Recover Unpaid Personal Loan: 5 Practical Steps That Help

Need Help Reviewing Your Account?

Contact UsTrying to recover unpaid personal loan balances can feel confusing, especially when notices arrive, and you are unsure what they mean for your finances. Many people in the United States face this moment and wonder what happens next.

You might be asking yourself simple but important questions. Can a past-due loan lead to wage garnishment? Are there debt repayment plans that fit your current income? Is it still possible to recover unpaid personal loan obligations without making your financial situation harder?

Feeling overwhelmed in this situation is common. When bills pile up and information feels unclear, it can be difficult to know where to begin. Clear guidance and practical information can help you review your options and take the next step with greater confidence.

Key Takeaways

- Personal loans often become unpaid due to financial strain, missed payment dates, unexpected expenses, or long-term income changes that make regular repayments difficult.

- Unpaid loans usually move through stages such as reminders, written notices, repayment discussions, and, in rare cases, legal review if the balance remains unresolved.

- Early communication, reviewing account notices, discussing repayment arrangements, and responding to legal documents are practical actions that help manage and recover unpaid personal loan obligations.

- U.S. laws limit harassment, restrict contact hours, protect wage income through garnishment caps, and allow disputes if debt information appears incorrect on credit reports.

- Installment plans, settlement agreements, adjusted payment timelines, and mediated discussions can help borrowers gradually resolve past-due accounts without overwhelming financial pressure.

What Does Recover Unpaid Personal Loan Mean?

Recover unpaid personal loan refers to the process of resolving a past-due loan balance by reviewing the account, confirming payment details, and arranging repayment through manageable payment plans or settlement options.

The goal is to address the unpaid balance responsibly while protecting your rights and financial stability.

Why Personal Loans Sometimes Go Unpaid?

Financial pressure can make loan payments difficult to keep up with. When life circumstances shift, even well-planned budgets can change. Knowing the common reasons payments stop can help you approach the situation calmly and take the first step toward resolving the balance.

Situations that often lead borrowers to miss or stop payments include the following:

- Missed Payment Dates: Busy schedules or multiple bills can lead to overlooked due dates, especially when reminders or automatic payments are not set.

- Unexpected Financial Strain: Medical expenses, job interruptions, or sudden household costs can reduce the funds available for scheduled loan payments.

- Avoidance Due To Stress: When financial pressure builds, some people delay responding to account notices because the situation feels overwhelming.

- Bankruptcy Filing: Serious financial distress may lead some individuals to pursue bankruptcy, which temporarily pauses most collection actions.

- Inability To Meet Obligations: At times, income changes or long-term hardship make repayment difficult until a structured plan or support option is arranged.

Recognizing the reasons behind missed payments can make the situation easier to address. Once the cause is identified, practical steps toward resolving the account become easier to take.

Discover practical strategies that can help improve lending outcomes and long-term growth in Accelerate Your Lending: Strategic Steps to Boost Loan Portfolio Growth.

What Happens When a Personal Loan Becomes Past Due?

When a payment deadline passes without a completed installment, the account typically enters a structured follow-up process.

The purpose of this stage is to clarify the balance, maintain proper records, and give you time to review the situation before it progresses further.

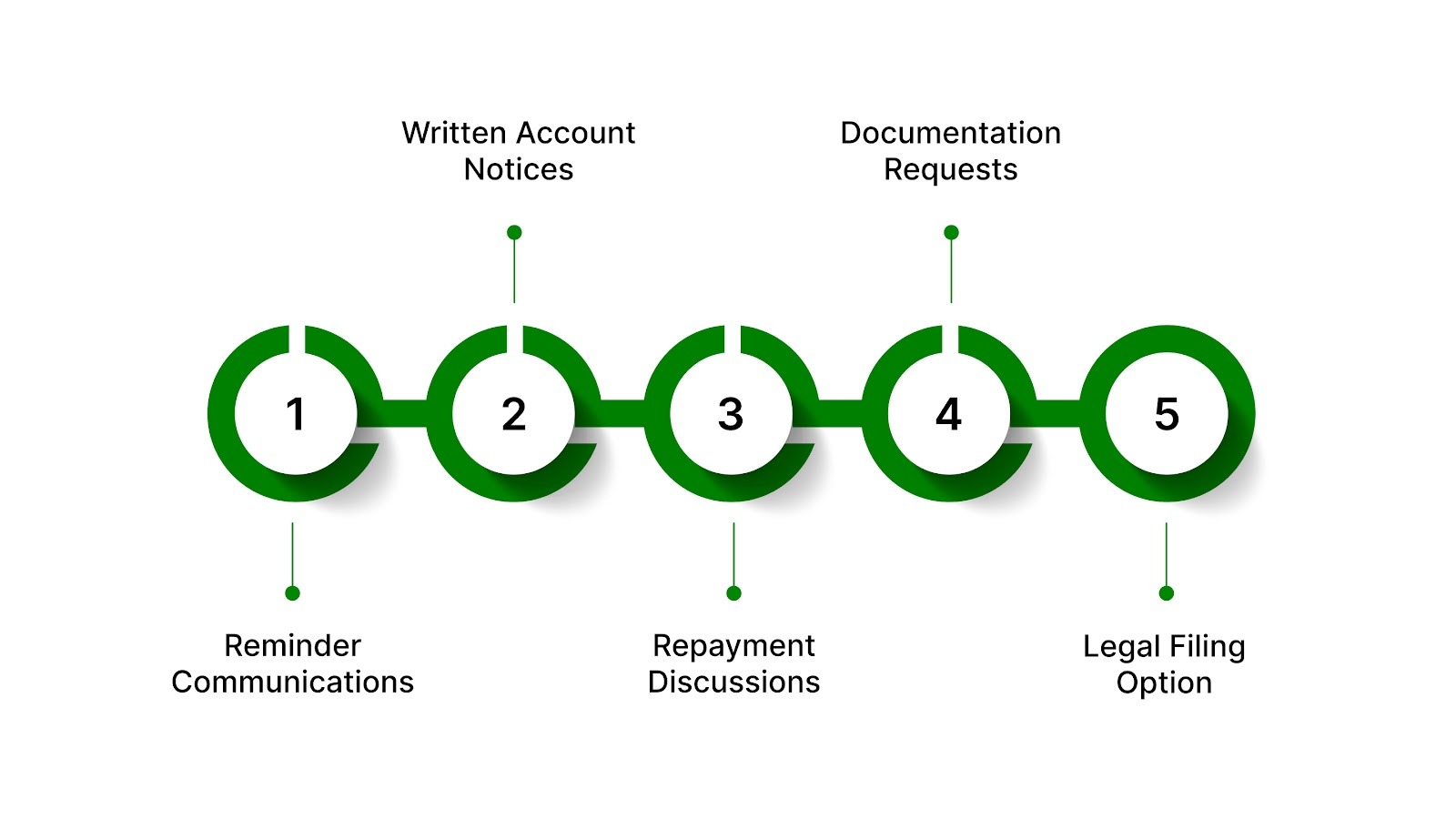

Developments that often occur as an account becomes past due include the following:

- Reminder Communications: You may receive polite reminders through calls, emails, or letters confirming the overdue amount and encouraging a response.

- Written Account Notices: Formal notices can outline payment details, the original obligation, and the timeline connected to the overdue balance.

- Opportunity for Repayment Discussions: Financial hardship can lead to conversations around modified repayment timelines or revised arrangements to resolve the balance.

- Formal Documentation Requests: Clear records, such as written agreements or communication history, may be referenced to confirm the account details.

- Legal Filing As A Final Option: When earlier communication attempts remain unresolved, a court filing may occur to formally review the repayment obligation.

Seeing how the process unfolds can reduce uncertainty and help you respond with confidence. Clear communication and verified account information create a path toward resolving the balance in a manageable way.

If you want to understand how financial distress affects loan accounts and what steps can help resolve them, read Distressed Loan Meaning, Causes, and How You Can Recover.

Practical Steps to Recover From an Unpaid Personal Loan

Taking action after a missed loan payment can feel overwhelming. A structured approach can help you respond calmly and move toward resolving the balance responsibly.

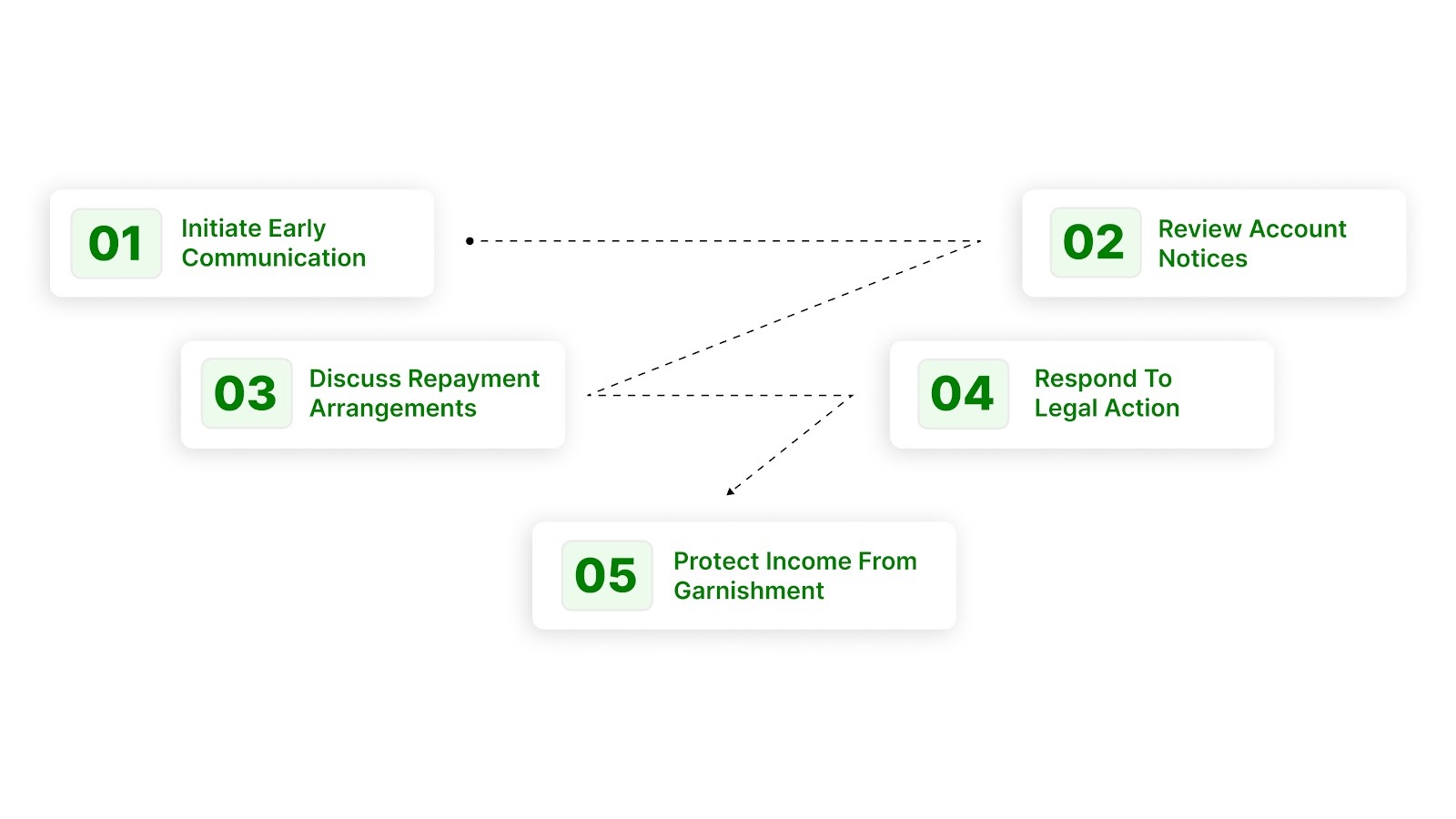

1. Initiate Communication Early

Opening a conversation quickly can prevent confusion and give you space to discuss the situation. Early communication often helps identify workable solutions before stress escalates further.

Actions that help start a constructive conversation include:

- Contact Support Promptly: Reach out by phone, email, or secure portal message to explain your situation and ask about available ways to address the past-due balance.

- Explain Your Circumstances Clearly: Share relevant details about your financial situation so the support team understands what you are facing and can guide the discussion constructively.

- Ask About Next Steps: Request clear guidance on how the account can move forward, including timelines, payment options, and how to keep the situation manageable.

How To Do It: Use the official contact information or secure portal listed in your account notice. Provide your account reference and briefly explain your circumstances.

2. Review and Respond to Account Notices

Account notices provide important details about the past-due balance. Taking time to review the information carefully helps you understand the situation before deciding how to respond.

Actions that help you review account notices carefully include:

- Check the Amount Listed: Compare the balance mentioned in the notice with your records so you understand the full amount associated with the account.

- Note the Response Timeline: Pay attention to the deadline mentioned in the notice so you know how much time you have to respond.

- Confirm Payment Instructions: Look for the official payment method listed in the notice to make sure you use a safe and accurate process.

How To Do It: Read the notice carefully and keep it for reference. If something appears unclear, contact the support team to ask questions and request clarification.

3. Discuss a Possible Repayment Arrangement

If paying the full balance immediately is difficult, discussing adjusted repayment terms can create a more manageable path forward.

Actions that help guide repayment discussions include:

- Request Flexible Payment Timing: Ask whether repayment schedules can be adjusted to match your current financial situation and income flow.

- Discuss Partial Payments: Explore whether smaller payments over time could help reduce the balance gradually.

- Clarify Updated Terms: Confirm that you understand any new repayment arrangement before agreeing, so expectations remain clear.

How To Do It: Contact the support team and explain what payment level you can reasonably manage. Request written confirmation of any revised arrangement.

4. Respond If Legal Action Begins

In rare situations, unresolved accounts may move into a court process. Participating calmly and responding properly helps protect your rights.

Actions that support responsible participation include:

- Attend Scheduled Hearings: If you receive a court notice, make sure you appear on the scheduled date to present your side.

- Review Agreement Details: Check whether written agreements or records clearly describe the original terms connected to the account.

- Check Applicable Time Limits: Laws in each state set time limits for filing certain claims, which may affect how cases proceed.

How To Do It: Read any legal documents carefully and seek guidance if something is unclear. Respond within the stated deadlines and keep copies of all documents.

5. Protect Your Rights If Income Is Garnished

If a court judgment leads to wage garnishment, federal and state protections help ensure a portion of your income remains available for living expenses.

Actions that help protect your income include:

- Review the Garnishment Notice: Check the document carefully to understand the amount requested and the response timeline.

- Request Applicable Exemptions: Courts may allow certain income protections depending on your financial situation and state rules.

- Respond Within The Deadline: Acting within the allowed response window helps preserve your ability to request adjustments.

How To Do It: Follow the instructions in the garnishment notice and contact the court if you need to request exemptions or clarify your rights.

Resolving a past-due personal loan often begins with calm communication and informed decisions. Taking steady steps forward helps you move toward financial clarity and greater peace of mind.

If you want guidance on managing complex debt situations and exploring professional support options, read Best Finance Advisory Service Providers for Debt Management.

How Do Lenders Recover Unpaid Personal Loans?

When a personal loan remains unpaid for an extended period, a structured recovery process may begin. The goal is to clarify the balance, document communication, and provide opportunities for resolution while protecting consumer rights.

Stages commonly involved in addressing unresolved personal loan balances include the following:

- Reminder Communications: Account reminders may begin with respectful calls or written notices that confirm the outstanding balance and encourage you to review the account.

- Formal Payment Request: A written request may outline the loan origin, balance details, and a response timeline, helping you understand what action may be needed next.

- Repayment Discussions: If financial hardship is involved, conversations may focus on adjusting the original terms or creating a new repayment schedule that reflects your circumstances.

- Court Review: When earlier communication does not lead to resolution, the matter may move to a court process where both sides present documentation related to the loan agreement.

- Post-Judgment Collection: If a court confirms the obligation, methods such as income garnishment or property claims may be used under limits established by federal and state law.

Seeing how recovery typically progresses can reduce uncertainty. Clear information helps you respond confidently and focus on practical steps that move the account toward resolution.

Your Rights When Resolving a Past-Due Loan

Resolving a past-due loan can feel stressful, especially when you are unsure what protections apply. U.S. consumer protection laws exist to help guarantee communication stays fair, transparent, and respectful while you review your options.

Legal protections that support consumers during the resolution process include the following:

Knowing these protections can help you approach the situation with greater confidence. Clear information and respectful communication support a path toward resolving the account responsibly.

Learn what happens when a loan portfolio is acquired and how it can affect your account in Is Loan Portfolio Acquisition a Loan Transfer for Your Account?

Payment Plan Options That Can Help You Move Forward

When a past-due balance feels difficult to manage, flexible repayment arrangements can create a practical way forward. Structured options focus on manageable payments, clearer timelines, and steady progress toward resolving the account.

Common repayment arrangements that can help you regain financial control include the following:

- Debt Settlement Agreement: A revised agreement may allow the total balance or repayment timeline to change so the account becomes easier to resolve during financial hardship.

- Structured Installment Plan: Smaller payments made on a consistent schedule can help you address the balance gradually without the pressure of a single large payment.

- Flexible Payment Timing: Repayment frequency may be adjusted to better match your income cycle, helping you maintain consistency without disrupting essential expenses.

- Good Faith Payment Start: Beginning with a smaller initial payment can demonstrate your commitment to resolving the balance while a longer-term plan is arranged.

- Mediated Repayment Discussion: A neutral third party may help guide a constructive conversation when direct discussions have stalled, supporting an agreement both sides can accept.

Exploring repayment arrangements can reduce financial pressure while keeping progress steady. With the right plan in place, you can focus on rebuilding stability one step at a time.

Moving Toward a Clear Financial Path

Dealing with a past-due personal loan can feel isolating, but taking the time to understand your options can make the situation far more manageable. When you have accurate information and a clear place to start, resolving an unpaid balance becomes a step-by-step process rather than an overwhelming problem.

Reviewing account details, payment history, and available repayment arrangements can help bring structure to the situation. In some cases, accounts may be managed by organizations such as The Forest Hill Management, where records and communication are maintained so consumers can review account information and understand the status of the balance.

Having access to clear documentation and accurate account details can make it easier to evaluate the situation and determine how to proceed. Contact our advisors for personalized support

FAQs

1. Can you recover unpaid personal loan balances after a long period of missed payments?

Yes, it is often still possible to recover unpaid personal loan balances even after several missed payments. The key step is reviewing the account details and discussing repayment options that fit your current financial situation.

2. What is the first step in learning how to recover unpaid personal loans?

The first step in understanding how to recover unpaid personal loans is checking the account balance and payment history. This helps you see where the account stands before choosing a repayment option.

3. Can setting up a payment plan help recover unpaid personal loan accounts?

Yes. Structured repayment plans can help you gradually recover unpaid personal loan balances. Smaller scheduled payments often make the process more manageable while reducing financial pressure.

4. Is it possible to recover unpaid personal loan balances without paying everything at once?

In many cases, yes. Payment arrangements may allow you to repay the balance over time rather than through one large payment, depending on your financial circumstances.

5. How long does it usually take to recover unpaid personal loans?

The timeline to recover unpaid personal loans varies based on the balance, repayment arrangement, and payment consistency. Regular payments often help resolve accounts faster and with less financial stress.