How to Manage Debt in Retirement

Need Help Reviewing Your Account?

Contact UsRetirement is often imagined as a phase where financial pressure finally eases. But for many people, that is not how it unfolds. Instead of fewer obligations, there is often a shift, where income becomes fixed, but expenses continue to move. When debt is part of that equation, even routine financial decisions can start to feel heavier than expected.

Recent research shows that 60%+ of U.S. households headed by someone over 65 now carry debt, a sharp rise compared to previous decades.

What makes this situation challenging is not just the presence of debt, but the way it interacts with limited income and long-term financial security.

In this blog, you will learn how to manage debt during retirement, the strategies that help protect your financial stability, and how structured account management can make the process clearer and more manageable.

Key Takeaways

- Managing debt in retirement requires a structured approach that prioritizes stability over aggressive repayment.

- Understanding your full financial picture, including income and obligations, is essential for making informed decisions.

- Focusing on high-interest debt and following a consistent repayment strategy helps reduce long-term financial pressure.

- Protecting retirement savings while repaying debt is critical to maintaining long-term financial security.

- Clear communication, organized records, and consistent tracking make the repayment process more manageable and less stressful.

What Debt in Retirement Really Looks Like?

Debt does not automatically disappear when you retire. In many cases, it carries forward into a phase of life where income becomes more fixed and financial decisions require greater precision. Understanding what debt looks like at this stage helps remove uncertainty and puts your situation into clearer perspective.

- Debt Can Continue Into Retirement Years: Many individuals enter retirement with existing financial obligations that have not yet been fully paid off. This can include long-term commitments like mortgages or shorter-term balances that extended over time due to changing financial circumstances.

- Common Types of Debt in Retirement: Retirement debt is not limited to one category. It often includes a mix of obligations, each with different repayment structures and timelines:

- Credit card balances that may carry higher interest rates

- Mortgage payments that extend into retirement years

- Medical expenses that arise unexpectedly

- Personal loans or service-related contracts that remain active

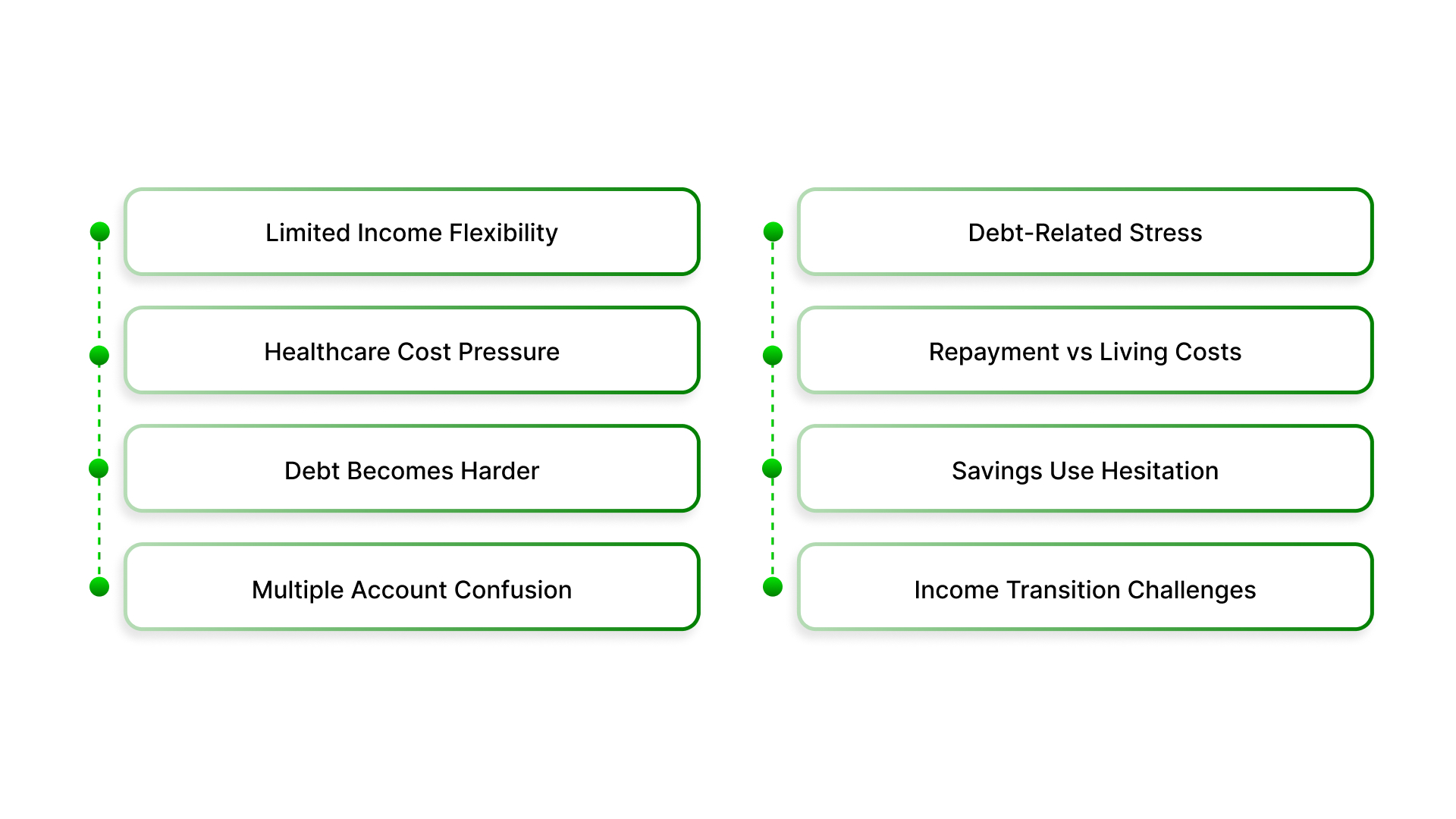

- A Fixed Income Changes How Debt Feels: Unlike earlier stages of life, retirement income often comes from fixed sources such as pensions, savings, or Social Security. This limits flexibility, making it important to manage payments in a way that aligns with a predictable monthly budget.

- Unexpected Expenses Can Add Pressure: Healthcare costs, home maintenance, or other unplanned expenses can arise without warning. When these occur alongside existing debt, they can make financial planning feel more constrained.

- Multiple Accounts Can Create Confusion: Managing several debts at once, each with different balances, due dates, and terms, can make it difficult to keep track of what needs attention. This lack of clarity often adds to the overall stress of managing finances in retirement.

- Financial Stability Becomes the Priority: At this stage, the focus shifts from aggressive repayment to maintaining balance. The goal is not just to reduce debt, but to do so in a way that supports long-term financial stability and avoids unnecessary strain.

Understanding these realities helps reframe the situation. The challenge is not simply having debt in retirement. It is managing it in a structured way that keeps your finances stable and predictable.

Also read: How to Get Out of Debt: Practical Steps that Work

With that context in place, the next step is to look at practical strategies that can help you manage debt more effectively during retirement.

8 Strategies to Manage Debt During Retirement

Managing debt in retirement requires a structured, priority-based approach. With a fixed or limited income, every financial decision carries more weight, which makes clarity and consistency essential. The goal is not just to reduce debt, but to do so in a way that protects your long-term stability and avoids unnecessary financial strain.

Here's how:

Start With a Clear View of Your Financial Situation

Understanding your complete financial picture is the first and most important step. Without clarity, it becomes difficult to prioritize debts or make confident decisions about repayment.

- List all your debts in one place: Include every outstanding balance such as credit cards, personal loans, mortgages, and medical bills. Seeing everything together helps you understand the full scope of your obligations and prevents accounts from being overlooked.

- Identify interest rates and balances: Each debt behaves differently based on its interest rate and size, which directly affects how quickly it grows. Knowing these details helps you decide where your payments will have the most impact over time.

- Review your monthly obligations: Take note of minimum payments, due dates, and any penalties tied to missed payments. This allows you to understand how much you are required to pay each month just to stay current.

- Assess all sources of income: Look at Social Security, pension income, savings withdrawals, and any additional earnings. This helps you determine what portion of your income can realistically be used for repayment without creating financial strain.

Clarity at this stage reduces uncertainty and allows you to approach the rest of the process with confidence.

Prioritize High-Interest Debt First

High-interest debt can quickly become difficult to manage, especially when your income is fixed. Addressing these accounts early helps prevent balances from growing faster than you can repay them.

- Focus on credit cards and unsecured loans first: These types of debt often carry the highest interest rates, which means a larger portion of your payment goes toward interest instead of reducing the balance. Over time, this can slow progress significantly if not addressed early.

- Apply the avalanche method strategically: Continue making minimum payments on all accounts while directing extra funds toward the highest-interest balance. This approach helps reduce the overall cost of debt and shortens the repayment timeline.

- Protect your monthly income from interest accumulation: High-interest debt can quietly consume a significant portion of your fixed income. Reducing it early helps free up more money for essential expenses and other obligations.

- Avoid letting balances grow unchecked: When interest compounds over time, even small balances can become difficult to manage. Prioritizing these debts prevents them from becoming long-term financial pressure points.

Focusing on high-interest debt first helps stabilize your financial situation and creates more breathing room in your budget.

Choose a Structured Repayment Strategy

A defined repayment strategy gives your plan direction and consistency. Without structure, it becomes easy to make inconsistent payments that do not lead to meaningful progress.

- Avalanche method for long-term efficiency: This method helps reduce the total amount of interest paid over time, making it financially effective for those focused on cost savings. It works best when you can stay consistent even without immediate visible results.

- Snowball method for steady motivation: Paying off smaller debts first creates a sense of accomplishment and frees up cash flow as each account is closed. This can make it easier to stay committed, especially when managing multiple debts.

- Maintain minimum payments across all accounts: While focusing on one priority debt, it is important to stay current on others to avoid penalties or further complications. This ensures that your overall financial position does not worsen.

- Choose a strategy that fits your situation: The most effective approach is one that aligns with your income, comfort level, and ability to remain consistent. A strategy that feels manageable is more likely to succeed over time.

A structured approach removes guesswork and helps you move forward with a clear, repeatable plan.

Build a Retirement-Focused Budget

Budgeting during retirement is less about flexibility and more about maintaining stability. With limited income, every expense must be planned carefully to support both daily living and debt repayment.

- Separate essential and non-essential expenses: Prioritize costs such as housing, food, healthcare, and utilities before allocating money to discretionary spending. This ensures that your basic needs are always covered first.

- Account for healthcare and unexpected costs: Medical expenses can increase with age and often come without warning. Including these in your budget helps prevent sudden financial disruptions.

- Align your budget with fixed income streams: Unlike working years, your income may not change significantly month to month. Your spending plan should reflect this consistency to avoid overspending.

- Create a sustainable repayment allocation: Identify a realistic amount that can be consistently applied toward debt without affecting essential expenses. This helps maintain progress without creating additional pressure.

A well-structured budget ensures that debt repayment fits within your financial reality rather than working against it.

Avoid Draining Long-Term Savings Too Quickly

Using savings to pay off debt may seem like a quick solution, but it can create long-term financial challenges if not handled carefully.

- Be careful with 401(k) or IRA withdrawals: Early distributions from retirement accounts before age 59½ are generally subject to an additional 10% tax unless an exception applies, and hardship withdrawals can permanently reduce what remains in the plan for retirement.

- Preserve your long-term financial security: Savings are meant to support you throughout retirement, not just solve immediate issues. Depleting them too quickly can leave you vulnerable to future expenses.

- Use savings strategically if needed: If you decide to use savings, do so in a controlled and gradual way that does not disrupt your overall financial plan.

- Balance immediate relief with future stability: Paying off debt quickly should not come at the cost of long-term financial independence. A balanced approach helps maintain both.

Protecting your savings ensures that you remain financially stable even after your debts are reduced.

Explore Ways to Reduce Financial Pressure

Lowering your overall expenses can create more room for repayment without requiring additional income. Small adjustments can make a significant difference over time.

- Consider downsizing your living space: Moving to a smaller or more affordable home can reduce housing costs, which are often one of the largest monthly expenses.

- Evaluate relocation options: Living in a lower-cost area can help stretch your income further and make debt repayment more manageable.

- Reduce recurring financial commitments: Review subscriptions, services, or ongoing expenses that may no longer be necessary in retirement. Eliminating these can free up funds.

- Adopt sustainable lifestyle adjustments: Gradual changes are easier to maintain and less likely to disrupt your overall well-being. Consistency matters more than drastic cuts.

Reducing financial pressure helps create a more balanced environment for managing both expenses and debt.

Consider Consolidation or Simplification

Managing multiple debts can become overwhelming, especially when each has different terms and deadlines. Simplifying your financial structure can make repayment easier to manage.

- Combine multiple debts into a single payment: Consolidation can reduce the number of accounts you need to track, making it easier to stay organized and consistent.

- Explore refinancing options where appropriate: Lowering interest rates or adjusting repayment terms can make monthly payments more manageable.

- Reduce the risk of missed or late payments: Fewer accounts mean fewer due dates, which helps minimize confusion and errors.

- Focus on creating a clearer repayment path: A simplified structure allows you to concentrate on progress rather than managing complexity.

Simplification does not eliminate debt, but it makes the process more manageable and less stressful.

Generate Additional Income If Possible

Increasing income, even slightly, can provide additional flexibility in your repayment plan without putting pressure on savings.

- Consider part-time or flexible work opportunities: Light work can provide a steady stream of additional income without significantly affecting your lifestyle.

- Leverage previous experience or skills: Consulting or freelance work can allow you to earn without committing to full-time employment.

- Delay claiming Social Security if possible: Delaying benefits beyond full retirement age increases monthly benefits, with the increase continuing until age 70.

- Reduce reliance on savings for everyday expenses: Additional income can help preserve long-term financial resources while supporting current needs.

Even a small increase in income can make a noticeable difference in your ability to manage debt.

For retirees, this kind of structured communication is valuable because it reduces uncertainty. It is also where a consumer-facing servicing approach, such as the one Forest Hill Management uses, can help create clarity around what is owed, what comes next, and how to move forward without confusion.

Once these financial priorities are in place, the next step is to look at the common challenges retirees face when managing debt and how those challenges affect the overall plan.

Common Challenges of Managing Debt in Retirement

Managing debt in retirement is not just about making payments. The situation often comes with a unique set of financial and emotional challenges that can make even simple decisions feel difficult.

Understanding these challenges helps you approach them with more clarity and realistic expectations.

- Limited and Fixed Income Creates Less Flexibility: In retirement, income usually comes from fixed sources such as pensions or Social Security. This means there is less room to adjust when expenses increase or unexpected costs arise, making debt payments feel more restrictive.

- Rising Healthcare Costs Add Financial Pressure: Medical debt expenses tend to increase with age and can be unpredictable. Even well-planned budgets can be disrupted by sudden healthcare needs, which may lead to additional financial strain or reliance on credit.

- Existing Debt Can Feel Heavier Over Time: Debts that once felt manageable during working years can become more difficult to handle without a steady or growing income. Interest accumulation and fixed payment obligations can make balances feel more persistent.

- Multiple Accounts Can Lead to Confusion: Managing several debts with different due dates, balances, and terms can become overwhelming. Without a clear system, it becomes harder to track progress, increasing the chances of missed payments or misunderstandings.

- Emotional Stress and Financial Uncertainty: Debt during retirement can create ongoing stress, especially when there is concern about outliving savings. This stress can make it harder to make clear decisions and may lead to avoidance or delayed action.

- Balancing Debt Repayment With Daily Living Needs: Retirement requires careful balancing between paying down debt and covering essential expenses. Focusing too much on one can disrupt the other, making it important to maintain a steady and realistic approach.

- Reluctance to Use Savings, Yet Limited Alternatives: Many individuals prefer not to draw from their savings, but without additional income, options can feel limited. This creates a constant tension between preserving long-term security and managing current obligations.

- Changes in Financial Management Habits: Transitioning from a working income to a fixed income often requires a shift in how finances are managed. Adjusting to this change can take time, especially when dealing with ongoing debt.

Also read: How to Manage Multiple Loan Repayments Effectively

Recognizing these challenges is important because it shifts the focus from pressure to planning. When you understand what makes debt management more complex in retirement, it becomes easier to adopt strategies that are realistic, structured, and sustainable.

Conclusion

Managing debt in retirement is not about eliminating everything at once. It is about creating a plan that fits your reality. When your income is steady but limited, the focus shifts from speed to sustainability. What matters most is knowing where you stand, prioritizing what needs attention, and moving forward in a way that protects both your present and your future.

Debt in retirement can feel uncertain, but it does not have to remain that way. With clear information, consistent steps, and structured communication, it becomes something you can manage rather than something that controls your decisions.

If your account is being handled by The Forest Hill Management, the goal is to support that clarity. Through organized account oversight, secure payment options, and realistic repayment discussions, you can understand your situation and take steps forward without unnecessary confusion.

Take the first step toward regaining financial clarity.

FAQs

1. Is it too late to manage or reduce debt after retirement?

No, it is never too late. Debt can still be managed effectively in retirement by adjusting your approach to match your income and focusing on steady, realistic progress.

2. How do I know if my debt is becoming unmanageable in retirement?

If your monthly payments are affecting your ability to cover essential expenses or causing ongoing stress, it may be time to reassess your plan and explore alternative options.

3. Can debt impact my retirement lifestyle significantly?

Yes, unmanaged debt can limit how you use your income and savings, which may affect your ability to maintain a comfortable and predictable lifestyle.

4. What should I do if I receive communication about an old or unfamiliar debt?

Take time to review the details carefully, verify the account information, and request clarification if needed before making any decisions.

5. Is it possible to manage debt without increasing income in retirement?

Yes, many people manage debt by adjusting expenses, prioritizing payments, and following a structured plan without relying on additional income.