How to Rebuild Credit After Collections in 10 Steps

Need Help Reviewing Your Account?

Contact UsSeeing a collection account on your credit report can feel discouraging.

The reality is that collection accounts are far more common than most people think. As of early March 2026, U.S. national debt has reached approximately $38.87 trillion, after surpassing the $38 trillion milestone in October 2025. The country’s debt-to-GDP ratio now stands at more than 124%, highlighting the scale of borrowing across the economy and the broader financial pressures.

While collections can affect your credit score, they do not define your financial future. Credit reports change over time, and consistent positive actions can gradually improve your credit profile.

In this blog, we’ll explain how to rebuild credit after collections. You’ll learn the steps to review and resolve collection accounts, build stronger credit habits, avoid common mistakes that slow recovery, and move toward a healthier financial position.

Key Takeaways

- Collection accounts can significantly affect your credit score, but their impact gradually decreases over time as you build a record of consistent, positive payment behavior.

- Rebuilding credit begins with understanding your credit report, verifying collection accounts, and resolving outstanding balances whenever possible.

- Establishing new positive credit activity, such as using secured credit cards or credit-builder loans responsibly, helps strengthen your credit profile after collections.

- Maintaining healthy financial habits, including low credit utilization and on-time payments, plays a major role in long-term credit recovery.

- Avoiding common mistakes such as ignoring collections, applying for excessive credit, or falling for credit repair scams can help protect and accelerate your progress.

What Happens to Your Credit When an Account Goes to Collections?

When an account is sent to collections, it usually means payments have been overdue long enough that the original creditor has transferred or sold the debt to a collection agency. At that point, the collection account may appear on your credit report and affect your credit score.

Collection accounts are considered serious negative marks because they indicate that a debt was not repaid according to the original agreement. Credit scoring models place significant weight on payment history, which is why collection accounts can cause a noticeable drop in your credit score.

Several important things happen once a debt enters collections:

- A new collection account may appear on your credit report: When a debt is transferred to a collection agency, it may be reported as a separate entry on your credit report alongside the original account. This new listing signals to lenders that the debt required external recovery efforts.

- Your credit score may decline significantly: Because payment history is one of the most influential factors in credit scoring models, collection accounts can reduce your score and make it harder to qualify for loans, credit cards, or favorable interest rates.

- The collection account can remain on your credit report for years: In most cases, a collection account stays on your credit report for up to seven years from the date of the first missed payment that led to the collection.

- Paying the collection can improve your financial profile over time: Even though a paid collection may still appear on your report, resolving the balance can prevent further damage and may help your credit recover gradually as new positive payment history is established.

Also read: Debt Resolution Programs: How They Work and What to Expect

The good news is that collections do not permanently define your credit profile. Their impact usually decreases over time, especially when you begin building a consistent record of on-time payments and responsible credit use.

Understanding how collections affect your credit is the first step toward rebuilding it. Once you know what you are working with, you can begin taking deliberate actions that gradually strengthen your credit profile again.

10 Steps to Rebuild Credit After Collections

Rebuilding credit after consumer collections is possible, but it usually requires a combination of resolving outstanding accounts and establishing new positive credit behavior. Credit scoring models reward recent activity more than older mistakes, which means consistent payments and responsible credit use can gradually strengthen your credit profile over time.

The following steps can help you rebuild your credit in a structured and practical way after dealing with collection accounts:

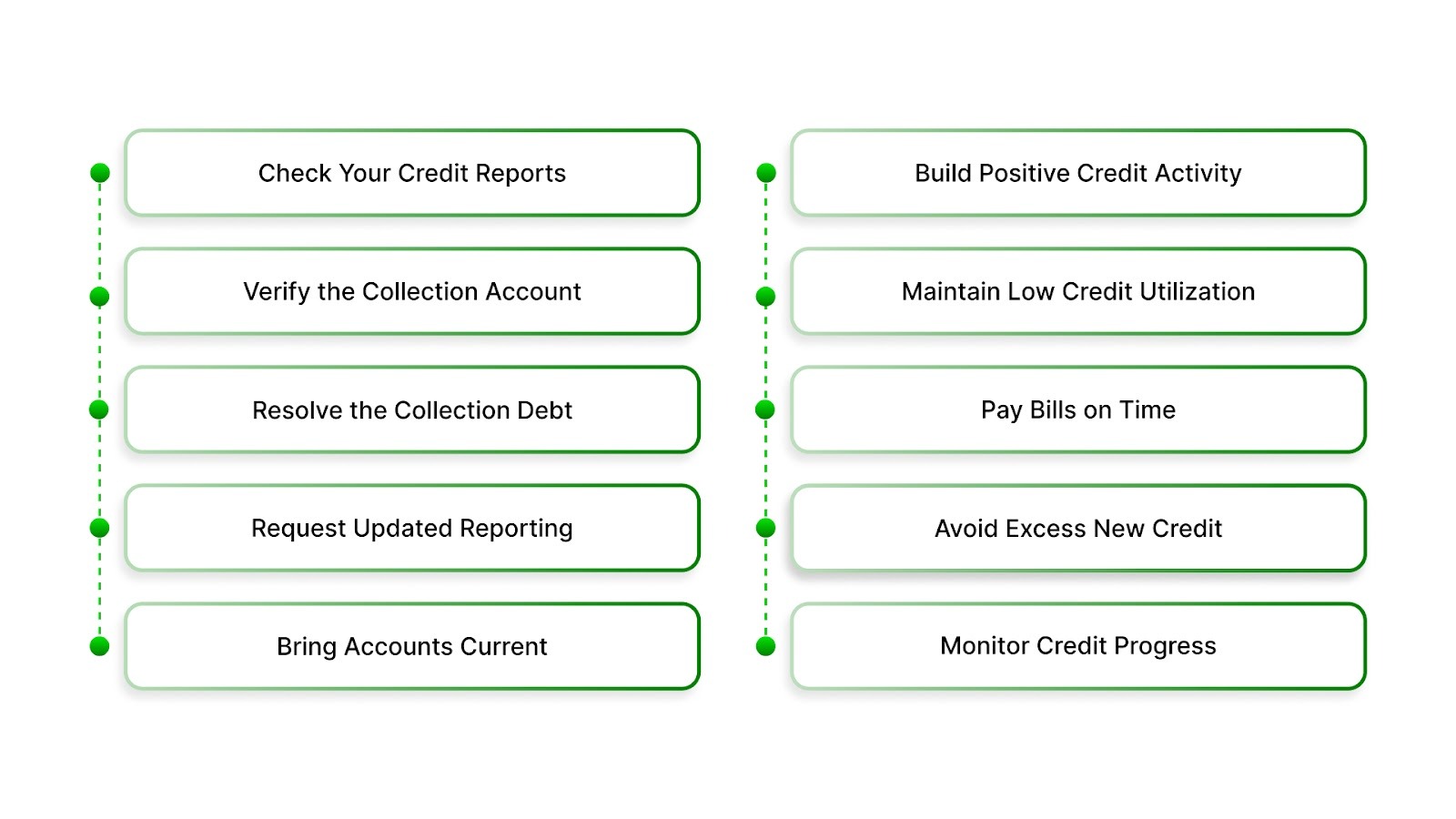

Step 1: Check Your Credit Reports Carefully

The first step in rebuilding credit is understanding exactly what appears on your credit report. This allows you to identify collection accounts and verify that the reported information is accurate.

- Obtain reports from all three credit bureaus: Review your reports from Equifax, Experian, and TransUnion. Each bureau may display slightly different information, so reviewing all three helps ensure you are not missing any accounts.

- Identify all collection accounts listed: Look for accounts marked as “collection,” “charged-off,” or “past due.” Note the account balance, the date it was first reported, and the agency managing the account.

- Look for errors or outdated reporting: Common mistakes include duplicate collections, incorrect balances, or accounts that do not belong to you. Credit reporting errors can negatively affect your score and should be disputed if discovered.

Starting with accurate information ensures that your rebuilding strategy is based on facts rather than assumptions.

Step 2: Verify the Collection Account

Before making payments toward a collection account, confirm that the debt is valid and that the reported information is correct.

- Review the validation notice carefully: Under the Fair Debt Collection Practices Act (FDCPA), debt collectors must provide written details about the debt, including the amount owed and the creditor’s name.

- Confirm the original creditor and account history: This step helps ensure the debt truly belongs to you and has not been incorrectly assigned or duplicated.

- Check that the reported balance is correct: Compare the amount requested with your previous records, statements, or payment history.

Verifying the account protects you from paying incorrect debts and ensures you address the correct financial obligation.

Step 3: Resolve the Collection Account

Once the account has been verified, resolving the balance can help prevent further damage and may support gradual credit recovery.

- Pay the balance in full if possible: Paying the account closes the collection and prevents additional recovery activity.

- Discuss repayment plans if full payment is difficult: Many agencies allow structured payment arrangements that spread the balance across manageable installments.

- Request written confirmation of the resolution: Documentation ensures that the account status is updated correctly and protects you if reporting issues arise later.

Although paying a collection does not instantly erase its credit impact, it can prevent further damage and allow the recovery process to begin.

Step 4: Ask About Pay-for-Delete or Updated Reporting

In some cases, resolving a collection account may also allow you to request updated credit reporting.

- Ask whether the agency offers pay-for-delete arrangements: Some collectors may agree to remove the collection entry from your credit report after payment, though this practice is not guaranteed.

- Request updated reporting showing a zero balance: Even if the collection remains on your report, an updated status showing the debt is paid can be viewed more favorably by lenders.

- Always obtain any reporting agreement in writing: Written confirmation helps ensure the change is properly reflected in your credit report.

While not always available, these reporting updates can sometimes accelerate the credit rebuilding process.

Step 5: Bring All Other Accounts Current

Rebuilding credit is not only about resolving past debts but also preventing new negative entries.

- Bring any delinquent accounts up to date: Addressing overdue payments quickly helps stop additional damage to your credit history.

- Stabilize your active credit accounts: Consistent payments signal to lenders that your financial situation has improved.

- Focus on maintaining positive activity moving forward: Avoiding new late payments is one of the most effective ways to rebuild credit.

Credit recovery begins when new financial behavior replaces past mistakes.

Step 6: Start Building Positive Credit Activity

Once existing issues are addressed, establishing new positive credit behavior becomes essential.

- Consider a secured credit card: These cards require a deposit but report payment activity to credit bureaus, helping rebuild credit history.

- Explore credit-builder loans offered by some financial institutions: These loans are designed specifically to help consumers establish consistent payment history.

- Use small, controlled balances: Charging modest amounts and paying them off regularly demonstrates responsible credit use.

Positive activity gradually strengthens your credit profile and reduces the relative impact of older collection accounts.

Step 7: Keep Credit Utilization Low

Credit utilization measures how much of your available credit you are currently using.

- Maintain low balances on revolving accounts: Financial experts often recommend keeping credit usage below about 30 percent of your available limit.

- Avoid carrying high balances across billing cycles: High utilization can signal financial risk to lenders.

- Make payments throughout the month if necessary: Regular payments can help keep your reported balance low.

Managing utilization carefully can lead to noticeable credit score improvements over time.

Step 8: Pay Every Bill On Time

Payment history is the most influential factor in most credit scoring models.

- Make every payment before the due date: Even a single late payment can temporarily slow your credit recovery.

- Use automatic payments for essential accounts: Automation reduces the risk of missing due dates during busy periods.

- Track payment dates with reminders or calendars: Staying organized helps maintain consistent financial behavior.

A strong pattern of on-time payments gradually rebuilds lender confidence in your credit reliability.

Step 9: Avoid Applying for Too Much New Credit

Opening several new credit accounts at once can create additional risk signals.

- Limit unnecessary credit applications: Each application can result in a hard inquiry, which may slightly affect your credit score.

- Allow time for existing accounts to build history: A stable credit profile often improves more steadily than one with frequent new applications.

- Focus on maintaining responsible credit usage rather than expanding credit quickly.

Patience and stability often lead to stronger long-term credit improvement.

Step 10: Monitor Your Credit Progress

Rebuilding credit is a gradual process, so tracking progress helps you stay informed and motivated.

- Review your credit reports regularly: Monitoring allows you to see when balances change or accounts update their status.

- Track improvements in your credit score: Even modest increases indicate that your positive habits are having an effect.

- Dispute any new reporting errors quickly: Correcting inaccuracies helps protect the progress you have made.

Over time, consistent payments, responsible credit use, and resolved collection accounts can gradually strengthen your credit profile and restore financial opportunities.

Also read: Understanding Portfolio Recovery Associates and Debt Collection

Mistakes That Can Slow Down Credit Recovery

Rebuilding credit after collections requires patience and consistency. While many people focus on the steps needed to improve their credit, certain financial habits can unintentionally slow down the recovery process. Avoiding these common mistakes can help ensure that your efforts to rebuild credit produce steady results.

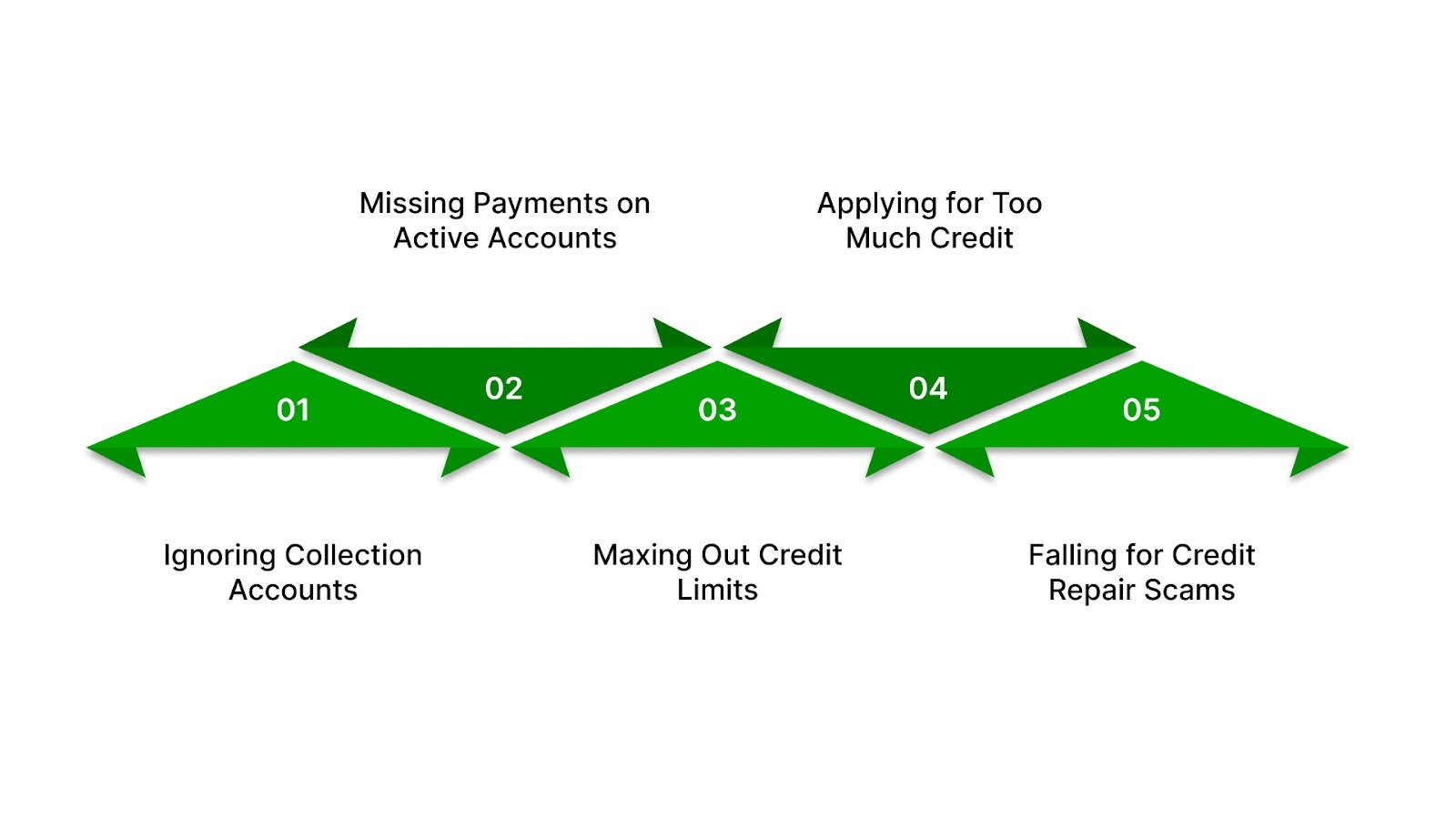

Ignoring Collection Accounts Completely

Some people avoid communication with collection agencies because the situation feels stressful or uncertain.

However, ignoring a collection account does not make it disappear. Unresolved accounts can continue affecting your credit report and may lead to additional collection activity. Reviewing the account details and discussing repayment options can often bring greater clarity and help move the situation toward resolution.

Continuing to Miss Payments on Active Accounts

When rebuilding credit, preventing new negative marks is just as important as resolving older ones. Missing payments on credit cards, loans, or other obligations can add fresh late-payment entries to your credit report, extending the time required for recovery. Consistently paying every bill on time helps establish positive financial behavior that gradually improves your credit profile.

Maxing Out Available Credit Limits

High credit utilization can negatively affect your credit score, even if payments are made on time. Using most or all of your available credit limit may signal financial strain to lenders. Maintaining lower balances and making regular payments helps demonstrate responsible credit use and supports credit improvement over time.

Applying for Too Many Credit Accounts at Once

Opening several new credit accounts within a short period can create multiple hard inquiries on your credit report. While occasional credit applications are normal, frequent applications may indicate higher financial risk. Limiting new credit requests allows your existing accounts to build a stable payment history.

Falling for Credit Repair Scams

Some companies promise to remove collections instantly or guarantee major credit score increases. In reality, legitimate credit recovery takes time and consistent financial behavior. Regulatory agencies such as the Federal Trade Commission warn consumers to be cautious of services that demand large upfront fees or make unrealistic promises about credit repair.

Closing Old Credit Accounts Too Quickly

In some cases, people close older credit accounts once balances are paid off. However, long-standing accounts can contribute positively to your credit history by demonstrating a longer record of credit use. Keeping older accounts open with low balances may support your credit profile, provided they are managed responsibly.

Avoiding these mistakes allows your positive financial management habits to have a stronger impact on your credit recovery. Over time, consistent payments, responsible credit usage, and resolved accounts can gradually rebuild your credit standing.

Final Thoughts

A collection account can feel like a setback, but it does not have to define your financial path. The most important step is moving forward with clarity. Understanding your accounts, communicating about repayment options, and maintaining organized records can make the rebuilding process far more manageable.

If you are dealing with collection accounts and want a clearer path toward resolution, The Forest Hill Management can help. Their team focuses on providing transparent account information, secure payment options, and structured repayment arrangements designed to support consumers working toward financial recovery.

Contact The Forest Hill Management today to review your account details and explore practical steps that can help you move forward with greater confidence.

FAQs

1. Can a collection account be removed from a credit report early?

In some cases, a collection agency may agree to update or remove an entry after the debt is resolved, but this is not guaranteed. If you believe a collection account is inaccurate or improperly reported, you can file a dispute with the credit bureaus for investigation.

2. How soon can credit scores start improving after resolving collections?

Credit scores may begin improving within a few months if positive financial behavior is established, such as making consistent payments and maintaining low credit balances. However, meaningful improvement typically develops gradually over time.

3. Will lenders still approve credit applications after collections?

Some lenders may still approve applications, especially if your recent financial behavior shows improvement. Factors such as income stability, payment history, and reduced outstanding debt can influence lending decisions.

4. Is it better to resolve a collection account immediately or gradually?

Resolving a collection account as soon as financially possible can prevent additional collection activity and help you move forward with rebuilding credit. However, structured repayment plans may be helpful if immediate full payment is not realistic.

5. Can rebuilding credit after collections improve financial opportunities in the future?

Yes. As your credit history strengthens through responsible financial behavior, you may gain access to better credit products, improved interest rates, and broader financial opportunities over time.