The 3-Step Formula for Financial Freedom (Even If You Have Debt)

Transform Your Financial Future

Contact UsFinancial freedom often feels like an unreachable goal when you are already managing debt, but it does not have to be. According to the Federal Reserve Bank of New York, total U.S. household debt increased by $197 billion in the third quarter of 2025, with credit card balances alone climbing to over $1.23 trillion.

Most Americans are juggling financial responsibilities while trying to create a sense of stability and control. Financial freedom is about learning how to manage debt strategically so that it no longer defines your life.

It means building a plan that lets you move forward, even while paying down what you owe. In this guide, you will learn the 3-step financial freedom formula. It is a practical approach to regain control, balance repayment with growth, and rebuild your financial future one clear step at a time.

Quick glance:

- Financial freedom is about control, not wealth. It means managing your money intentionally so that your income and expenses align with your goals instead of your stress.

- The financial freedom formula gives structure to your goals. Multiplying your annual expenses by 25 helps you see what long-term stability could look like, even while repaying debt.

- Debt and independence can coexist. Paying down what you owe consistently, managing interest, and maintaining savings habits are all parts of the same strategy.

- Progress depends on awareness and adaptability. Tracking spending, adjusting plans, and staying calm during setbacks matter as much as financial calculations.

- Consistency creates momentum. Every payment, every small saving, and every month of planning adds up, turning discipline into long-term financial confidence.

What Is the Financial Freedom Formula?

The financial freedom formula is a simple and practical way to measure how close you are to living without relying on your regular paycheck. This is what experts call active income.

In other words, it helps you determine the point where the money you earn passively (through savings, investments, or other income sources) can cover your living expenses without additional employment.

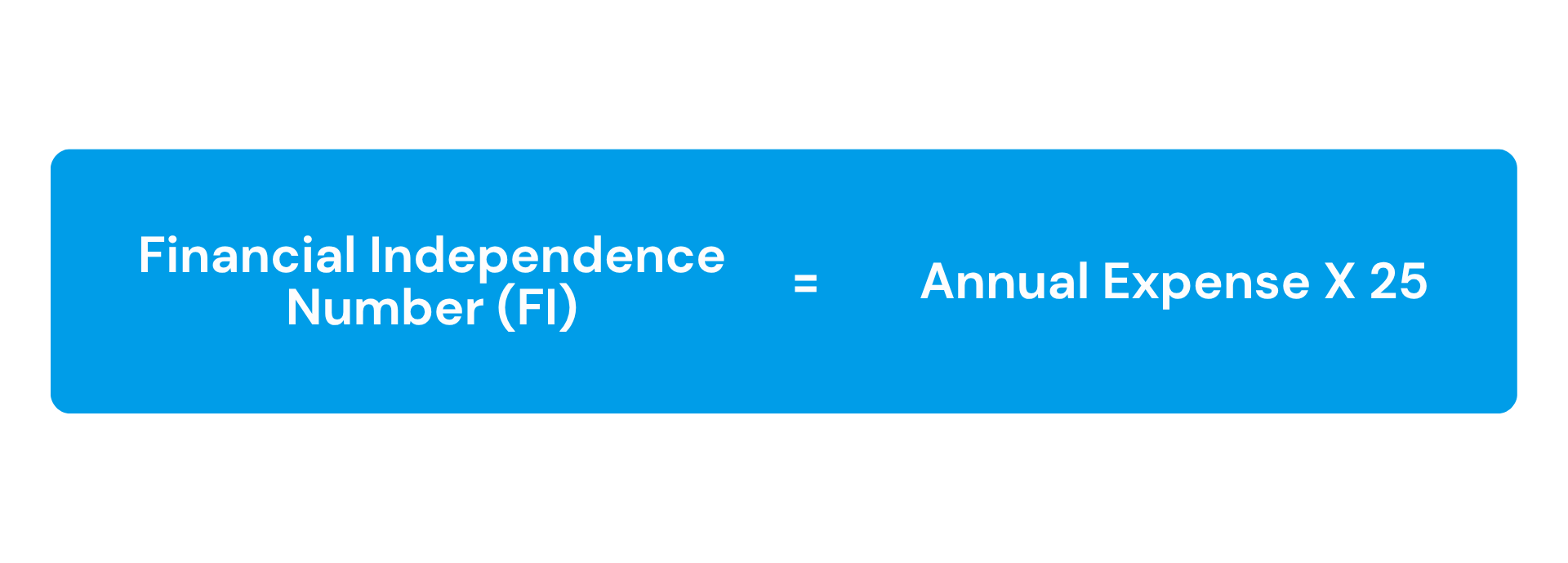

The formula is straightforward:

This calculation is based on the 4% rule, which assumes you can safely withdraw 4% of your total assets annually to cover your expenses once you reach financial independence.

But why does this matter, especially if you are still dealing with debt? It provides you with something concrete to work toward, helping you focus on long-term progress rather than short-term panic.

Here is why even those managing debt should look forward to financial independence:

- It shifts your mindset from survival to structure. When you have a long-term goal, debt becomes one part of the plan and not the entire story.

- It builds awareness. Understanding your expenses helps you make smarter repayment decisions and identify where you can free up funds.

- It creates motivation. Every payment you make and every balance you reduce moves you closer to financial stability.

- It helps you visualize progress. Tracking your FI number can show how your efforts — even small ones — impact your future freedom.

Financial freedom helps you calculate what independence could realistically look like for you. It is a personal roadmap that begins with debt management but leads toward lasting control and stability. In the next section, we look at how to calculate your financial independence (FI) number.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

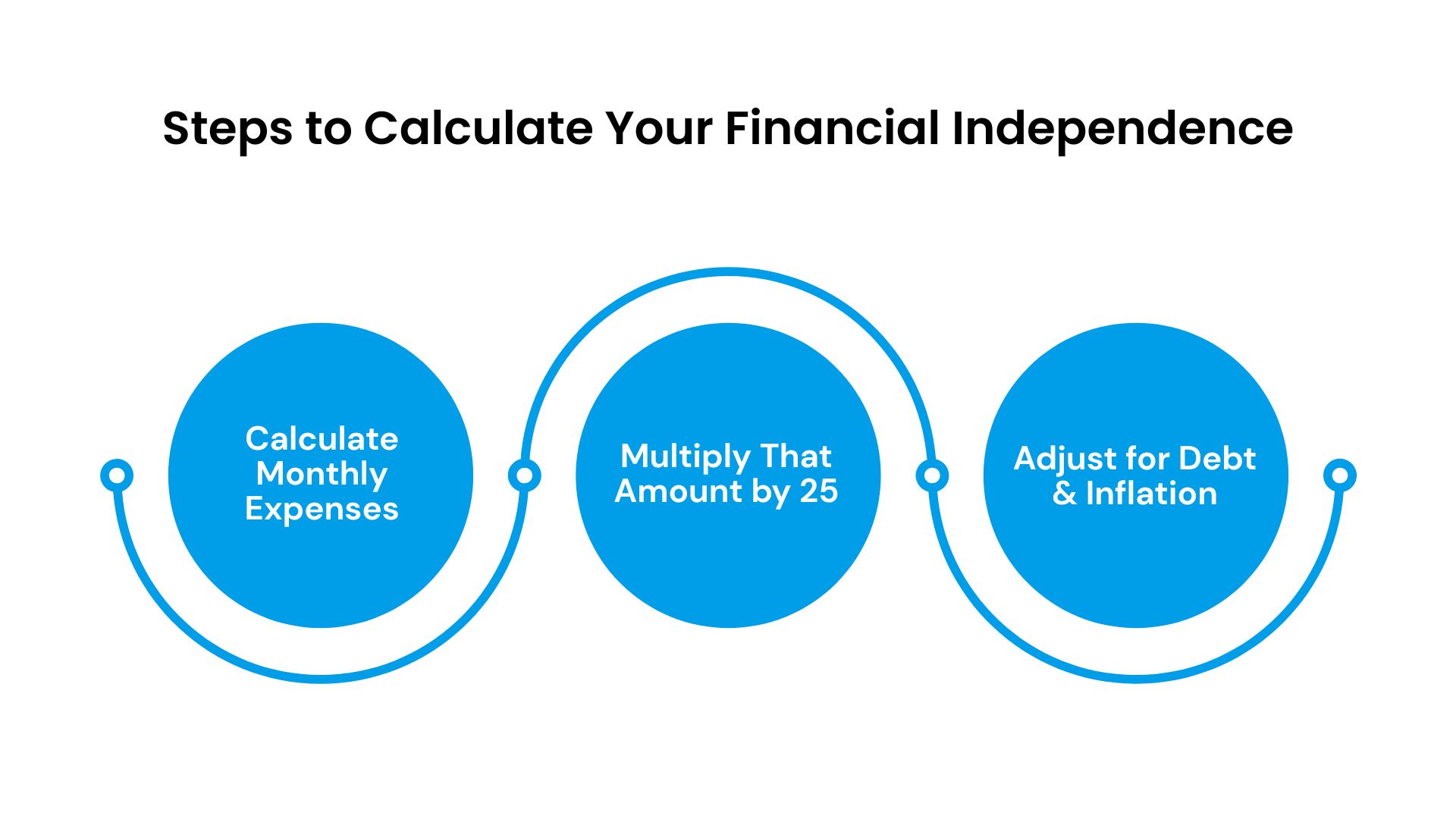

Steps to Calculate Your Financial Independence

The financial freedom formula works because it takes something that feels abstract — “financial independence” — and makes it measurable. It helps you see exactly how your spending, debt, and savings fit together.

These steps can help you plan your financial goals better by giving you direction:

Step 1: Calculate Your Monthly Living Expenses

Start by listing what you spend each month on essentials and debt. This provides a clear baseline for determining the amount of income you need to sustain your lifestyle.

Here is what to include in your expense review:

- Rent or mortgage, utilities, and insurance premiums.

- Groceries, fuel, and transportation costs.

- Loan payments, credit card minimums, or any recurring debt obligations.

- Occasional costs, such as subscriptions or small repairs.

Step 2: Multiply That Amount by 25

This gives you your Financial Independence (FI) Number. This is the amount of money you would ideally need invested to cover your expenses through passive income.

Here is what this step tells you:

- It assumes you can withdraw about 4% of your savings each year and still maintain long-term stability.

- It helps you see the connection between reducing expenses today and reaching independence sooner.

- It turns your monthly budget into a long-term financial plan.

Step 3: Adjust for Debt and Inflation

Your FI number is a guide, not a fixed target. Adjusting it for debt and inflation keeps your plan realistic.

Here is how to do it:

- Subtract high-interest debts since they reduce available income.

- Add 10–15% to your FI target to account for inflation and future expenses.

- Recalculate yearly as you pay down debt or change your spending habits.

This keeps your goals grounded in your current reality, not in where you think you “should” be.

This is an easy example to help you see things:

Let’s say your total monthly expenses, including rent, groceries, bills, and debt payments, come to $2,800.

Your annual expenses = $2,800 × 12 = $33,600.

Then, your FI Number = $33,600 × 25 = $840,000.

Now imagine you pay off one credit card and bring your monthly expenses down to $2,500. Your new FI target becomes $750,000.

That $300 monthly difference reduces your long-term financial goal by nearly $90,000. Now, you see how even small changes now can create a major shift over time.

Knowing your FI number gives you perspective, not pressure. It shows that progress is measurable and achievable — even when you are still repaying debt.

Forest Hill Management offers personalized financial guidance to help you understand what financial independence means for your unique situation. Our goal is to make your repayment journey smoother and more manageable, so you can plan for progress without feeling overwhelmed. Speak with one of our advisors today to explore practical strategies that fit your goals.

Also Read: Calculating Financial Freedom Number using Passive Income Formula

How Does the Financial Freedom Formula Apply When You Have Debt

Many traditional FIRE (Financial Independence, Retire Early) concepts are built on the idea of having zero debt; however, real life rarely fits that mold. Most people pursuing financial stability are managing credit cards, car loans, or student debt while trying to plan ahead.

For those balancing repayment and planning, think of a more grounded approach:

FIRE = Financial Independence, Realistically Earned.

It is about setting progress in motion without waiting for perfect conditions.

Freedom, even while in debt, comes from three simple but powerful principles:

- Paying Consistently: Regular, on-time payments are progress. They build momentum, improve credit health, and increase confidence.

- Managing Interest Costs: Prioritizing high-interest debt first frees up more of your income for future goals.

- Reinvesting Time and Energy Saved Into New Income or Skills: Every bit of progress gives you back bandwidth. This is energy you can use to earn, learn, or plan for your next stage of growth.

Debt does not disqualify you from financial freedom; it redefines your path toward it. The same formula still applies — but with patience, structure, and realistic expectations, you can make it work for your situation.

To see how quickly you can move toward stability, it helps to understand the key elements that shape your personal timeline to financial independence.

Suggested Read: How To Pay Debt in Credit Collection Services

Core Factors That Shape Your Financial Independence Timeline

Financial independence is shaped by how you respond to the variables that define your financial life.

“Your economic security does not lie in your job; it lies in your own power to produce — to think, to learn, to create, to adapt. That’s true financial independence.”

— Stephen R. Covey, author of The 7 Habits of Highly Effective People

Covey’s words remind us that independence comes from adaptability, not just accumulation. Your ability to make choices, reframe setbacks, and create systems that work for your reality is what determines how long it takes to reach true stability.

Here are the core factors that determine how quickly you can reach financial stability and independence:

- Income Stability: Having a consistent income matters more than earning a high amount. Predictable earnings allow you to plan, pay down debt, and invest with confidence.

- Debt Load and Interest Rate: The total you owe — and the rate at which it grows — affects how much of your income is available for savings and investing. Reducing interest costs is one of the fastest ways to gain financial traction.

- Expense Flexibility: Being able to adjust your lifestyle when needed by cutting costs temporarily or delaying large purchases creates breathing room during financial transitions.

- Savings and Investment Rate: Even small, steady contributions to savings or retirement accounts make a measurable difference over time through compound growth.

- Time Horizon: The earlier you start organizing your finances, the greater your long-term leverage. Time amplifies every financial decision you make — both good and bad.

Financial progress is as much mental as it is mathematical. Staying calm, patient, and focused during setbacks matters just as much as sticking to your budget. Emotional steadiness helps you adapt without losing motivation.

These variables can be managed through strategy, not luck. The right approach allows you to balance repayment, savings, and growth in a way that fits your life, not someone else’s timeline.

Suggested Read: When Does the Collection Process Begin for Overdue Balances

Balancing Debt Repayment and Retirement Planning

Debt repayment and investing are often viewed as opposites, as one focuses on the present, while the other focuses on the future. But in reality, they work best together.

Paying down what you owe reduces financial pressure, while investing, even in small amounts, builds habits, confidence, and security for the years ahead.

Tables showing a few strategies that can help you strike a balance:

Even if the numbers seem small, investing early builds the discipline that sustains your long-term success. It reminds you that progress is possible.

Here are a few quick, actionable tips to help you stay balanced while managing debt and building for the future:

- Review interest rates every six months. Lenders may adjust them, and refinancing can sometimes free up cash sooner than expected.

- Use one-time income wisely. Bonuses, tax refunds, or cash gifts can either accelerate repayment or bolster your emergency fund.

- Track your net worth, not just your debt. Watching assets grow alongside shrinking balances helps you stay motivated.

- Set financial checkpoints, not deadlines. Reassess your plan periodically to stay flexible and prevent burnout.

- Avoid all-or-nothing thinking. Saving and paying debt are both progress; even small steps in each direction create long-term impact.

Managing your finances is about optimizing time as much as money, and that is where Forest Hill Management can help guide you forward.

Suggested Read: Is Paying Debt Collection Agencies a Bad Idea?

Forest Hill Management Offers Beyond Debt Collection

Forest Hill Management is more than a debt collection agency. We are dedicated to helping individuals rebuild structure, stability, and confidence in their financial lives.

We understand that managing debt is about regaining control, creating clarity, and finding direction for the future. Our approach focuses on respect, transparency, and collaboration rather than pressure.

Here is what sets us apart:

- Personalized Financial Guidance. We take time to understand each individual’s situation and help create a plan that fits their capacity and goals.

- Flexible Repayment Options. We work with you to design manageable payment schedules that reduce stress and support steady progress.

- Secure Online Payment Systems. Our platform offers convenience and peace of mind, allowing you to make payments safely from anywhere.

- Clear and Respectful Communication. Every conversation is rooted in professionalism and empathy — you will always know where your account stands.

- Focus on Financial Education. We aim to help you understand how repayment connects to long-term stability, not just clearing balances.

At Forest Hill Management, our mission goes beyond collecting payments — we help people move forward. Every interaction is an opportunity to simplify the repayment journey, save time, and support you as you build your financial future with confidence and control.

Conclusion

The financial freedom formula provides a measurable way to track progress. It enables you to see how budgeting, debt repayment, and smart saving contribute to long-term stability. Even if you are still managing debt, understanding your path to financial independence helps you plan realistically and move forward with clarity.

At Forest Hill Management, we make that journey easier. Through personalized financial guidance, flexible repayment plans, and secure online tools, we help you organize your finances. Our goal is to make repayment a step toward independence and not a setback.

Start taking control of your finances today. Speak with a financial advisor to explore your repayment and planning options. The sooner you begin, the sooner your financial freedom starts to take shape.

Frequently Asked Questions

1. How Often Should I Review My Financial Independence Plan?

It is best to review your plan at least once or twice a year. Reassessing your expenses, debt, and savings helps you stay aligned with your current goals and adjust when life circumstances or income change.

2. Can I Still Work Toward Financial Freedom With a Low Income?

Absolutely. Financial independence is about consistency, not income level. Even small steps — such as lowering interest costs, setting up automatic payments, or saving a fixed amount each month — can lead to meaningful progress over time.

3. How Do Interest Rates Affect My Financial Independence Timeline?

High-interest debts slow progress because more of your payment goes toward interest rather than principal. Paying these off first can significantly shorten your journey to financial freedom and free up income for saving or investing.

4. Should I Pay Off Debt Before I Start Saving for Retirement?

It depends on your situation. Paying high-interest debt should take priority, but it is wise to contribute at least a small amount to retirement savings — especially if your employer offers a match. The goal is balance, not perfection.

5. How Can Forest Hill Management Support Me During My Repayment Journey?

Forest Hill Management provides structured repayment options and personalized financial guidance to make your journey smoother. Our goal is to help you manage debt with less stress while giving you the clarity to focus on long-term financial goals.