Understanding Debt Resolution and Collection Processes

Need Help Reviewing Your Account?

Contact UsDebt collection is more common than many people realize. Research shows that approximately 20% of people with a credit report, or one in five, had at least one debt in collections listed on their credit report as of the first quarter of 2023, highlighting how widespread the issue is across the United States.

At the same time, 15 million Americans continue to deal with collection accounts related to medical bills, utilities, credit cards, and other everyday financial obligations.

The good news is that understanding how the process works can make the situation far less intimidating. When you know your rights and the steps involved, you can approach collection communication with more confidence and clarity.

In this blog, we’ll explain how to deal with collection agencies, how the debt resolution process works, what rights you have as a consumer, and the practical steps you can take to address collection accounts responsibly.

Key Takeaways

- Collection accounts are common. Around one in five people with a credit report has had a debt in collections at some point.

- Understanding the process helps you respond confidently. Knowing how debts move from delinquency to collections removes uncertainty.

- Consumers have legal protections. The FDCPA requires collectors to provide validation, communicate fairly, and respect dispute rights.

- A structured approach makes resolution easier. Verify the debt, review documentation, and explore repayment options before taking action.

- Keeping records protects you. Saving notices, messages, and payment confirmations helps maintain clarity throughout the resolution process.

Why Collection Agencies Contact Consumers?

When a debt moves into collections, the collection agency’s role is to contact the consumer and attempt to resolve the unpaid balance. These agencies act on behalf of creditors or companies that now manage the account, and their goal is typically to establish communication and explore ways the debt can be addressed.

Understanding why collection agencies reach out can make the process feel less uncertain and help you respond with clearer expectations.

- To notify you that the account is in collections: One of the first reasons a collection agency contacts you is to inform you that the debt has been transferred or assigned for recovery. This communication often includes details about the balance owed and the creditor involved.

- To provide information about the debt: Federal regulations require collectors to share certain information about the account, such as the amount owed and the name of the current creditor. This helps consumers understand what the debt relates to and who is managing it.

- To confirm or verify account details: Collection agencies may ask questions to ensure they are speaking with the correct individual and that the account information is accurate before discussing repayment.

- To discuss repayment options: In many cases, the purpose of the contact is to explore possible ways to resolve the balance. This may include discussing payment plans, settlement options, or other arrangements that make repayment more manageable.

- To maintain communication about the account: Ongoing communication allows both parties to track the status of the debt, clarify questions, and document repayment discussions if they occur.

While receiving contact from a collection agency can feel stressful, the purpose of the outreach is typically to establish communication and work toward resolving the account in an organized way.

Understanding why the agency is contacting you can help you approach the conversation more confidently and make informed decisions about the next steps.

What Happens When a Debt Goes to Collections?

When a payment remains unpaid for an extended period, the account may eventually move into collections. This step usually occurs after several months of missed payments and unsuccessful attempts by the original creditor to recover the balance.

While the timeline varies by lender, many creditors begin internal collection efforts after the first missed payment. If the account remains unpaid for a longer period, typically around 90 to 180 days, the creditor may transfer the account to a third-party collection agency or sell the debt to a company that specializes in recovering unpaid balances.

Understanding how this process works can help remove some of the uncertainty surrounding collection notices.

- The account first becomes delinquent: When a payment is missed, the account enters delinquency. Creditors often begin sending reminders, late notices, or phone calls requesting payment during this stage.

- The creditor may attempt internal recovery: Many lenders try to resolve the issue directly before involving outside parties. This can include additional reminders, payment discussions, or temporary hardship arrangements.

- The account may be transferred or assigned to a collection agency: If the balance remains unpaid, the creditor may place the account with a collection agency that contacts the borrower on the creditor’s behalf to discuss repayment.

- In some cases, the debt may be sold to another company: Certain debts are sold to specialized companies that purchase delinquent accounts and then attempt to recover the balance.

Once an account reaches the collections stage, the primary goal typically shifts toward resolving the balance through communication, verification of the debt, and discussion of possible repayment options.

Also read: Debt Collection Advice: Know Your Rights and Options

Receiving a notice from a collection agency does not automatically mean legal action will occur. In many cases, the situation can be addressed by reviewing the account details, understanding your rights, and exploring realistic repayment solutions.

Know Your Rights When Dealing With Collection Agencies

When a collection agency contacts you about an unpaid debt, it is important to remember that U.S. consumer protection laws provide specific safeguards. The Fair Debt Collection Practices Act (FDCPA) establishes rules that debt collectors must follow when communicating with consumers. These protections are designed to ensure that the collection process remains transparent, respectful, and fair.

Understanding these rights can help you respond with confidence and make informed decisions about how to handle the situation.

- Right to Receive a Debt Validation Notice: Within five days of first contacting you, a debt collector must provide a written notice explaining the amount owed, the name of the creditor, and how you can dispute the debt. This notice is known as a validation letter and ensures you receive clear information about the account before making payments.

Also read: Understanding Debt Validation Letters: How to Validate Debt

- Right to Dispute the Debt Within 30 Days: After receiving the validation notice, you generally have 30 days to dispute the debt in writing if you believe the balance is incorrect, already paid, or does not belong to you. If you dispute the debt during this period, the collector must pause collection activity until it provides verification of the debt.

- Right to Be Free From Harassment or Deceptive Practices: Debt collectors cannot threaten, harass, or mislead you while attempting to collect a debt. For example, they cannot use abusive language, make repeated calls intended to intimidate you, or falsely claim that legal action will occur if it is not actually planned.

- Right to Limit or Stop Certain Communications: You may request that a collector stop contacting you or limit how they communicate with you. When such a request is made in writing, the collector generally must stop most communication except to confirm the request or notify you of potential legal action.

- Right to Accurate Reporting and Documentation: Debt collectors must provide accurate information about the debt and cannot report false details to credit bureaus. If a debt is disputed, collectors must also notify credit reporting agencies that the account is under dispute.

These rights exist to protect consumers during the debt resolution process.

If you believe your rights have been violated, you can submit a complaint to the Consumer Financial Protection Bureau (CFPB) for review.

Step-by-Step Guide on How to Deal With Collection Agencies

Receiving communication from a collection agency can feel stressful, especially if you are unsure how to respond. However, handling the situation methodically can help you protect your rights, confirm the accuracy of the debt, and explore practical options for resolving the account.

The following steps outline a structured approach to dealing with collection agencies while keeping the process clear and manageable.

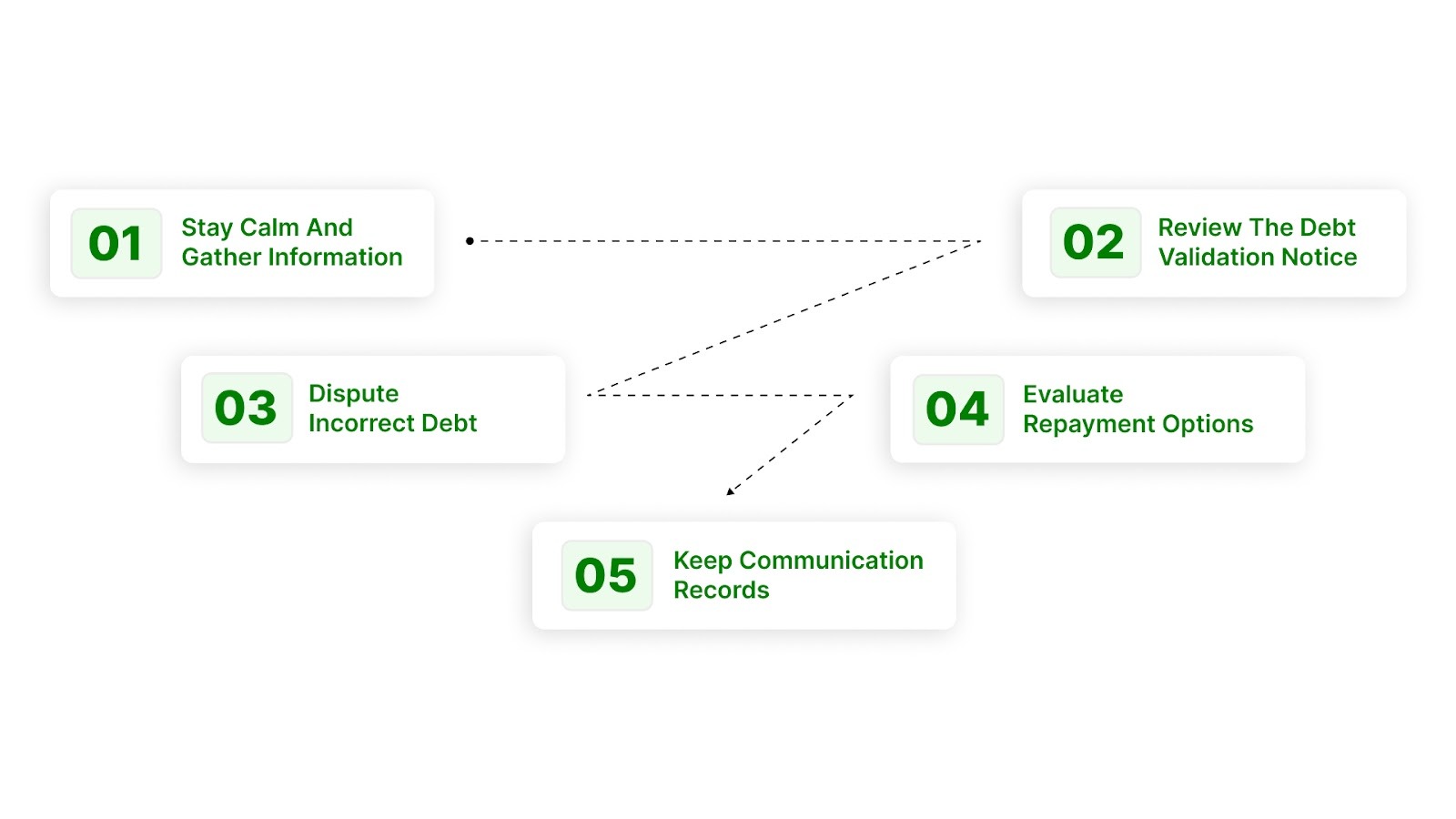

Step 1: Stay Calm and Gather Basic Information

The first step is simply understanding who is contacting you and why. Collection agencies are required to identify themselves and provide certain information about the debt.

- Ask for the collector’s details: Request the company name, mailing address, and contact information so you know who is reaching out.

- Confirm the creditor and account information: Ask which original creditor the debt relates to and what the balance is supposed to represent.

- Take notes during the conversation: Record the date, time, and key details of the communication so you have a clear record moving forward.

Gathering this information helps you determine whether the contact appears legitimate before discussing repayment.

Step 2: Review the Debt Validation Notice

Under the Fair Debt Collection Practices Act (FDCPA), collectors must provide written information about the debt shortly after their first contact. This notice typically includes the amount owed and the name of the creditor.

- Check the balance carefully: Compare the amount listed with your own records or past statements.

- Confirm the creditor’s identity: Make sure the debt relates to an account you actually recognize.

- Look for instructions on how to dispute the debt: The notice should explain how to respond if you believe the information is incorrect.

Reviewing the validation notice helps ensure that you are dealing with the correct account.

Step 3: Dispute the Debt if Something Appears Incorrect

If you believe the debt is inaccurate, incomplete, or does not belong to you, you have the right to dispute it.

- Send a written dispute if necessary: A written letter or email creates a clear record of your request for verification.

- Ask for supporting documentation: This may include account statements or proof that the debt belongs to you.

- Keep copies of your correspondence: Documentation can help protect you if questions arise later.

Disputing inaccurate information ensures that you are not making payments toward a debt that may not be valid.

Step 4: Evaluate Your Repayment Options

If the debt is valid, the next step is determining how you might resolve it. Many collection agencies are willing to discuss repayment options.

- Ask about payment plans: Installment arrangements can make balances easier to manage over time.

- Discuss settlement options if appropriate: In some situations, a one-time payment may resolve the account.

- Choose a payment schedule that fits your financial situation: A realistic plan helps ensure you can maintain the agreement.

Clear communication about repayment can often move the situation toward resolution without further escalation.

Step 5: Keep Records of All Communication

Documentation is an important part of managing collection accounts.

- Save letters, emails, and messages: These documents show the history of communication about the account.

- Keep proof of all payments: Payment confirmations and receipts help demonstrate that balances were paid as agreed.

- Document phone conversations when possible: Record dates, representative names, and key points discussed.

Debt resolution often becomes easier when communication remains clear and organized. However, there are situations where handling the process alone can become difficult or confusing.

You may consider seeking professional support when:

- You are dealing with multiple collection accounts at the same time

- The account ownership or balance details are unclear

- You are unsure how to respond to collection communication

- Repeated attempts to resolve the account have not produced progress

In these situations, professional assistance can help organize the process and clarify the next steps. Structured support can help ensure that communication remains clear, account details are properly reviewed, and repayment options are discussed in a practical and responsible way.

Also read: How to Keep Your Debt Resolutions in 2025

Approaching collection agencies with a structured plan helps you stay informed, protect your rights, and work toward resolving outstanding balances in a responsible way.

Conclusion

Collection accounts can feel stressful at first, but they are often easier to manage once you understand how the process works. Just as importantly, dealing with collection agencies does not mean you have to face the process alone.

If you are dealing with a collection account and want help understanding your options, The Forest Hill Management provides structured support designed to bring clarity to the process.

Through organized account management, secure payment options, and respectful communication practices, individuals can review their accounts and explore repayment arrangements that align with their financial circumstances.

Contact The Forest Hill Management today to review your account details and take the next step toward resolving collection balances with confidence and clarity.

FAQs

1. Will paying a collection account remove it from my credit report?

Not necessarily. A paid collection may still remain on your credit report for a certain period, but its status may be updated to reflect that the balance has been resolved.

2. How can I confirm if a collection agency contacting me is legitimate?

You can verify the agency by requesting written information about the debt, checking the company’s official contact details, and confirming that the account matches your records.

3. Can a collection agency add additional fees to the debt?

Additional fees may only be added if they are permitted by the original agreement or allowed under state law. If you notice unexpected charges, you can request clarification in writing.

4. What should I do if multiple agencies contact me about the same debt?

Ask each agency for written verification of the debt and the current creditor. This helps determine which company is authorized to manage the account.

5. Is it possible to resolve a collection account even if I cannot pay the full balance immediately?

In many situations, repayment arrangements or settlement discussions may be available. These options allow individuals to address outstanding balances in a structured and manageable way.