How to Get Medical Debt Forgiven: A Step-by-Step Guide

Transform Your Financial Future

Contact UsMedical debt is one of the leading causes of financial hardship for individuals and families in the U.S. Did you know that Americans owe at least $220 billion in medical debt? Whether caused by emergency treatment, outpatient procedures, or chronic illness, medical debt can put immense stress on individuals, impacting both financial stability and mental well-being.

Fortunately, there are several paths available to help reduce or eliminate medical debt. From government programs and nonprofit debt relief organizations to direct negotiation strategies, there are numerous resources at your disposal to alleviate the burden of medical bills.

In this guide, we will explore ways to have your medical debt forgiven or significantly reduced, offering practical steps to help you regain control of your financial health.

Key Takeaways

- Medical debt relief comes through multiple paths, like hospital charity care, nonprofits, state programs, and direct negotiation, not a single universal solution.

- Hospital financial assistance (charity care) can significantly reduce or fully eliminate bills, but eligibility depends on income, family size, and timely application.

- Nonprofits and state programs can forgive debt by purchasing it at a lower cost, mainly supporting low-income individuals with high unpaid balances.

- Government programs like Medicaid, Medicare, and CHIP help reduce medical costs and prevent future debt, but they are not direct means of forgiveness.

- Even without forgiveness, negotiating bills, checking errors, and setting payment plans can lower the amount owed and make repayment manageable

What is Medical Debt Forgiveness?

Medical debt forgiveness refers to the process of having part or all of your medical debt eliminated through government programs, nonprofit organizations, or direct negotiations with your healthcare provider.

Distinction Between Forgiveness, Reduction, and Repayment Plans

- Debt Forgiveness: When the total amount owed is completely wiped away. This is typically offered by charitable organizations or through state-funded programs.

- Debt Reduction: This involves lowering the amount owed, usually through negotiations or settlements, and is often achieved with the help of nonprofits or financial institutions.

- Repayment Plans: These are structured plans that allow you to repay the debt in installments over time. Although this doesn't eliminate the debt, it makes the repayment process more manageable.

Despite the absence of a single federal program for universal medical debt forgiveness, many people can still find relief through various mechanisms. Understanding these options and taking proactive steps can lead to significant debt reduction or complete forgiveness.

Hospital Financial Assistance and Charity Care

Many nonprofit hospitals offer financial assistance programs, commonly known as charity care, to help patients manage medical bills they cannot afford. These programs can reduce or fully eliminate outstanding balances for eligible individuals.

Rather than being broadly mandated under the Affordable Care Act, tax-exempt hospital organizations are required under Internal Revenue Code Section 501(r)(4) to establish and maintain a written Financial Assistance Policy (FAP). This policy outlines who qualifies for assistance, how to apply, and what types of support are available.

How Charity Care Programs Work?

Hospitals that provide financial assistance typically base eligibility on factors such as household income, family size, and financial hardship. Each hospital defines its own criteria within its Financial Assistance Policy, so eligibility thresholds and coverage levels can vary.

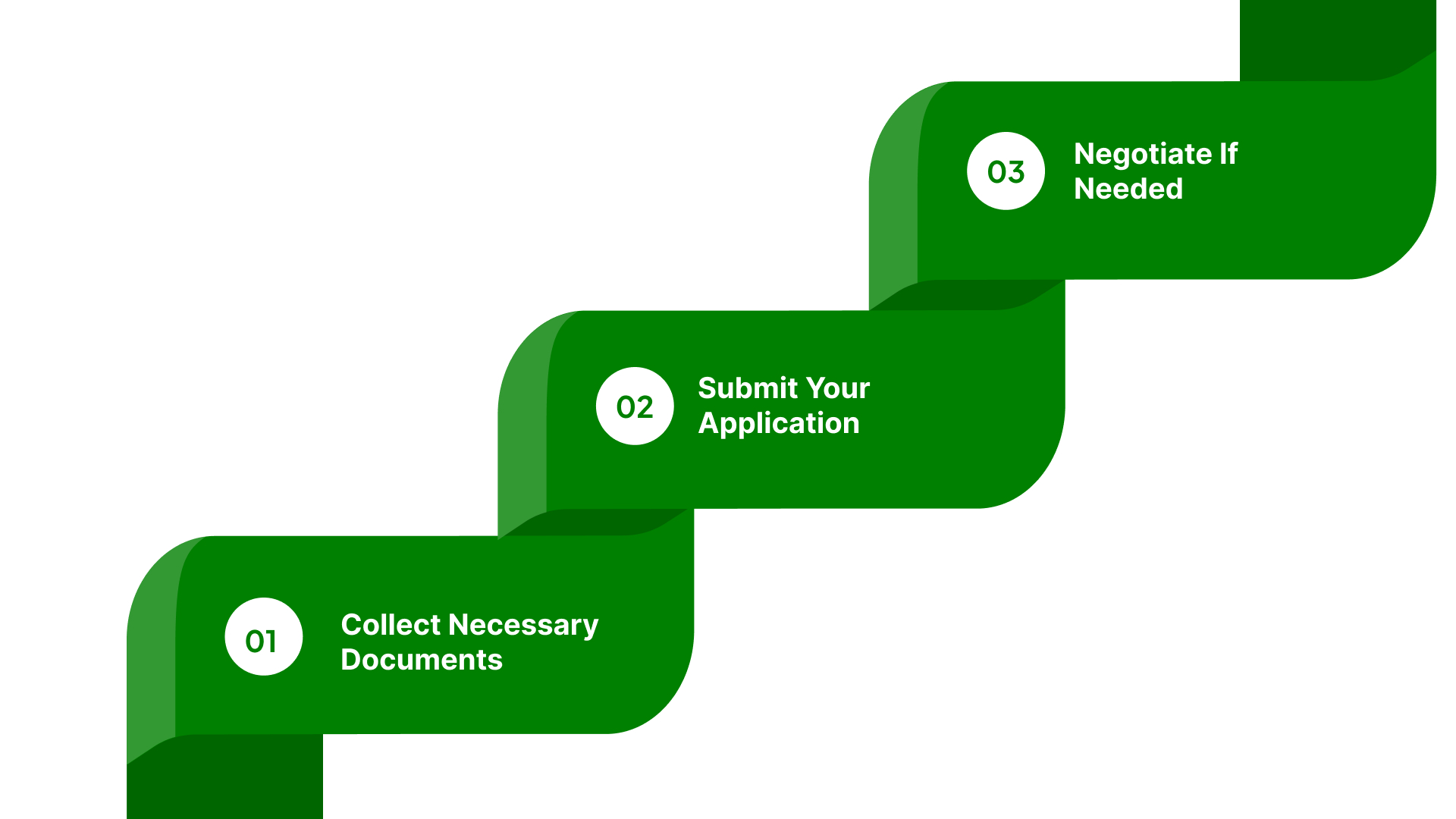

Let’s look at the typical steps involved in applying for hospital financial assistance:

- Collect Necessary Documents

Hospitals usually require proof of income, tax returns, and other financial records to assess eligibility. Having these ready can speed up the process. - Submit Your Application

Complete the hospital’s financial assistance application and submit all required documents. It is important to follow up to ensure your application is being reviewed. - Negotiate If Needed

If you do not qualify for full assistance, you may still be able to request a reduced balance or set up a manageable payment plan. Many hospitals are open to offering flexible arrangements.

Applying as early as possible after receiving medical care is critical. Delays can lead to additional charges or collection activity, making the situation more difficult to manage over time.

Nonprofit and Charitable Medical Debt Forgiveness Organizations

Several nonprofits focus specifically on helping individuals with medical debt by purchasing it at a discounted rate and forgiving it. These organizations aim to alleviate the burden for people who cannot pay their medical bills due to financial hardship.

Let's look at this in detail.

- Undue Medical Debt: This nonprofit buys medical debt from healthcare providers at a fraction of the cost and then forgives it for individuals who qualify. The organization focuses on low-income individuals who cannot pay off their medical debt. Undue Medical Debt has helped thousands of people by forgiving millions of dollars in medical debt each year.

How These Organizations Determine Eligibility?

Eligibility for medical debt forgiveness programs is typically based on:

- Income level: Many organizations prioritize those who earn below a certain income threshold.

- Total medical debt: The amount of debt owed can influence eligibility.

- Geographic location: Some programs are available only in specific areas or for residents of certain cities or states.

Nonprofit debt forgiveness is an excellent option for those struggling with medical bills who meet the qualifications for assistance.

If you're looking for expert insights and practical advice tailored to your specific needs, explore our comprehensive guide on Effective Debt Resolution Strategies.

Government and State Medical Debt Relief Programs

In addition to private organizations, there are state-specific medical debt relief programs that help residents reduce or eliminate medical debt. These programs are often implemented in partnership with nonprofit organizations and can be a significant resource for those in need.

Examples of State-Specific Programs:

- Rhode Island’s Medical Debt Relief Program: Rhode Island partners with Undue Medical Debt to offer medical debt relief to residents. The program helps eliminate medical debt for those who qualify, and it is one of the first state-level programs to provide this type of assistance.

- Illinois Medical Debt Relief Pilot Program: This state initiative aims to reduce the burden of medical debt for Illinois residents, particularly those who are struggling financially. The program works with nonprofit organizations to help people pay off their medical debt in a manageable way.

- New York City’s Medical Debt Relief Program: NYC has created a program that forgives medical debt for eligible residents. This program targets individuals in financial distress and helps them eliminate their medical bills, offering a crucial lifeline to those in need.

These state programs offer debt relief to residents based on factors like income, residency, and total medical debt. Each program has different eligibility requirements, so it's important to contact the relevant state office to find out about available options in your area.

Negotiation Strategies and Appeals

Even if you do not qualify for medical debt forgiveness programs, negotiating directly with your medical providers or debt collectors can significantly reduce your debt or make it more manageable.

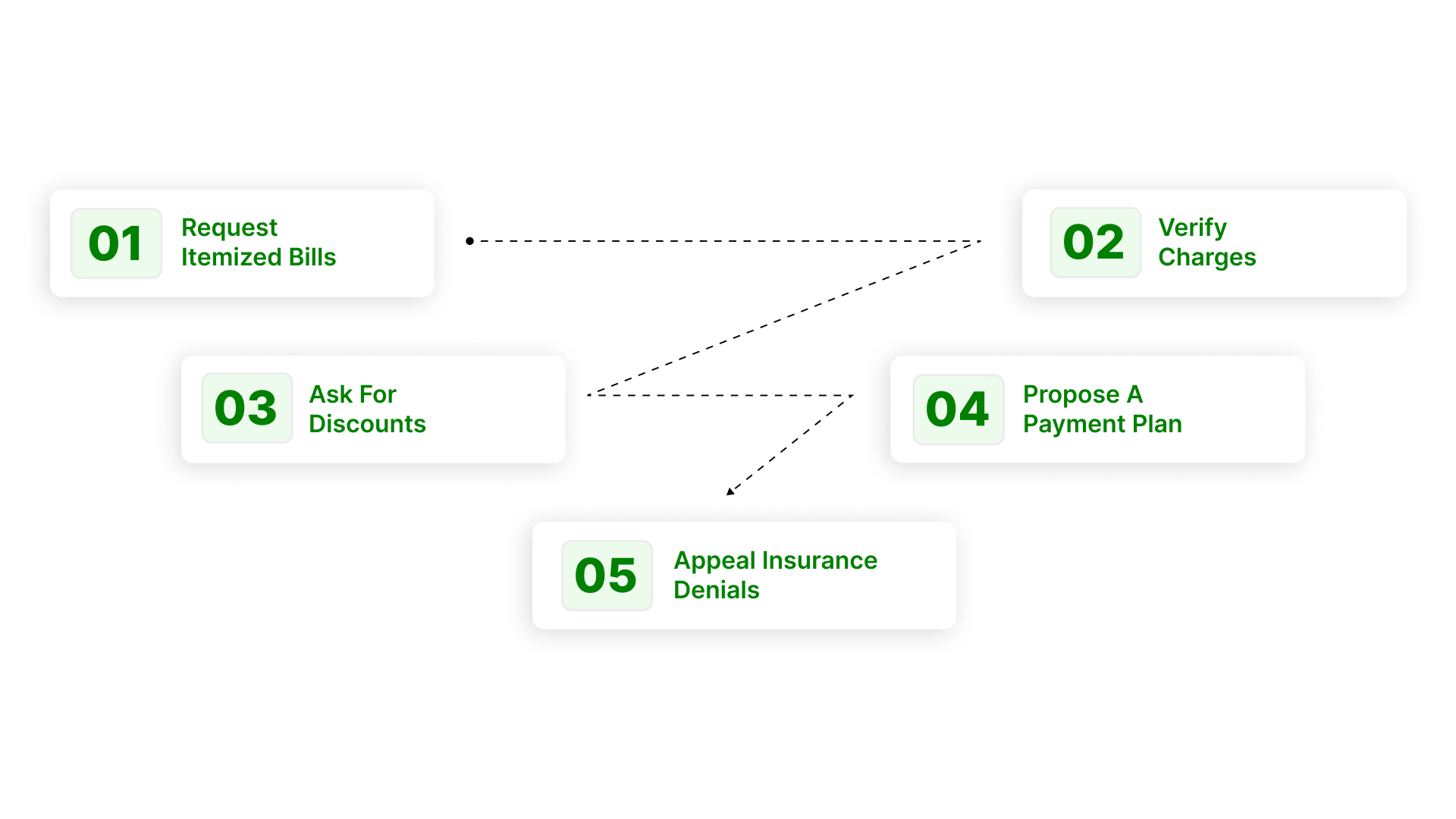

Let's look at some negotiation tips.

- Request Itemized Bills: Before entering into any negotiations, request an itemized bill to ensure there are no errors or discrepancies. Many people find that their bills contain overcharges or services they didn’t receive.

- Verify Charges: Double-check the charges on your bill to ensure they are accurate. If there are any discrepancies, dispute them immediately.

- Ask for Discounts: Many hospitals and healthcare providers are willing to offer discounts to patients who cannot afford to pay. Don’t hesitate to ask for a discount, especially if you’re in financial hardship.

- Propose a Payment Plan: If you cannot pay the full amount, ask the provider if you can set up a payment plan that fits your budget. Many providers will work with you to find a manageable solution.

- Appeal Insurance Denials: If your insurance denied coverage for treatments that were necessary, appeal the decision. Often, insurance companies will reverse the denial after a successful appeal, reducing your medical debt.

By negotiating effectively, you may be able to reduce your debt or arrange a payment plan that makes the situation more manageable. Always make sure that any agreements are put in writing to avoid any future misunderstandings.

Government Coverage Programs That May Reduce Your Medical Costs

Government programs such as Medicaid, Medicare, and CHIP are designed to provide health coverage, not direct medical debt forgiveness. However, they can play an important role in reducing out-of-pocket costs and, in many cases, help individuals avoid accumulating large medical bills in the first place.

Understanding how these programs work is essential, especially if you are trying to manage current expenses or prevent future financial strain from healthcare costs.

Let’s look at how these programs support cost reduction:

- Medicaid: Medicaid provides free or low-cost health coverage to eligible low-income individuals and families. It typically covers a wide range of services, including hospital visits, doctor consultations, prescriptions, and preventive care. By covering these costs upfront, Medicaid can significantly reduce the likelihood of unpaid medical bills.

- Medicare: A federal health insurance program primarily for individuals aged 65 and older, as well as for certain younger individuals with disabilities. It includes different parts that cover hospital care (Part A), outpatient services (Part B), and prescription drugs (Part D). While it does not eliminate all out-of-pocket expenses, it helps reduce the overall cost burden of medical care.

- CHIP(Children’s Health Insurance Program)

CHIP provides low-cost health coverage for children in families who do not qualify for Medicaid but cannot afford private insurance. It covers essential services such as doctor visits, immunisations, prescriptions, and emergency care, helping families manage healthcare expenses more effectively.

How Do These Programs Help in Practice?

While these programs are not structured as debt forgiveness solutions, they can:

- Reduce the upfront cost of medical care

- Limit the amount you need to pay out of pocket

- Help prevent new medical debt from accumulating

In some situations, enrolling in these programs or qualifying retroactively may also help address recent medical expenses, depending on eligibility and timing.

The key takeaway is that these programs are best viewed as cost-reduction and prevention tools, rather than direct debt forgiveness options.

If you need a clear breakdown of how debt resolution and collection work so you can make informed decisions with confidence, check out our detailed guide on Understanding Debt Resolution and Collection Processes.

State Protections and Consumer Rights

It’s essential to understand your rights when dealing with medical debt collection. In the U.S., both federal and state laws are designed to protect consumers from aggressive debt collection practices, ensuring they are treated fairly throughout the process. These protections provide a much-needed shield for individuals experiencing financial hardship due to medical debt.

Let's look at the key consumer protection rights.

- Limitations on Contact Hours: Under the Fair Debt Collection Practices Act (FDCPA), debt collectors are prohibited from contacting you at inconvenient hours. They cannot call you before 8 a.m. or after 9 p.m. unless you have agreed to it. This regulation helps ensure that collectors do not invade your personal time or cause undue stress outside of reasonable hours. Learn more about the FDCPA here.

- Written Validation Notice: Debt collectors are required by law to provide you with a written validation notice within five days of their first contact. This notice must include the amount of the debt, the name of the creditor, and details about how to dispute the debt.

- 30-Day Dispute Window: If you dispute a medical debt within 30 days of receiving a written notice, collection activities must pause until the debt is verified. This gives consumers the opportunity to confirm the accuracy of the debt before any further action, such as wage garnishment or lawsuits, is pursued.

Understanding your rights is crucial for navigating medical debt and making informed decisions about your finances. Always keep records of communication with debt collectors and seek professional advice if you feel your rights have been violated.

Discover why personalized repayment discussions create steadier outcomes by reading Why One-Size-Fits-All Debt Solutions Don't Work for Real Relief.

How Medical Debt May Affect Your Credit?

Medical debt does not always appear on your credit report immediately, and recent policy changes have reduced its impact compared to other types of debt.

Here’s how it typically works:

- $500 threshold: Medical collections under $500 are generally not included on credit reports. This helps prevent small balances from affecting your credit profile.

- 365-day grace period: Unpaid medical debt is not reported right away. Credit bureaus typically wait at least 365 days before adding it to your report, giving you time to resolve bills, apply for assistance, or dispute charges.

- Paid collections are removed: Once a medical debt in collections is paid, it is removed from your credit report. This is different from many other types of debt, where paid collections may still remain visible.

- Only unresolved larger balances may appear: Medical collections over $500 that remain unpaid after the grace period may be reported and can impact your credit score.

- Disputing errors matters: Medical bills often contain errors. If a balance is incorrect, disputing it early can prevent it from being reported or affecting your credit.

Understanding these rules can help you act early, avoid unnecessary credit damage, and focus on resolving medical bills before they escalate.

Alternatives When Forgiveness Isn’t Available

If you’re unable to secure medical debt forgiveness, there are still several alternatives you can explore to manage and reduce your medical debt.

The alternative options include:

- Payment Plans: Many healthcare providers offer monthly payment plans to help patients manage their debt over time. If you can’t pay the full balance, ask if you can pay in installments.

- Debt Settlement: If you can afford to pay a reduced lump sum, you might be able to settle your debt for a lower amount. Contact your provider or debt collector and negotiate a settlement.

- Credit Counseling: Credit counseling services can help you create a budget, develop a debt repayment plan, and, in some cases, negotiate better terms for your medical debt. Counselors can help you manage your finances and reduce the overall impact of your medical debt.

While forgiveness may not be available, these alternatives can provide immediate relief and make your debt more manageable. It’s essential to explore all your options to find the best solution for your financial situation.

Final Thoughts

Medical debt can feel overwhelming, but understanding your options is key to regaining control. With the right information, you can navigate the complexities of medical debt relief and forgiveness with clarity and confidence. It's important to know your rights and the resources available to you, whether through government programs, nonprofit organizations, or direct negotiations with your healthcare provider.

If your medical bill has already moved into collections or servicing, Forest Hill Management can help you understand your account status, review available repayment options, and communicate through a structured process.

If you have questions about your medical debt or need personalized support, contact our advisors for tailored assistance.

FAQs

1. Can medical debt be completely forgiven?

Yes, medical debt can be forgiven through various programs, including charity care from hospitals, nonprofit debt-forgiveness organizations, and government initiatives such as Medicaid and Medicare. Eligibility for forgiveness depends on your income, the amount of debt, and sometimes, your residency.

2. How can I apply for charity care at a hospital?

To apply for charity care, you typically need to contact the hospital's billing department, submit a financial assistance application, and provide documentation such as proof of income, tax returns, and proof of residency. Hospitals often have their own specific eligibility criteria, so it’s important to ask about their process early.

3. What are the eligibility requirements for nonprofit medical debt forgiveness?

Eligibility for nonprofit medical debt forgiveness usually depends on your income level, the total amount of debt, and sometimes, your geographic location. Many organizations prioritize individuals with low incomes who cannot afford to pay their medical bills. Check with organizations like Undue Medical Debt.

4. How do Medicaid and Medicare help with medical debt?

Medicaid and Medicare can significantly reduce or eliminate medical debt by covering the costs of medical services. Medicaid provides low-cost or free coverage for low-income individuals, while Medicare helps those over 65 or with certain disabilities. These programs can help pay for doctor visits, hospital stays, medications, and preventive care.

5. What should I do if I cannot qualify for medical debt forgiveness?

If you don’t qualify for medical debt forgiveness, you can negotiate payment plans with your healthcare providers, consider debt settlement options, or work with credit counselors. These options can help you manage and pay off your debt without overwhelming your financial situation.