6 Personal Debt Relief Options 2026 Ranked by Risk, Cost, and Results

Need Help Reviewing Your Account?

Contact UsDebt relief often sounds like a promise. A reset. A way to make everything easier overnight. But when you actually start looking into it, the options can feel confusing, even contradictory. Some claim to reduce your debt, others reorganize it, and a few come with risks that are not always obvious at first.

And this is not a rare situation. In Q4 2026, U.S. credit card debt alone crossed $1.28 trillion, with millions of individuals carrying balances month to month.

At the same time, delinquency rates have risen to nearly 4.8% of total household debt, showing that more people are struggling to keep up with payments.

This is exactly why understanding your options matters. Not just what they are called, but how they actually work in real situations.

In this blog, you will learn the top personal debt relief options in 2026, how each approach works, what trade-offs to expect, and how to choose a path that helps you move forward with clarity.

Key Takeaways

- Debt relief is not a single solution but a range of structured approaches that help manage, reduce, or resolve debt over time.

- Different options such as consolidation, settlement, or structured repayment come with varying trade-offs in cost, time, and credit impact.

- Debt relief companies typically help by organizing payments, negotiating terms, or providing clarity and structure around your accounts.

- Structured repayment approaches often provide more transparency and stability compared to negotiation-based solutions that carry higher risks and fees.

- Choosing the right option depends on your financial situation, ability to make consistent payments, and understanding of the risks involved.

What Does a Debt Relief Company Do?

A debt relief company helps you manage, restructure, or resolve outstanding debt through different approaches depending on your situation. The goal is not to erase debt instantly, but to create a clearer, more manageable path toward resolving what you owe.

- Structured account support and repayment guidance: This approach focuses on helping you clearly understand your account, including balances, history, and next steps, while offering structured repayment options. It avoids third-party complexity and keeps the process transparent, secure, and focused on steady resolution.

- Negotiating with creditors on your behalf: Some companies act as intermediaries and attempt to negotiate reduced balances or revised repayment terms with creditors. This can sometimes lower the total amount owed, but outcomes are not guaranteed and often involve fees and credit impact.

- Creating structured repayment plans: Certain services organize your debts into a single monthly payment with a defined timeline, making repayment more predictable. These plans improve consistency and structure but usually do not reduce the original principal amount.

- Assessing your financial situation and recommending options: Many providers begin by reviewing your income, expenses, and outstanding balances to suggest suitable debt relief paths. This helps you understand what options are realistic and what trade-offs each one involves before making a decision.

- Consolidating multiple debts into one payment structure: Some services help combine several debts into a single loan or payment plan, simplifying tracking and management. While this can make repayment easier to follow, it typically does not reduce the total debt owed.

- Managing communication and documentation: Debt relief companies often handle account records, payment tracking, and communication related to your debt. This helps reduce confusion, especially when accounts are transferred or involve multiple parties, and ensures information remains consistent and organized.

Understanding these roles helps you see that debt relief is about changing how your debt is handled.

Also read: How to Handle Debt Collector Calls Effectively

With this clarity in place, the next step is to look at the most common personal debt relief options available in 2026 and how each one works in practice.

Types of Personal Debt Relief Options in 2026

There is no single way to approach debt relief. In 2026, several structured options are available, each designed for different financial situations. Some focus on simplifying payments, others on reducing balances, and some on legally resolving debt.

The key is understanding how each option works in practice so you can choose a path that aligns with your situation.

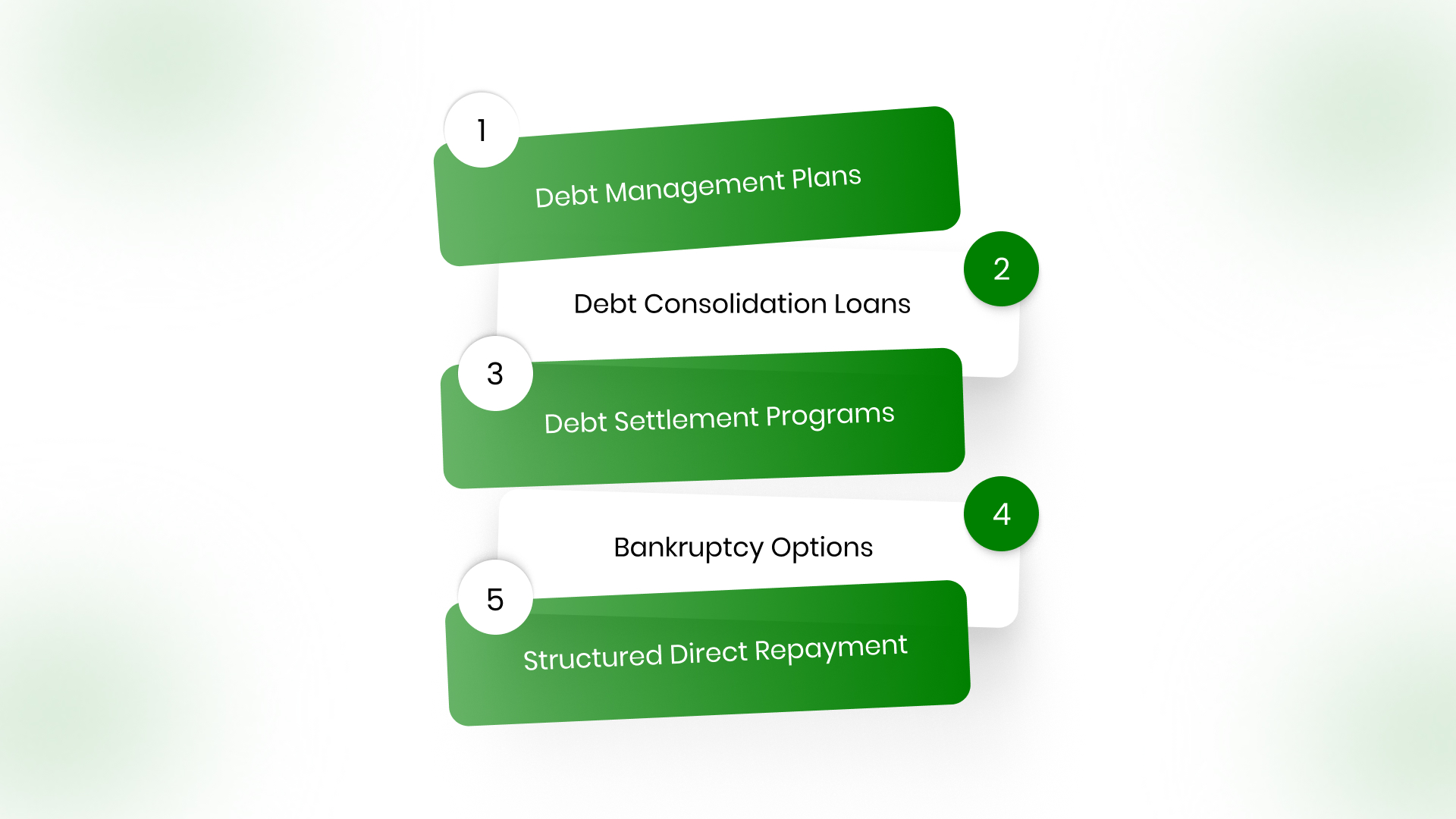

1. Debt Management Plans (DMPs)

A Debt Management Plan is a structured repayment program typically arranged through credit counseling services. It is designed to help you manage multiple unsecured debts through a single, organized payment.

How it works:

- Multiple debts are combined into one monthly payment

- Interest rates may be reduced depending on agreements

- The plan usually runs for 3 to 5 years

Pros:

- Predictable and structured repayment schedule

- Less severe impact on credit compared to more aggressive options

Considerations:

- Requires consistent monthly payments over several years

- Does not reduce the total principal owed

2. Debt Consolidation Loans

Debt consolidation involves taking out a new loan to pay off multiple existing debts. The goal is to simplify repayment and potentially reduce interest costs.

How it works:

- A single loan replaces multiple balances

- Interest rate may be lower if you qualify

- Fixed repayment timeline is established

Pros:

- Easier to track and manage one payment

- Clear repayment structure with defined end date

Risks:

- Approval often depends on your credit profile

- If spending habits continue, new debt can accumulate alongside the consolidated loan

3. Debt Settlement Programs

Debt settlement focuses on negotiating with creditors to reduce the total amount owed. This option is often considered during significant financial hardship.

How it works:

- Negotiations aim to settle debt for less than the full balance

- Typically takes 24 to 48 months

- Payments may be paused during negotiation periods

Pros:

- Potential to reduce the overall debt amount

Risks:

- Credit score can drop significantly during the process

- Fees can range between 15% and 25% of the enrolled debt

- Does not prevent potential legal action from creditors

4. Bankruptcy (Chapter 7 & Chapter 13)

Bankruptcy is a formal legal process designed to resolve debt when repayment is no longer feasible under normal conditions.

Considerations:

- Long-term impact on credit history

- Legal process that requires careful evaluation

- May affect future borrowing ability

5. Direct Repayment with Structured Support

In many cases, debt can be resolved by working directly through a structured repayment approach, without involving third-party negotiation or complex financial products.

How it works:

- You gain a clear understanding of your account details, balances, and obligations

- Repayment is organized into defined, manageable payment plans

- Communication remains direct, transparent, and consistent

Key benefits:

- Clarity from the start: You know exactly what you owe, who you are dealing with, and what steps are required. This removes the uncertainty that often comes with third-party programs.

- No hidden fee structures: Unlike some relief options that involve high service fees, structured repayment focuses directly on resolving the balance itself.

- Lower risk of complications: There is no dependency on negotiations that may or may not succeed, and no added risk of delayed communication or legal uncertainty.

- Consistent and trackable progress: Payments are applied directly toward your balance, allowing you to see steady, measurable improvement over time.

- Better alignment with long-term stability: Instead of short-term relief with long-term consequences, this approach focuses on resolving debt in a way that supports financial consistency and control.

Also read: How to Easily Track All Your Debts in One Place

For many individuals, the biggest challenge is not just the debt itself, but the lack of clarity around it. Structured repayment removes that confusion. It replaces uncertainty with a clear path, defined steps, and steady progress, making it one of the most stable and transparent ways to move toward becoming debt-free.

Top Debt Relief Options for Personal Debt in 2026

In 2026, several well-known debt relief companies offer structured ways to manage or reduce personal debt. Each company follows a different approach, from negotiation-based settlement to structured repayment planning. Understanding how they work helps you decide what aligns best with your situation:

The Forest Hill Management

The Forest Hill Management focuses on structured account resolution and repayment clarity, rather than negotiation-heavy or high-risk approaches. The emphasis is on helping you understand your account and move toward resolution with transparency and consistency.

- Clear account visibility and documentation: You get a structured view of your balance, payment history, and account status, reducing confusion and helping you make informed decisions.

- Defined and manageable repayment options: Payment plans are structured based on your situation, allowing steady progress without relying on uncertain negotiations.

- Compliance-focused communication: All interactions follow regulated standards, ensuring your rights and data are protected throughout the process.

- Secure and direct payment systems: Payments go directly toward resolving your balance, making progress trackable and transparent.

- Focus on long-term resolution: Instead of quick but uncertain outcomes, the approach prioritizes stability, clarity, and consistent progress.

National Debt Relief

National Debt Relief is one of the largest debt settlement companies, focusing on negotiating unsecured debts like credit cards and personal loans.

- Negotiation-based debt settlement programs: The company works with creditors to reduce the total balance owed, often targeting partial repayment agreements.

- No upfront fee structure: Fees are typically charged only after successful settlements are reached.

- Client dashboards for tracking progress: Users can monitor settlements and account activity through structured online systems.

- Works with various unsecured debts: Includes credit cards, medical bills, and personal loans.

Freedom Debt Relief

Freedom Debt Relief is one of the most affluent debt settlement providers, helping consumers negotiate lower balances on unsecured debt.

- Settlement-based approach to reduce total debt: The company negotiates with creditors after you build savings in a dedicated account.

- Programs typically last 24–48 months: Debts are settled one by one over time through structured negotiation.

- Legal support network available: Offers access to legal guidance in some cases during the process.

- High fees and credit impact considerations: Fees can reach up to 25% of enrolled debt, and credit scores may be significantly affected.

Accredited Debt Relief

Accredited Debt Relief specializes in handling larger unsecured debts and settlement programs.

- Focus on high-debt clients (typically $10,000+): Designed for individuals with substantial unsecured balances.

- Negotiated settlements with creditors: Works to reduce total debt through structured agreements.

- Typical fees range between 18%–25%: Fees are based on the enrolled debt amount.

- Covers multiple debt types: Includes credit cards, medical bills, and personal loans.

CuraDebt

CuraDebt offers a mix of debt settlement and management services, including specialized support for certain debt types.

- Settlement and debt management plan options: Provides both negotiation-based and structured repayment approaches.

- Supports a wider range of debts: Includes tax debt and some business-related obligations.

- Custom evaluation of financial situations: Helps determine which path fits based on your financial profile.

- Focus on flexibility across different debt categories: Useful for individuals with mixed types of debt.

Pacific Debt Relief

Pacific Debt Relief is known for its structured settlement programs and customer-focused approach.

- Negotiation-focused debt settlement services: Aims to reduce balances through creditor agreements.

- Transparent process and communication: Emphasizes clarity around timelines and program structure.

- Tailored plans based on financial hardship: Designed for individuals struggling with unsecured debt repayment.

- Recognized for overall value and service quality: Often highlighted for balancing cost and outcomes in settlement programs.

These companies represent different ways of approaching debt relief:

- Settlement-based models focus on reducing balances but involve fees, timelines, and credit impact

- Structured repayment approaches focus on clarity, consistency, and steady resolution

Understanding how each company works helps you move beyond marketing claims and choose a path that fits your financial situation with fewer surprises along the way.

How to Choose the Right Debt Relief Option

Choosing the right debt relief option is not about finding a quick fix. It is about selecting an approach that fits your financial reality, your capacity to manage payments, and the level of risk you are comfortable with. A structured way of thinking about this can help you make a more informed and confident decision.

- Understand your financial situation clearly: Start by identifying whether your situation is temporary or long-term. If your financial strain is short-term, options that restructure payments may be sufficient. If challenges are ongoing, you may need a more structured or formal resolution approach. This distinction helps avoid choosing a solution that does not match your actual needs.

- Assess your ability to make consistent payments: Most debt relief options depend on regular, sustained payments. Review your income, essential expenses, and available balance to determine what you can realistically commit each month. A plan that is manageable over time is far more effective than one that feels aggressive but cannot be maintained.

- Evaluate your risk tolerance carefully: Each option comes with trade-offs. Some may affect your credit more significantly, while others may involve legal or financial risks. It is important to consider how comfortable you are with potential credit impact, additional fees, or uncertainty around outcomes before making a decision.

- Weigh structure against speed: Some debt relief options aim for faster resolution but may involve higher costs or risks. Others focus on structured, predictable repayment over a longer period. Deciding between these depends on whether you prioritize immediate results or long-term stability and clarity.

- Use a simple self-check before committing: Pause and ask yourself a few key questions:

- Can I realistically maintain the required monthly payments over time?

- Do I fully understand all fees, timelines, and conditions involved?

- Is this option actually reducing my debt, or simply restructuring it?

This approach helps you move beyond surface-level comparisons and choose a path that is practical, sustainable, and aligned with your financial situation.

Conclusion

Debt relief is often presented as a solution, but in reality, it is a set of choices. Each option comes with its own structure, timelines, and consequences. The difference lies in how clearly you understand those trade-offs before you commit.

What tends to work best is not the fastest or most aggressive option, but the one you can follow consistently without added confusion or risk. When you have clear account information, defined repayment steps, and reliable communication, the process becomes far more manageable.

If your account is being handled by The Forest Hill Management, the focus is on giving you that structure. You are not left guessing what comes next. You have visibility, support, and a practical way to move toward resolution at a pace that fits your situation.

You do not need to solve everything at once. You just need a clear next step.

Take that first step toward financial clarity with The Forest Hill Management.

FAQs

1. How long does it usually take to become debt-free using relief options?

Timelines vary depending on the approach. Some structured repayment plans may take a few years, while settlement or legal options can differ based on complexity and progress.

2. Can I handle debt relief on my own without a company?

Yes, many individuals manage repayment directly by organizing their accounts and creating a structured payment plan. External support may help with clarity, but it is not always required.

3. Will all creditors agree to reduced payments or settlements?

Not always. Agreements depend on individual creditor policies, account status, and your financial situation, which means outcomes can vary.

4. Are there risks in delaying action on unpaid debt?

Delaying action can lead to increased balances, added fees, or escalation in the account status. Addressing the situation early often provides more flexibility.

5. How can I tell if a debt relief option is too risky for me?

If the option involves unclear fees, uncertain outcomes, or commitments you cannot realistically maintain, it may not be the right fit for your situation.