Start 2026 Strong: 7-Step Financial Planning Process for Managing Debt

Transform Your Financial Future

Contact UsIf it feels like you are carrying the weight of the world on your shoulders, you are not alone. U.S. household debt recently hit a record $18.59 trillion, while delinquency rates are climbing. This is an unmistakable sign that many people are juggling obligations they cannot afford to ignore.

This year does not have to be a repeat of last year’s stress. Instead, imagine a clear, steady path forward. This guide presents a 7-step financial planning process designed especially for people managing debt, so you can begin 2026 with purpose, control, and hope.

A quick snapshot:

- Planning reduces overwhelm. A structured financial plan replaces confusion with clarity and helps you approach debt with confidence.

- Early action creates breathing room. Starting your plan at the beginning of the year spreads decisions and adjustments across manageable timelines.

- Seven steps build steady progress. Knowing your numbers, budgeting, building buffers, reducing costs, increasing flexibility, and reviewing quarterly create a balanced system for debt management.

- Setbacks are a normal part of the journey. Unexpected events do not erase progress. Gentle adjustments help you stay moving forward.

- Savings and debt can grow together. Small, strategic savings alongside repayment protect you from new debt and support long-term stability.

How Can Strategic Planning Help You Reduce Debt?

Debt often feels overwhelming, not because of the amount alone, but because of the lack of structure surrounding it. When bills, deadlines, and balances pile up without a clear plan, everything blends into stress and uncertainty.

As personal finance expert Dave Ramsey puts it, “A budget is telling your money where to go instead of wondering where it went.”

Planning gives you direction, and direction brings relief.

Here is how strategic planning changes the way you manage debt and rebuild financial stability:

- Clear Visibility: When you map out your debts, due dates, and income, the unknown becomes manageable. Clarity replaces fear and helps you make informed decisions.

- Prioritized Action: A plan helps you identify which debts require attention first, based on factors such as interest rates, balances, or emotional impact. Prioritization saves money, time, and stress.

- Consistent Progress: Planning turns repayment into a routine. Whether weekly or monthly, consistency keeps you moving forward, even when progress feels slow.

- Better Cash Flow Control: With a structured budget, you decide where each dollar goes. This reduces overspending and frees up more money for repayment.

- Protection Against Setbacks: A plan includes buffers, such as a small emergency fund, that prevent unexpected expenses from derailing your progress.

Most Americans carry debt into the new year, and the numbers continue to rise. But with structure, intention, and steady habits, you can move from feeling overwhelmed to feeling in control.

Forest Hill Management helps borrowers turn financial planning into action. Our structured repayment plans, clear communication, and flexible options support consistent progress, even when income or circumstances change. Speak to us today.

Suggested Read: How to Win Debt Collection Disputes: A Complete Step-by-Step Guide

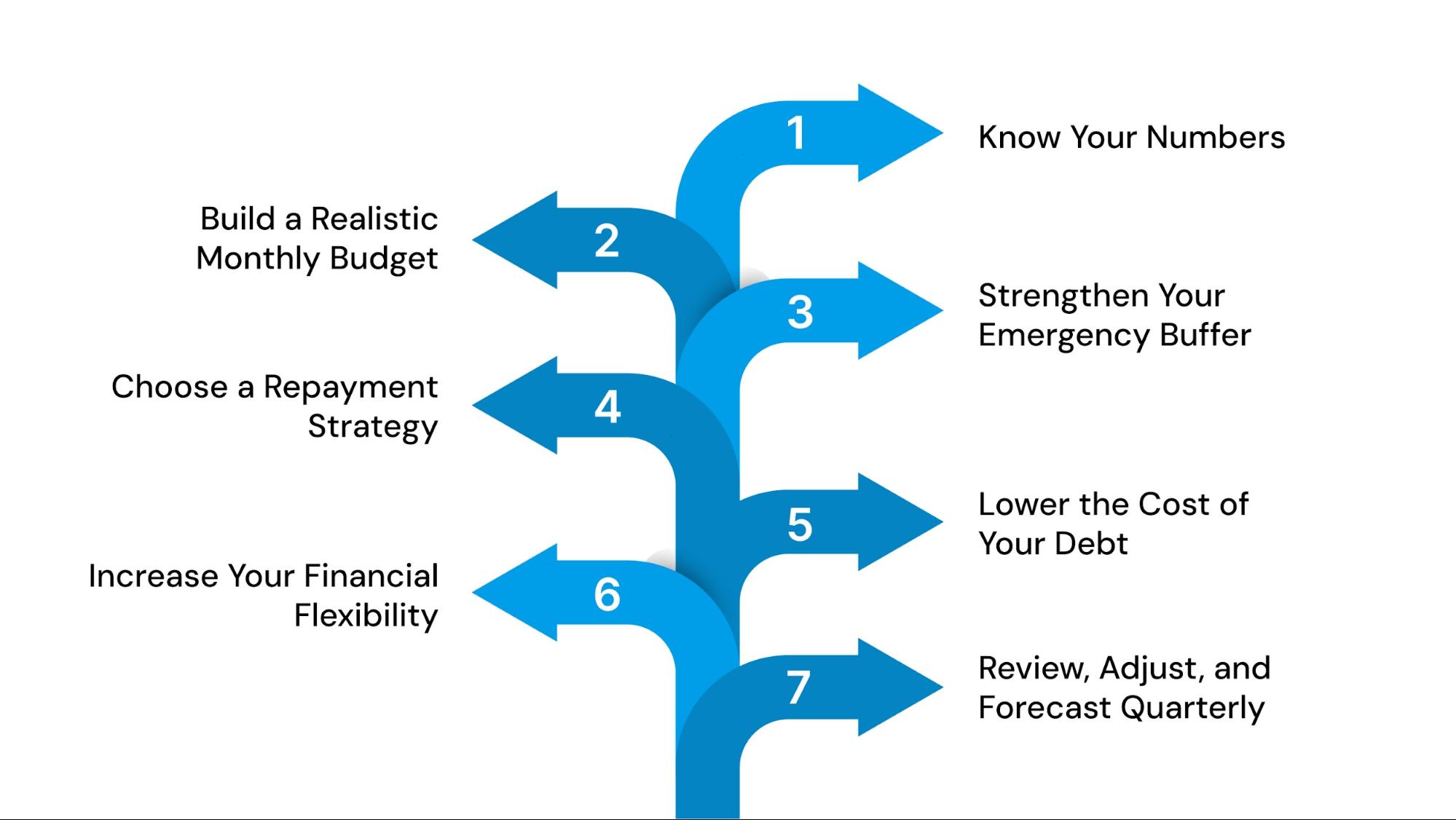

The 7 Steps to Manage Debt and Build a Strong 2026

Starting early gives you something that debt rarely allows: breathing room. When you plan at the beginning of the year, you spread decisions, adjustments, and improvements across twelve months instead of scrambling later.

This is how progress becomes sustainable; not rushed, not reactive, but steady and genuinely life-changing.

Below are seven high-impact steps designed to help you manage debt with structure, intention, and confidence.

Step 1: Know Your Numbers

Most people underestimate how much they owe, how much interest they are paying, or how quickly balances can grow. This step is about reconstructing the actual financial blueprint of your life. When you know your numbers in detail, you operate with clarity instead of assumptions.

Here’s what to review and organize:

- Total debt balances, broken down by lender

- Interest rates (APR) and how often interest compounds

- Minimum payments versus actual monthly outflow

- Payment due dates and any penalties or fees

This step gives you data you can act on. For example, understanding your interest structure lets you calculate which balances cost you the most each day.

You can also use the Rule of 72 (72 divided by your interest rate = approximate years for the balance to double) to see how quickly high-interest debt grows when left unmanaged. This turns a simple list into a strategic financial roadmap for the year.

Step 2: Build a Realistic Monthly Budget

Build the budget around what you actually receive each pay period, not an idealized monthly total. When your budget reflects real-time and real-life behavior, it eliminates surprises and creates predictable cash available for debt reduction.

The following points are about how to structure a practical, resilient budget:

- Track net (take-home) pay by pay period.

- Allocate fixed buckets: essentials, debt obligations, sinking funds, and one discretionary buffer.

- Convert large irregular costs (insurance, taxes) into monthly equivalents via a sinking fund.

- Use a rolling 30- or 60-day cashflow calendar to prevent shortfalls.

Use pay-period budgeting and a rolling cashflow calendar. Convert irregular annual costs into monthly amounts (annual cost divided by 12) and automate transfers into sinking funds.

This reduces the volatility that often forces people to use credit and reveals the true monthly surplus that can be redirected to pay off.

Step 3: Strengthen Your Emergency Buffer

An emergency fund prevents one surprise from undoing months of progress. Rather than aiming immediately for three to six months, build modular, goal-oriented buffers (such as car, medical, and housing) with clear targets and separate accounts.

This approach protects your repayment plan without waiting for a large, intimidating lump sum. The following points are about how to create useful, protected buffers quickly:

- Start with a $500–$1,000 rapid response fund for immediate shocks.

- Create specific sinking funds for predictable risk (car repairs, prescriptions).

- Keep funds liquid but separated (high-yield savings or money-market accounts).

- Replenish from a dedicated “rainy-day” category before reallocating to debt.

Use a liquidity ratio: target having 10–30% of one month’s net take-home pay in an instantly accessible account as a micro-buffer while you build the modular funds.

This small metric reduces the chance of turning to high-interest credit when a minor shock occurs.

Step 4: Choose a Repayment Strategy

The right payoff strategy combines math with psychology so you do not burn out. A hybrid ladder of quick, small wins, followed by mathematically optimal targeting, keeps momentum while minimizing total interest.

Define triggers (e.g., when a balance is cleared, roll freed cash to the account with the highest APR) so the strategy is automatic, not emotional.

The following points are about selecting and operationalizing a repayment ladder:

- Eliminate the two smallest balances first for behavioral momentum.

- Then switch to avalanche targeting the highest APR balances.

- Automate extra payments and document the “rollover” of freed cash.

- Reassess if interest rates or income change significantly.

Calculate daily interest cost to compare debts accurately (balance × APR / 365). Use that to prioritize beyond APR alone.

A mid-APR, high-balance account can cost more per day than a small, higher-APR balance. Spreadsheet the daily cost column to reveal where each incremental dollar reduces interest fastest.

Step 5: Lower the Cost of Your Debt

Explore targeted rate reductions: creditor hardship programs, lender repricing requests, balance transfers with fee break-evens, or consolidation only when the net present value (NPV) of savings exceeds fees and risk.

Treat every negotiation as an ROI decision, not a moral plea. The following points are about tactical ways to reduce financing costs:

- Request rate reductions and fee waivers in writing.

- Calculate refinancing or balance transfer break-even points.

- Consolidate only when the new APR and fees lower the lifetime interest.

- Use hardship programs to temporarily reduce interest while rebuilding cash flow.

Forest Hill Management offers flexible repayment options designed to reduce the lifetime cost of your debt. Whether you are negotiating lower rates, exploring hardship programs, or evaluating consolidation, our team helps you align repayment terms with your financial goals. Expert advice is just a call away.

Step 6: Increase Your Financial Flexibility

Increasing effective cash flow is more powerful than cutting tiny expenses; it changes the denominator of your problem.

Focus on repeatable, scalable income lifts with strong net take-home. Ask for targeted raises tied to deliverables, secure recurring freelance contracts, or monetize underused assets.

Also improve “financial leverage” by shifting expenses (e.g., lowering housing cost via roommate or refinancing mortgage) when feasible.

The following points are about practical ways to increase sustainable net income:

- Negotiate a raise with a one-page case showing impact and market comps.

- Start a repeatable side income with predictable weekly hours.

- Review fixed expenses for renegotiation (insurance, internet, subscriptions).

- Convert occasional windfalls (tax refunds, bonuses) into payoff acceleration.

Measure effective hourly return on any income option: net dollars gained divided by hours invested. Prioritize side work or gigs where the effective hourly rate exceeds your opportunity cost. Make sure it can be sustained for at least six months to materially accelerate debt reduction.

Step 7: Review, Adjust, and Forecast Quarterly

Life changes too quickly for once-a-year financial check-ins. Quarterly reviews help you catch small problems before they grow, and they show you the progress you don’t always notice month to month.

This rhythm keeps your plan alive by being flexible, realistic, and aligned with what is happening in your actual life, not just on paper.

The following points are about what to measure and how to adjust every quarter:

- Look at your net surplus and how much debt you paid down in the last three months.

- Reorder your debt priorities if any interest rates or minimums have changed.

- Adjust your emergency and sinking fund targets in response to new expenses or life events.

- Pick one simple task for the next quarter. You need something specific, like lowering one APR or paying off a small balance.

Instead of annual forecasting, use a rolling 12-month view that updates each quarter. You can keep this simple: estimate where your balances, savings, and cash flow will be 12 months from now if you keep going the way you are going.

This forward glance helps you spot opportunities to accelerate progress or catch pressure points early so nothing derails your journey.

Suggested Read: Debt Settlement Explained: How It Works and If It's a Good Option for You

Setbacks That Can Derail Progress

Setbacks are a normal part of any financial journey. They do not erase your progress, and they do not mean you are starting over. The important thing is remembering that a setback is just a pause, not a failure, and with the right approach, you can get back on track without shame or panic.

This table can bring clarity to moments that usually feel chaotic and help you reset gently:

Every person dealing with debt faces at least one of these moments. They do not reflect your character, strength, or ability. They simply reflect life. What matters most is how gently and intentionally you reset, not how fast you bounce back.

These are a few things you need to keep in mind:

- Pause, don’t quit. A temporary slowdown is still part of forward movement.

- Rebuild in small steps. Even $20–$50 adjustments help you regain control.

- Automate where possible. Let systems carry you when motivation dips.

- Track only one metric. Focus on progress in one area (like total debt paid) to avoid overwhelm.

- Give yourself grace. Emotional recovery is part of financial recovery — both matter equally.

The next section explores why savings and debt repayment can, and should, work together, even when money feels tight.

Suggested Read: Does Debt Consolidation Affect Buying a Home?

Smart Strategies for Tackling Debt

Paying down debt and saving at the same time can feel impossible, especially when money is tight, but doing both together builds stability. Savings protect you from new debt, while repayment lowers financial pressure month after month.

These strategies can help you balance savings and debt repayment effectively:

- Use the 70/20/10 Split: Allocate 70% of income to essentials, 20% to debt + savings (combined), and 10% to breathing-room or personal spending.

- Create “Parallel Progress”: Even saving $25 per paycheck builds momentum while your repayment plan continues.

- Automate Minimums + Micro-Savings: Set autopay for minimums and automatic transfers for small savings amounts to eliminate decision fatigue.

- Send Windfalls to Both Goals: Split tax refunds, bonuses, or side income between one debt target and your emergency buffer.

- Adopt the “Pay Yourself Second” Rule: After paying your minimums, dedicate a fixed percentage to savings before discretionary spending.

When you pair savings with repayment, you build resilience — the kind that prevents setbacks from turning into new debt. This is also where professional repayment support can help you stay consistent and organized.

In the next section, we will explore how Forest Hill Management makes your repayment journey easier and more manageable, even when life feels unpredictable.

Suggested Read: What Are Installment Loans and How Can They Help Pay Debt?

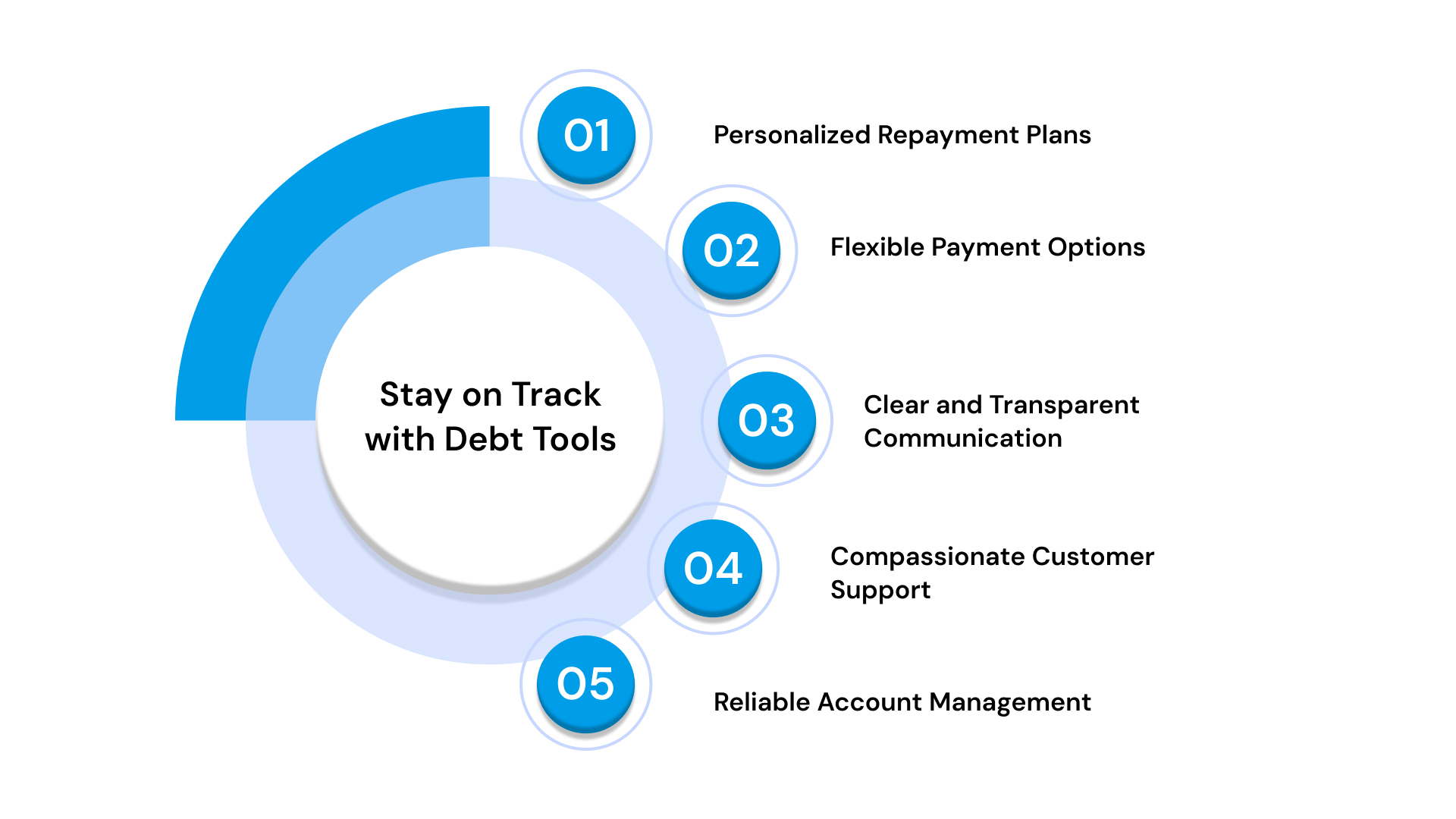

Stay on Track With Debt Support and Planning Tools

Managing debt is easier when you are not doing it alone. This is where Forest Hill Management makes a meaningful difference. We focus on clear communication, flexible repayment options, and a respectful, people-first approach so you can stay consistent without feeling overwhelmed.

Our role is to support your financial plan, not pressure it, and to help you move through repayment with confidence and control.

This is how we can help you stay steady and organized:

- Personalized Repayment Plans: We tailor repayment schedules to match your income, routine, and obligations so you can stay on track without added pressure. This ensures payments feel manageable, not overwhelming.

- Flexible Payment Options: You can pay online, by phone, or through scheduled arrangements — whatever fits your life best. Flexibility helps you stay consistent even when your schedule or income shifts.

- Clear and Transparent Communication: We keep you informed about balances, due dates, and account changes in ways that are simple and easy to understand. When information is clear, decision-making becomes easier and less stressful.

- Compassionate Customer Support: Our team listens first and responds with respect, empathy, and professionalism. You are never judged for your situation. Our focus is on helping you move forward.

- Reliable Account Management: We maintain accurate records and provide steady guidance throughout your repayment journey. This removes confusion and gives you confidence that your progress is being tracked properly.

When debt payments have structure and support behind them, they stop feeling intimidating and start becoming a steady, manageable routine. Every payment you make is a step toward stability and a future with less stress and more control.

Conclusion: A Strong 2026 Begins With a Clear Plan

Starting 2026 with intention and structure can transform your relationship with debt. When you plan, you replace guesswork with direction, and each small step becomes part of a larger, steady financial shift. With thoughtful budgeting, realistic goals, and consistent review, this can be the year you finally break the cycle of stress and move toward long-term stability.

Forest Hill Management supports that journey by offering flexible repayment options, clear communication, and a respectful, human approach that helps you stay committed. When repayment becomes structured and manageable, progress begins to feel achievable.

Start building your plan today. Reach out to explore debt repayment options that fit your life.

Frequently Asked Questions

1. How do I know if my financial goals for 2026 are realistic?

Your goals are realistic if they fit your current income, essential expenses, and lifestyle. Start with small, achievable targets and adjust quarterly as your situation improves.

2. Should I pay off high-interest debt before saving for retirement?

Generally, high-interest debt should come first because it grows faster than most investments. However, if your employer offers a retirement match, contribute enough to receive it while still prioritizing debt repayment.

3. What should I do if my income changes unexpectedly during the year?

Rebuild your budget from the ground up based on your new income, not the old one. Then adjust your repayment strategy, minimums, and savings to match your new baseline.

4. Is it better to track my finances manually or with apps?

Choose whichever method you will actually stick with. Apps automate reminders and categorization, while manual tracking builds deeper awareness. Both are effective if used consistently.

5. What if I lose motivation halfway through the year?

Focus on one simple financial win, like paying down a small balance or rebuilding a $100 buffer, to regain momentum. Small victories renew confidence and help you reconnect with your larger goal.