How to Get Out of Bad Debt Quickly

Need Help Reviewing Your Account?

Contact UsMost people don’t struggle with debt because they don’t want to pay it off. They struggle because they are not sure where to start. When multiple balances, interest rates, and due dates compete for attention, even a simple question like “what should I pay first?” becomes unclear.

That confusion is more common than it seems. Recent data shows that nearly half of credit card holders carry a balance from month to month, which means interest continues to build while repayment feels slow and uncertain. The challenge is not just the debt itself, but the lack of a clear, structured path out of it.

Getting out of bad debt quickly is not about extreme measures. It is about removing that confusion, putting the right steps in order, and following a plan that works consistently over time.

In this blog, you will learn how to get out of bad debt through a clear step-by-step plan, which repayment strategies actually work, what to avoid along the way, and how structured support can help you move forward with confidence.

Key Takeaways

- Getting out of bad debt becomes easier when you follow a structured plan instead of reacting to individual payments or pressures.

- The first step is stabilizing your situation by stopping new debt and clearly understanding everything you owe.

- Choosing the right repayment strategy and staying consistent can significantly improve how quickly you reduce your balances.

- Avoiding common mistakes like ignoring debt, disorganization, or unclear agreements helps prevent setbacks.

- Support options such as counseling, structured plans, or guided communication can make the process more manageable when needed.

What Is Considered Bad Debt?

Bad debt generally refers to financial obligations that become difficult to manage due to high interest costs, missed payments, or ongoing balances that do not reduce over time. It is not a judgment on the borrower. It is a way to describe debt that creates ongoing financial pressure rather than supporting long-term stability.

Bad debt is more about how it behaves over time. The key issue is whether the debt is increasing or decreasing over time.

When Does Bad Debt Become Difficult to Manage?

Bad debt typically becomes difficult to manage when it moves beyond a single account or temporary setback and starts affecting your overall financial clarity and control. This shift often happens gradually rather than all at once.

- When multiple accounts begin to overlap: Managing several balances with different due dates, amounts, and terms can create confusion, especially if there is no clear system in place to track them.

- When interest and fees start compounding: As balances grow, interest charges and additional fees can increase the total amount owed, making repayment feel slower and less effective.

- When payments become inconsistent or delayed: Missing or delaying payments can lead to further complications, including added charges or changes in account status, which make the situation harder to stabilize.

- When there is limited visibility into account details: Not having clear, up-to-date information about balances, payment history, or account ownership can make it difficult to make informed decisions.

- When communication becomes unclear or overwhelming: Receiving multiple notices or not fully understanding who to contact can add to the sense of uncertainty and delay meaningful action.

- When financial decisions become reactive instead of planned: Without a structured approach, it becomes easy to respond to immediate pressures rather than following a consistent plan toward reducing debt.

Also read: How to Create an Effective Debt Repayment Plan

This is the point where structure becomes essential. With clear information, organized tracking, and steady communication, even complex debt situations can be understood and managed more effectively.

How to Get Out of Bad Debt (Step-by-Step Plan)

.jpg)

Getting out of bad debt works best when you treat it like a process. The most effective approach is the one you can follow consistently, especially if some of your accounts are already past due or in collections.

1. Stop Adding New Debt

The first step is to stop making the situation larger. If you keep using credit while trying to reduce balances, you are working against your own repayment plan. We would recommend adding up your income and expenses first, then deciding what you can realistically afford before taking on any more borrowing.

- Pause credit card spending unless it is essential.

- Avoid new loans or financing that add to your monthly pressure.

- Keep the focus on stabilizing the debt you already have.

2. Get a Complete Picture of What You Owe

You cannot build a workable plan until you know exactly what is on the table. That means listing every debt, the balance, the minimum payment, the interest rate, and whether the account is current, overdue, or already in collections.

- Write down each account in one place.

- Include the creditor, balance, interest rate, and due date.

- Mark which debts are costing you the most each month.

3. Create a Strict Budget You Can Actually Follow

A budget is not just a spending log. It is the structure that shows you how much can realistically go toward debt without derailing your essentials.

- Keep the budget realistic, not idealistic.

- Cut the spending that does not support your essential needs.

- Revisit the budget often so it stays useful as your situation changes.

4. Choose a Repayment Strategy That Fits Your Situation

Two of the most common payoff methods are the snowball and avalanche approaches. The highest-interest method and the smallest-balance method are often described as the two main strategies for reducing debt.

- Use snowball if motivation is your biggest challenge.

- Use avalanche if high interest is draining your budget fastest.

- Keep making minimum payments on all other accounts to avoid new penalties where possible.

5. Increase the Amount Going Toward Debt

Once the budget is in place, look for ways to free up even a little more cash for repayment. Small extra payments can make a difference over time, especially when they are applied consistently.

- Put tax refunds, bonuses, or side income toward debt instead of absorbing them into routine spending.

- Add extra money to one target account whenever possible.

- Even modest increases help reduce the balance faster than minimum payments alone.

6. Talk to Creditors or the Debt Collector Early

If an account is already behind, communication matters. You can contact their creditors to explain what they can afford, and they can also work with debt collectors to set up repayment agreements when an account has fallen into collections. That conversation should include what you owe, who to contact if you need to dispute the debt, and what payment options are available.

- Ask whether lower payments, a different due date, or temporary relief is available.

- If the account is in collections, ask for the current creditor name and the amount owed.

- Keep written notes or request confirmation in writing whenever possible.

7. Be Careful With Debt Relief Offers That Sound Too Easy

Debt relief and settlement schemes can be risky, especially when they ask for upfront fees or promise fast results that do not match reality.

- Be cautious with companies that promise quick debt reduction.

- Do not stop paying just because a company says it can “handle everything.”

- Get every claim in writing before agreeing to anything.

8. Consider Credit Counseling or a Debt Management Plan

If you need structure beyond a personal budget, nonprofit credit counseling can help. Reputable counselors can help you review your situation, create a budget, and may recommend a debt management plan for unsecured debts.

- A debt management plan can simplify multiple payments into one structured monthly plan.

- These plans are generally used for unsecured debts such as credit cards or medical debt, not debts secured by collateral like a home or car.

- A nonprofit counselor should explain costs, terms, and likely outcomes before you enroll.

9. Keep Records and Track Progress

Staying organized makes the process easier to manage and protects you if questions come up later. Keeping a file of letters and documents, recording conversation dates and times, and noting what was discussed will help you in the long run.

- Save every notice, statement, email, and payment confirmation.

- Track balances so you can see real progress over time.

- Keep notes on calls, agreements, and any changes to your repayment plan.

10. Know When a Debt May Need Legal Guidance

If an account is already in collections, if a lawsuit is threatened, or if the debt feels too old or complicated to sort out alone, legal support may be worth considering. You should respond promptly if sued and should not ignore court papers.

- Read any legal notices carefully and note response deadlines.

- Keep your records together in case you need them for a lawyer or court.

- Seek help quickly if the situation escalates beyond normal repayment discussions.

Getting out of bad debt is usually less about one dramatic move and more about a series of disciplined ones. Once the debt is organized, the budget is clear, and the repayment path is defined, the process becomes much more manageable.

When an account is being handled by The Forest Hill Management, the most useful next step is often to review the details, understand the balance, and work through the available options with clarity rather than pressure.

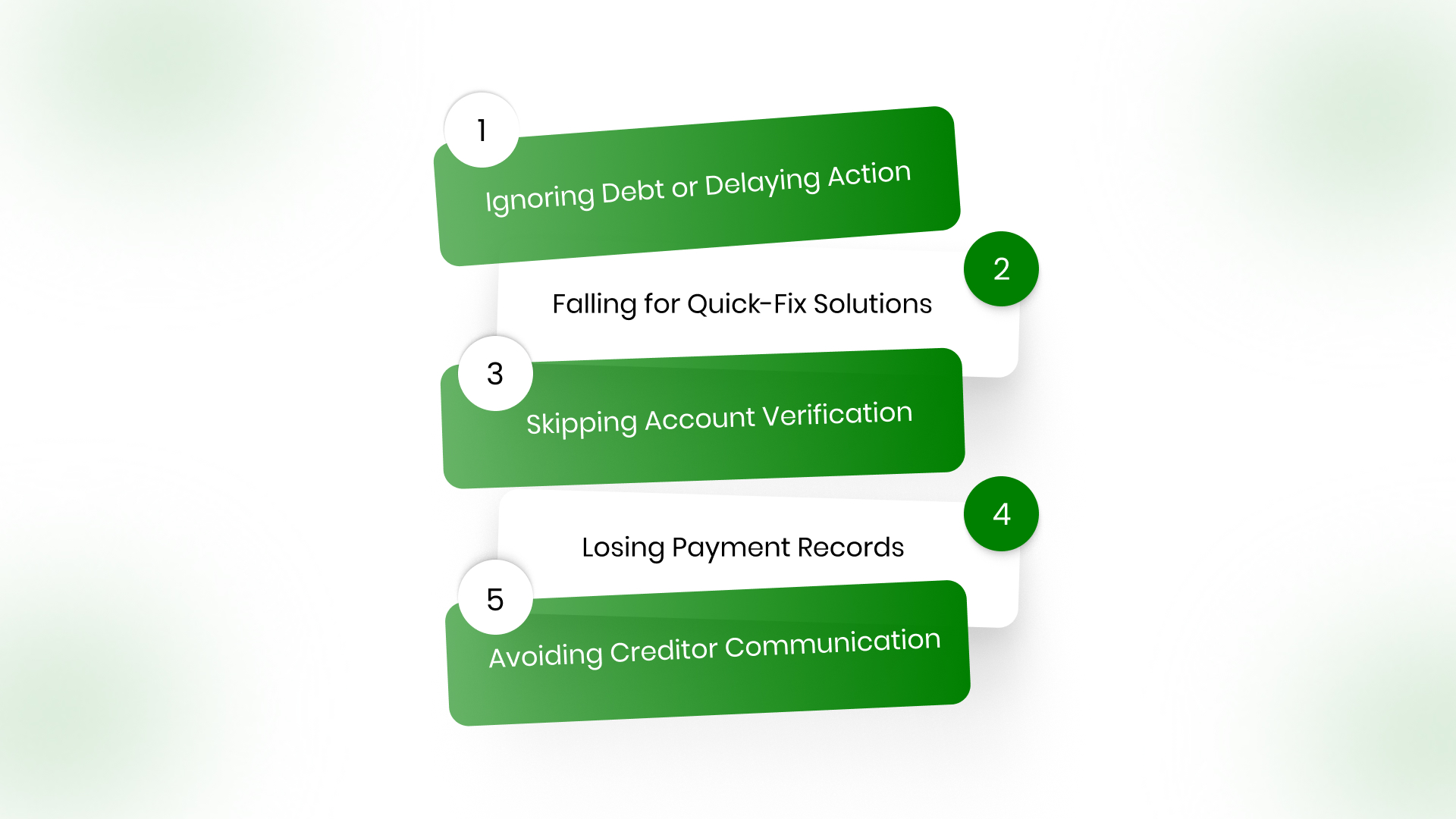

What to Avoid When Trying to Get Out of Bad Debt

When you are working to get out of bad debt, progress depends just as much on what you avoid as what you do. Certain habits and decisions can quietly slow down repayment, increase costs, or make the situation harder to manage over time.

Here are the most important things to avoid:

- Ignoring the debt or delaying action: Putting off action can lead to additional fees, growing balances, and more complex account situations. Over time, delayed responses can reduce flexibility and make it harder to resolve accounts efficiently.

- Falling for “quick fix” or high-fee solutions: Some debt relief options promise fast results but may involve high fees or unclear processes. Without proper understanding, these can complicate your situation rather than improve it.

- Not reviewing account details carefully: Moving forward without verifying balances, payment history, or account ownership can lead to errors. Clear and accurate information is essential for making informed decisions.

- Losing track of payments and communication: Disorganization can create confusion around what has been paid and what remains. Keeping records of payments, notices, and conversations helps maintain clarity throughout the process.

- Avoiding communication with account managers or collectors: Not engaging when questions arise can increase uncertainty. Clear communication helps you understand your account status and explore available options.

Avoiding these mistakes helps keep your debt repayment process structured and manageable. When you combine the right actions with awareness of these risks, it becomes easier to move forward with clarity and steady progress.

What Are Your Additional Support Options?

If managing bad debt feels difficult to handle on your own, there are structured support options available that can help you move forward with more clarity and control. These are designed to organize your situation, provide guidance, and create realistic repayment pathways based on your financial position.

Below are the key support options you can consider:

- Financial Counseling and Educational Resources: Beyond formal programs, financial education resources can help you improve budgeting, spending habits, and long-term financial planning. This support helps you not only address current debt but also build better financial stability moving forward.

- Legal Guidance for Complex Situations: If your situation involves disputes, unclear account details, or legal notices, seeking legal guidance can help you understand your rights and responsibilities. This can be especially useful if the situation becomes more complex or requires a formal response.

- Bankruptcy as a Last-Resort Option: In cases where debt cannot be realistically repaid, bankruptcy may be considered as a legal option. It can restructure or discharge certain debts depending on the situation. However, it involves long-term financial implications and should be approached carefully with proper guidance.

Also read: How to Manage Debt Stress: Practical Steps to Regain Control and Peace of Mind

You are not expected to handle everything alone. The right support can make the process of getting out of bad debt more structured, more transparent, and easier to manage over time.

Conclusion

Bad debt can feel like a cycle that keeps repeating itself. Payments go out, balances remain, and the end point feels unclear. What changes that experience is not a single decision, but a structured approach that gives you visibility, direction, and consistency.

Once you understand your accounts, follow a realistic plan, and avoid common setbacks, progress becomes easier to track and sustain. The process becomes less about reacting to pressure and more about steadily reducing what you owe.

If your account is being managed by The Forest Hill Management, the focus is on helping you stay in control of that process. With clear account information, secure payment options, and flexible repayment pathways, you have the support needed to move forward without unnecessary confusion.

Take the next step with clarity. Review your account, understand your options, and move ahead with a plan that works for your situation.

FAQs

1. How do I know if my debt situation is getting worse?

If your balances continue to grow despite making payments, or if you are relying on credit to cover regular expenses, it may indicate that your debt is becoming harder to manage.

2. Can I still make progress if I can only pay small amounts each month?

Yes, consistent small payments can still reduce your balance over time, especially when combined with a structured plan and controlled spending.

3. What should I do if I feel overwhelmed by multiple debts?

Start by organizing all your accounts in one place. Breaking the situation into smaller, manageable steps can help reduce confusion and make it easier to take action.

4. Is it okay to pause payments while figuring things out?

It is better to review your options and communicate with the account manager rather than pausing payments without a plan, as delays can lead to additional complications.

5. How can I avoid falling back into debt after paying it off?

Maintaining a clear budget, tracking your expenses, and staying aware of your financial commitments can help you avoid repeating the same cycle.