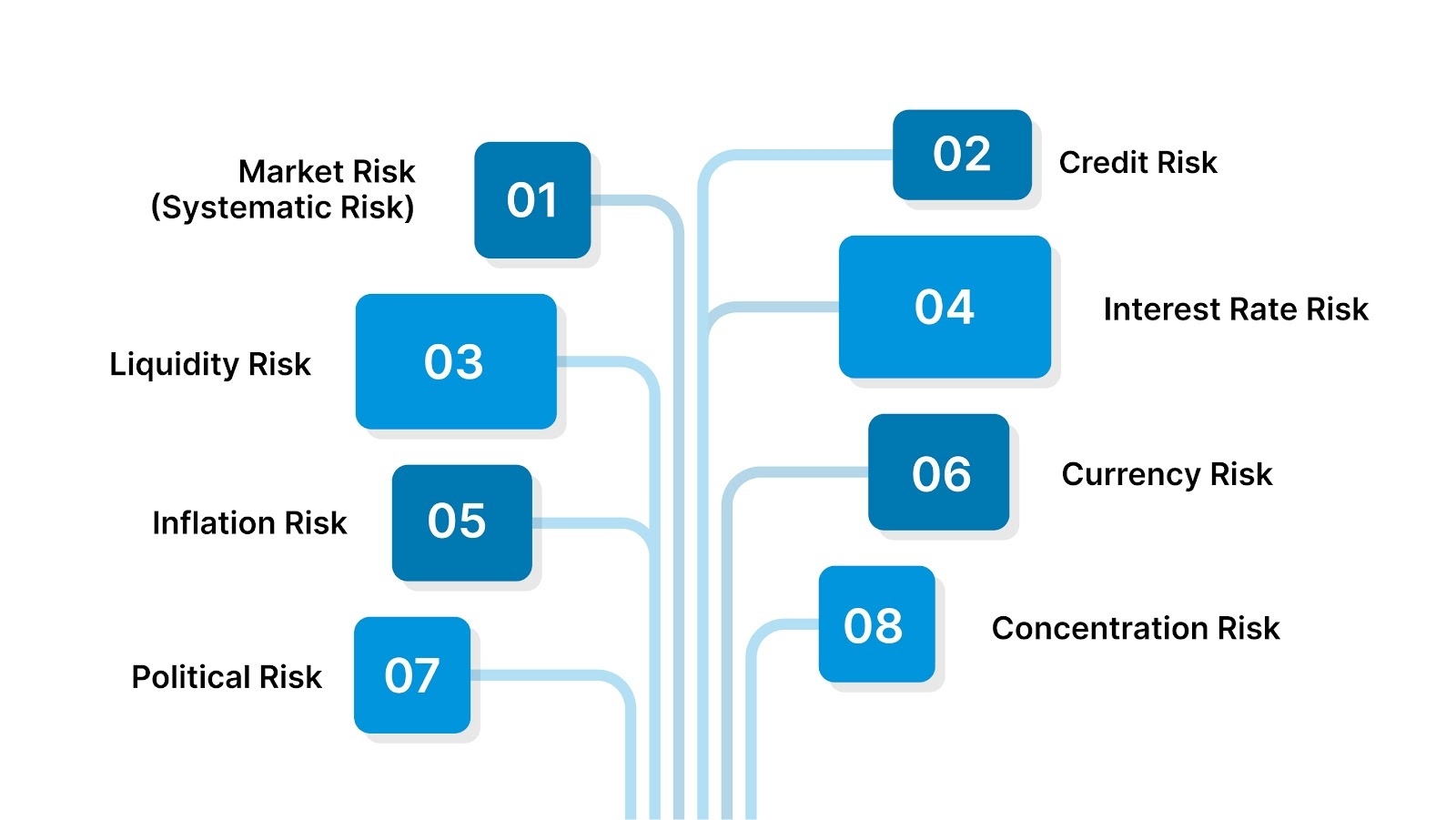

Types of Portfolio Risk You Need to Know

Different risks threaten your financial stability in unique ways. Recognizing each type helps you prepare and respond appropriately.

The following sections break down the most common portfolio risks. You will learn what each one means and how it might impact you.

1. Market Risk (Systematic Risk)

Market risk affects everyone who invests or carries debt. You cannot avoid it completely, but you can prepare for it.

What causes market risk:

- Economic recessions lower stock prices across all sectors

- Rising unemployment affects consumer spending patterns

- Inflation erodes your purchasing power

- Interest rate changes impact investments and borrowing costs

How it affects your investments:

Your portfolio value can drop even when individual companies perform well. Consider these scenarios:

- A strong tech company's stock falls during market-wide declines

- Your diversified portfolio loses value when entire markets struggle

- Bond prices decrease when interest rates rise

- Retirement accounts shrink during economic downturns

How it affects your debt:

Economic conditions create different challenges for debt management:

- Downturns threaten job security and income stability

- Rising rates increase monthly payments on variable-rate debts

- Inflation makes fixed payments feel more manageable but reduces overall wealth

- Credit availability tightens during economic stress

2. Credit Risk

Credit risk takes different forms depending on whether you are investing or managing debt. Both versions deserve your attention.

For Investors: Default Risk

When you buy bonds or debt instruments, you face the chance that issuers will fail to make payments.

Risk levels by investment type:

- Low risk: U.S. Treasury bonds backed by the government

- Moderate risk: Investment-grade corporate bonds from stable companies

- High risk: High-yield bonds offering better returns with a greater default chance

- Very high risk: Bonds from struggling companies or unstable governments

Warning signs of credit problems:

- Credit rating downgrades from agencies

- Company financial statement deterioration

- Industry-wide challenges affecting multiple issuers

- Economic conditions threaten business models

For Debt Holders: Your Credit Situation

Your own credit creates risks that limit financial options and increase costs.

How poor credit affects you:

- Higher borrowing costs: Increased interest rates on loans and credit cards

- Reduced access: Credit card limit reductions and loan denials

- Employment impact: Some employers check credit during hiring

- Housing challenges: Landlords review credit before approving rentals

- Insurance costs: Companies use credit information for pricing decisions

Credit score factors:

Managing credit risk requires:

- Paying all bills on time without exception

- Keeping credit card balances below 30% of limits

- Monitoring credit reports quarterly for errors

- Addressing problems immediately before they compound

Also Read: Credit Portfolio Management: Ultimate Guide and Strategies

3. Liquidity Risk

Liquidity risk emerges when you cannot access cash quickly without taking significant losses. This affects both your investments and day-to-day finances.

Investment Liquidity Spectrum

High liquidity (easy to convert to cash):

- Savings and checking accounts

- Money market funds

- Publicly traded stocks during market hours

- Treasury bonds and notes

Low liquidity (difficult or slow to convert):

- Real estate properties

- Certificate of deposits with early withdrawal penalties

- Private equity investments

- Collectibles and physical assets

The liquidity trade-off:

Liquid investments often offer higher returns to compensate for reduced flexibility. The problem arises when you need cash urgently and cannot access it.

Personal Cash Flow Liquidity

This means having enough accessible cash for immediate needs and emergencies.

Common liquidity challenges:

- Valuable assets but insufficient cash for monthly bills

- Paycheck timing is misaligned with expense due dates

- Emergency expenses arrive unexpectedly

- Job loss, eliminating income suddenly

Quick liquidity assessment:

Ask yourself these questions:

- Can you cover three months of expenses without selling investments?

- Do you have cash available for a $1,000 emergency?

- Could you handle unexpected medical bills or car repairs?

- Would job loss create an immediate financial crisis?

If you answered no to any question, you face significant liquidity risk. Building accessible savings should become a priority.

4. Interest Rate Risk

Interest rate risk affects nearly every aspect of your financial life. When rates change, both your investments and debt obligations feel the impact.

Understanding this risk helps you prepare for rate fluctuations and make better financial decisions.

How Interest Rates Affect Investments

Bond values move in the opposite direction to interest rates. This inverse relationship creates predictable patterns.

When interest rates rise:

- Existing bond prices fall because new bonds offer better rates

- Your bond portfolio loses market value

- Long-term bonds experience larger price drops than short-term bonds

- Fixed-income investments become less attractive to buyers

When interest rates fall:

- Existing bond prices increase in value

- Your fixed-rate investments become more valuable

- Reinvestment options offer lower returns

- Income from interest payments decreases over time

Impact on Your Debt Obligations

Interest rate changes directly affect how much you pay on various debts.

Variable-rate debt is most affected:

Fixed-rate debt provides stability:

- Mortgage payments remain constant regardless of rate changes

- Auto loans maintain predictable monthly costs

- Fixed student loans offer payment certainty

- Personal loans with fixed rates protect against increases

Also Read: Portfolio Management Steps and First Step Explained

5. Inflation Risk

Inflation erodes your purchasing power over time. What costs $100 today might cost $103 next year. This steady increase affects both your investments and your debt situation.

Understanding inflation risk helps you protect your long-term financial health.

How Inflation Affects Your Investments

Inflation reduces the real value of your investment returns. Nominal gains might hide actual losses.

The math of inflation:

- Your investment earns 5% annual return

- Inflation runs at 3% annually

- Your real return equals only 2%

- You have less purchasing power than the numbers suggest

Investments most vulnerable to inflation:

- Cash savings: Loses value sitting in low-interest accounts

- Fixed-rate bonds: Future payments are worth less in real terms

- Fixed annuities: Predetermined payments cannot keep pace

- Money market funds: Returns often trail inflation rates

Investments that may offer inflation protection:

- Stocks: Companies can raise prices to maintain profits

- Real estate: Property values and rents typically rise with inflation

- Treasury Inflation-Protected Securities (TIPS): Principal adjusts with inflation

- Commodities: Physical goods maintain intrinsic value

How Inflation Affects Your Debt

Inflation creates a complex situation for debt holders. Some effects help you, while others create challenges.

Potential benefits:

- Fixed-rate debt becomes easier to pay with an inflated income

- The real value of your debt decreases over time

- Nominal wages often increase during inflationary periods

- Long-term mortgages become relatively cheaper

Serious challenges:

- The cost of living increases faster than income growth

- Less money available for debt repayment after covering expenses

- Variable-rate debt costs rise as central banks fight inflation

- Emergency expenses grow along with general price levels

6. Currency Risk

Currency risk affects you when investments or obligations involve foreign currencies. Exchange rate fluctuations can increase or decrease actual values.

This risk primarily impacts investors with international holdings. However, currency movements affect everyone indirectly.

When currency risk matters most:

- International stocks: Foreign company values fluctuate with exchange rates

- Foreign bonds: Returns depend on both interest rates and currency values

- Overseas property: Real estate values tied to local currency

- International business: Companies with foreign operations face exposure

How exchange rates create risk: You invest $10,000 in European stocks when the euro trades at $1.10.

Scenario 1 - Currency helps you:

- Stock value increases 10% in euros

- Euro strengthens to $1.20 against the dollar

- Your gain exceeds 10% when converted back to dollars

Scenario 2 - Currency hurts you:

- Stock value increases 10% in euros

- The euro weakens to $1.00 against the dollar

- Your gain drops below 10% or becomes a loss in dollars

Indirect currency effects:

Even domestic investors feel the currency impact through:

- Import prices rise when the dollar weakens

- Export company profits when the dollar strengthens

- Multinational corporation earnings are affected by rates

- The dollar value influences commodity prices

Managing currency risk:

Most individual investors should:

- Accept currency risk as part of international diversification

- Avoid excessive concentration in a single foreign market

- Consider currency-hedged funds for large international positions

- Focus on long-term holdings to smooth short-term fluctuations

Currency risk requires attention but should not prevent international diversification. The benefits of global exposure typically outweigh currency concerns for long-term investors.

Also Read: Portfolio Expansion Strategies Through Acquisition

7. Political Risk

Political risk emerges when government actions or instability affect your financial holdings. Policy changes, regulations, and political events create uncertainty.

This risk exists in every country, including stable democracies like the United States.

Types of political risk:

Regulatory changes:

- New tax laws affecting investment returns

- Financial regulations altering market operations

Government policy:

- Trade agreements opening or closing markets

- Tariffs are changing import and export dynamics

Political instability:

- Election outcomes are creating market uncertainty

- Government shutdowns are disrupting services

How political risk affects different investments:

8. Concentration Risk

Concentration risk occurs when too much of your financial situation depends on a single source. Putting all eggs in one basket creates vulnerability.

This risk appears in multiple areas of your financial life. Recognizing it helps you build more resilient strategies.

Investment concentration dangers:

Single stock exposure: Many people hold too much of one company's stock, often their employer.

Income concentration risk:

Your income sources deserve the same diversification thinking.

Debt concentration problems:

High-interest debt focus:

Carrying too much high-rate debt creates severe pressure:

- Credit card balances above $10,000 create a major burden

- Interest charges consume income needed for other obligations

- A single creditor might hold multiple accounts

- Default risk increases with concentration

Quick concentration assessment:

Ask yourself these questions:

- Does any single stock represent more than 10% of your portfolio?

- Would losing your job eliminate all income?

- Is more than 50% of your debt with one creditor?

- Are all investments in one country or sector?

Each "yes" answer indicates a concentration risk needing attention. Taking steps to diversify reduces vulnerability and improves financial resilience.

Also Read: Steps to Economically Profitable Portfolio Acquisitions

How to Measure and Assess Your Portfolio Risk

Measuring risk helps you understand exposure and make informed decisions. You need both professional metrics and personal assessment.

Key Risk Metrics Simplified

Professional investors use specific tools to quantify risk. Understanding the basics gives you valuable insights.

Four essential metrics:

Standard Deviation - Measures volatility

- Shows how much returns fluctuate over time

- A higher number means more volatility

- Helps compare investment stability

Beta Coefficient - Measures market sensitivity

- Beta of 1.0 matches market movements exactly

- Above 1.0 amplifies market swings

- Below 1.0 cushions market changes

Value at Risk (VaR) - Estimates potential loss

- Shows the maximum expected loss over a specific period

- Calculated with confidence levels

- Example: 95% confidence VaR of $5,000 means a 95% chance that losses stay below that amount

Sharpe Ratio - Measures risk-adjusted returns

- Compares returns to risk taken

- A higher ratio indicates better risk-adjusted performance

- Values above 1.0 are generally considered good

You do not need to calculate these yourself. Investment platforms and advisors provide these metrics. Understanding what they mean helps you evaluate options intelligently.

Your Personal Risk Assessment

Beyond technical metrics, evaluate your overall financial risk exposure through honest self-assessment.

Critical assessment questions:

Income stability:

- How secure is your current employment?

- Do you have backup income sources available?

- Could you replace lost income within three months?

Debt burden:

- What percentage of income goes to debt payments?

- Do you carry high-interest credit card balances?

- Are debts mostly fixed-rate or variable-rate?

Emergency preparedness:

- Can you cover three months of expenses from savings?

- Do you have accessible cash for emergencies?

- Would unexpected costs force more debt?

Investment exposure:

- How much could you lose without lifestyle changes?

- Are retirement accounts properly diversified?

- Does market volatility cause stress or panic?

Calculate these key metrics:

- Debt-to-income ratio: Total monthly debt payments divided by gross monthly income. Below 36% is healthy. Above 43% indicates high risk.

- Emergency fund adequacy: Monthly expenses multiplied by months covered. Minimum three months recommended. Six months provides better protection.

When to seek professional help:

Consider expert guidance when you feel overwhelmed by decisions, carry significant debt without clear plans, approach retirement without a solid strategy, or experience major life changes.

Personalized financial advisory services provide clarity and direction. Professional support helps you understand options and create actionable plans tailored to your unique situation.

Also Read: How to Analyze a Debt Portfolio Effectively

Understanding Your Risk Tolerance

Risk tolerance describes how much uncertainty you can handle financially and emotionally. This varies significantly between individuals based on multiple factors.

Your risk tolerance combines two elements. Willingness represents emotional comfort with uncertainty. Ability reflects financial capacity to absorb losses. Both matter equally in determining appropriate strategies.

Key influencing factors:

Age and time horizon affect risk capacity. Younger investors can recover from losses over decades. Older individuals near retirement need capital preservation.

Financial obligations reduce risk capacity. Mortgage payments, dependents, and healthcare costs limit how much risk you can take. Stable income allows more investment risk. Variable income requires conservative approaches.

Emotional factors shape comfort levels. Previous financial trauma affects future decisions. Natural temperament influences reactions to volatility. Market experience shapes how you respond to downturns.

Three common risk profiles:

Your risk tolerance changes over time. What works today might not fit tomorrow. Regular reassessment ensures alignment with current circumstances and goals.

Also Read: The Ultimate Guide to Repair Your Credit Fast: 8 Sure Steps for a Stronger Score

How to Manage Portfolio Risk Effectively

Managing risk requires active strategies and consistent attention. Several proven approaches help protect your financial future without eliminating growth potential.

Diversification

Diversification spreads risk across multiple holdings. This fundamental strategy reduces concentration risk significantly and protects against single-point failures.

Investment diversification includes:

- Multiple asset classes such as stocks, bonds, and real estate

- Different sectors and industries to avoid concentration

- Various company sizes, from large to small-cap

- Geographic regions, including domestic and international

Financial diversification extends beyond investments:

- Multiple income sources provide stability

- Emergency savings in accessible accounts

- Insurance coverage for major risks

- Backup plans for income disruption

Diversification does not eliminate risk. It manages risk by ensuring no single event destroys your entire financial position. One investment declining hurts less when others perform well.

Asset Allocation and Rebalancing

Asset allocation divides your portfolio according to risk tolerance and timeline. This strategic distribution determines most of your long-term returns.

Common allocation approaches:

Age-based guideline: Subtract your age from 110. The result equals your stock percentage. The remainder goes to bonds. Example: Age 40 means 70% stocks and 30% bonds.

Goal-based allocation:

- Short-term goals under 3 years: Conservative with mostly bonds and cash

- Medium-term goals 3-10 years: Moderate balanced mix

- Long-term goals over 10 years: Aggressive with mostly stocks

Regular rebalancing maintains intended risk:

Review allocations quarterly or annually. Sell overweight positions that grew too large. Buy underweight positions that fell below targets. This discipline forces you to sell high and buy low.

Additional Protection Strategies

Beyond diversification and allocation, other tools provide additional security layers.

- Hedging basics: Insurance protects against catastrophic losses like disability or property damage. Emergency funds hedge against income disruption. These tools cost money but provide valuable protection.

- Risk budgeting: Allocate risk across different goals strategically. Prioritize essential needs over wants. Balance debt payoff with investing based on interest rates and tax benefits.

- Professional guidance options: Financial advisors provide objective perspectives and expertise. Online tools offer portfolio analysis and recommendations. Robo-advisors automate management for lower costs.

Personalized support helps you navigate complexity and avoid costly mistakes. Expert guidance proves especially valuable during major life transitions or market volatility.

Also Read: Top 10 Money Management Tips to Help You Take Control

Common Portfolio Risk Mistakes to Avoid

Learning from common errors helps you avoid costly mistakes that derail financial progress.

Five critical mistakes:

- Ignoring risk until problems emerge - Address risks proactively through regular reviews. Small adjustments prevent major corrections later.

- Emotional decision-making - Panic selling locks in losses. Chasing returns increases risk exposure. Fear and greed drive poor choices that hurt long-term results.

- Inadequate diversification - Single stock concentration creates vulnerability. Sector overweighting amplifies downturns. Geographic limits reduce opportunities for growth.

- Neglecting debt in risk assessment - High-interest debt compounds problems quickly. Variable-rate exposure creates uncertainty. Holistic views include all obligations, not just investments.

- Set-and-forget approach - Life changes require strategy updates. Market shifts demand rebalancing. Regular monitoring catches drift before it becomes problematic.

Avoiding these mistakes requires discipline and awareness. Check your situation regularly. Make adjustments as circumstances change. Stay focused on long-term goals despite short-term noise.

Also Read: How to Diversify Your Income Streams Successfully

Taking Action on Portfolio Risk

Understanding portfolio risk means nothing without action. Use this knowledge to improve your financial position starting today.

Your action plan:

Step 1: Assess current position. Review all investments and debts. Calculate the debt-to-income ratio. Check emergency fund adequacy. Identify your largest risk exposures.

Step 2: Identify specific risks. Which risk types threaten you most? Market risk affects everyone. Credit risk matters if you carry debt or invest in bonds. Liquidity risk appears when savings are inadequate.

Step 3: Determine your tolerance. Consider age, obligations, income stability, and emotional capacity. Be honest about what keeps you awake at night. Match strategies to your real comfort level.

Step 4: Create an actionable plan. Start with quick wins. Build an emergency fund if lacking. Rebalance overweighted positions. Address high-interest debt. Implement one change each month.

When to seek help: Complex situations benefit from professional guidance. Major life changes like retirement or inheritance require expert input. Feeling overwhelmed indicates you need support.

Whether facing investment portfolio risk or managing debt obligations, personalized support can help you find the right path forward. Take the first step toward better risk management today.

Conclusion

Portfolio risk affects every aspect of your financial life. Market risk, credit risk, liquidity risk, interest rate risk, and inflation risk each require attention and management.

You can take control of your financial future. Assess your current risk exposure honestly. Identify areas needing immediate attention. Make adjustments aligning with your goals and comfort level.

Start with one change today. Build emergency savings. Rebalance your portfolio. Pay down high-interest debt. Each step reduces risk and increases financial confidence.

Managing financial obligations can feel overwhelming, especially when you are juggling multiple debts or facing unexpected challenges.

If you are managing a receivables portfolio or outstanding debts and need tailored support, The Forest Hill Management offers secure online payment options, flexible repayment arrangements, and personalised guidance built around your specific circumstances.

FAQs

1. What is portfolio risk in simple terms?

Portfolio risk is the possibility that your investments or debts will lose value or not perform as expected. This includes your stocks, bonds, retirement accounts, and debt obligations like credit cards or loans. Various factors, such as market changes, interest rate shifts, and economic conditions, create this uncertainty.

2. What are the main types of portfolio risk?

The five main types include market risk (economic downturns affecting all investments), credit risk (default on bonds or your own credit challenges), liquidity risk (inability to access cash quickly), interest rate risk (rate changes impacting investments and debt), and inflation risk (purchasing power erosion over time).

3. How do I know my risk tolerance?

Your risk tolerance depends on two factors: willingness (emotional comfort with uncertainty) and ability (financial capacity to absorb losses). Consider your age, income stability, debt obligations, emergency savings, and how market volatility affects your stress levels. Conservative investors prioritize preservation, while aggressive investors accept volatility for higher growth potential.

4. Can diversification eliminate all portfolio risk?

No. Diversification reduces unsystematic risk (company-specific problems) but cannot eliminate systematic risk (market-wide events). A well-diversified portfolio spreads investments across different asset classes, sectors, and geographic regions. This minimizes damage from single failures, but all investments still face some market risk during economic downturns.

5. Should I focus on paying debt or investing first?

Prioritize high-interest debt (credit cards above 15-20%) before investing, as interest costs likely exceed investment returns. However, contribute enough to employer retirement plans to capture full matching contributions. Once high-interest debt is manageable, balance debt payoff with investing based on interest rates and tax benefits.

6. How often should I review my portfolio risk?

Review your portfolio quarterly at a minimum, and immediately after major life events like job changes, marriage, having children, or approaching retirement. Rebalance when allocations drift more than 5% from targets. Regular monitoring catches problems early and keeps your strategy aligned with current goals and risk tolerance.