Complete Guide to Asset Receivables Management

Transform Your Financial Future

Contact UsMany overdue accounts begin long before individuals are contacted about them. Studies show that 44% of B2B invoices are overdue, and roughly 6% are written off as bad debts, meaning they are never recovered.

This highlights how common delayed payments and unresolved balances have become, which is why structured receivables management systems exist to organize accounts and guide them toward resolution.

In this blog, we’ll explain what asset receivables management means, how the process works, the key metrics used to monitor accounts, and how structured receivables management helps move outstanding balances toward resolution.

Key Takeaways

- Asset receivables management is a structured system used to track and resolve unpaid balances, helping bring clarity to overdue accounts.

- Understanding how the receivables process works can make dealing with an outstanding account less confusing, since it explains how payments, communication, and repayment arrangements are handled.

- Overdue balances often arise from temporary financial challenges, which is why many receivables systems include structured repayment plans and flexible resolution options.

- Financial metrics and monitoring systems help track payment progress, ensuring that accounts are managed consistently and fairly over time.

- Working with a structured receivables management partner can help individuals better understand their accounts and move toward resolving outstanding balances in an organized way.

What Is Asset Receivables Management?

Asset receivables management is the structured process of tracking, managing, and resolving amounts owed by individuals to creditors. These unpaid balances, often called receivables, are considered financial assets because they represent funds that are expected to be paid in the future.

For consumers, this process usually means that an outstanding balance, such as a credit card account, personal loan, or service bill, is being managed through an organized framework. The goal is to track the debt while creating a clear path toward resolution through communication, documentation, and repayment options.

Asset receivables management typically includes several key activities:

- Maintaining accurate records of outstanding balances

- Monitoring payment history and account status

- Communicating with account holders about the balance owed

- Offering repayment arrangements where appropriate

- Recording payments and updating account information

When handled properly, this process helps ensure that overdue accounts are managed responsibly while keeping communication clear and organized for everyone involved.

Why Asset Receivables Management Matters?

Asset receivables management plays an important role in bringing clarity and structure to outstanding accounts. Without a clear system for tracking and resolving overdue balances, both creditors and consumers can face confusion about account details, payment status, and next steps.

A structured receivables process helps address these challenges in several ways:

- Clear account visibility: Organized account records make it easier to understand the balance owed, payment history, and current account status.

- Consistent communication: Structured communication ensures that account holders receive clear information about their obligations and available repayment options.

- Improved resolution of outstanding balances: When accounts are managed systematically, it becomes easier to establish repayment plans and move toward resolving the balance.

- Reduced misunderstandings about the debt: Clear documentation and communication help prevent confusion about the origin of the account, the amount owed, or the repayment expectations.

For individuals dealing with an overdue account, asset receivables management helps create a more organized and transparent process that focuses on resolving the balance rather than leaving the situation uncertain.

Understanding the purpose of receivables management helps see how the process actually works, providing a clearer picture.

The Asset Receivables Management Process

Asset receivables management follows a structured lifecycle that tracks financial obligations from the moment credit is extended until the account is fully resolved. This lifecycle is part of the broader order-to-cash process, which begins when a sale occurs and ends when payment is collected and recorded.

Understanding each stage helps explain how receivable assets are monitored and eventually converted into actual payments:

1. Credit Evaluation and Approval

The receivables process often begins before a transaction occurs. When businesses allow purchases on credit, they evaluate whether the customer is likely to repay the obligation. This step helps reduce the risk of unpaid balances and protects the individual from potential bad debt.

Key activities in this stage include:

- Assessing creditworthiness and payment history: Customer’s past payment behaviour, financial stability, and credit records will be reviewed before approving credit. This evaluation helps determine whether the customer can responsibly manage delayed payment terms.

- Setting credit limits and repayment timelines: Credit policies establish how much credit can be extended and how long the customer has to repay the balance. Terms such as Net 30 or Net 60 define the expected payment window and may include incentives for early payment or penalties for delays.

- Documenting the financial agreement: The credit terms, payment conditions, and responsibilities of both parties are recorded, so expectations are clearly defined before the transaction takes place.

2. Invoice Creation and Delivery

Once goods or services are delivered, an invoice is issued to formally request payment. The invoice acts as the official financial management record that begins the receivable lifecycle.

Important elements included in invoices are:

- Detailed transaction breakdown: Invoices typically list the products or services provided, quantities, individual prices, taxes, and the total amount owed. This ensures transparency about how the final balance was calculated.

- Payment terms and due dates: The invoice clearly states when payment is expected, including the due date, accepted payment methods, and any late-payment conditions that apply if the balance is not settled on time.

- Delivery through financial communication channels: Invoices are sent through email, electronic invoicing systems, or traditional mail to ensure the customer receives the payment request promptly.

3. Payment Monitoring and Account Tracking

After an invoice is issued, the account enters a monitoring phase that tracks whether payment is made within the agreed timeframe.

Typical monitoring activities include:

- Tracking outstanding balances and invoice status: Financial systems track which invoices remain unpaid and categorize them by due dates. This allows individuals to see which payments are approaching deadlines or becoming overdue.

- Using receivables aging reports: Aging reports group invoices based on how long they have remained unpaid, such as 0–30 days, 31–60 days, or 90+ days. This helps identify accounts that may require follow-up.

- Maintaining accurate financial records: Every change in account status, including partial payments or adjustments, is recorded to ensure that the financial data reflects the most current account balance.

4. Collection Follow-Ups for Overdue Accounts

If payment is not received by the due date, the account moves into the collection stage. At this point, communication becomes more structured to encourage payment and clarify any issues preventing repayment.

This stage often includes:

- Sending payment reminders and follow-up notices: Automated reminders, emails, or letters may be sent shortly before or after the due date to notify the customer that payment is outstanding.

- Investigating potential billing disputes: Sometimes invoices remain unpaid because of billing errors, delivery issues, or discrepancies between the invoice and the original agreement. Addressing these issues helps resolve legitimate disputes.

- Escalating collection efforts when necessary: If initial reminders are ignored, additional communication steps may follow, including direct calls or structured collection workflows designed to bring the account toward resolution.

5. Repayment Discussions and Payment Arrangements

When customers are unable to pay the entire balance immediately, receivables management often shifts toward negotiation and resolution strategies.

Key activities during this phase include:

- Evaluating repayment capacity: Communication may focus on understanding the customer’s financial situation and identifying realistic repayment options.

- Creating structured payment plans: Installment agreements allow the balance to be repaid in smaller payments over time, which can increase the likelihood of recovering the outstanding amount.

- Documenting repayment agreements: Once an arrangement is agreed upon, the repayment terms and payment schedule are formally recorded to ensure both parties clearly understand the expectations.

6. Payment Processing and Application

When payments are received, they must be properly recorded and applied to the correct accounts. This stage ensures the financial records remain accurate.

Important activities include:

- Processing payments through secure systems: Payments may be received through bank transfers, online payment portals, or other approved channels designed to ensure security and transparency.

- Matching payments to specific invoices: Each payment must be reconciled with the corresponding invoice so that the correct balance is updated and accounting records remain accurate.

- Updating outstanding balances in real time: As payments are processed, account balances are adjusted to reflect the remaining amount owed.

7. Final Account Resolution

The final stage occurs when the balance is fully resolved. This may happen through complete repayment, fulfillment of a payment plan, or another agreed resolution.

At this point, the receivables system typically include:

- Confirming the balance has been satisfied: The account is updated to show that the financial obligation has been completed.

- Closing or updating the account status: The account is marked as resolved within the receivables management system.

- Maintaining documentation for auditing and reporting: Final account records are retained to ensure accurate financial reporting and compliance with accounting standards.

Also read: Debt Resolution Programs: How They Work and What to Expect

Because receivables management involves monitoring many accounts at once, individuals can rely on specific financial indicators to track payment progress and account performance.

Key Metrics Used in Asset Receivables Management

When an account becomes part of a receivables management process, it is usually monitored through specific financial indicators. These metrics help track how long balances remain unpaid, how repayment progress is developing, and whether accounts are moving toward resolution.

While individuals dealing with an outstanding balance do not need to calculate these metrics themselves, understanding them can help explain why certain follow-ups or repayment discussions occur.

- Days Sales Outstanding (DSO): Days Sales Outstanding measures the average time it takes for a balance to be paid after it becomes due. When accounts remain unpaid beyond expected timelines, they are more likely to enter structured receivables management processes and receive follow-up communication.

- Accounts Receivable Aging: Aging reports categorize outstanding balances based on how long they have been overdue, typically in ranges such as 1–30 days, 31–60 days, 61–90 days, and over 90 days past due. Accounts that remain unpaid for longer periods generally receive more attention because the likelihood of recovery decreases over time.

- Collection Effectiveness: Collection effectiveness measures how successfully overdue balances are resolved through payments, repayment arrangements, or settlements. Higher effectiveness indicates that communication and repayment options are helping accounts move toward resolution.

- Payment Completion Rate: This metric tracks how many agreed repayment plans are successfully completed. Consistent payments over time show that repayment arrangements are working and that outstanding balances are gradually being resolved.

- Bad Debt Rate: The bad debt rate reflects the percentage of accounts that remain unpaid and eventually cannot be recovered. Monitoring this helps identify accounts that may require earlier intervention or more structured repayment discussions.

While structured systems exist to manage overdue balances, individuals dealing with outstanding accounts often face real financial and practical challenges along the way.

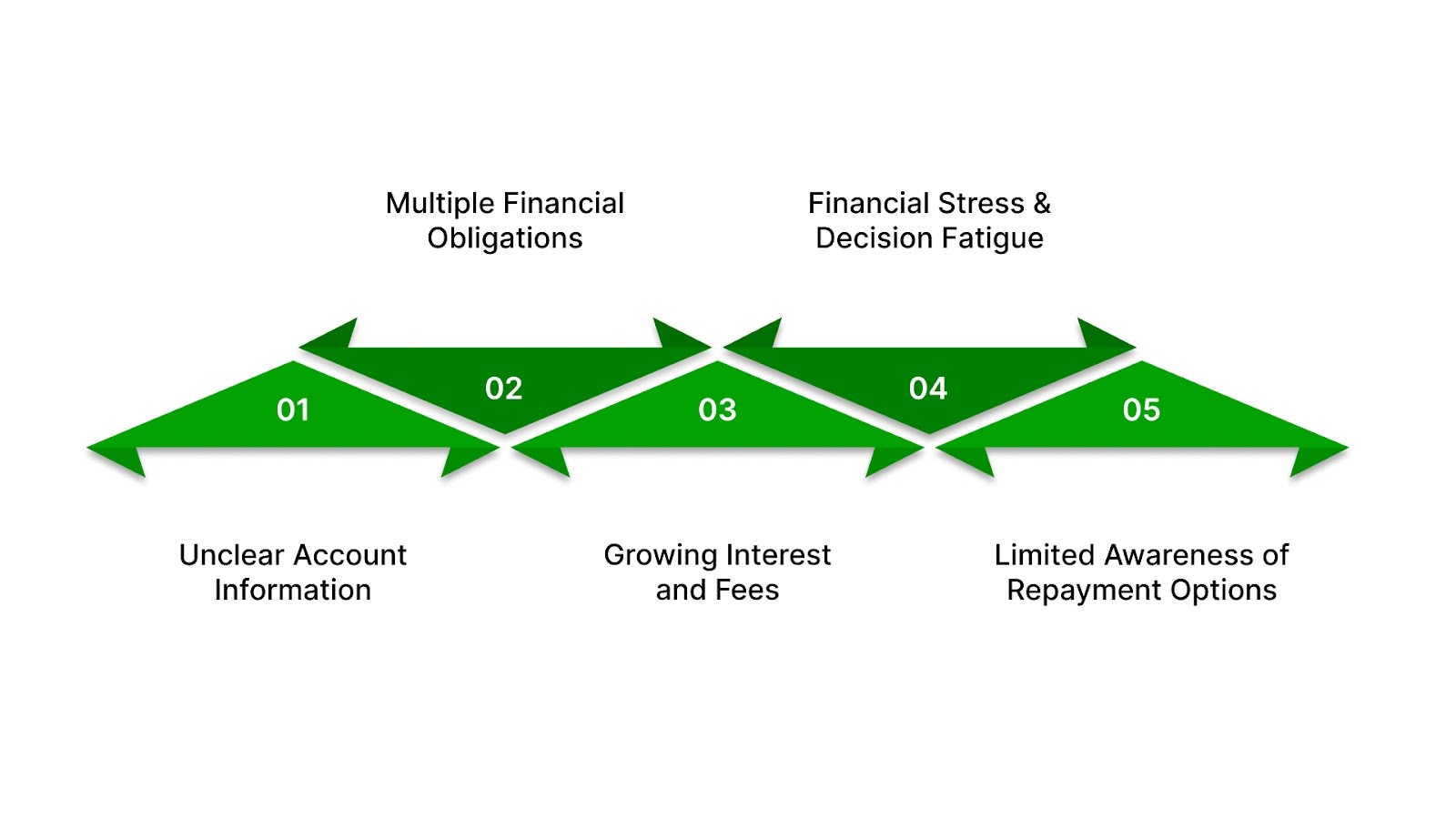

Challenges Consumers Face With Outstanding Accounts

Dealing with an overdue account can be stressful, especially when financial obligations begin to overlap with everyday living expenses. Many people do not fall behind intentionally. Job changes, unexpected costs, or temporary income disruptions can quickly affect someone’s ability to keep up with payments.

When accounts remain unpaid for longer periods, several practical challenges can make resolving the situation feel more complicated.

- Uncertainty About Account Details: Many individuals are unsure about the exact balance owed, the original creditor, or who is currently managing the account. When account information is unclear or spread across multiple statements and messages, it can make the situation feel confusing and harder to address.

- Multiple Financial Obligations at the Same Time: Rent, groceries, transportation, and other essential expenses compete with debt payments for the same monthly income. When several financial responsibilities occur at once, it can become difficult to decide which obligations to prioritize first.

- Accumulating Interest and Fees: Some outstanding accounts may continue to grow because of interest charges or late fees. When balances increase over time, it can make repayment feel more difficult, even if the person is trying to make progress.

- Financial Stress and Decision Fatigue: Money-related stress can affect how people make financial decisions. When someone is already dealing with financial pressure, reviewing account statements, negotiating repayment options, or organizing payment plans may feel overwhelming.

- Limited Understanding of Available Options: Many individuals are not aware that repayment plans, structured settlements, or other resolution options may be available. Without clear information, people may delay taking action simply because they are unsure about what steps they can take next.

Also read: Pay Recovery Guide: Resolve Debts Before They Escalate

When outstanding accounts become difficult to manage alone, working with an experienced receivables management partner can help bring structure and clarity to the process.

Conclusion

Outstanding accounts can feel overwhelming when payment timelines, balances, and communication become unclear. But asset receivables management exists to bring structure to this situation.

Understanding how receivables management works can help you approach the situation with more clarity and confidence.

If you’re dealing with an account that requires attention, The Forest Hill Management can help guide the process forward. Through structured account management, secure payment systems, and clear communication, Forest Hill Management supports individuals in understanding their accounts and working toward practical repayment solutions.

Take the first step toward resolving your outstanding account. Contact The Forest Hill Management today to review your options and move forward with greater clarity and confidence.

FAQs

1. Does asset receivables management affect my credit score?

It can, depending on how the account is reported to credit bureaus. If an account becomes significantly overdue or enters collections, it may appear on a credit report. Resolving the balance can help prevent further negative reporting.

2. What should I do if I believe the balance listed on my account is incorrect?

You should request verification of the debt and review any account statements or documentation provided. If you believe there is an error, you can dispute the balance and request clarification before making payments.

3. Can overdue accounts be resolved without paying the full balance at once?

In many cases, repayment arrangements can be discussed that allow balances to be paid over time. These structured plans help make repayment more manageable for individuals facing financial pressure.

4. How long can an unpaid account remain active?

The timeline varies depending on the original agreement, creditor policies, and applicable state laws. Some accounts may remain active for several years if they are not resolved or legally discharged.

5. What information should I gather before discussing repayment options?

It helps to review your recent account statements, payment history, and any communication you received about the balance. Having this information available makes it easier to understand your options and discuss possible repayment arrangements.