How Long Does It Take to Pay Off Debt?

Need Help Reviewing Your Account?

Contact UsTwo people can have the same amount of debt and still take completely different amounts of time to pay it off.

One clears it in a couple of years. The other stays in it for much longer, even while making regular payments. The difference is not always income or effort. It often comes down to how the debt is structured, how payments are made, and how clearly the situation is understood.

This is especially relevant today. With average credit card balances per borrower hovering around $6,715 in recent U.S. data, many people are actively paying down debt, but not always seeing fast results. The gap between effort and outcome is what creates confusion.

The question is not just how much you owe. It is how that amount behaves over time.

In this blog, you will learn how long it takes to get out of debt, what actually influences that timeline, realistic payoff scenarios, and how you can shorten that timeline with a more structured and informed approach.

Key Takeaways

- Debt payoff timelines vary widely, and two people with similar balances can take very different amounts of time depending on how their accounts are managed.

- Monthly payments, interest rates, balance size, and consistency all work together to shape how quickly your debt reduces.

- Certain types of debt, especially high-interest or revolving accounts, can quietly extend repayment if not handled with a clear plan.

- Small, structured changes in how you manage payments and spending can significantly shorten your overall timeline.

- Clarity and consistency matter more than speed. A well-structured approach helps you make steady and predictable progress over time.

How Long Does It Take to Get Out of Debt?

The honest answer is that there isn’t a single fixed timeline. What most people are really asking is whether this will take months, years, or much longer. The reality sits somewhere in between, and it becomes clearer once you look at real-world timelines rather than guesses.

In general, debt payoff tends to fall into a few broad ranges:

These are not strict categories, but they help set realistic expectations. Many people find themselves in the middle range, where progress is steady but takes time.

To make this more tangible, here are a few simplified examples:

- Around $5,000 in debt can often be cleared within about a year with consistent payments.

- Around $10,000 in debt may take close to 2 years depending on the repayment pace.

- Around $20,000 in debt can take anywhere from 2 to 6 years or more, depending on how it is managed.

What stands out in these examples is not just the amount, but how much the timeline can vary for the same balance. This is why two people with similar debt can have very different outcomes.

It is also important to understand that paying only the minimum on certain types of debt, especially credit cards, can stretch repayment far beyond these ranges. In some cases, it can take decades to fully clear a balance if progress remains slow.

The key takeaway here is simple:

- There is no fixed timeline for all

- Most debt payoff journeys take longer than expected, but shorter with structure

- Your timeline becomes clearer once you look at your own numbers

Also read: How to Manage Multiple Loan Repayments Effectively

This sets the foundation for the next step, which is understanding exactly what influences your personal timeline and how it can be shaped over time.

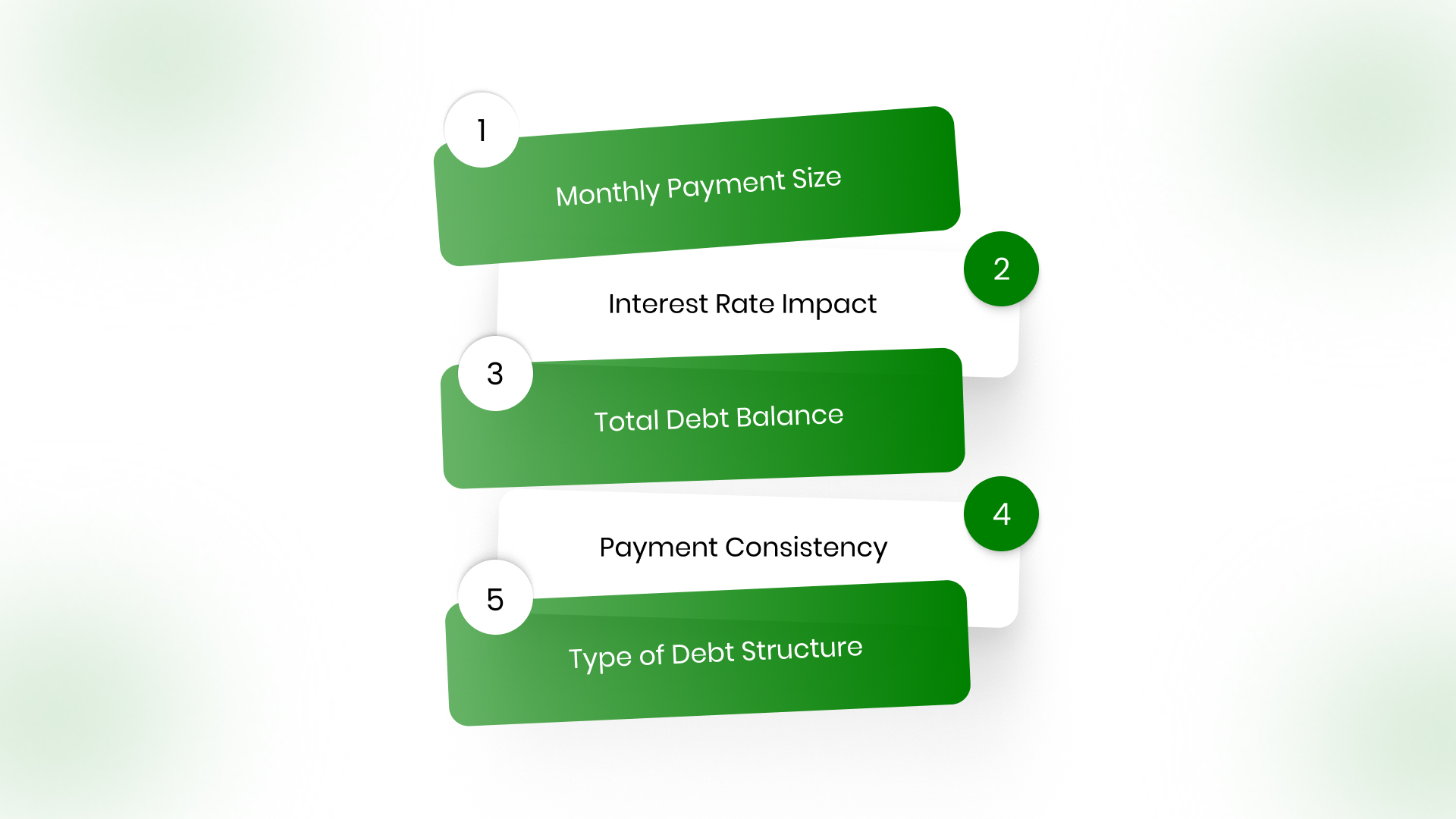

What Determines How Long It Takes to Pay Off Debt?

Once you know the timeline is not fixed, the next question is what actually shapes it. In practice, the answer usually comes down to how much you pay each month, how much interest the debt carries, how large the balance is, how consistently you pay, and what type of debt you are dealing with.

These are the core factors that influence how quickly your balance reduces and how much progress you make month after month.

Monthly Payment Amount

Your monthly payment is the most direct way to influence how fast your debt goes down. It determines how much of your balance you are actively reducing every month.

- Larger payments reduce the principal faster, which shortens the overall repayment period.

- Smaller payments extend the timeline because a lower portion goes toward reducing the actual balance.

- Even moderate increases in your monthly payment can significantly change how long repayment takes.

The key idea here is simple: the more you put toward your debt each month, the faster it reduces.

Interest Rate (APR)

Interest works in the background of every payment you make. Before your payment reduces the actual balance, a portion is often applied toward interest, especially in the earlier stages.

- Credit card interest rates commonly range between 15% and 25%, which can significantly increase the total cost.

- Higher interest rates mean a larger share of your payment goes toward interest rather than reducing the balance.

- Lower interest allows more of your payment to go directly toward repayment.

Interest quietly extends your timeline by slowing how quickly your balance decreases.

Total Debt Balance

The total amount you owe sets the scale of your repayment journey. Larger balances naturally require more time, even when payments are consistent.

- Higher balances take longer to reduce because each payment makes a smaller proportional impact.

- When combined with interest, larger debts can grow more complex to manage over time.

- Smaller balances are easier to clear quickly, which is why some strategies focus on resolving them first.

The size of your debt does not determine everything, but it does set the scale of the effort required.

Payment Consistency

Consistency plays a critical role in maintaining progress. Even a well-planned repayment strategy can lose effectiveness if payments are irregular.

- Missing or delaying payments can slow progress and increase the total amount paid.

- Consistent payments keep the balance moving downward in a predictable way.

- Regular payment patterns also make it easier to track progress and stay organized.

In many cases, steady and reliable payments matter more than occasional larger contributions.

Type of Debt

Not all debt behaves the same way. The structure of the account can influence how predictable or flexible your repayment timeline is.

- Revolving debt (like credit cards) has no fixed end date, which means timelines can extend without a clear plan.

- Installment loans (like personal or auto loans) follow a defined schedule, making timelines more predictable.

- Accounts under structured management often provide clearer repayment pathways and visibility.

The type of debt affects how structured and predictable your repayment journey will be.

Together, these factors determine how your timeline actually unfolds. Once you understand how each one works, you can start to see the different kinds of debts that you should be aware of.

What Kinds of Debts Should You Be Careful About?

Not all debt affects your timeline in the same way. Some types of debt require closer attention because they can quietly extend repayment, increase costs, or create confusion if not managed carefully. Recognizing these early helps you stay in control and avoid unnecessary delays.

- High-Interest Credit Card Debt: Credit cards often carry higher interest rates, which means a significant portion of your payment may go toward interest instead of reducing the actual balance. Over time, this can slow progress and increase the total amount paid. If only minimum payments are made, these balances can remain active far longer than expected.

- Revolving Debt With No Fixed End Date: Unlike structured loans, revolving debt does not come with a defined repayment timeline. As long as payments are made, the account stays open, which can make it easy for balances to linger. Without a clear plan, repayment can stretch indefinitely.

- Accounts With Variable or Increasing Interest Rates: Some debts do not stay constant. Interest rates may change over time, which can increase the overall cost of the debt even if your payment amount remains the same. This can quietly extend your repayment timeline without it being immediately noticeable.

- Past-Due or Transferred Accounts: When accounts move into a past-due status or are transferred to another organization for management, they often require more attention. Details such as balances, ownership, and payment history should be reviewed carefully to ensure clarity and avoid confusion during repayment.

Also read: How to Pay Off Debt in Collections Safely

- Multiple Small Debts Across Different Accounts: Managing several smaller debts can be more complex than handling one larger balance. Multiple due dates, varying balances, and scattered information can make it harder to stay consistent and track progress effectively.

- Debts Without Clear Documentation or Visibility: If account details are unclear or not easily accessible, it becomes difficult to verify balances, track payments, or make informed decisions. Lack of clarity can slow down progress and create hesitation in moving forward.

Understanding these types of debt does not mean they cannot be managed. It simply helps you identify where extra attention is needed so your repayment process stays structured, consistent, and easier to follow.

Practical Ways to Shorten Your Debt Payoff Timeline

Speeding up debt repayment is not just about paying more. It is about making your payments work smarter, reducing friction in the process, and staying consistent without burning out. The most effective approaches are usually simple, repeatable, and built around your real financial habits.

Here are strategies that go beyond the obvious and actually help you move faster in a sustainable way.

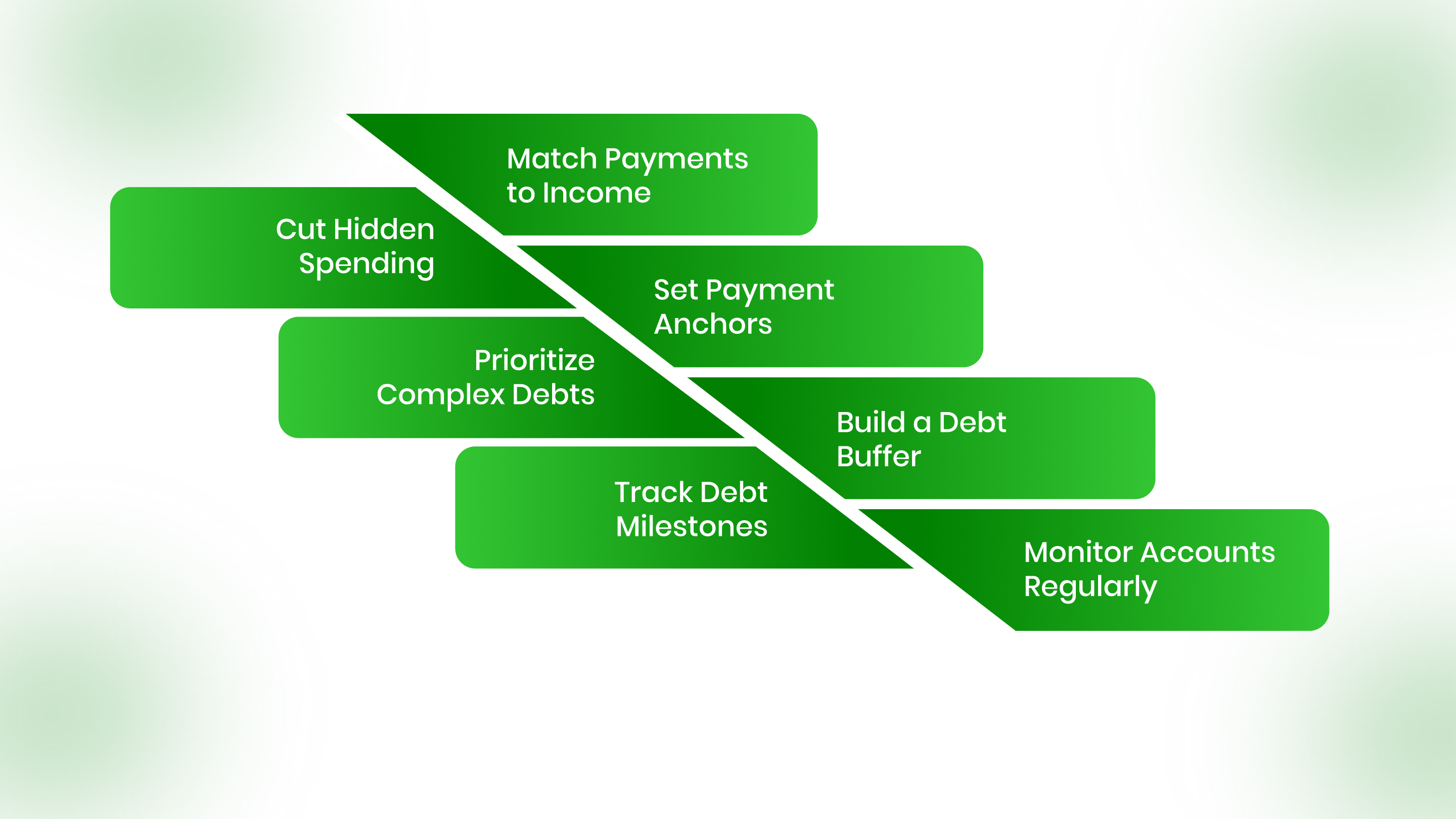

Align Your Payments With Your Income Cycle

Instead of treating debt as a once-a-month obligation, align your payments with how you earn.

- Split your monthly payment into smaller parts that match your paydays.

- This reduces the risk of running short at the end of the month.

- It also keeps your balance moving down more frequently rather than in one large step.

This approach makes repayment feel more manageable and keeps your progress steady.

Target “Dead Zones” in Your Spending

Most budgets fail not because of big expenses, but because of small, unnoticed ones.

- Identify categories where money quietly leaks such as subscriptions, impulse purchases, or irregular spending.

- Redirect those amounts directly toward debt rather than absorbing them elsewhere.

- Even small recovered amounts can create consistent monthly impact.

This strategy works because it improves your repayment capacity without changing your overall lifestyle drastically.

Use “Payment Anchors” to Stay Consistent

Consistency improves when payments are tied to something predictable.

- Link your debt payments to fixed events like salary credits, rent payments, or bill cycles.

- Treat debt repayment as a non-negotiable obligation, not a flexible expense.

- This reduces decision fatigue and builds a routine around repayment.

Over time, this makes progress feel automatic rather than effort-driven.

Prioritize High-Friction Accounts First

Some debts create more stress or confusion than others. Addressing these early can improve your overall momentum.

- Focus on accounts that are harder to track, have higher pressure, or create uncertainty.

- Clearing or stabilizing these accounts simplifies your overall financial picture.

- This often makes it easier to stay consistent across all remaining accounts.

Reducing complexity can be just as important as reducing balance.

Create a “Debt Buffer” for Stability

Unexpected expenses often disrupt repayment plans. A small buffer can prevent setbacks.

- Set aside a modest amount for emergencies while continuing repayments.

- This reduces the need to rely on credit again during unexpected situations.

- It helps maintain consistency even when financial conditions change.

Stability allows your repayment plan to continue without interruption.

Track Progress in Terms of Milestones

Focusing only on the total amount can feel discouraging. Breaking it into milestones improves motivation.

- Track the number of accounts reduced or closed.

- Monitor percentage reduction instead of only total balance.

- Recognize progress in stages rather than waiting for the final outcome.

This keeps you engaged and makes long timelines feel more achievable.

Stay Actively Engaged With Your Accounts

Clarity plays a bigger role than most people expect in speeding up debt payoff.

- Regularly review your account details, balances, and payment history.

- Ask questions if something feels unclear or inconsistent.

- Keep your records organized so you always know where you stand.

When your information is clear, your decisions become faster and more confident.

These approaches focus on behavior, structure, and consistency. Instead of relying on occasional large payments, they help you build a system where progress happens regularly and predictably.

Conclusion

Debt timelines are rarely obvious at the start. They become clearer once you understand how your balance, payments, and account structure work together over time.

What this really means is that your timeline is not something you have to guess. It is something you can shape. With the right information and a consistent approach, what once felt uncertain starts to feel more defined.

Progress does not always look fast, but it becomes meaningful when it is steady and structured. Knowing where you stand and what comes next makes it easier to stay consistent and avoid setbacks.

If your account is being managed by The Forest Hill Management, the focus is on giving you that structure. With clear account visibility, secure payment options, and flexible repayment discussions, the process becomes easier to follow and easier to manage.

You do not need to predict the entire timeline today. Start by taking the first step toward clarity.

FAQs

1. Can my debt payoff timeline change after I’ve already started?

Yes, your timeline can shift at any point. Increasing payments, reducing interest impact, or improving consistency can shorten it, while missed payments or changes in financial situation can extend it.

2. Is it possible to estimate my exact debt-free date?

You can get a close estimate using your current balance, payment amount, and interest rate. However, changes in payments or account conditions can affect the final timeline.

3. Should I focus on paying off one account completely or multiple at the same time?

Focusing on one account at a time while maintaining minimum payments on others often creates clearer progress and helps maintain consistency.

4. What should I do if my timeline feels too long or discouraging?

Break it into smaller milestones. Focusing on progress in stages, rather than the full timeline, can make the process feel more manageable and help you stay engaged.

5. How do I know if I’m actually making progress?

Look beyond the total balance. Consistent payments, reduced interest impact, and fewer active accounts are all signs that your situation is improving.