How to Respond to a Debt Collector: 7 Smart Steps

Need Help Reviewing Your Account?

Contact UsMost people don’t struggle with the idea of becoming debt-free. They struggle with the starting point. When you have multiple balances, different due dates, and unclear totals, the problem is not motivation, it is lack of structure. Without a clear path, even small debts can feel harder to manage than they actually are.

That is why so many repayment efforts stall. Not because people are not trying, but because the process feels scattered. What works is not a drastic change, but a system that helps you see your situation clearly and act on it step by step.

In this blog, you will learn the steps to become debt free, how to organize your finances in a way that makes sense, and the strategies that help you move forward consistently without confusion.

Key Takeaways

- Responding to a debt collector is most effective when you follow a structured process instead of reacting quickly or emotionally.

- Verifying the collector, requesting validation, and reviewing details gives you control before making any decisions.

- Your legal rights protect you from unfair practices and ensure you have time to review, dispute, and respond appropriately.

- Keeping records and setting communication boundaries helps reduce confusion and keeps the process organized.

- Most debt situations can be resolved through clear communication and realistic repayment options without immediate escalation.

What to Expect When a Debt Collector Contacts You?

The first contact from a debt collector often creates uncertainty, mostly because it is unfamiliar. In reality, there is a structured process behind it, and understanding what typically happens can help you approach the situation with more clarity and less confusion.

Debt collectors usually reach out when an account has become past due and is being managed for repayment. This does not automatically mean legal action is underway. In most cases, it is an initial step to establish communication, share account details, and provide you with options to review and respond.

Here is what you can generally expect during this stage:

- Initial communication through multiple channels: You may be contacted by phone, email, text message, or a formal letter. The method can vary, but the purpose remains the same, to inform you about the account and initiate a conversation.

- Details about the account and creditor: The communication should include information about the amount owed and the name of the current or original creditor. This helps you identify which account is being referenced.

- A validation notice with your rights: Within the first few communications, you should receive written information outlining the debt details and your right to dispute or request verification. This is a standard part of the process and is designed to give you time to review the information.

- An opportunity to ask questions and clarify information: You are not expected to make immediate decisions. This stage allows you to understand the account, verify details, and determine your next step.

- Structured and compliant communication practices: Debt collectors are required to follow specific guidelines around how and when they can contact you. This helps ensure that communication remains respectful and within defined limits.

- No immediate enforcement action without formal process: Legal actions, such as lawsuits or wage garnishment, require separate formal steps. Initial contact is not the same as legal escalation.

Understanding these expectations helps you approach the situation with a clearer perspective. Instead of reacting quickly, you can take a moment to review the information, gather details, and decide how you want to respond.

Also read: How to Make a Budget and Get Out of Debt

This clarity makes the next step easier, knowing exactly how to respond to a debt collector in a structured and informed way.

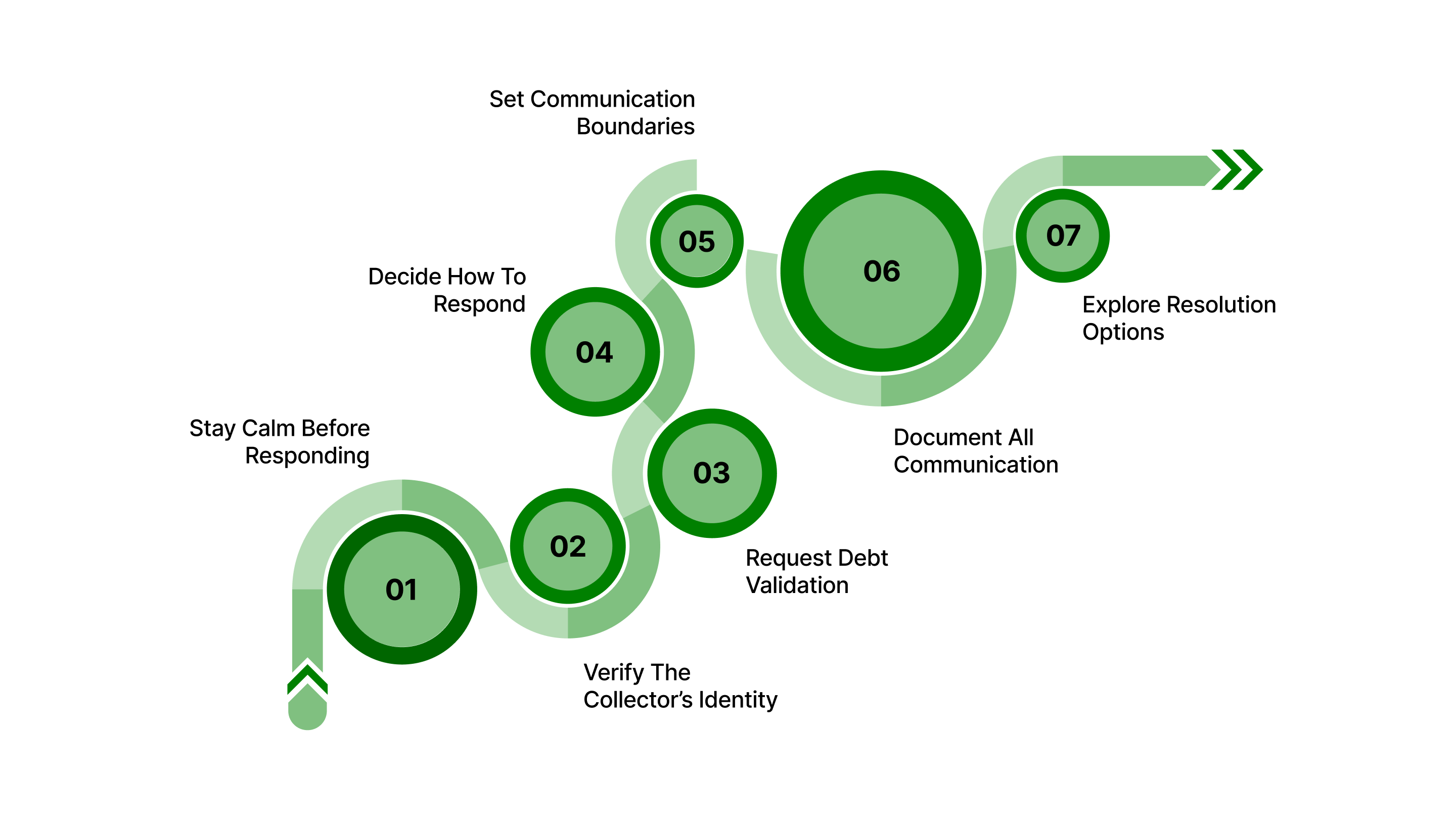

7 Steps to Responding to a Debt Collector

Responding to a debt collector is not about reacting quickly. It is about following a clear, structured process to verify information, protect your rights, and make informed decisions. U.S. consumer protection rules are designed to give you time and control, especially in the early stages of contact.

Step 1: Stay Calm and Do Not Commit Immediately

The first interaction often feels urgent, but there is no requirement to make a decision right away. In fact, rushing can lead to agreeing to terms without full clarity.

- Avoid verbal commitments during the first interaction: Anything you say can be documented by the collector and used as part of the account record. It is better to wait until you have reviewed all details before agreeing to anything.

- Focus on gathering accurate information first: Treat the first conversation as an information-gathering step. Understanding the account clearly is more important than resolving it immediately.

- Give yourself time to review before responding: You are allowed to pause, review documents, and respond later. This helps ensure your decisions are based on facts, not pressure.

Step 2: Verify Who You Are Speaking With

Before discussing any details, confirm that the contact is legitimate. This helps protect you from errors or potential scams.

- Ask for the collector’s full name and company details: This ensures transparency and allows you to confirm that the agency is authorized to contact you.

- Request official contact information: Having a phone number, address, or website allows you to independently verify the organization if needed.

- Confirm the original creditor: Debt collectors are required to provide the name of the creditor and the amount owed, helping you match the account with your own records.

Step 3: Request Debt Validation

You have a legal right to receive written proof of the debt. This step is one of the most important protections available to you.

- Review the full amount and how it is calculated: The validation notice should include the total balance and any applicable charges or adjustments.

- Confirm the creditor and account origin: This ensures the debt is correctly linked to you and not a reporting error.

- Understand your 30-day dispute window: You typically have 30 days to dispute the debt after receiving validation information.

- Use your right to pause collection activity: If you dispute the debt in writing within this period, the collector must stop collection efforts until they provide verification.

This step protects you from paying a debt that may be incorrect, incomplete, or not yours.

Step 4: Decide Your Position (Acknowledge, Dispute, or Clarify)

Once you have the details, you can decide how to proceed. Every situation is different, and your response should reflect your specific circumstances.

- If the debt is valid, move toward resolution: You can begin exploring repayment options that align with your stable financial situation.

- If you are unsure, request additional clarification: You can ask for more documentation or explanation before making any decision.

- If the information is incorrect, submit a formal dispute: A written dispute ensures the issue is reviewed and documented properly, helping prevent further confusion.

- Check the statute of limitations before taking action: If the debt is several years old, it is important to understand your state’s statute of limitations for filing a lawsuit to collect it. In many cases, this time period begins from your last activity on the account. This could include:

- your last payment

- the last time you used the account

- a promise to pay

- entering into a payment arrangement

- or even acknowledging that the debt is yours

The exact timeline depends on the type of debt and the laws of your state or the terms outlined in your original agreement.

Reviewing this before making any commitments helps ensure you fully understand your position and avoid unintentionally resetting timelines.

Step 5: Keep Communication Structured and Documented

Documentation gives you control over the process. It ensures that every step is clear, traceable, and verifiable.

- Save all written communication: Keep copies of letters, emails, and notices for reference and future use.

- Log phone calls and interactions: Note dates, times, and key points discussed. This creates a timeline of communication.

- Keep proof of payments and agreements: Payment confirmations and written agreements help prevent disputes later and confirm your progress.

- Use written communication when possible: Written records reduce misunderstandings and provide clarity if questions arise later.

Step 6: Set Communication Boundaries

You have the right to control how a debt collector communicates with you. Setting boundaries can make the process more manageable.

- Request communication in writing: This gives you time to review information carefully and creates a clear record of all interactions.

- Specify convenient times for contact: Debt collectors must follow guidelines regarding when they can contact you.

- Send a stop-contact request if needed: You can request that communication stops, although this does not remove the debt itself.

- Understand what boundaries do and do not do: Limiting communication helps reduce stress, but it does not stop the underlying process or obligation.

Step 7: Explore Resolution Options

Once you have clarity, most debt situations can be resolved through structured and manageable approaches rather than escalation.

- Discuss structured payment plans: These allow you to repay the balance gradually in a way that fits your financial situation.

- Explore settlement options where applicable: In some cases, accounts may be resolved through negotiated terms.

- Focus on realistic and sustainable arrangements: A manageable plan is more effective than one that creates additional financial strain.

- Keep agreements documented and clear: Written confirmation ensures both sides understand the terms and expectations.

Following these steps allows you to move from uncertainty to clarity. Instead of reacting to the situation, you are actively managing it with structure, information, and control.

If your account is being handled by The Forest Hill Management, this process is designed to feel structured and transparent rather than overwhelming. With clear account information, compliant communication practices, secure payment options, and flexible repayment discussions, you are given the space to understand your situation and move forward at a pace that works for you.

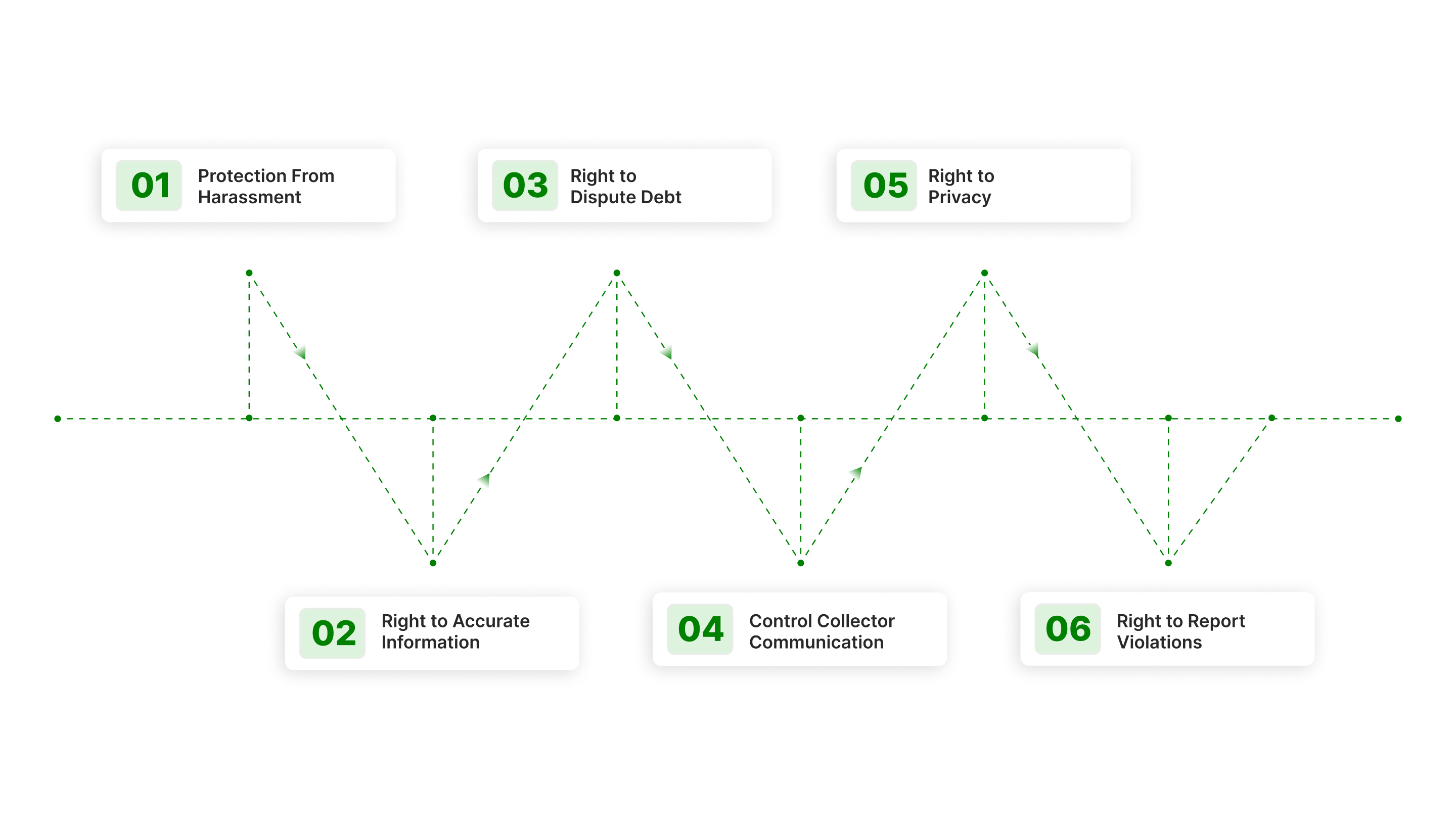

Your Rights When Dealing With a Debt Collector

When you are contacted about a debt, the process is not unregulated or one-sided. U.S. law, particularly the Fair Debt Collection Practices Act (FDCPA), sets clear boundaries on what debt collectors can and cannot do. These rules are designed to protect you from unfair treatment and ensure that the process remains transparent and manageable.

Understanding your rights helps you respond with confidence rather than uncertainty.

Protection From Harassment or Unfair Practices

Debt collectors are not allowed to pressure or intimidate you. The law clearly prohibits abusive behavior during collection efforts.

- No harassment or repeated calls meant to pressure you: Collectors cannot call continuously or excessively with the intent to harass or overwhelm you.

- No threats, abusive language, or misleading statements: They cannot threaten legal action they do not intend to take or use deceptive tactics to force payment.

- No unfair practices during collection: The FDCPA prohibits any unfair or deceptive methods used to collect a debt.

Right to Clear and Accurate Information

You are entitled to understand exactly what the debt is and where it comes from before taking any action.

- Right to receive a validation notice: Collectors must provide details about the debt, including the amount owed and the creditor’s name.

- Right to verify the debt’s accuracy: You can request written confirmation to ensure the debt belongs to you and the details are correct.

- Right to question unclear or incomplete information: If anything does not match your records, you can request clarification before proceeding.

Right to Dispute the Debt

If you believe the debt is incorrect, incomplete, or not yours, you have the right to challenge it.

- Dispute within the allowed timeframe (typically 30 days): This gives you the opportunity to review and question the debt formally.

- Collection activity must pause during verification: If you dispute the debt in writing, the collector must stop collection efforts until they provide verification.

- Protection against paying incorrect or invalid debts: This process ensures you are not obligated to act on inaccurate information.

Right to Control Communication

You have control over how and when a debt collector can contact you.

- Limits on contact times: Collectors generally cannot contact you before 8 a.m. or after 9 p.m. without permission.

- Right to request preferred communication methods: You can ask for communication in writing or limit certain types of contact.

- Right to request that communication stops: You can send a written request asking the collector to stop contacting you, although this does not remove the debt itself.

Right to Privacy

Your financial situation is protected, and collectors must respect your confidentiality.

- Limited third-party communication: Collectors cannot discuss your debt with friends, neighbors, or coworkers without your permission.

- Contact with others is restricted: They may only reach out to others to locate you, and even then, they cannot disclose details about the debt.

- Protection of personal information: Your account details must be handled securely and used only for legitimate collection purposes.

Right to Take Action if Rules Are Violated

If a debt collector does not follow the law, you have options.

- You can file a complaint with regulatory authorities: Agencies like the Consumer Financial Protection Bureau (CFPB) review and respond to complaints.

- You may have the right to take legal action: Consumers can pursue action against collectors who violate the FDCPA.

Understanding these rights changes how you approach the situation. Instead of feeling pressured or uncertain, you can respond with clear expectations, knowing that the process is governed by rules designed to protect you.

Also read: What to Do If Sued for Debt in California

This foundation makes it easier to move forward, communicate effectively, and handle the situation in a structured and informed way.

Conclusion

Becoming debt-free does not come from doing everything at once. It comes from doing the right things in the right order and repeating them consistently. When your finances are organized and your actions are structured, progress stops feeling uncertain and starts becoming measurable.

The real shift happens when you move from reacting to your debt to actively managing it. That is where clarity replaces stress, and steady progress replaces hesitation.

If your account is being managed by The Forest Hill Management, the goal is to support that shift. With clear account information, structured communication, and practical repayment options, you are able to move forward with a plan that makes sense for your situation.

Take the first step toward financial freedom.

FAQs

1. What should I do if a debt collector contacts me about a very old debt?

Before taking any action, check your state’s statute of limitations. If the debt is too old, legal action may no longer be enforceable, but you should still review details carefully before responding.

2. Is it better to communicate with a debt collector by phone or in writing?

Written communication is generally easier to track and review, especially when you need clear records of what was discussed or agreed upon.

3. Can I negotiate the terms of repayment with a debt collector?

In many cases, repayment terms can be discussed. The key is to ensure any agreement is realistic for your situation and confirmed in writing.

4. What happens if I accidentally acknowledge a debt before verifying it?

Acknowledging a debt can sometimes affect timelines or your position, depending on the situation. It is best to verify all details first before making any statements or commitments.

5. How do I know if a debt collector is legitimate or a scam?

A legitimate collector should provide clear company details, contact information, and written validation of the debt. If this information is missing or unclear, take time to verify before proceeding.