How to Get Out of a Debt Spiral Successfully

Need Help Reviewing Your Account?

Contact UsThere’s a point where debt stops feeling like something you’re managing and starts feeling like something you’re reacting to. Payments go out, balances shift, due dates come and go, but there is no clear sense of progress. It becomes harder to tell what is working and what is not.

That is what makes a debt spiral difficult. Not just the amount owed, but the lack of visibility and direction. When decisions are made one step at a time without a clear structure, it becomes easy for the situation to stay the same or gradually become more complex.

The way out is a shift toward clarity, structure, and consistent steps that work together over time.

In this blog, you will learn how to get out of a debt spiral, what causes it, how to recognize it early, and the exact steps and strategies that can help you move from uncertainty to a more stable and manageable position.

Key Takeaways

- A debt spiral happens when payments stop reducing your balance due to interest, multiple obligations, or ongoing borrowing.

- The first step to breaking the cycle is stopping new debt and gaining full clarity on what you owe.

- Structured actions like budgeting, prioritizing debts, and following a consistent repayment strategy help create steady progress.

- Small system changes, such as separating finances and tracking behavior, can prevent slipping back into the same cycle.

- Consistency and clear communication with your accounts are what turn effort into visible and lasting progress.

What Is a Debt Spiral?

A debt spiral is a situation where your debt continues to grow even though you are making payments. Instead of reducing what you owe, a significant portion of your payments goes toward interest, fees, or overdue charges, leaving the actual balance largely unchanged or, in some cases, increasing over time.

This usually happens when multiple financial pressures overlap. As balances grow and payments become harder to manage, you may rely on additional credit to stay current on expenses. Over time, this creates a cycle where new debt is used to manage existing debt, making it increasingly difficult to break out of the pattern.

What makes a debt spiral challenging is not just the amount owed, but the lack of clear progress. Without structure and visibility, it becomes difficult to see how and when the situation will improve.

Why It Happens?

A debt spiral rarely develops from a single decision. It is usually the result of several factors building up over time, often without immediate warning.

- High-interest rates that slow down repayment: When interest rates are high, a large portion of each payment is applied to interest rather than the principal. This makes it harder for balances to decrease, even with consistent payments.

- Reliance on credit for everyday expenses: When income does not fully cover regular expenses, credit cards or short-term borrowing may be used to fill the gap. Over time, this increases the overall debt load.

- Missed or reduced payments: Even occasional missed or partial payments can lead to additional charges and increased balances, which can disrupt repayment progress.

- Multiple overlapping debts: Managing several accounts at once can make it difficult to prioritize payments effectively, especially when each account has different terms and due dates.

- Unexpected financial disruptions: Events such as job loss, reduced income, or emergency expenses can quickly affect your ability to maintain consistent payments.

- Lack of clear financial visibility: When account details, balances, or repayment timelines are unclear, it becomes harder to make informed decisions, which can lead to delays or missteps.

Also read: How to Manage Multiple Loan Repayments Effectively

Understanding why a debt spiral happens is important because it shifts the focus from blame to structure. When the causes are clear, it becomes easier to identify what needs to change in order to move toward a more stable and manageable financial position.

Signs You May Be in a Debt Spiral

A debt spiral is not always obvious at first. It often shows up through small patterns that repeat over time. Recognizing these signs early can help you understand what is happening and take more structured steps to regain control.

Below are some of the most common indicators to look for:

- Your balances are not decreasing despite regular payments: You continue making monthly payments, but the total amount owed stays the same or reduces very slowly. This usually means interest and fees are offsetting most of your payments.

- You rely on credit to cover everyday expenses: If you find yourself using credit cards or short-term borrowing for essentials like groceries, bills, or rent, it may indicate that your current income is not covering your ongoing obligations.

- Minimum payments are becoming harder to manage: Meeting minimum payment requirements across multiple accounts may start to feel strained, especially when due dates overlap or income varies.

- Interest charges are increasing over time: A growing portion of your balance comes from interest rather than the original amount borrowed, making it harder to see progress.

- You are juggling multiple accounts without a clear plan: Managing several debts with different balances, rates, and due dates can create confusion, leading to reactive decisions instead of a structured approach.

- You are unsure of your total outstanding debt: If you do not have a clear understanding of how much you owe across all accounts, it becomes difficult to plan repayments or measure progress.

- You delay or avoid reviewing account details: Feeling overwhelmed can sometimes lead to avoiding statements, calls, or updates, which can make the situation harder to manage over time.

- You feel stuck despite ongoing effort: Even when you are trying to stay current with payments, it may feel like there is no clear path toward reducing your debt.

Recognizing these signs is not about labeling your situation. It is about gaining awareness. Once these patterns are clear, it becomes easier to move from uncertainty to a more structured and manageable approach.

How to Get Out of a Debt Spiral: Step-by-Step Plan

Getting out of a debt spiral requires two clear shifts. First, you stop the cycle from growing further. Then, you begin reversing it with structured and consistent actions. This process is about creating clarity, applying the right strategy, and following through over time.

Stop Adding New Debt Immediately

You cannot reduce debt while continuing to increase it. The first step is to stabilize your situation so that your current balances stop growing further.

- Pause credit card usage: Limit usage to essential transactions only, or stop entirely if possible. This prevents new balances from being added while you are trying to reduce existing ones.

- Avoid short-term borrowing options: Payday loans, personal loans, or quick credit solutions can increase pressure rather than solve it, especially when interest rates are high.

- Focus on maintaining current obligations: Prioritize keeping up with essential payments so your situation does not become more complex over time.

List and Organize All Your Debts

Clarity is one of the most important steps in breaking a debt spiral. When everything is documented in one place, it becomes easier to understand and manage.

- Bring all your accounts together in one place.

- Review each detail carefully to ensure accuracy.

- Use this list as your working foundation for the next steps.

Create a Survival-Level Budget

At this stage, your focus shifts from lifestyle to recovery. A survival-level budget helps you prioritize essential expenses and free up funds for repayment.

- Prioritize essential expenses first: Cover necessities such as housing, utilities, food, and transportation before allocating funds elsewhere.

- Reduce discretionary spending: Limit non-essential expenses temporarily to create more room for debt repayment.

- Identify realistic repayment capacity: Determine how much you can consistently allocate toward debt each month without creating additional strain.

You can use simple frameworks like the 50/30/20 rule as a guide, adjusting it to place a stronger emphasis on debt repayment during this phase.

Choose a Repayment Strategy

A structured repayment strategy gives direction and helps you stay consistent. Without it, payments may feel scattered and less effective.

- Debt avalanche method: Focus on paying off debts with the highest interest rates first. This approach helps reduce the overall cost of debt over time.

- Debt snowball method: Start by paying off the smallest balances first. This creates visible progress and can help build momentum.

- Choose based on what you can sustain: If motivation helps you stay consistent, the snowball method may work better. If reducing interest is your priority, the avalanche method may be more effective.

Pay Strategically, Not Randomly

Making payments without a clear plan can slow down your progress. A focused approach ensures that your efforts lead to measurable results.

- Prioritize one debt at a time: Direct extra payments toward a single target account while maintaining minimum payments on others.

- Maintain consistency across all accounts: Continue meeting minimum obligations to avoid penalties or further complications.

- Apply extra funds intentionally: Any additional money should be directed toward your priority debt to accelerate progress.

Increase Available Cash Flow

The speed at which you can reduce debt often depends on how much surplus you can create. Increasing available cash flow gives you more flexibility.

- Reduce everyday expenses where possible: Even small reductions in spending can add up and be redirected toward repayment.

- Use additional income effectively: Bonuses, refunds, or side income can be applied directly to reduce balances faster.

- Redirect saved amounts toward debt: Any money freed up through budgeting or reduced expenses should be used to support your repayment plan.

Stay Consistent and Track Progress

Progress in a debt spiral situation may feel slow at first, but consistency builds momentum over time.

- Track your balances regularly: Monitoring changes helps you stay aware of your progress and adjust your plan if needed.

- Monitor closed or reduced accounts: Seeing accounts fully paid off can help reinforce progress and maintain focus.

- Adjust your plan when necessary: Financial situations can change, and your approach should remain flexible enough to adapt.

Stay Engaged With Your Accounts

Staying connected with your accounts and communication channels can reduce confusion and prevent delays in your progress.

- Review account details carefully: Make sure you understand your balances, payment history, and any updates.

- Ask for clarification when needed: If anything is unclear, reaching out can help you avoid mistakes or misunderstandings.

- Maintain clear records of communication and payments: Keeping documentation ensures that you have a reliable reference for your progress and any agreements made.

Breaking out of a debt spiral is not about one single action. It is about applying a structured plan and following it consistently. Each step builds on the previous one, helping you move from uncertainty toward a more stable and manageable financial position.

Practical Strategies That Help Break the Debt Cycle

Once you have a structured plan in place, the next layer is how you sustain it. Breaking a debt cycle is not only about what you do once, but what you consistently do differently over time. These strategies focus on strengthening your approach, so progress continues without slipping back into the same pattern.

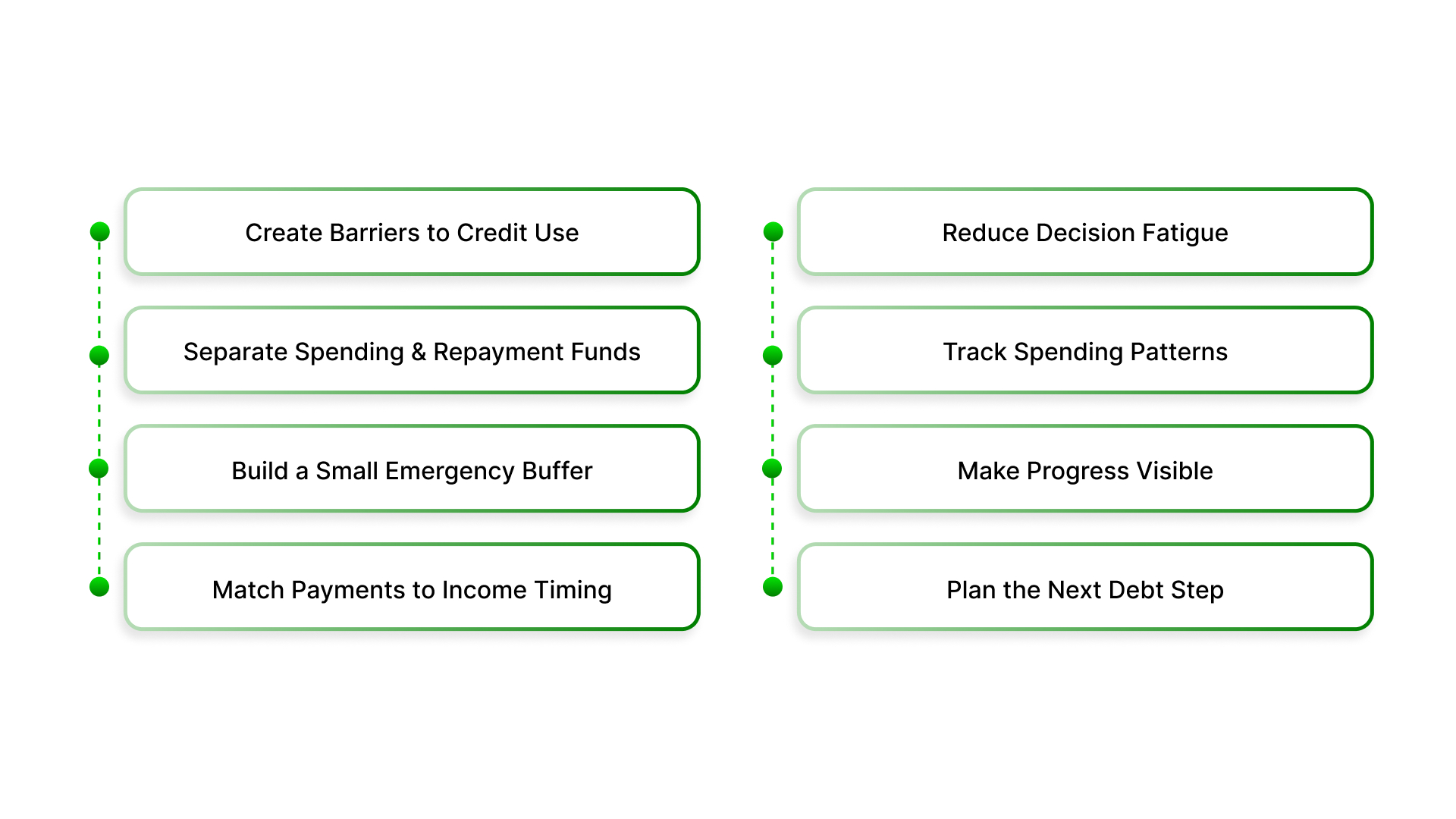

- Create Friction Between You and Credit Usage: Easy access to credit often leads to repeated usage without much thought. Introducing small barriers can help you make more deliberate decisions.

- Remove saved card details from apps and websites

- Keep credit cards out of immediate reach for daily spending

- Use debit or cash for routine expenses to stay within limits

- Separate Spending and Repayment Accounts: Mixing everyday spending with repayment funds can make it harder to stay consistent. Creating separation brings clarity and control.

- Maintain a dedicated account for bills and debt payments

- Transfer repayment amounts as soon as income is received

- Avoid dipping into repayment funds for discretionary use

- Build a Small Financial Buffer First: Even a minor unexpected expense can push you back into borrowing. Having a small reserve helps prevent that cycle.

- Set aside a modest emergency amount before accelerating payments

- Use this buffer only for genuine, unavoidable expenses

- Replenish it whenever it is used to maintain stability

- Align Payment Timing With Your Income Flow: Mismatched timing between income and payments often creates short-term pressure. Aligning the two can make repayments smoother.

- Schedule payments around your salary or income dates

- Break large payments into smaller, manageable parts if needed

- Avoid last-minute payments that depend on remaining funds

- Limit Financial Decision Fatigue: Too many choices and constant adjustments can lead to inconsistency. Simplifying decisions helps you stay on track.

- Standardize how much you pay and when you pay it

- Reduce the number of active repayment decisions each month

- Follow a fixed routine instead of rethinking your plan repeatedly

- Track Behavioral Patterns, Not Just Numbers: Progress is not only about balances. It is also about understanding habits that affect your financial decisions.

- Identify situations where overspending tends to happen

- Notice patterns around income cycles and spending spikes

- Adjust routines based on what consistently works or fails

- Create Visible Progress Markers: Debt reduction can feel slow without clear indicators. Making progress visible helps maintain motivation and direction.

- Track the percentage reduction in total debt

- Note milestones such as reduced balances or improved consistency

- Use simple trackers to visually see movement over time

- Plan for Transitions Between Debts: As one account is reduced or resolved, the next step should already be clear. This prevents loss of momentum.

- Redirect freed-up payment amounts immediately to the next account

- Maintain the same repayment intensity instead of easing off

- Keep your structure intact as your situation improves

Also read: Steps to Become Debt-Free: A Clear Financial Path

These strategies work because they address the underlying patterns that create and sustain debt cycles. Instead of relying on willpower alone, they build a system that supports better decisions, reduces friction, and keeps your progress steady over time.

Conclusion

A debt spiral can make progress feel invisible. You make payments, adjust your habits, and still feel like nothing is changing. That is what makes the situation difficult, not just the numbers, but the uncertainty that comes with it.

What changes that experience is structure. When you clearly understand your accounts, follow a consistent plan, and apply the right strategies, the cycle begins to shift. Progress may not be immediate, but it becomes visible, and more importantly, predictable.

If your account is being managed by The Forest Hill Management, the focus is on helping you move through this process with clarity rather than confusion. With structured account oversight, secure payment options, and flexible repayment discussions, you have a clear way to understand your position and take steady steps forward.

Take the first step toward breaking the cycle.

FAQs

1. Can I get out of a debt spiral without increasing my income?

Yes, many people start by restructuring their existing finances. While additional income can help, consistent budgeting and prioritization can still create progress.

2. What should I do if I feel overwhelmed by multiple debts?

Start by focusing on organizing all your accounts in one place. Clarity often reduces overwhelm and helps you decide your next step more confidently.

3. Is it normal for progress to feel slow at the beginning?

Yes, early progress may not always be visible, especially when interest is involved. Consistency over time is what creates noticeable change.

4. How do I avoid falling back into a debt cycle after making progress?

Maintaining structure is key. Keeping clear systems for spending, saving, and repayment helps prevent the same patterns from repeating.

5. When should I seek help or support with my debt?

If you are unsure about your account details, struggling to manage payments, or need clarity on your options, reaching out can help you move forward with more confidence.