Collection Debt Agency Contacted You? Here’s What to Know

Need Help Reviewing Your Account?

Contact UsHave you received a notice from a collection debt agency and wondered what it means for your situation? When messages about an unpaid account appear, it can leave you questioning what the balance is, how it reached this stage, and what choices you actually have moving forward.

Many people feel uncertain when a collection debt agency becomes involved because the process is unfamiliar and the information can feel incomplete at first.

If a collection debt agency has contacted you, the most helpful step is gaining a clear picture of the account before making any decisions. Taking time to review the details, understand your rights, and explore possible debt repayment plans can bring much-needed clarity.

With accurate information and a structured path forward, you can approach the situation with more confidence and begin working toward a stable financial footing.

Key Takeaways

- A collection debt agency contacts consumers when an unpaid account remains unresolved after earlier reminders, helping explain the balance and discuss possible repayment options.

- Accounts are typically sent to a collection debt agency after payments remain overdue for around 60–90 days, shifting communication to a dedicated team that handles account resolution discussions.

- Federal laws such as the Fair Debt Collection Practices Act protect you from harassment, limit contact times, and give you the right to request written verification of the debt.

- Before moving forward with payments, you can request documentation showing the original creditor, account details, and the agency’s authority to discuss the balance.

- With secure payment tools, transparent account information, and flexible repayment plans, resolving an overdue account can become a structured step toward financial stability.

What is a Collection Debt Agency?

A collection debt agency is a company that contacts consumers about unpaid accounts after payments remain overdue. The agency communicates details about the balance, verifies the account, and may discuss repayment options or payment arrangements on behalf of the original creditor.

Key points that explain the role of a collection debt agency include:

- Support After Missed Payments: Agencies step in when earlier billing reminders did not resolve the balance, and additional help is needed to address the account.

- Communication About the Account: You may receive letters, phone calls, or secure messages explaining the balance and inviting you to discuss repayment options.

- Different Collection Arrangements: Some agencies manage accounts for the original company, while others may take responsibility for the account after it is transferred.

- Repayment Discussions: If paying the full amount immediately is difficult, the agency may discuss structured payment options that help you work toward resolution.

- Clear Account Information: Agencies provide details about the balance so you can review the information and confirm the account before making decisions.

Knowing the purpose of a collection debt agency can help you approach the situation calmly and focus on the next step toward resolving the account.

If your budget feels stretched and progress seems slow, practical strategies can help you regain control. Learn actionable steps in 6 Steps to Get Out of Debt on a Low Income Fast.

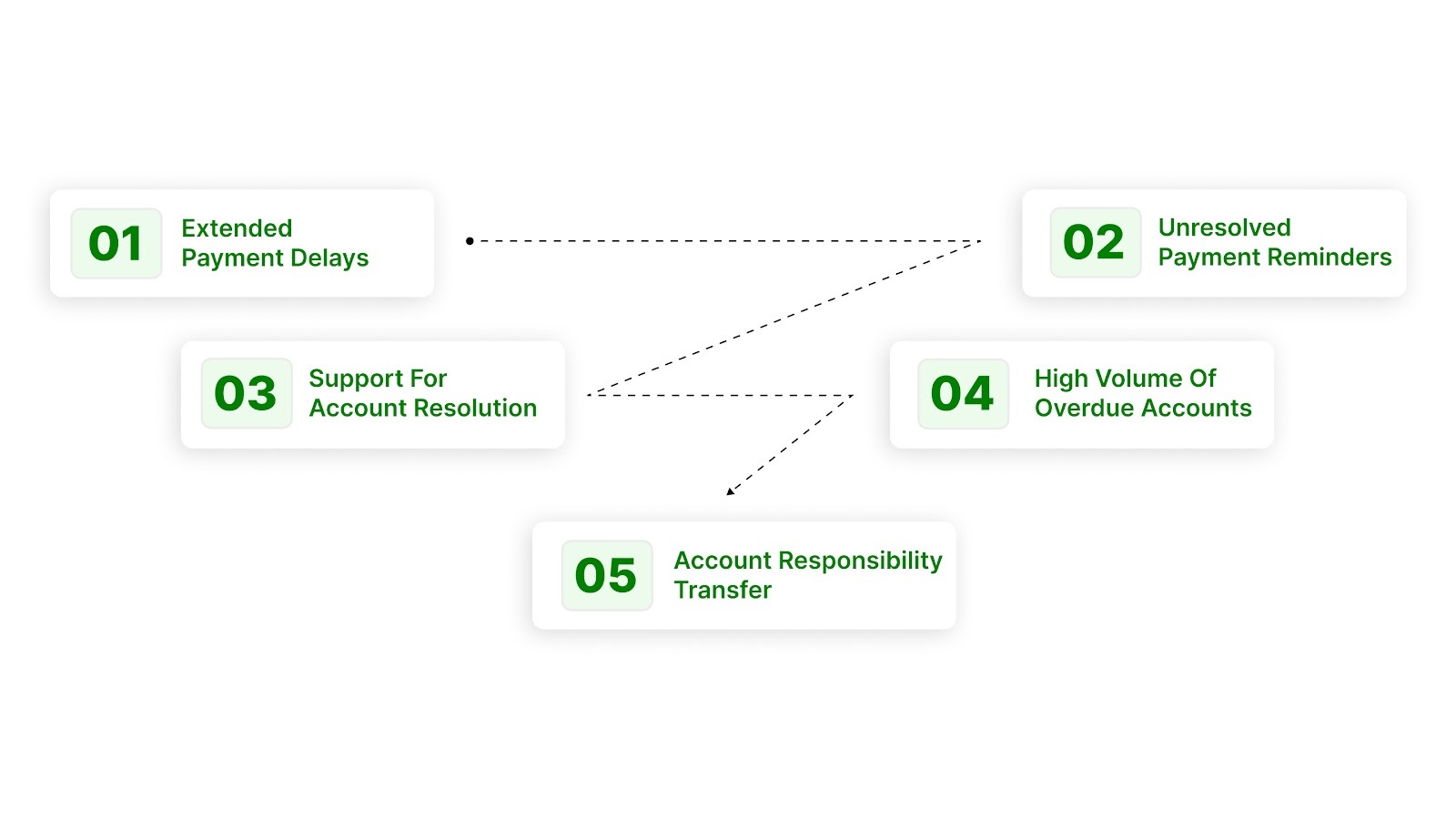

Why Are Accounts Sent to a Collection Debt Agency?

If an account remains unpaid for an extended period, it may be transferred to a collection agency after earlier payment reminders and follow-ups fail to resolve the balance. This transfer means that a different team now manages communication with you and helps clarify the next steps to address the account.

Common reasons accounts reach this stage include:

- Extended Payment Delays: Accounts may be transferred when payments remain overdue for about 60–90 days or longer without resolution.

- Earlier Reminders Went Unresolved: Billing notices or follow-up contacts may not have resulted in payment, prompting the account to move to the next stage of review.

- Additional Support For Account Resolution: A dedicated team may be assigned to discuss the balance and explore realistic repayment options with you.

- High Volume Of Past-Due Accounts: When many accounts become overdue at the same time, agencies help manage communication and resolution discussions.

- Transfer of Account Responsibility: In some situations, responsibility for managing the account may shift to another organization that now handles communication regarding the balance.

Knowing why an account may be sent to a collection agency can make the process feel less uncertain and help you focus on reviewing the details and deciding your next step.

Every financial situation is different, which is why rigid repayment approaches often fall short. Discover the reason in Why One-Size-Fits-All Debt Solutions Don't Work for Real Relief.

How a Collection Debt Agency Works

Once your account reaches a collection debt agency, the process typically follows a series of steps that explain the balance and outline possible ways to resolve it. Clear communication during this stage allows you to review the account details and consider practical options for addressing the balance.

The collection process often includes several stages that help clarify the account and support communication with you:

- Initial Contact: You may receive letters, phone calls, emails, or text messages explaining the balance and inviting you to understand the account information.

- Account Review Opportunity: Communication gives you a chance to look over the account details and confirm the information before deciding how to proceed.

- Payment Arrangement Discussions: If paying the balance at once feels difficult, structured payment options may be discussed to help you move toward resolving the account.

- Credit Report Updates: Unpaid balances may appear on your credit report, which can affect your credit history for several years.

- Extended Resolution Steps: If the account remains unresolved over time, the situation may move into a formal review process through the court system.

Understanding how the process typically unfolds can help you approach each stage with more clarity and confidence as you decide how to move forward.

If you need guidance while reviewing repayment options, professional support can help you move forward with confidence. Explore trusted resources in Best Finance Advisory Service Providers for Debt Management.

Your Rights When Dealing With a Collection Debt Agency

If a collection debt agency contacts you, federal law sets rules that protect you during communication. In the United States, the Fair Debt Collection Practices Act (FDCPA) limits how agencies may contact you, what information they must provide about the account, and which actions require court approval.

Consumer protections under the FDCPA help define what agencies are allowed to do and what they are prohibited from doing.

Understanding these protections can help you feel more confident when reviewing an account and deciding the next step toward resolving it.

Planning for future financial goals often raises questions about how debt decisions may influence them. Find out in Does Debt Consolidation Affect Buying a Home?

What a Collection Debt Agency Can and Cannot Do

When a collection debt agency contacts you, federal law sets clear limits on how communication can occur and which actions require legal approval. These rules protect respectful interaction while allowing agencies to discuss possible ways to address the balance and review the account with you.

Federal protections outline what collection agencies are allowed to do and what actions are not permitted.

Understanding these boundaries can help you recognize fair communication and approach conversations about your account with greater clarity and confidence.

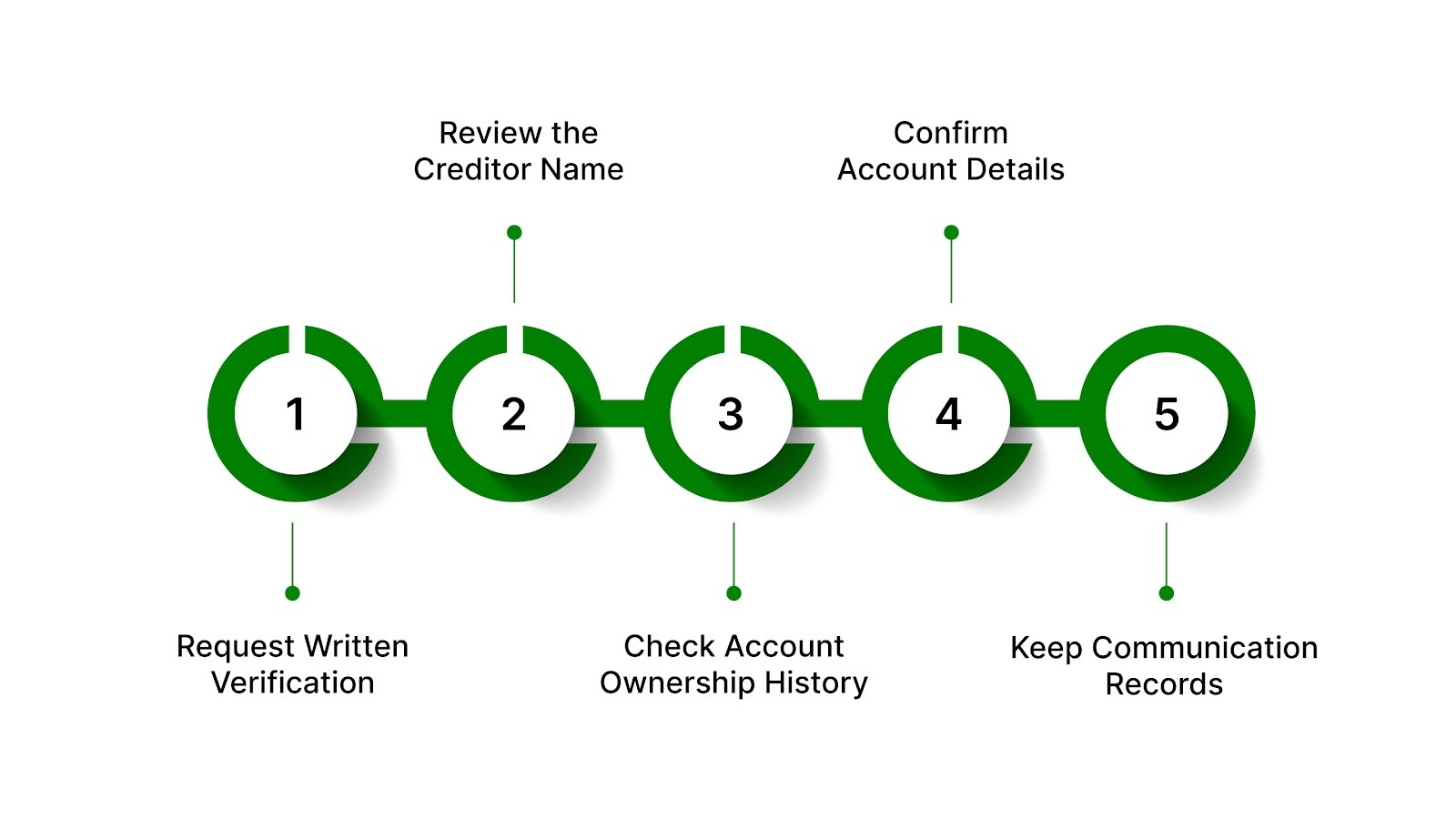

How to Verify the Original Creditor on a Collection Account?

When you receive communication about a collection account, confirming the original creditor helps prevent mistakes and ensures the balance information matches your records. Reviewing the source of the account allows you to verify the details and confirm the information is accurate before making repayment decisions.

Steps that help confirm the original creditor on a collection account include:

- Request Written Verification: Ask the agency in writing to provide documentation showing the account details and identifying the original creditor connected to the balance.

- Review the Creditor Name: Compare the creditor listed in the documentation with past statements or records you may have kept from the original account.

- Check Ownership History: If the account has been transferred, documentation should explain how responsibility for the account moved from the original company to the current agency.

- Confirm Account Information: Look for matching details such as account numbers, balance amounts, and dates to ensure they align with your financial records.

- Keep Communication Records: Save copies of letters or messages you send and receive so you can track the verification process clearly.

Confirming the original creditor can help you examine the account records with clarity and move forward knowing the information you are working with is accurate.

What to Do First When a Collection Debt Agency Contacts You

When a collection debt agency contacts you, taking a few careful steps can help you review the situation calmly. Checking the account details, confirming the information provided, and keeping records of communication can help you decide the most appropriate way to address the balance.

Practical actions that can help you manage the situation confidently include:

- Learn the Account Details: Ask for information about the balance, including the creditor’s name and the amount owed, so you clearly understand what the communication relates to.

- Confirm the Agency Is Legitimate: Before sharing sensitive information, make sure the organization contacting you is authorized to discuss the account.

- Request Written Documentation: Written information allows you to check the documentation carefully and confirm whether the balance is accurate.

- Keep Copies Of Communications: Save letters or messages and note the dates of calls so you have a clear record of your interactions.

- Provide Documentation If Needed: If the account information appears incorrect or already resolved, sharing relevant records can help clarify the situation.

Taking measured steps when communication begins can help you review the account with confidence and decide the most appropriate path toward addressing the balance.

Conclusion

When an account enters the collections stage, many people feel as though the situation has already been decided. In reality, this stage often becomes the point where conversations around the account begin to take shape and where clearer paths toward resolving the balance start to emerge.

Forest Hill Management works with individuals across the United States who are ready to bring overdue accounts back under control through transparent communication, secure payment options, and respectful support.

If you are reviewing an account and want to better understand the information connected to it, you may use the available communication channels to contact our advisors for personalized support.

FAQs

1. Can a collection debt agency help if my account has been transferred multiple times?

Yes. A collection debt agency can review the history of the account and explain which organization currently manages it. This helps confirm the balance details and clarify how repayment discussions typically move forward.

2. Are professional debt collection services different from standard recovery services?

Professional debt collection services generally follow structured compliance rules and consumer protection laws. These recovery services' debt collection practices focus on communication, documentation, and repayment discussions rather than aggressive collection tactics.

3. Why do companies use professional debt recovery services instead of handling accounts internally?

Many organizations rely on professional debt recovery services when accounts remain unresolved for long periods. A collection debt agency may provide dedicated teams who communicate with consumers and discuss repayment options.

4. Are fast debt collection services USA required to follow the same consumer protection rules?

Yes. Even fast debt collection services in the USA must follow federal regulations such as the Fair Debt Collection Practices Act. These laws set boundaries on communication and help protect consumers during the collection process.

5. Do certain industries use specialized debt collection services for technology companies?

Yes. Some organizations rely on specialized debt collection services for technology companies or industry-specific solutions from debt collection providers. These agencies manage accounts connected to subscription services, software platforms, or digital billing systems.