How to Collect Money Owed to You Steps

Need Help Reviewing Your Account?

Contact UsLending money to someone you trust often feels like the right thing to do. It might be a friend who needs help covering rent or a family member dealing with an unexpected expense. But when repayment doesn’t happen, the situation can quickly become uncomfortable.

And it’s more common than many people realize. Surveys show that over 77% of people have lent money to friends or family, and about 32% say they didn’t get repaid the last time they did. When personal loans happen without clear agreements, misunderstandings about repayment timelines are easy to create.

The good news is that there are practical steps you can take to address the situation calmly and improve your chances of recovering the money.

In this blog, we’ll explain how to collect money from someone who owes you, including the steps you can take to request repayment, document the debt, and pursue more formal solutions if needed.

Key Takeaways

- Personal loans often become difficult to recover because they are informal. Without written agreements or clear timelines, repayment expectations can easily become unclear.

- Start with a calm and respectful conversation. Many repayment issues can be resolved once both sides discuss the loan and agree on next steps.

- Follow a step-by-step approach if repayment is delayed. Written requests, repayment plans, demand letters, mediation, and small claims court can help move the process forward.

- Keep clear records of the loan and all communication. Documentation can support your claim if the situation later requires legal action.

- Professional help can simplify the recovery process. Services like The Forest Hill Management can assist with structured communication and repayment solutions.

Why Recovering Personal Loans Can Be Difficult?

Lending money to a friend, family member, roommate, or acquaintance often starts with good intentions. In many cases, the agreement is informal.

The problem arises when repayment does not happen as expected. Weeks or months may pass, and the conversation about money becomes uncomfortable. You may wonder whether the person intends to repay the money, whether you should ask again, or what your options are if the situation continues.

There are several factors that can make recovering personal loans challenging:

- Informal agreements between friends or family: Personal loans often rely on trust rather than written agreements. While this can feel natural at the time, it can later create uncertainty about repayment terms or expectations.

- Lack of written documentation: When there is no written record of the loan, it may be harder to confirm the exact amount owed, the repayment timeline, or whether the money was intended as a loan rather than a gift.

- Borrower financial hardship: Sometimes repayment delays happen because the borrower is facing financial challenges such as job loss, unexpected expenses, or other debt obligations.

- Emotional discomfort around money conversations: Asking someone to repay money can feel awkward, especially when personal relationships are involved. This discomfort often causes people to delay the conversation longer than they should.

- Miscommunication about repayment timelines: One person may believe repayment will happen quickly, while the other assumes there is no urgency. Without clear expectations, these misunderstandings can grow over time.

Understanding these dynamics is important before taking action. When you approach the situation calmly and with a clear plan, it becomes easier to move the conversation toward repayment rather than conflict.

Now that we’ve clarified why these situations happen, let’s walk through the practical steps you can take to recover money that someone owes you.

First Steps to Take Before Escalating the Situation

Before considering legal action or formal recovery methods, it is usually best to take a few practical steps to resolve the situation directly. Many personal loan disputes happen because expectations were never clearly discussed or documented.

Taking the following steps can help clarify the situation and move the conversation toward a solution:

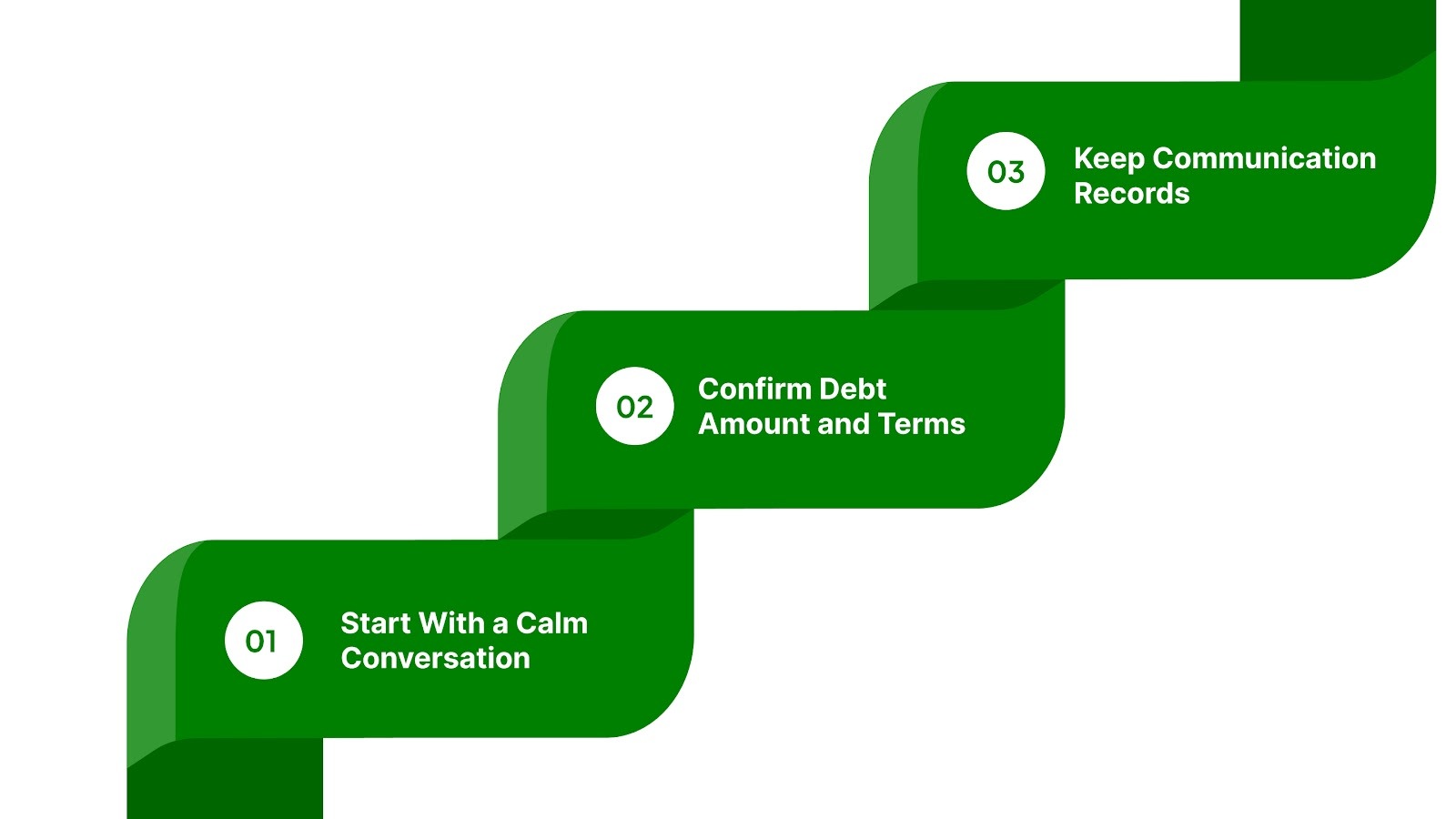

Start With a Calm Conversation

When someone owes you money, it can be tempting to jump straight into frustration or demands. However, respectful communication is often the most effective starting point. Many repayment issues arise because the borrower assumed the timeline was flexible or because their financial situation changed unexpectedly.

Beginning the conversation calmly creates space for an honest discussion about what happened and how the situation can be resolved.

- Explain the situation clearly: Remind the person about the loan and the amount involved without sounding accusatory. A simple statement keeps the conversation constructive.

- Ask about their current situation and repayment plans: The borrower may be experiencing financial difficulties that delayed repayment. Asking about their ability to repay can help you understand whether the delay was intentional or circumstantial.

- Set expectations moving forward: If repayment has been delayed, discuss what a realistic timeline might look like. Agreeing on a specific date or installment plan can help both sides move forward with clarity.

Also read: How Installment Loans Work and Their Key Features

Experts often recommend starting with open communication because many disputes can be resolved once both parties understand each other’s expectations.

Confirm the Amount and Terms of the Debt

Before pushing further, it is important to make sure both parties are working with the same understanding of the loan. When personal loans are informal, details such as the repayment timeline or total amount owed can become unclear over time.

Taking a moment to confirm these details helps avoid confusion and ensures that both sides are discussing the same agreement.

- Identify exactly how much money was loaned: Review the original transaction or conversation to confirm the amount. This may involve checking bank transfers, payment app records, or previous messages discussing the loan.

- Clarify what the original repayment expectations were: Some loans were meant to be repaid by a specific date, while others may have been open-ended. Confirming this helps prevent misunderstandings about whether the repayment is overdue.

- Review any agreements that may have been discussed earlier: Even informal agreements through text messages or emails can help clarify what both parties initially agreed upon.

Confirming these details helps ensure that the discussion remains focused on facts rather than assumptions.

Keep Records of Your Communication

Even when the situation begins with a simple conversation, it is helpful to document important details moving forward. Clear records protect both parties and make future discussions easier to manage.

Documentation also becomes important if the situation eventually requires mediation or legal action.

- Save messages or emails related to the loan: Written communication showing that money was borrowed and discussed as a loan can help establish that the funds were not intended as a gift.

- Keep proof of the original payment: Bank transfers, digital payment receipts, or transaction records can confirm the exact amount and date the money was provided.

- Document repayment discussions and agreements: If the borrower agrees to a repayment schedule, write it down and confirm it through email or message so both sides have a clear reference.

Keeping organized records can make it much easier to resolve repayment issues if the situation becomes more complicated later.

These initial steps often resolve repayment issues without needing to escalate the situation further.

Practical Steps to Collect Money From Someone Who Owes You

If a calm conversation and clarification haven’t led to repayment, the next step is to move forward with a more structured approach. Collecting money from someone who owes you often works best when you escalate gradually, starting with clear written communication and only moving to legal options if necessary.

Many people looking for how to collect money from someone who owes you assume they must immediately involve lawyers or courts. In reality, most repayment issues can be resolved through a few organized steps that establish clear expectations and create accountability.

The steps below outline a practical process you can follow, beginning with a formal written request and progressing toward mediation or small-claims court if repayment still does not occur.

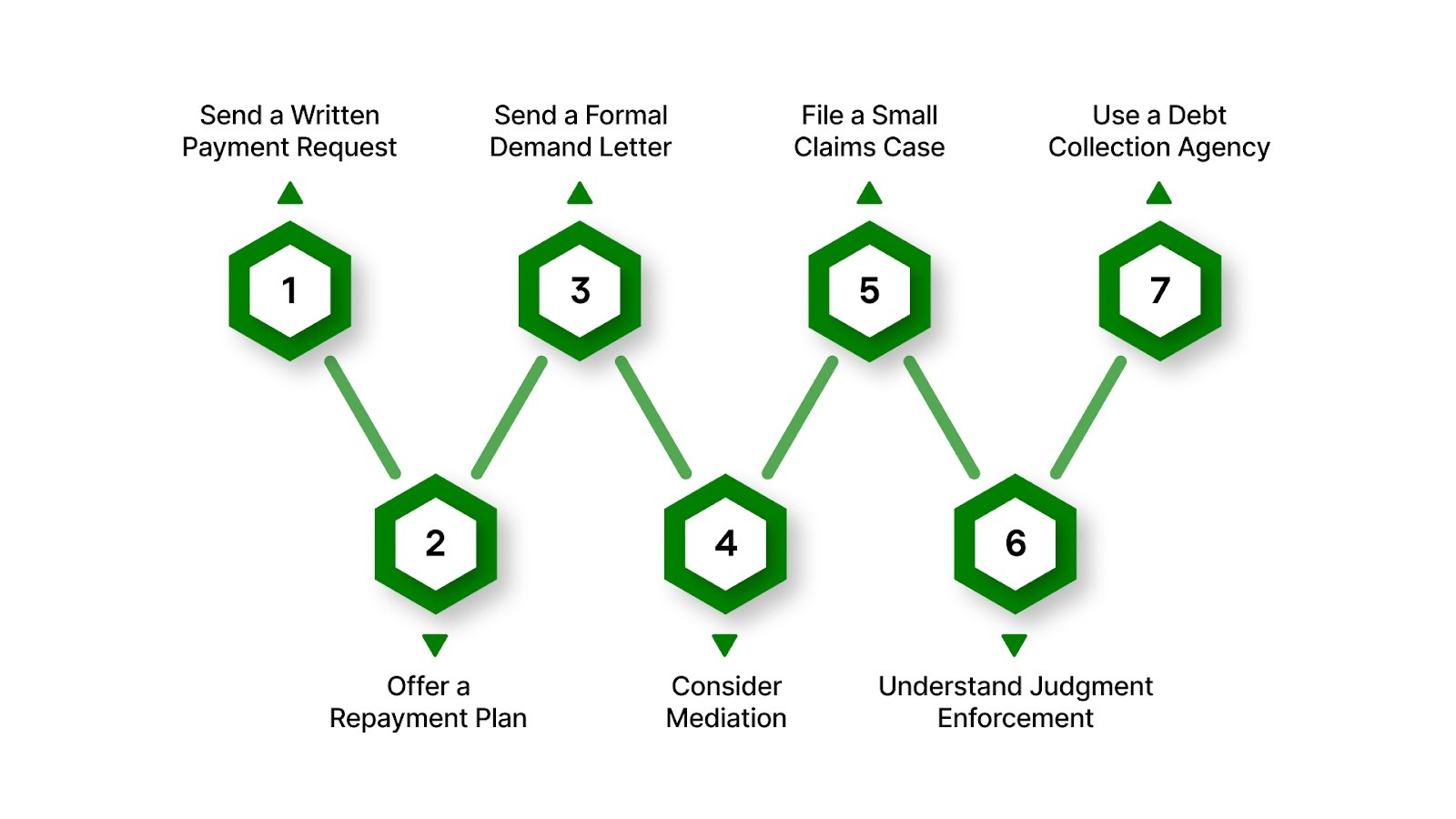

Step 1: Send a Clear Written Payment Request

If verbal reminders have not worked, sending a written payment request is often the first effective step. A written message clarifies the amount owed, sets a repayment expectation, and shows that you are taking the situation seriously.

Include the following details in your request:

- State the amount owed and when the loan occurred: Clearly mention the amount of money that was loaned and reference the date it was provided so there is no confusion about the debt.

- Provide a specific repayment deadline: Setting a clear deadline, often 7–14 days from the date of the message, encourages action and prevents the conversation from being delayed indefinitely.

- List the available payment methods: Make repayment easier by providing simple options such as bank transfer, digital payment platforms, or another agreed method.

- Invite the borrower to discuss repayment if they cannot pay: For example, you might include a sentence such as: “If you cannot repay the full amount right now, please contact me within the next week so we can discuss a repayment plan.”

How to send the request:

Send the message by email or written message first, and if possible follow up with a trackable delivery method such as certified mail or a payment-platform message. Keeping the tone factual and non-threatening is important, as courts generally respond better to calm, documented communication.

Step 2: Offer a Realistic Repayment Plan

Sometimes repayment delays occur because the borrower cannot afford to repay the entire amount at once. Offering a reasonable repayment plan can make it easier for the borrower to meet their obligation while still allowing you to recover the money.

Possible repayment arrangements may include:

- Monthly installment payments: Dividing the balance into smaller monthly payments with clear due dates can make repayment manageable while ensuring steady progress.

- Short-term repayment schedules: Agreeing on a defined timeline, such as three to six months of scheduled payments, helps both parties track progress.

- Partial settlement agreements: In some situations, accepting a slightly reduced lump-sum payment may allow you to resolve the situation quickly.

If a repayment arrangement is agreed upon, confirm the details in writing. Even a short email summarizing the payment schedule and total amount owed can help prevent misunderstandings later.

Step 3: Send a Formal Demand Letter

If repayment still does not occur after written reminders or repayment discussions, the next step is often a formal demand letter. This type of letter signals that you are preparing to take further action if the debt remains unpaid.

Demand letters are commonly used as a final step before legal action and are often expected by courts as proof that you attempted to resolve the dispute.

A formal demand letter should include:

- The exact amount owed and the original loan date: Clearly restate the loan details and the balance that remains unpaid.

- A brief summary of previous repayment attempts: Mention earlier messages or conversations requesting repayment.

- A firm repayment deadline: Many demand letters provide a final deadline of about 10–14 days.

- A clear statement about potential legal action: For example: “If payment is not received by [date], I may consider filing a claim to recover the amount owed and any applicable costs.”

Attach copies of any relevant documentation, such as payment receipts or previous communication, but keep the originals for your records.

How to deliver a demand letter:

Send the letter through a trackable method such as certified mail or a tracked courier service. Keeping proof of delivery is important in case the dispute later moves to court.

Step 4: Consider Mediation or Neutral Dispute Resolution

Before pursuing court action, mediation may offer a faster and less expensive way to resolve the issue. Many local courts and community programs provide mediation services designed to help individuals resolve financial disputes.

During mediation:

- A neutral third party helps both sides discuss the situation.

- The mediator does not make decisions but helps facilitate an agreement.

- If a settlement is reached, the agreement is documented in writing.

Mediation can be especially helpful when the loan involves friends, relatives, or colleagues, since it focuses on finding a workable solution without escalating conflict.

Step 5: File a Claim in Small Claims Court

If repayment attempts and mediation fail, filing a claim in small claims court may be the next option. Small claims courts are designed to resolve disputes involving relatively smaller financial amounts without the complexity of higher courts.

You may consider filing a claim if:

- The borrower has ignored demand letters or repayment requests.

- The amount owed falls within your state’s small-claims limit.

- You have evidence showing that the money was loaned and remains unpaid.

When preparing for small claims court, gather clear documentation such as:

- Bank transfer or payment records showing the loan

- Messages or emails confirming the loan agreement

- Copies of written repayment requests or demand letters

- Any written repayment agreements

Courts generally expect organized, chronological evidence that clearly demonstrates the existence of the loan and the attempts made to recover it.

Filing fees vary by location but are typically lower than those required for full civil court cases.

Step 6: Understand How Court Judgments Are Enforced

Winning a case in small claims court does not always mean immediate payment. If the borrower still refuses to repay after a judgment is issued, additional enforcement options may be available depending on local laws.

Common enforcement methods may include:

- Wage garnishment: A portion of the borrower’s wages may be directed toward repaying the debt through a court-ordered process.

- Bank account levies: Courts may allow funds to be withdrawn from certain bank accounts to satisfy the judgment.

- Property liens: In some cases, a legal claim may be placed on property owned by the borrower until the debt is repaid.

Before pursuing enforcement measures, it is often helpful to confirm whether the borrower has assets or income that could realistically satisfy the judgment. Enforcement actions can involve additional time and costs, so understanding the borrower’s financial situation may help determine whether further steps are worthwhile.

Step 7: Consider Working With a Debt Collection Agency

If repeated attempts to recover the money have not worked and you prefer not to pursue legal action yourself, another option is to contact a debt collection agency.

These agencies specialize in helping individuals and businesses recover unpaid debts through structured communication and formal collection processes.

When considering a debt collection agency, keep the following points in mind:

- Agencies communicate directly with the borrower: The collection agency contacts the person who owes the money and works to establish repayment through calls, letters, or payment arrangements.

- Fees are usually charged as a percentage of the recovered amount: Many agencies operate on a contingency basis, meaning they receive a portion of the amount collected rather than charging upfront fees.

- Collection agencies must follow consumer protection laws: In the United States, debt collectors must follow regulations such as the Fair Debt Collection Practices Act (FDCPA), which limits harassment, deceptive practices, and improper communication.

- Documentation will still be required: Agencies typically ask for proof that the money was loaned, including payment records or written communication confirming the debt.

Also read: Debt Collection Oversight: Consumer Advice and Management

Working with a collection agency can sometimes resolve the issue without the time and effort involved in filing a court case, especially when the borrower responds more seriously to formal collection attempts.

Conclusion

Recovering money from someone you know can feel difficult, especially when personal relationships are involved. But approaching the situation with clear communication, proper documentation, and a structured plan can make the process far more manageable.

By taking steady steps and understanding your options, you can work toward resolving the debt in a fair and organized way.

If you’re dealing with unpaid debts and need help moving the situation toward resolution, The Forest Hill Management provides structured account support, secure payment options, and clear communication designed to help individuals resolve outstanding obligations responsibly.

FAQs

1. Can you charge interest when someone repays a personal loan?

In many cases, interest can only be charged if it was clearly agreed upon when the loan was made. Without a written agreement specifying interest, courts often treat the loan as interest-free.

2. What should you do if the borrower stops responding completely?

If the person stops communicating, it may be helpful to switch to written communication such as email or certified mail. This creates a record showing that you attempted to resolve the issue before considering legal options.

3. Is there a time limit to recover money someone owes you?

Yes. Most states have statutes of limitations that limit how long you can legally pursue repayment through the courts. The time period varies by state and the type of debt.

4. Can a verbal agreement be used as proof in a debt dispute?

Yes, verbal agreements can sometimes be considered valid, but they are harder to prove. Supporting evidence such as bank transfers, messages, or witnesses may help demonstrate that the money was intended as a loan.

5. What if the borrower claims the money was a gift?

This is a common dispute in personal lending situations. Documentation such as text messages, repayment discussions, or written agreements can help demonstrate that the money was loaned rather than gifted.