How to Report Fake Debt Collectors and Scams

Transform Your Financial Future

Contact UsGetting a call about a debt you don’t recognize can feel unsettling. The urgency, the unfamiliar details, and the pressure to act quickly can make it hard to know what’s real and what isn’t.

In 2024, consumers reported losing over $12.5 billion to fraud, with impersonation scams among the most frequent. Many of these involve people posing as debt collectors to demand payments that may not be valid.

In this blog, you will learn how to identify fake debt collectors, what steps to take if something feels suspicious, how to report a fake debt collector, and how legitimate account management works.

Key Takeaways

- Fake debt collectors often rely on urgency, confusion, and partial information to pressure you into making payments without proper verification.

- You have the right to request clear details and written validation before taking any action on a debt.

- Recognizing warning signs such as threats, unclear information, or unusual payment requests can help you avoid scams.

- Taking a structured approach, including verifying the collector and documenting communication, helps protect your personal and financial information.

- Reporting suspicious activity to the appropriate authorities helps prevent fraud and supports wider consumer protection efforts.

What Is a Debt Collector?

A debt collector is a person or organization that contacts individuals to recover unpaid balances on behalf of a creditor or account owner. If an account has gone unpaid for a period of time, it may be handled by a third party whose role is to communicate with you, provide account details, and discuss ways to resolve the balance.

When a legitimate debt collector contacts you, there are clear standards they must follow. You should receive accurate information about the account, including the amount owed and the name of the original creditor. You also have the right to request written verification and take time to review the details before making any decisions.

In most cases, the purpose of this communication is to help you understand your account and explore options for resolving it in a structured and manageable way.

What Makes a Debt Collector “Fake” or Suspicious?

Fake debt collectors do not operate randomly. Most scams follow a pattern designed to create urgency, confusion, and pressure so that individuals act before verifying the information. Understanding how these scams typically work can help you recognize them early and respond more carefully.

While the details may vary, many fake debt collection schemes follow a similar process:

- They rely on timing, not accuracy: Scammers often contact people when they are more likely to feel uncertain, such as after a missed payment, during tax season, or when financial stress is common. The goal is not to be correct, but to sound believable at the right moment.

- They use just enough information to seem credible: Instead of having full account details, they may use partial or outdated information to make the interaction feel real. This creates a sense of familiarity without providing verifiable proof.

- They control the flow of information: Fake collectors avoid giving you time or space to verify anything. They may interrupt questions, redirect the conversation, or repeat the same demand to keep you focused on payment rather than verification.

- They depend on confusion between real and fake processes: Many people are not fully aware of how legitimate debt collection works. Scammers take advantage of this by mimicking certain terms or phrases while avoiding the formal steps real collectors must follow.

- They aim for quick closure, not long conversations: Legitimate account resolution takes time and documentation. Scammers, on the other hand, try to complete the interaction quickly before doubts arise.

Understanding the difference between legitimate communication and potential scams can help you respond more confidently. Taking time to verify information and review your options is always a reasonable and important first step.

Warning Signs of a Debt Collection Scam

While some warning signs may seem obvious, debt collection scams often rely on more subtle tactics that are designed to create confusion or urgency. These scams are not always easy to identify at first, especially when they use familiar terminology or reference partial account details.

In fact, regulators like the Federal Trade Commission and Consumer Financial Protection Bureau regularly warn that scammers often impersonate debt collectors to pressure people into making payments they do not owe.

Below are some of the most common and well-documented red flags.

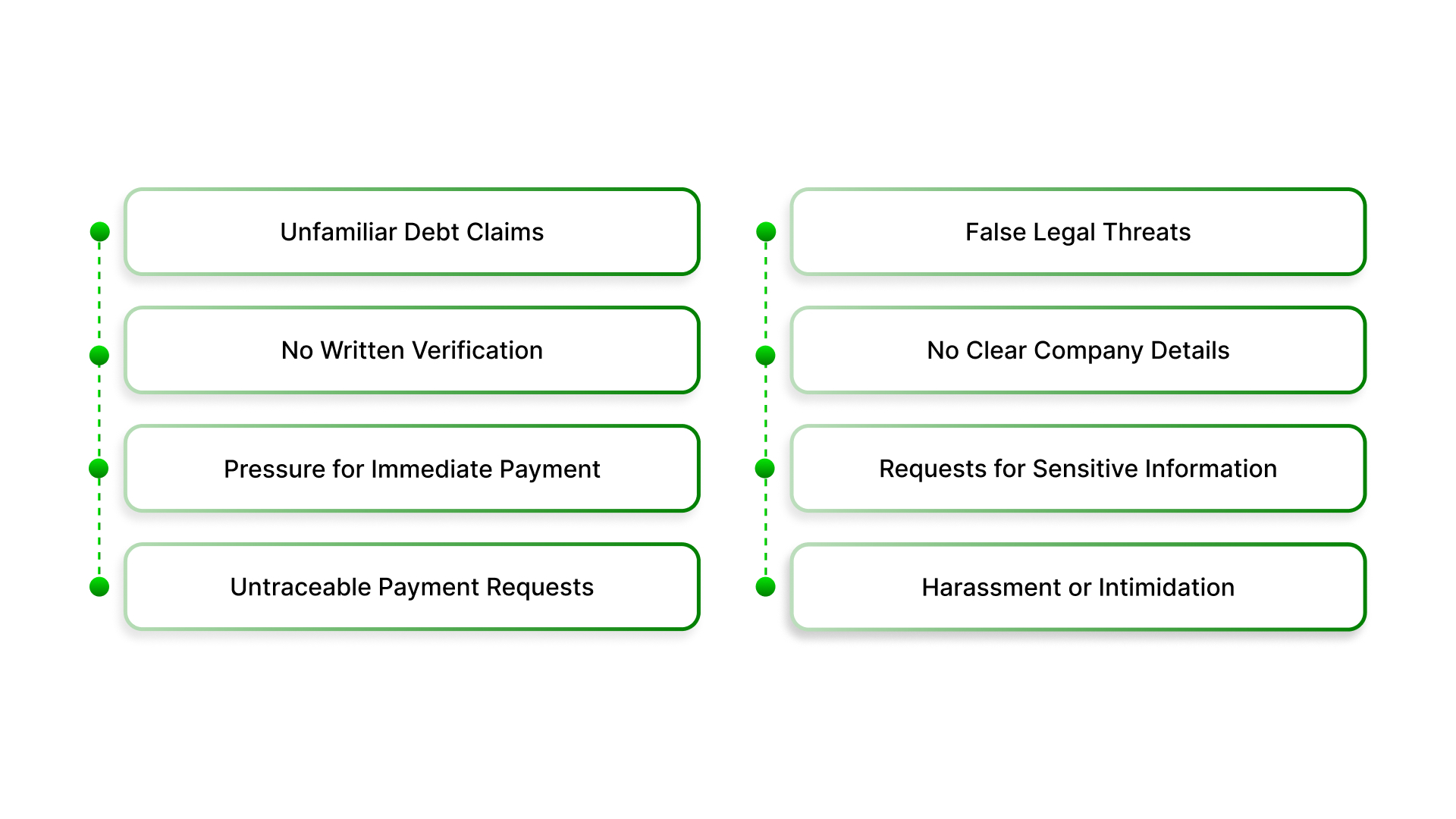

- You don’t recognize the debt, or the details seem unclear

One of the most common signs of a scam is being contacted about a debt that does not sound familiar or does not match your records. Scammers may invent debts or use incomplete information to confuse you into paying without verification.

- They refuse to provide written verification of the debt

Legitimate debt collectors are required to provide details such as the amount owed and the original creditor, often in writing. If someone avoids giving this information or delays it, it is a strong signal to proceed with caution.

- They pressure you to pay immediately

Scammers often create urgency to prevent you from verifying the information. They may insist that you must pay right away to avoid consequences, which is not how structured debt resolution processes typically work.

- They ask for unusual or untraceable payment methods

Requests for payment through gift cards, wire transfers, cryptocurrency, or prepaid cards are a major red flag. These methods are difficult to trace and are commonly used in fraud schemes.

- They threaten arrest, legal action, or wage garnishment without process

Threats of immediate arrest or legal action are often used to create fear. In reality, legal actions follow a formal process, and collectors cannot make false threats to force payment.

- They refuse to identify themselves or their company clearly

A legitimate collector should be able to provide their name, company details, and contact information. If this information is missing, vague, or cannot be verified, it may indicate a scam.

- They ask for sensitive personal or financial information upfront

Requests for details such as your Social Security number, bank information, or full financial data without proper verification can signal fraudulent intent. Real collectors typically already have basic account information.

- They use intimidation, harassment, or repeated aggressive contact

Scammers often rely on fear-based tactics, including repeated calls, threats, or claims of severe consequences. Legitimate debt collection must follow rules that prohibit harassment or abusive behavior.

Also read: Collection Debt Agency Contacted You? Here’s What to Know

Recognizing these warning signs does not mean every contact is fraudulent. However, if one or more of these behaviors appear, it is important to pause, verify the information, and avoid making any immediate payments until you are confident the communication is legitimate.

Ways to Avoid Debt Collection Fraud

The best way to protect yourself is not by reacting quickly, but by slowing down and verifying details before taking any action. Following a few structured steps can help you avoid fraud while still addressing legitimate account matters responsibly.

Here are some practical ways to protect yourself from fake debt collectors:

Always verify the debt before making any payment

If you are contacted about a debt, take time to confirm that it is actually yours. Legitimate collectors are required to provide details such as the creditor’s name, amount owed, and verification if requested.

If this information is missing or unclear, it is important to pause and verify before proceeding.

Request written validation and review it carefully

A legitimate process includes a written notice explaining the debt and your rights. If someone refuses to provide documentation or avoids sending details in writing, that is a strong warning sign.

Reviewing written information helps you make informed decisions instead of reacting under pressure.

Do not share personal or financial information too quickly

Scammers often try to collect sensitive information such as bank details or Social Security numbers.

You should only share such information after you are confident the collector is legitimate. Real collectors typically already have basic account details and will not require unnecessary personal data upfront.

Be cautious of pressure, threats, or urgent payment demands

Fraudulent collectors often use intimidation tactics, including threats of arrest or immediate legal action, to force quick decisions.

In reality, debt collection follows a structured legal process, and you are given time to review and respond. Urgency is often a sign to slow down and verify.

Avoid unusual payment methods

Requests for payment through gift cards, wire transfers, prepaid cards, or cryptocurrency are commonly associated with scams. These methods are difficult to trace and recover. Legitimate payment processes are typically secure, documented, and verifiable.

Verify the company independently

If you are unsure about a collector, ask for their name, company, and contact details. Then verify this information independently through official sources rather than relying on the contact details provided during the call or message.

Keep records of all communication

Save emails, letters, and details of phone calls, including dates and names. Having a record helps you track what was said and provides useful information if you need to report suspicious activity.

Understand your rights as a consumer

Debt collection is regulated, and collectors must follow rules around communication, transparency, and fairness. Knowing that you cannot be threatened, misled, or rushed into payment helps you approach the situation with more confidence.

Also read: How to Verify a Debt Collector and Protect Your Rights

Avoiding debt collection fraud is not about ignoring communication. It is about taking a structured and informed approach. By verifying details, protecting your information, and understanding your rights, you can respond with clarity and reduce the risk of falling victim to scams.

How to Report a Fake Debt Collector?

If you believe someone is trying to collect a debt that does not belong to you or is using pressure and unclear information, it is important to act carefully and report the situation. Reporting fraud not only helps protect you but also helps authorities track and stop similar scams from affecting others.

Taking a structured approach can help you stay in control while ensuring the issue is handled properly:

Report the incident to the Federal Trade Commission (FTC)

The FTC collects reports of fraud and uses them to investigate and take action against scammers. You can file a complaint online at ReportFraud.ftc.gov or call 1-877-FTC-HELP (1-877-382-4357). When reporting, include details such as phone numbers, emails, and any payment requests you received.

Submit a complaint to the Consumer Financial Protection Bureau (CFPB)

The CFPB helps monitor and respond to issues related to financial services, including debt collection concerns. You can submit a complaint through their online portal or call 1-855-411-CFPB (1-855-411-2372). This step helps ensure the situation is reviewed and documented appropriately.

Report to the Internet Crime Complaint Center (IC3)

If the contact involved emails, websites, or online communication, you can file a report with the IC3, a division of the FBI. This is especially useful for internet-based scams and helps authorities track digital fraud activity.

Contact your state attorney general or local authorities

State offices and local law enforcement agencies can help address fraud cases within your area. If you feel threatened or pressured, filing a report with local authorities can add an additional layer of protection.

Keep detailed records of all communication

Save emails, text messages, voicemails, and any written notices you receive. Document dates, times, and what was said during calls. Having clear records can support your report and help authorities understand the situation more accurately.

Place a fraud alert on your credit report

If you shared personal or financial information, consider placing a fraud alert with one of the major credit bureaus:

- Equifax: 1-800-525-6285

- Experian: 1-888-397-3742

- TransUnion: 1-800-680-7289

A fraud alert makes it more difficult for unauthorized accounts to be opened in your name and lasts for one year, with the option to extend.

Taking these steps can help you respond to suspicious activity in a calm and informed way. Reporting fraud ensures that the situation is documented, your information is protected, and appropriate action can be taken against those responsible.

Conclusion

Being contacted about a debt can feel confusing, especially when you are unsure whether it is legitimate. The key is to pause, verify the information, and follow a structured approach rather than reacting under pressure.

Knowing how to report a fake debt collector helps you protect your information and take control of the situation. At the same time, understanding how legitimate account management works can make the process clearer and less stressful.

If your account is being managed by The Forest Hill Management, you can expect clear communication, secure payment options, and support in understanding your next steps.

Take your first step to financial freedom!

FAQs

1. Can a scammer use real company names when posing as a debt collector?

Yes. Scammers sometimes use the names of legitimate companies to appear credible. It is always important to verify contact details independently rather than relying on the information provided during the interaction.

2. What should I do if I accidentally shared my personal information?

If you have shared sensitive details, consider placing a fraud alert on your credit report and monitoring your accounts closely for any unusual activity.

3. Is it safe to ignore a debt collection call if I think it is a scam?

It is better to verify first rather than ignore completely. Confirming whether the debt is legitimate ensures you do not overlook a valid account while protecting yourself from fraud.

4. Can fake debt collectors contact me through email or text messages?

Yes. Scammers often use multiple channels, including email, text messages, and social media, to make their communication appear more convincing.

5. What happens after I report a fake debt collector?

Your report helps authorities track patterns, investigate fraudulent activity, and take action against scammers, which can prevent others from being affected.