Debt Collection Predictive Analytics for Easier Repayment

Need Help Reviewing Your Account?

Contact UsFinancial worries can make it hard to enjoy even a moment. The stress of falling behind on payments builds gradually, turning everyday life into a constant balancing act.

If this feels familiar, you’re not alone. Consumer debt continues to rise, with total debt increasing by 3.2% between 2024 and 2025.

When pressure is already high, resolving debt shouldn’t feel more confusing or overwhelming. Modern, data-driven systems now help make communication clearer, more manageable, and more supportive.

This article explains how debt collection predictive analytics works and why predictability matters. It also looks at how clearer systems support realistic repayment options and consumer protections.

Key Takeaways

- Predictive analytics can reveal patterns in payment behavior, helping you anticipate challenges and plan actions more strategically.

- Structured, data-driven systems reduce confusion and errors, making financial decisions clearer and less stressful.

- When available, structured repayment options that reflect real-life constraints (like income changes and essential expenses) can make plans easier to maintain.

- Maintaining accurate records and taking small, consistent steps empowers you to stay in control and avoid surprises.

- Expert guidance, like that from Forest Hill Management, can turn insights into actionable steps, providing clarity and confidence in managing debt.

What Does Debt Collection Predictive Analytics Mean?

In simple terms, predictive analytics looks at past account patterns, such as payment history, to help guide more thoughtful and consistent next steps.

For you, this often means fewer repeated contacts, clearer messages, and repayment options that better reflect real-life circumstances. Instead of confusing or unexpected communication, the process feels more structured and easier to follow.

Understanding how predictive analytics works is just the first step. Knowing why it matters for your peace of mind makes the difference.

Why Predictability Reduces Financial Anxiety?

Uncertainty often makes financial stress worse because it’s harder to plan your next step. When you are unaware of what’s next, the chances of making accurate decisions are reduced. Here’s how predictability helps:

- Clear expectations: Structured communication helps you understand when and how you may hear about your account.

- Organized records: Clear payment tracking and documented communication reduce confusion about what happened and what comes next.

- Less Fear of Surprise Changes: A consistent system always lowers the chances of sudden or unpredictable shifts in information.

- Improved Confidence: When you know your information is organized, decision-making becomes easier and your confidence increases.

Also Read: What to Do If Sued for Debt in California

A steady process like this reduces your mental load, and flexible and realistic repayment plans drop it even further.

How Repayment Plans Become More Realistic

Finances don’t always stay predictable. Income can change, emergencies happen, and everyday expenses can rise unexpectedly. Because of this, repayment plans today are designed to reflect real-life financial situations rather than fixed assumptions.

Here’s how modern systems make repayment plans more realistic:

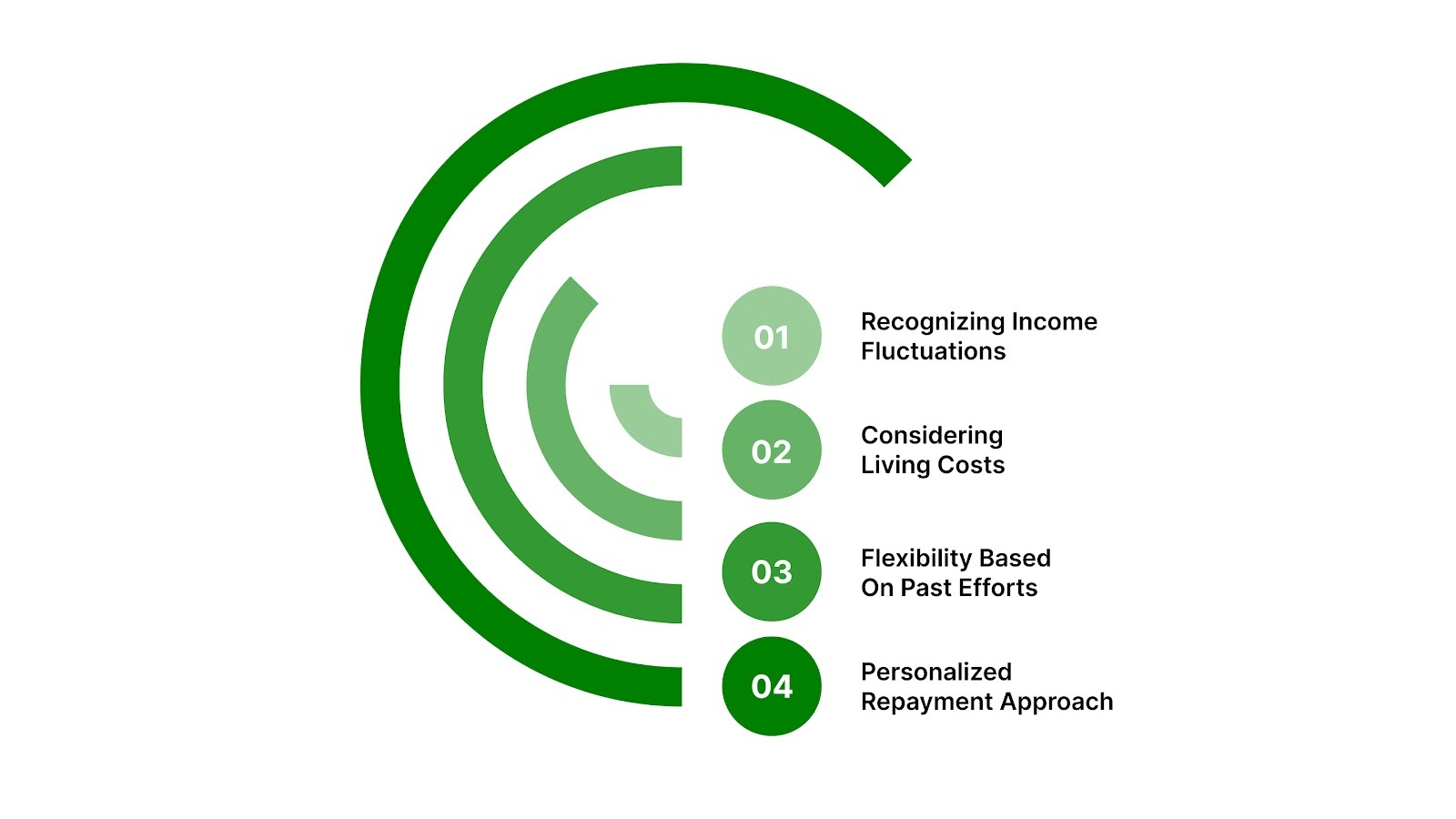

1. Recognition of Income Fluctuations

Income is not the same for everyone each month. When you share changes in income or timing (like seasonal work), payment arrangements can sometimes be adjusted to better fit your cash flow. Instead of assuming a stable salary, these tools analyze trends over time to determine what someone can consistently afford.

2. Consideration of Living Costs

Affordability is no longer judged in isolation from everyday expenses. Realistic arrangements work best when essential expenses (like rent, utilities, groceries, childcare, and medical needs) are taken into account. By factoring in real cost-of-living pressures, repayment expectations are set at levels that leave room for essential spending.

3. Flexibility Based on Past Efforts

Repayment planning also takes behavior into account. Even small, irregular, or partial payments show willingness and effort to manage obligations.

Instead of viewing missed or uneven payments as non-compliance, Past payment history can provide context for discussing amounts that are easier to maintain going forward.

4. Personalized Approach to Repayment

Data-driven tools help move away from one-size-fits-all repayment models. By reviewing payment history, income patterns, expense pressures, and previous arrangements, systems can suggest more personalized plans.

This personalized structure increases the likelihood of long-term success, as the plan is shaped around actual capacity rather than standardized expectations.

Also Read: Pay Recovery Guide: Resolve Debts Before They Escalate

With all the data made available, it is also important that your consumer rights are not violated.

How Better Systems Help Protect Your Rights?

Account resolution in the US operates under consumer protection rules, which guide how communication and information must be handled. Modern systems can support compliance by helping keep records accurate and communication consistent.

- Reduced risk of incorrect or outdated account details that may create problems in the future.

- All your payment histories and balances are accurately recorded with these advanced systems.

- You will see a controlled communication frequency where structured systems help prevent unnecessary outreach.

- Digital processes are built to manage personal and financial data more safely than ever, leading to secure information handling.

- When information is clear, there are always fewer disputes caused by errors.

It is up to you to overcome the debt you are in by following the necessary steps to gain control.

Small Steps That Help You Regain Control

Taking small, consistent actions can help you feel more confident and in control of your financial situation.

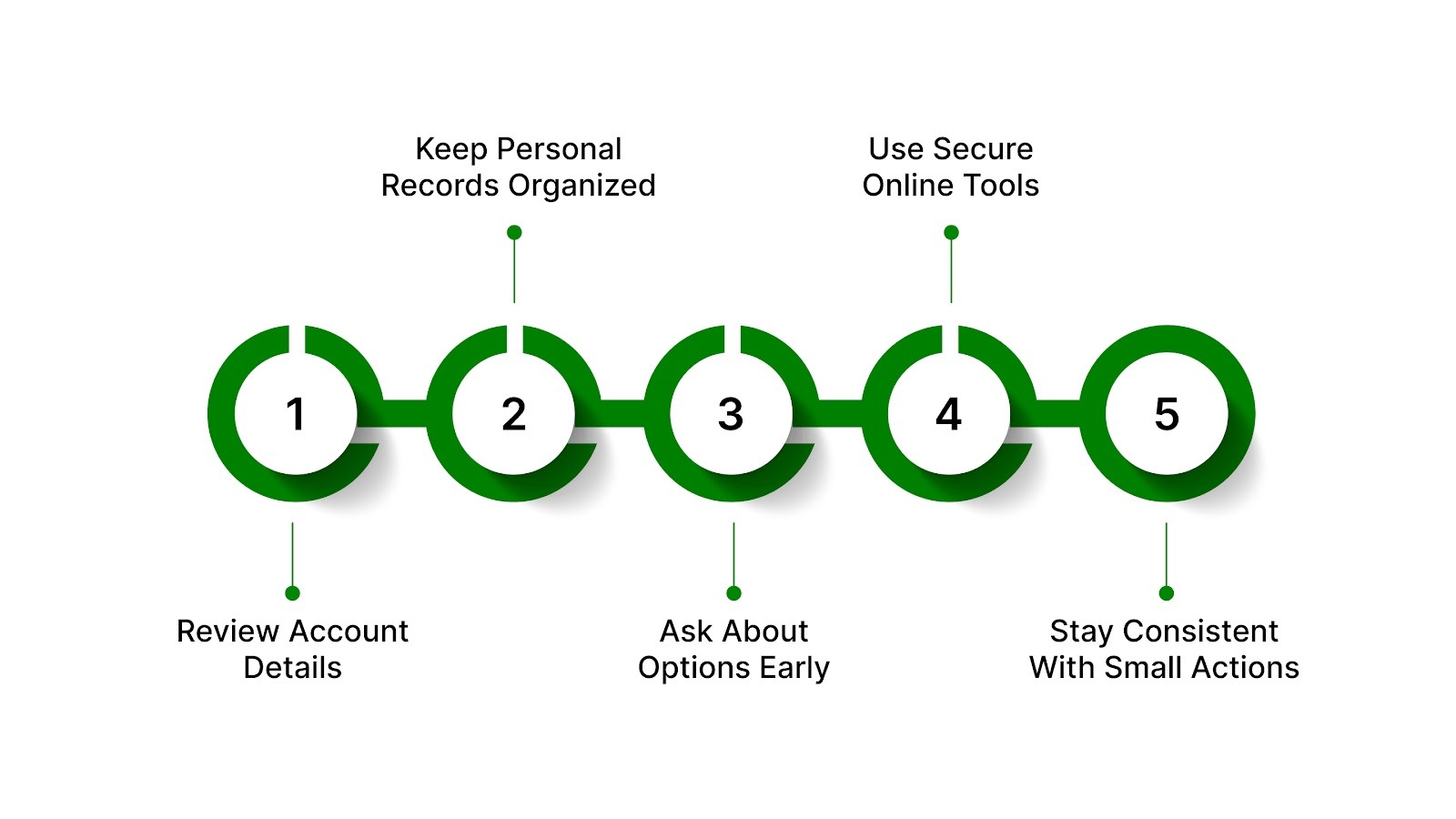

1. Review Your Account Details Carefully

Take time to understand your current balance, recent transactions, and any upcoming due amounts. Regularly checking your account helps you spot errors, track progress, and avoid surprises that could disrupt your plans.

2. Keep Personal Records Organized

Save payment confirmations, emails, and letters so you always have proof of past actions and agreements. Making brief notes after phone conversations also helps you remember key details, dates, and any commitments discussed.

3. Ask About Options Early

Reaching out early gives you more flexibility and a wider range of possible solutions to consider. When you communicate before a situation becomes urgent, support teams can often suggest arrangements that are easier to manage.

4. Use Secure Online Tools

Digital platforms make it easier to check balances, track payments, and manage plans at any time. Using secure online tools also reduces paperwork and helps you stay updated without waiting for phone or mail responses.

If you agree to any plan or settlement, ask for the terms in writing and save the confirmation.

5. Stay Consistent With Small Actions

Steady, manageable steps build progress over time and reduce the pressure of trying to fix everything at once. Consistency creates stability, which makes it easier to stick to plans and regain a sense of financial control.

Also Read: Debt Collection Advice: Know Your Rights and Options

By taking these steps, you’re already regaining control, but having a clear path and expert support can make the process easier and less stressful.

How Forest Hill Management Supports a Clearer Path Forward

When accounts start piling up, it’s easy to feel stuck or unsure which step to take first. Many people delay action simply because they don’t know where to begin. Forest Hill Management helps you move forward with confidence by offering clear guidance, timely support, and practical ways to regain control of your situation.

Here’s how we support you:

- Clear support when you contact us: We help explain your account details and available options so you can choose a manageable next step.

- Step-by-Step Guidance: Each part of the process is explained in plain language, so you know what’s coming and what actions to take.

- Flexible options when available: If you’re eligible, we can discuss repayment arrangements that fit your situation and help you stay consistent.

- Clear, Informed Decision-Making: You receive straightforward information that helps you understand your choices and select what feels manageable.

- Respectful, Human Communication: Every interaction is focused on clarity and support, never pressure or intimidation.

Our goal is to keep the process clear, respectful, and structured so you can move forward with fewer surprises.

Conclusion

Debt doesn’t have to feel unpredictable or chaotic. Understanding patterns, anticipating challenges, and seeing the bigger picture can make the entire process feel more navigable. By approaching your accounts with awareness and clarity, you can make informed decisions that fit your unique situation.

When you’re ready to move forward, Forest Hill Management can help turn understanding into action and guide you toward responsible next steps.

Take the next step toward resolving your accounts - explore your options with Forest Hill Management today.

FAQs

1. Does predictive analytics decide how much I must pay?

No, predictive analytics does not make final decisions on its own. It helps identify patterns and affordability indicators, but repayment arrangements are still reviewed within guidelines and adjusted based on individual circumstances.

2. Will using data-driven systems affect my credit score?

Predictive analytics itself does not directly impact your credit score. Your credit file is influenced by reporting activity and payment behavior, not by the internal tools used to manage communication or repayment planning.

3. Can predictive analytics help reduce account disputes?

Yes, better data organization and tracking can lower the chances of misunderstandings about balances, payment history, or past communication. When records are clearer and more consistent, it becomes easier to resolve questions quickly and accurately.

4. What if my financial situation changes after a plan is set?

If your income drops or expenses increase unexpectedly, you can request a review of your arrangement. Repayment plans can often be reassessed to reflect new circumstances rather than remaining fixed.

5. Is my personal financial information safe in these systems?

Modern account management systems use secure digital processes to store and handle financial data. These systems follow strict privacy and data protection standards designed to keep your information protected.