Can a Debt Collector Take Your Car? Essential Facts

Transform Your Financial Future

Contact UsMany people worry that falling behind on payments could mean losing their car. While lenders may have the right to repossess a vehicle tied to an auto loan, debt collectors generally do not. The laws surrounding this are often misunderstood, leading people to assume the worst.

According to the Consumer Federation of America, Americans collectively owe over $1.66 trillion in auto loan debt. Delinquencies for 90+ days are now at their highest levels since before the Great Recession. If these numbers represent more than statistics for you, this guide is for you.

In this guide, we will explain what debt collectors can and cannot do, when repossession is legal, and how to protect your vehicle and your rights if you are struggling with auto-related debt.

Here's the short version:

- Debt collectors cannot take your car without legal authority. Only lenders on secured auto or title loans can initiate repossession, and even then, they must follow state laws.

- Unsecured debts do not permit repossession. Credit cards, personal loans, and medical debts are not tied to your vehicle, so collectors cannot seize it without first obtaining a court judgment.

- A judgment lien is a legal claim, not immediate possession. It may restrict your ability to sell or transfer a car, but it does not mean someone can take it from you overnight.

- Threats of repossession are often illegal. Under the FDCPA, collectors cannot use intimidation, false claims, or harassment to pressure you into paying.

- Understanding your debt type protects your rights. Knowing whether your debt is secured, unsecured, or judgment-based helps you respond calmly and avoid being misled by unlawful collection tactics.

What Debt Collectors Can and Cannot Do

Debt collectors are responsible for collecting payments on behalf of lenders or creditors, but their authority has limits, especially when it comes to property. Under federal law, particularly the Fair Debt Collection Practices Act (FDCPA), collectors cannot seize assets or use threats, harassment, or intimidation to recover payments.

The FDCPA was created to protect consumers from unfair or abusive collection practices, ensuring that all communication remains professional, truthful, and within legal boundaries.

The table below breaks down what debt collectors can and cannot do under federal law:

It is important to remember that debt collectors are not lenders. They cannot repossess your vehicle unless a court order or legal judgment grants that right. Any claim or threat of immediate repossession from a debt collector should be viewed as a potential FDCPA violation.

To understand whether your car is truly at risk, you first need to know the conditions under which repossession is legally permitted. This is covered in the next section.

Suggested Read: Is Paying Debt Collection Agencies a Bad Idea?

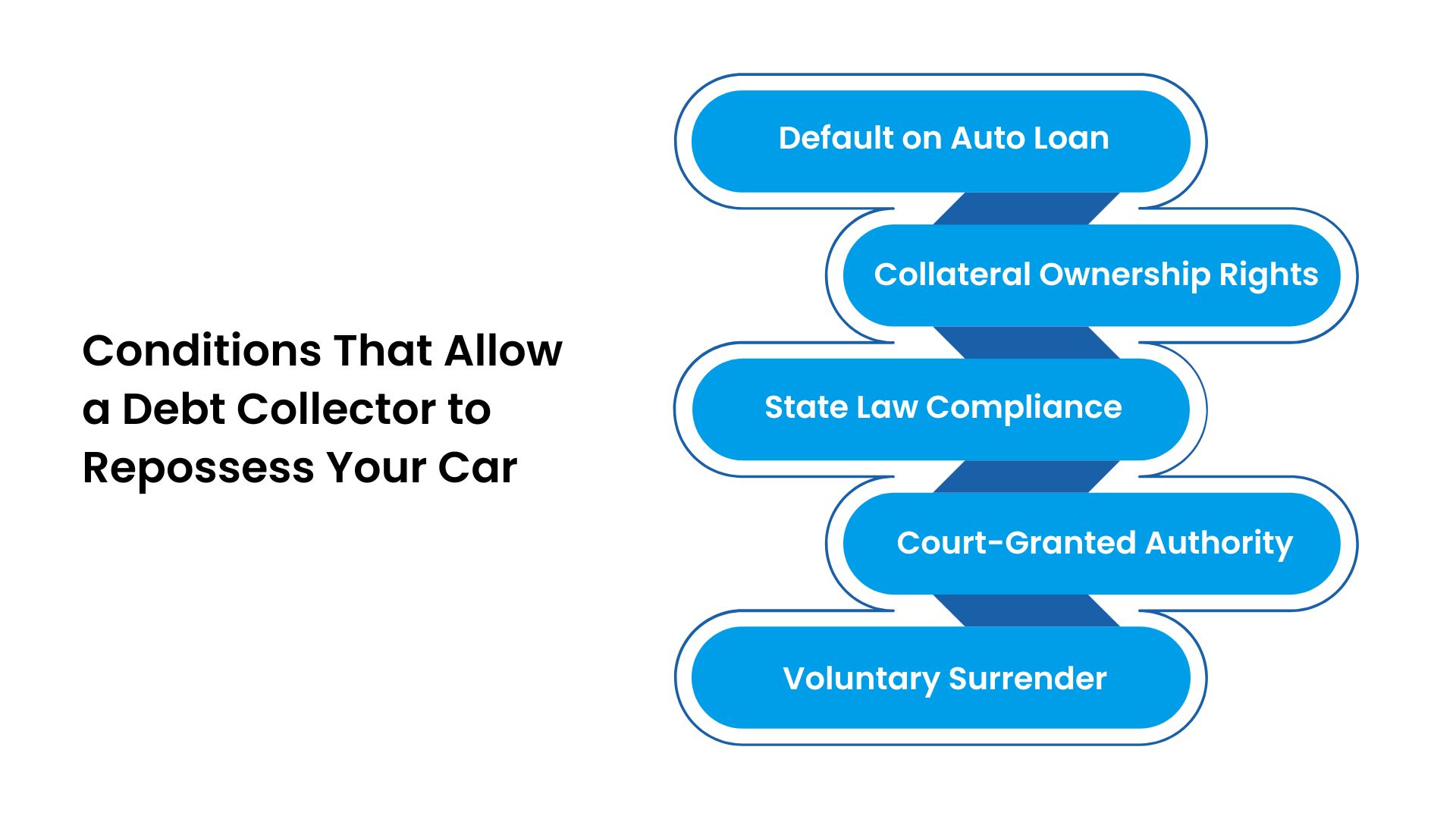

Conditions That Allow a Debt Collector to Repossess Your Car

Repossession usually happens with auto loans or title loans, where the vehicle itself acts as collateral. In these cases, the lender, not the debt collector, holds the legal right to take back the car if payments are missed or the loan terms are violated.

This process applies only to secured loans, meaning the debt is directly tied to the car. For unsecured debts such as credit cards, medical bills, or personal loans, a collector cannot legally repossess your vehicle without a court order or judgment.

Here are the main conditions under which a vehicle can be repossessed:

- Default on a Secured Auto Loan: If you fall behind on payments for a car loan or title loan, the lender may initiate repossession according to your contract.

- Legal Ownership of Collateral: The lender must have a valid lien on the vehicle’s title. This is proof that the car secures the loan.

- State Law Compliance: Some states require advance written notice before repossession, while others allow “self-help” repossession as long as it does not involve force or breach of peace.

- Court-Granted Authority: A debt collector can only repossess property if a court judgment allows them to claim it.

- Voluntary Surrender: Borrowers sometimes choose to return the vehicle to reduce fees and credit impact.

At Forest Hill Management, we take a different approach. Our goal is to help individuals manage repayment ethically and respectfully. We offer flexible plans, secure online systems, and personalized financial guidance that makes repayment smoother and never intimidating. Speak to our financial advisors today.

But what if your car is not tied to a loan: can a collector still take it? That is where judgment liens come in.

Suggested Read: Top 12 Proven Steps to Becoming Financially Stable

What Is a Judgment Lien? Can It Affect Your Car?

A judgment lien is a legal claim a creditor can place on your property, such as your car, home, or other assets, after winning a lawsuit against you for unpaid debt.

Unlike repossession, which applies only to secured loans, a judgment lien can arise from unsecured debts (like credit cards or medical bills) once a court has issued a final ruling. It does not happen automatically; it is the result of a legal process that requires notice, documentation, and your right to respond.

Here is what you should know about judgment liens:

- They Follow a Court Judgment. A creditor or collector must first sue and win in court before a lien can be attached to your property.

- They Allow Creditors to Claim Value, Not Possession. A lien means the creditor has a right to part of the property’s value if you sell it — not the right to take it immediately.

- They Are Governed by The State Law. Each state has its own limits on what property can be liened, and many protect personal vehicles up to a certain dollar amount.

- They Expire Over Time. Most liens last between five and twenty years, depending on state law, and may be renewed only under specific conditions.

- They Are Public Record. You can confirm if a lien exists by checking county or state court records. This is an important step in protecting your assets.

It is important to understand that a debt collector cannot show up and take your car. Only a valid court judgment can create a lien, and even then, state laws protect basic personal property.

To protect yourself, the next step is to identify the type of debt you have (secured, unsecured, or judgment-based), as each carries different rules and consequences.

Suggested Read: The Ultimate Guide to Repair Your Credit Fast: 8 Sure Steps for a Stronger Score

Identifying the Type of Debt You Have

Whether or not your car can be repossessed depends on how your debt is classified: secured, unsecured, or judgment-based. Each category has different protections and risks.

Under the Fair Debt Collection Practices Act (15 U.S.C. § 1692), debt collectors are prohibited from taking or threatening to take any property without a legal right to do so.

That means knowing your debt type helps you recognize when a collector’s action or threat crosses a legal line.

Table showing how these debt types differ:

Knowing these distinctions helps you see where the real risk lies and where fear is unnecessary. To make it clearer, let us look at how these scenarios might play out in everyday life.

Illustrative Case Study: How Debt Type Determines What Happens to Your Car

Scenario 1: Secured Debt (Auto Loan)

Dan purchased a car through a secured auto loan. After several missed payments, his lender sent a notice of default explaining that the car could be repossessed if he did not bring the account current. When Dan failed to respond within the grace period, the lender (not a third-party collector) lawfully repossessed the car under the loan agreement.

Dan still owed the balance remaining after the car was sold, but the process was entirely legal because the loan was secured by the vehicle.

Scenario 2: Unsecured Debt (Credit Card)

Rachel fell behind on a $3,000 credit card balance. A collection agency began contacting her about repayment, but she worried they might “take her car” since she could not pay right away. In truth, they could not.

Her credit card debt was unsecured since it was not connected to any asset. The collector could call, send letters, or report the debt to credit bureaus, but they had no right to seize her vehicle without first suing and obtaining a judgment.

Scenario 3: Judgment Debt (Court-Ordered Lien)

Marcus had an unpaid personal loan that went to court after months of nonpayment. The creditor won a judgment, and a lien was placed on Marcus’s car. This meant he could not sell or refinance the vehicle until the lien was satisfied.

However, state law protected his primary car from being taken because its equity value was below the exemption threshold. The lien affected his credit and limited his financial options, but it did not result in repossession.

Each case shows how the nature of your debt determines the outcome and not the intensity of the collector’s demand. A debt collector cannot take your car unless the law and your loan agreement specifically allow it.

Understanding what type of debt you have is the first step in protecting your rights. The next is knowing what to do if a debt collector threatens to take your car, even when they legally cannot.

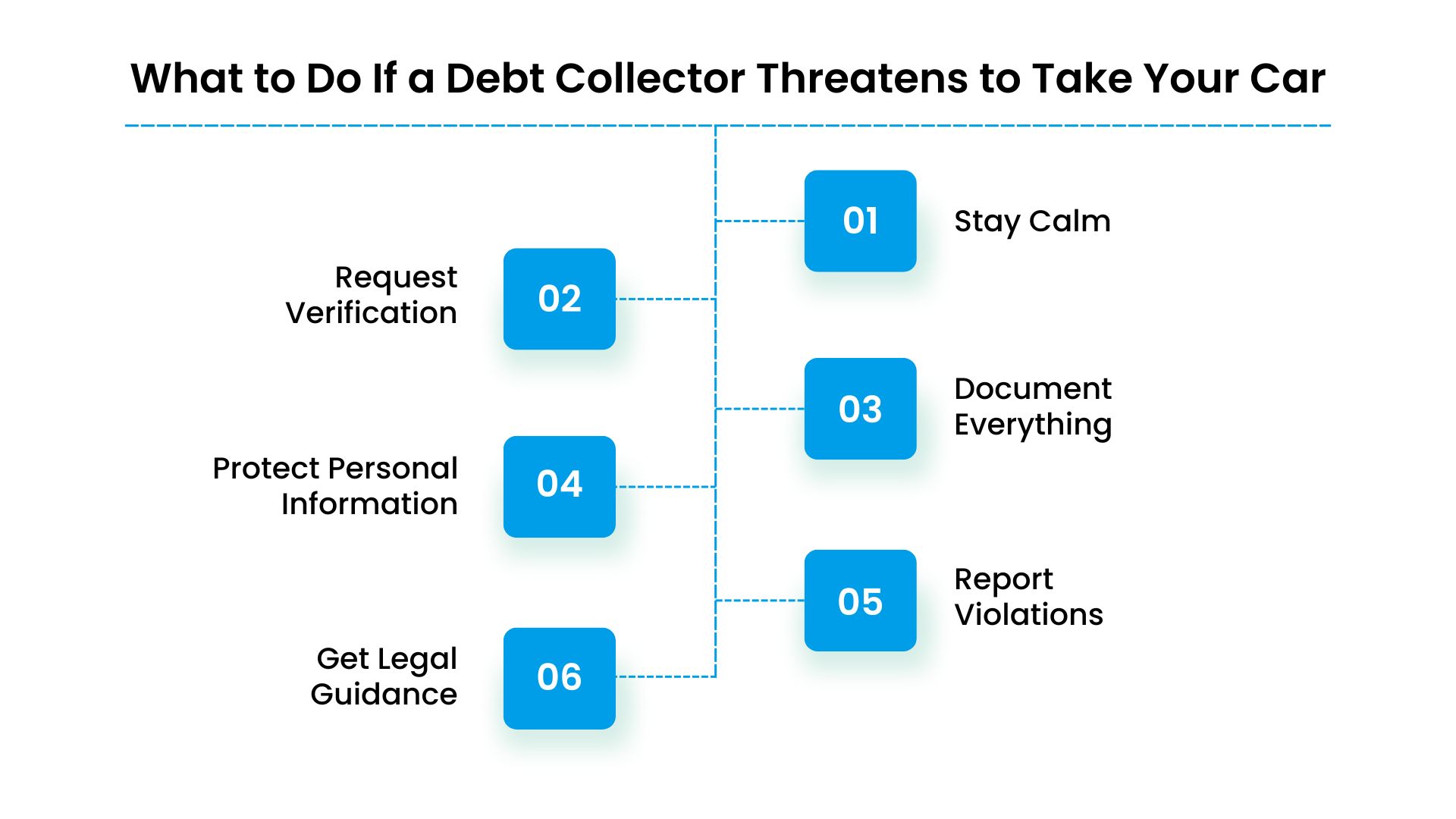

What to Do If a Debt Collector Threatens to Take Your Car

Several debt collectors use intimidation or misinformation to scare people into paying quickly, even when they have no legal right to do so. The Federal Trade Commission (FTC) regularly publishes a “wall of shame,” listing collectors and agencies banned from the industry for harassment, false threats, and illegal practices.

Many of those cases involved collectors falsely claiming they could seize cars or personal property. Knowing your rights is your strongest defense against these tactics.

If a debt collector threatens to take your car, here is what you should do immediately:

- Stay Calm. Do not react emotionally or make quick decisions. Take time to confirm whether the debt is even connected to your car.

- Request Verification. Ask the collector for written proof of the debt and the creditor’s details before taking any action.

- Document Everything. Keep notes, call logs, and copies of letters or emails in case you need to file a formal complaint.

- Protect Personal Information. Never share financial or identification details until you confirm the agency’s legitimacy.

- Report Violations. File complaints with the CFPB, FTC, or your state attorney general if a collector uses threats or harassment.

- Get Legal Guidance. Speak to a consumer rights attorney if the collector persists or you receive court-related documents.

At Forest Hill Management, we take pride in doing things the right way. We do not threaten, harass, or misrepresent our authority — ever. Our approach centers on transparent communication, flexible repayment plans, and ethical collection practices that respect your rights and dignity. Contact us today.

Knowing how to respond to false threats is crucial, but so is protecting your assets before problems arise. Next, we will explore how to shield your car and your credit during the debt collection process.

How to Shield Your Car and Credit During Debt Collection

There are proactive ways to protect both your car and your credit profile, even while navigating overdue payments. Shielding yourself requires using smart, lawful strategies that keep you one step ahead and prevent avoidable damage.

Here are some practical strategies that go beyond the basics:

- Engage Before You Default

Contact your lender or collection agency as soon as you anticipate trouble. Early communication can open doors to deferments or restructured plans that prevent repossession or lawsuits.

- Negotiate Interest Adjustments

If your debt has grown due to compounding interest, ask for a rate reduction or temporary freeze. Many collectors prefer a steady, lower-rate payment plan over an uncollectible account.

- Request a “Pay for Delete” Agreement

In limited cases, a collector may agree to remove a collection entry from your credit report once the debt is paid in full. However, always get this agreement in writing before paying.

- Use a Separate, Controlled Payment Account

Set up a low-balance checking account solely for debt payments. This reduces exposure and prevents collectors from accessing your main funds through ACH authorizations.

- Monitor Your Credit Reports Quarterly

Check for duplicate entries or errors. Dispute any inaccurate or outdated information. Even one wrongful report can impact future credit access.

- File a “Cease and Desist” if Harassed

If a collector crosses legal lines, a formal written request to stop communication compels them to respond only through official notice or legal channels.

- Document Every Payment and Promise

Keep written confirmation for every settlement, payment plan, or communication. It prevents future disputes and strengthens your position if issues arise.

- Preserve Your Car’s Title Integrity

Regularly check with your state DMV to ensure no unauthorized lien or title hold has been added. Fraudulent claims do happen, especially when accounts are sold multiple times.

Protecting your car and credit during debt collection is about being strategic, not reactive. Staying informed, keeping records, and maintaining composure can make all the difference between a stressful experience and a manageable one.

If you are already working with a debt collection agency, knowing your options and your rights can make repayment far less stressful.

Suggested Read: How to Recover from Debt: A Simple, Step-by-Step Guide (2025 Update)

Forest Hill Management Values Respect Over Pressure

At Forest Hill Management, we believe that debt resolution should be rooted in understanding, not intimidation. We are a professional debt management organization that helps individuals navigate repayment with clarity, structure, and compassion.

Here is what we offer:

- Personalized Repayment Plans: Every financial situation is different, so we work with you to create a plan that fits your budget and helps you move forward at a sustainable pace.

- Secure Online Payment System: Our platform allows you to make payments safely and conveniently, with full transparency and instant confirmation.

- Flexible Scheduling Options: We understand life changes. Our flexible arrangements adapt to your income flow, ensuring consistency without added stress.

- Clear Communication: You will always know where your account stands. We communicate honestly, professionally, and in compliance with the Fair Debt Collection Practices Act (FDCPA).

- Financial Guidance and Support: Our advisors can help you understand your options, manage your repayment plan effectively, and build confidence in your financial future.

We recognize that financial setbacks can happen to anyone. That is why our approach focuses on building trust and providing realistic solutions rather than adding pressure. When we work with you, our goal is to help you take control of your financial obligations in a way that supports your long-term stability.

Conclusion

Falling behind on payments can feel overwhelming, but the reality is often less dire than it seems. In most cases, debt collectors cannot legally take your car or personal property without proper authorization. Understanding your rights, the type of debt you owe, and the steps you can take to protect yourself can replace fear with clarity.

At Forest Hill Management, we are here to make that path clearer and calmer. We provide transparent communication, flexible repayment options, and secure online systems that allow you to manage debt responsibly. Our financial advisors will work with you without intimidation or pressure.

Know your rights. Know your options. Work with professionals who value respect over pressure. Contact us today.

Frequently Asked Questions

1. Can My Car Be Repossessed Without Warning?

In some states, lenders are allowed to repossess vehicles without prior notice once you default on a secured auto loan. However, they must still follow state laws and cannot “breach the peace” during repossession. It is always best to review your loan agreement to see if a notice period applies in your state.

2. What Happens to My Debt After My Car Is Repossessed?

If your car is sold after repossession, the sale proceeds are applied to your remaining balance. If there is still a shortfall, known as a deficiency balance, you may still owe that amount. Collectors may contact you about repayment, but they cannot add unauthorized fees or act outside FDCPA guidelines.

3. How Long Does a Judgment Lien Stay on My Record?

Judgment liens typically remain in effect for 5 to 20 years, depending on your state’s laws. They can sometimes be renewed, but once the debt is paid, the lien should be released. Always request a written release once the balance is settled to avoid future complications with your title or credit report.

4. Can Debt Collectors Garnish My Wages Without a Court Order?

No. Wage garnishment for consumer debt requires a court judgment. If a collector threatens garnishment without one, it is a violation of the Fair Debt Collection Practices Act (FDCPA) and should be reported to the Consumer Financial Protection Bureau (CFPB).

5. What Should I Do If I Suspect a Fake Debt Collector?

Ask for written verification immediately. Legitimate collectors must send documentation that clearly identifies the creditor, the balance owed, and your rights to dispute it. Do not share personal or financial information until you verify the agency through official records or the CFPB’s complaint database.