Distressed Debt Portfolio Management: Meaning, Risk and Recovery

Need Help Reviewing Your Account?

Contact UsFinancial setbacks rarely happen all at once. A missed payment, a sudden expense, or a temporary drop in income can slowly turn manageable balances into overdue accounts. Over time, these unpaid obligations can become part of what financial institutions refer to as distressed debt.

This situation is more common than many people realize. In fact, U.S. household debt reached $18.8 trillion in 2025, and about 4–5% of that debt is currently in delinquency, meaning payments are already behind. As these overdue accounts grow, they often require structured management to help borrowers and creditors work toward resolution.

Understanding how distressed accounts are handled can make the process far less confusing. With the right information and support, resolving past-due balances becomes a clearer and more manageable step.

In this blog, we’ll explain what distressed debt portfolio management means, why distressed accounts occur, the risks involved, and the strategies used to recover and resolve these accounts responsibly.

Key Takeaways

- Distressed debt portfolio management refers to the structured process of organizing and resolving accounts where borrowers are unable to meet their financial obligations on time.

- Distressed portfolios often develop due to economic downturns, personal financial disruptions, credit risk exposure, or operational gaps in collections management.

- Managing distressed accounts involves multiple risks, including recovery uncertainty, regulatory compliance requirements, operational complexity, and potential reputation damage.

- Effective recovery strategies rely on structured approaches such as portfolio segmentation, data-driven analysis, consumer-friendly repayment options, and compliant communication practices.

- Consumers facing past-due accounts can often resolve them through clear communication, secure payment options, and flexible repayment plans provided by servicing organizations like Forest Hill Management.

What Is Distressed Debt Portfolio Management?

Distressed debt portfolio management refers to the structured process of managing accounts where borrowers are struggling to meet their financial obligations. These accounts may already be in default or approaching default, making recovery more complex than standard credit servicing.

Distressed debt generally arises when individuals or businesses face significant financial challenges such as income loss, business disruption, or mounting financial obligations. Because repayment becomes uncertain, these debts are often valued at a significant discount compared with their original balance.

When multiple distressed accounts accumulate, they form a distressed debt portfolio. Lenders, financial institutions, or portfolio buyers may hold these collections of past-due accounts, each with varying levels of risk, repayment potential, and regulatory considerations.

Effective distressed debt portfolio management focuses on organizing and servicing these accounts in a structured way. Rather than treating all delinquent accounts the same, organizations apply strategic oversight to determine how each account should be handled.

This process typically includes several key activities:

- Assessing portfolio risk by reviewing account history, borrower behavior, and likelihood of repayment

- Prioritizing accounts based on recoverability, allowing teams to focus efforts where resolution is most achievable

- Managing collections and repayment discussions in a clear and responsible manner

- Ensuring legal and regulatory compliance throughout all communications and servicing activities

For many lenders, managing distressed portfolios internally can become resource-intensive. Handling large volumes of delinquent accounts requires specialized systems, regulatory oversight, and experienced teams capable of navigating sensitive consumer interactions.

As a result, many organizations choose to work with specialized receivables management partners that focus on distressed portfolio servicing. These firms provide structured portfolio oversight, compliance-focused communication practices, and technology-driven processes that help creditors manage past-due accounts while maintaining transparency and regulatory alignment.

Also Read: Guide to Debt Portfolio Analysis: Definition and Compliance

Now that the concept of distressed debt portfolio management is clearer, the next step is understanding how these portfolios develop in the first place and what factors typically lead to accounts becoming distressed.

Why Distressed Debt Portfolios Occur

Distressed debt portfolios rarely develop from a single issue. In most cases, they build over time as multiple financial, operational, and market factors affect borrowers’ ability to meet their obligations. Understanding these causes helps lenders and creditors manage risk and develop more effective recovery strategies.

Below are some of the most common reasons distressed portfolios emerge.

Economic and Market Conditions

Broad economic shifts can quickly affect borrowers across entire industries. During periods of financial uncertainty, businesses and individuals may struggle to maintain consistent payment schedules.

Common triggers include:

- Recessions, which reduce income stability and business revenue

- Industry downturns, where sector-specific challenges affect large groups of borrowers

- Liquidity shortages, making it difficult for companies or individuals to meet short-term obligations

When these pressures occur at scale, lenders may see a sharp increase in past-due accounts.

Borrower Financial Instability

Individual financial circumstances often play a major role in distressed accounts. Changes in income, rising expenses, or unexpected financial events can disrupt repayment plans.

Some common drivers include:

- Cash flow disruptions, particularly for small businesses or self-employed borrowers

- Excessive leverage, where debt obligations exceed sustainable repayment capacity

- Job loss or business closures, which can immediately affect repayment ability

When these situations arise, accounts may transition from active repayment to delinquency and eventually into collections.

Credit Risk Exposure

Credit risk is a core factor in any lending environment. It refers to the possibility that borrowers may fail to meet their repayment obligations as agreed.

Even well-structured credit programs carry some level of risk. Over time, a portion of accounts may become delinquent due to changing financial conditions, leading lenders to accumulate distressed balances across their portfolios.

Operational Gaps in Collections

In some cases, distressed portfolios grow because organizations lack the internal resources needed to manage delinquent accounts effectively.

Common operational challenges include:

- Limited specialized recovery teams trained to handle distressed accounts

- Lack of advanced analytics for identifying high-priority accounts

- Insufficient compliance infrastructure to manage regulatory requirements in collections

Without structured systems and experienced servicing teams, past-due accounts can accumulate quickly.

When distressed accounts grow across a portfolio, organizations often need to adopt more structured portfolio management strategies to stabilize recovery efforts, maintain regulatory compliance, and reduce potential losses.

Key Risks in Distressed Debt Portfolio Management

Managing a distressed portfolio involves far more than simply pursuing overdue balances. Distressed portfolios introduce a set of financial, operational, and regulatory risks that can quickly escalate if they are handled without a structured recovery framework. For creditors, these risks affect not only recovery outcomes but also legal exposure and long-term customer relationships.

Below are some of the most significant challenges organizations face when managing distressed debt portfolios.

Recovery Uncertainty and Declining Asset Value

Distressed accounts carry a much higher probability of default than performing loans. As accounts age or remain unresolved, the likelihood of full repayment typically decreases. This creates uncertainty around how much of the outstanding balance can realistically be recovered.

For creditors holding large portfolios, this uncertainty makes it difficult to forecast recovery rates, allocate resources efficiently, or determine whether to continue servicing the accounts internally. Effective distressed debt portfolio management requires detailed analysis of account history, borrower behavior, and repayment potential so that recovery efforts focus on accounts where resolution is most achievable.

Compliance and Regulatory Risk

Debt collection activities are governed by strict consumer protection regulations. In the United States, laws such as the Fair Debt Collection Practices Act (FDCPA) establish clear standards for how collectors communicate with consumers, verify accounts, and handle disputes.

Organizations must also account for broader compliance requirements related to:

- consumer communication practices

- dispute and account verification procedures

- data privacy and protection standards

- secure handling of sensitive financial information

Failure to follow these rules can expose creditors and collection partners to legal penalties, regulatory scrutiny, and reputational damage. This is why many organizations rely on compliance-focused servicing frameworks that combine clear communication processes with secure technology infrastructure.

Operational Complexity at Scale

Distressed portfolios often contain thousands of accounts with different balances, repayment histories, and legal statuses. Managing these portfolios effectively requires more than basic collections outreach.

Organizations typically need:

- systems for organizing and tracking account data

- segmentation strategies to prioritize recoverable accounts

- structured communication workflows for consumer engagement

- reporting tools to monitor performance and recovery progress

Without the right operational infrastructure, distressed portfolios can become difficult to manage, leading to inconsistent recovery efforts and inefficient use of resources.

Reputation and Consumer Experience Risk

The way distressed accounts are handled can directly affect how creditors are perceived by consumers and regulators. Aggressive or unclear communication practices can damage trust and increase the likelihood of complaints or disputes.

Modern distressed portfolio management increasingly emphasizes transparent, respectful communication and clear repayment options. Providing consumers with accessible ways to review their accounts, submit disputes, or establish payment arrangements can improve resolution rates while protecting brand reputation.

Because distressed portfolios involve multiple risks and uncertainties, successful management requires structured recovery strategies designed to balance financial recovery

Distressed Debt Portfolio Recovery Strategies

Recovering value from distressed portfolios requires a clear, repeatable playbook that balances return, compliance, and consumer care. These portfolios often contain thousands of accounts with different repayment capacities, legal statuses, and financial circumstances, making consistent strategy essential.

Below are practical strategies organized so teams can read, act, and match each step:

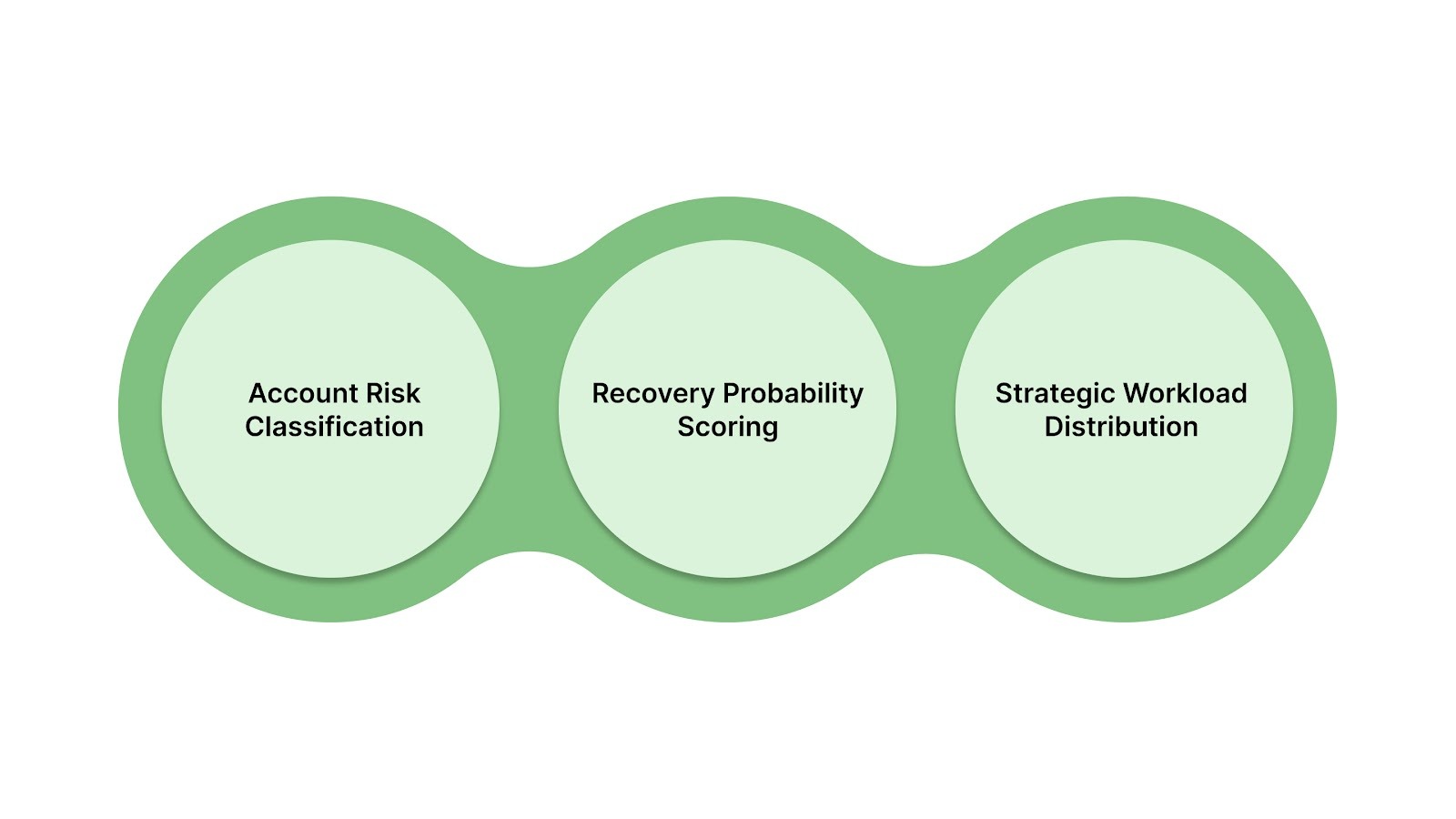

Portfolio Segmentation and Prioritization

Distressed portfolios contain accounts with very different recovery probabilities. Segmenting accounts allows creditors to identify which accounts are most likely to be resolved and apply appropriate recovery strategies to each category.

- Account risk classification: Accounts are categorized based on factors such as delinquency age, outstanding balance, payment history, and borrower financial indicators. This structured classification helps identify which accounts require immediate outreach and which may need longer-term servicing strategies.

- Recovery probability scoring: Data models evaluate account characteristics to estimate the likelihood of repayment or settlement. These scoring systems allow recovery teams to prioritize high-potential accounts and allocate resources more efficiently.

- Strategic workload distribution: Segmentation allows organizations to assign accounts to specialized recovery teams based on complexity, ensuring that experienced personnel manage high-risk or high-value accounts.

Data-Driven Portfolio Analysis

Large distressed portfolios require continuous monitoring and performance analysis. Data-driven insights help creditors understand how accounts behave over time and which recovery methods produce the best results.

- Recovery performance monitoring: Organizations track key metrics such as repayment rates, settlement success, and time-to-resolution. Monitoring these indicators helps determine whether recovery strategies are producing expected outcomes.

- Predictive repayment modeling: Advanced analytics use historical payment behavior and credit indicators to forecast which accounts are most likely to respond to repayment offers or structured payment plans.

- Strategy optimization through analytics: Ongoing analysis helps organizations refine outreach timing, settlement thresholds, and communication strategies to improve recovery performance across the portfolio.

Consumer-Focused Repayment Solutions

Many distressed borrowers experience temporary financial hardship rather than a permanent inability to repay. Offering flexible repayment options often increases engagement and improves resolution rates.

- Structured payment plans: Payment schedules can be tailored to the borrower’s financial capacity, allowing balances to be resolved gradually without creating additional financial pressure.

- Settlement opportunities for eligible accounts: In certain cases, negotiated settlements allow borrowers to close accounts through reduced lump-sum payments, helping creditors recover part of the outstanding balance while resolving accounts efficiently.

- Accessible payment channels: Secure online portals, automated payment options, and clear payment instructions reduce friction and make it easier for consumers to fulfill their repayment commitments.

Compliance-Driven Collection Practices

Debt recovery must operate within a strict regulatory framework designed to protect consumers and ensure fair collection practices. Compliance is therefore a central component of distressed portfolio management.

- Adherence to debt collection regulations: Laws such as the Fair Debt Collection Practices Act establish guidelines on how collectors may communicate with consumers and prohibit abusive or deceptive practices.

- Clear account verification procedures: Consumers must be able to verify the origin and accuracy of the debt, ensuring transparency and reducing disputes throughout the recovery process.

- Secure data management systems: Organizations must maintain strong data protection measures to safeguard personal and financial information during servicing and payment processing.

Multi-Channel Consumer Engagement

Successful recovery strategies rely on consistent, compliant communication with consumers. Using multiple outreach channels helps increase engagement while giving borrowers convenient ways to respond.

- Structured outreach programs: Recovery teams follow defined communication schedules that combine phone calls, written notices, and digital communication to maintain consistent engagement.

- Digital communication channels: Email, SMS notifications, and secure online portals allow consumers to review account details and respond to repayment offers more conveniently.

- Consumer-centered messaging: Clear explanations of account balances, repayment options, and dispute resolution procedures help build trust and encourage cooperation in resolving outstanding debts.

Settlement and Resolution Planning

Not every distressed account can be recovered through standard repayment schedules. Settlement planning provides an alternative strategy for resolving accounts where full repayment may not be feasible.

- Structured settlement programs: Creditors may offer negotiated settlements that allow borrowers to resolve accounts for a portion of the outstanding balance under clearly defined terms.

- Time-bound settlement incentives: Limited-time settlement opportunities can encourage borrowers to act quickly and resolve accounts before further collection steps occur.

- Standardized negotiation guidelines: Establishing clear policies for settlement approvals ensures consistency and prevents recovery teams from applying inconsistent terms across the portfolio.

Strategic Portfolio Sales and Acquisitions

In some situations, creditors may decide that selling distressed accounts is more efficient than continuing to service them internally. Portfolio transactions allow lenders to recover value while reducing operational complexity.

- Portfolio valuation and due diligence: Buyers analyze account documentation, repayment history, and legal collectability to determine the fair value of distressed portfolios.

- Transfer and onboarding processes: Once acquired, accounts must be integrated into servicing systems while maintaining compliance with consumer communication requirements.

- Recovery-focused portfolio servicing: Specialized receivables management firms often manage these acquired portfolios using structured recovery strategies designed to maximize resolution rates.

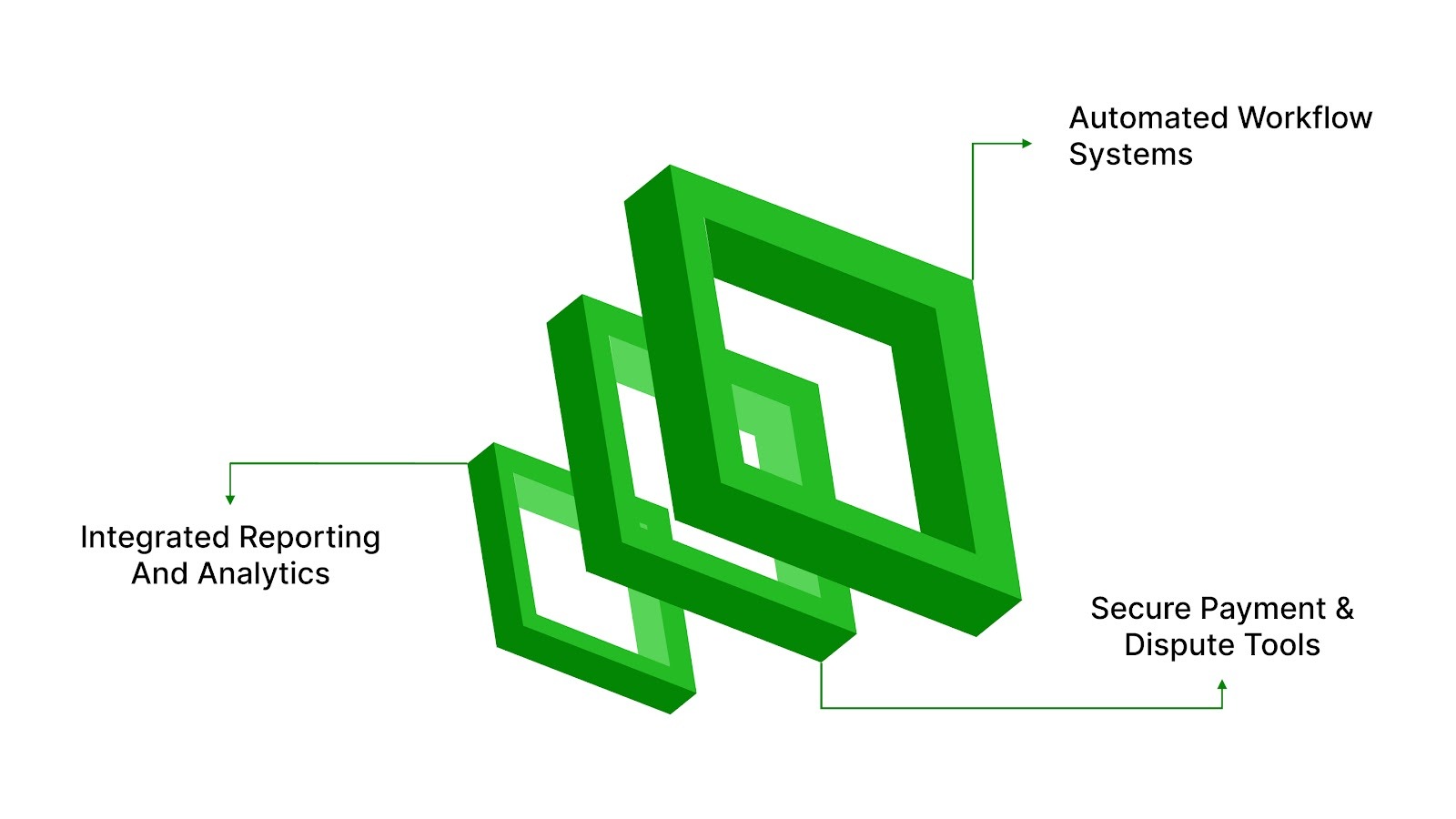

Technology-Enabled Portfolio Management

Managing large distressed portfolios requires technology systems capable of supporting large volumes of accounts and complex compliance requirements.

- Automated workflow systems: Digital platforms help manage communication schedules, track account activity, and ensure that recovery processes follow established operational procedures.

- Integrated reporting and analytics: Real-time dashboards allow portfolio managers to monitor recovery progress, identify underperforming segments, and adjust strategies accordingly.

- Secure payment and dispute management tools: Technology platforms enable consumers to verify account details, make payments securely, and submit disputes through structured digital channels.

Continuous Portfolio Performance Monitoring

Distressed portfolio recovery is an ongoing process that requires continuous evaluation and improvement. Regular performance monitoring helps organizations refine strategies and maintain operational efficiency.

- Recovery performance reviews: Portfolio managers analyze recovery rates, settlement outcomes, and operational costs to determine whether strategies are producing expected results.

- Compliance audits and process reviews: Periodic audits ensure that recovery practices remain aligned with regulatory requirements and internal compliance policies.

- Strategy refinement over time: Insights gained from performance data help organizations adjust segmentation models, outreach strategies, and recovery tactics for future portfolios.

Also read: Benefits and Process of Portfolio Management Services

While these strategies provide a framework for managing distressed accounts, their effectiveness often depends on having the right systems, processes, and support in place.

Conclusion

Distressed debt portfolios are a reality of modern credit systems. Economic challenges, unexpected life events, or financial disruptions can all lead to overdue accounts that require structured management.

The important thing to remember is that these situations are often resolvable with the right guidance and clear communication. Understanding your account details, exploring repayment options, and taking proactive steps can help turn uncertainty into a manageable path forward.

The Forest Hill Management supports this process by helping individuals understand their accounts and providing clear ways to resolve past-due balances.

FAQs

1. What happens when a debt becomes distressed?

When a debt becomes distressed, it usually means the borrower has missed payments for an extended period or is at high risk of default. At this stage, the account may be transferred to a specialized servicing organization that helps manage communication and repayment resolution.

2. Can distressed accounts affect your credit history?

Yes. Past-due or delinquent accounts may appear on credit reports and can affect credit scores depending on the length of delinquency and whether the account is resolved or remains unpaid.

3. How can someone verify that a collection account is legitimate?

Consumers can request written verification of the account, including details about the original creditor and the outstanding balance. This helps confirm the validity of the debt before making payments or establishing repayment arrangements.

4. Are repayment plans available for people facing financial hardship?

In many cases, yes. Servicing organizations may offer structured repayment plans designed to help individuals resolve balances gradually based on their financial circumstances.

5. What should someone do after being contacted about a past-due account?

The best first step is to review the account details, confirm the balance and creditor information, and communicate with the servicing team to understand available payment or resolution options.